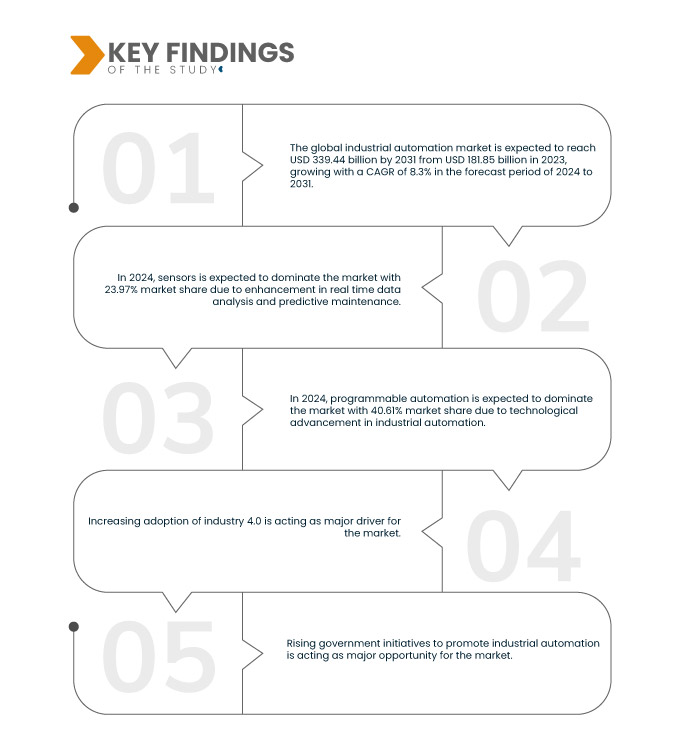

Растущее внедрение принципов Индустрии 4.0 служит важной движущей силой мирового рынка промышленной автоматизации. Индустрия 4.0, также признанная четвертой промышленной революцией, подчеркивает интеграцию цифровых технологий с традиционными производственными процессами для повышения эффективности, производительности и гибкости. Одной из ключевых составляющих Индустрии 4.0 является внедрение передовых решений по автоматизации, таких как робототехника, передовые датчикии облачные вычисления в различных отраслях. Эти технологии обеспечивают бесперебойную связь и сотрудничество между машинами, системами и людьми, что приводит к оптимизации операций и улучшению процессов принятия решений.

Доступ к полному отчету @https://www.databridgemarketresearch.com/reports/global-industrial-automation-market

Исследование рынка Data Bridge показывает, что Мировой рынок промышленной автоматизации ожидается, что к 2031 году объем достигнет 339,44 млрд долларов США со 181,85 млрд долларов США в 2023 году, а среднегодовой темп роста составит 8,3% в течение прогнозируемого периода с 2024 по 2031 год.

Ключевые результаты исследования

Растущий спрос на автоматизацию для надежного и эффективного производства

Глобальная промышленная автоматизация Рынок переживает значительный всплеск спроса, вызванный, прежде всего, необходимостью в надежных и эффективных производственных процессах. Технологии автоматизации становятся все более сложными, предлагая производителям возможность оптимизировать операции, повысить производительность и снизить затраты. Одним из ключевых движущих факторов этой тенденции является растущий спрос на решения по автоматизации, которые могут решить проблемы современного производства, такие как потребность в точности, гибкости и масштабируемости.

В сегодняшней высококонкурентной бизнес-среде производители вынуждены повышать свою эффективность и производительность, сохраняя при этом высокие стандарты качества. Технологии автоматизации предлагают решение, автоматизируя повторяющиеся задачи, оптимизируя рабочие процессы и сводя к минимуму риск ошибок. Это не только приводит к увеличению производительности и повышению качества продукции, но также позволяет компаниям более эффективно распределять ресурсы, что приводит к экономии затрат и повышению прибыльности.

Объем отчета и сегментация рынка

|

Отчет по метрике

|

Подробности

|

|

Прогнозный период

|

2024–2031 гг.

|

|

Базисный год

|

2023 год

|

|

Исторические годы

|

2022 г. (настраивается на 2016–2021 гг.)

|

|

Количественные единицы

|

Выручка в миллиардах долларов США

|

|

Охваченные сегменты

|

Компоненты (датчики, промышленные роботы, промышленные ПК, машинное зрение, промышленная 3D-печать, человеко-машинный интерфейс (HMI), полевые приборы, регулирующие клапаны и другие), режимы автоматизации (полуавтоматические и полностью автоматические), системы ( ПИД, управление на основе моделей и другие), решение (программируемый логический контроллер (ПЛК), распределенная система управления (DCS), диспетчерское управление и сбор данных (SCADA), средства управления на уровне предприятия, программируемое автоматическое управление (PAC), управление активами предприятия ( PAM), цифровизация, функциональная безопасность, контроль выбросов, тип (программируемая автоматизация, фиксированная или аппаратная автоматизация, интегрированная автоматизация и гибкая или мягкая автоматизация), конечный пользователь (перерабатывающие и дискретные отрасли)

|

|

Охваченные страны

|

США, Канада, Мексика, Германия, Франция, Великобритания, Нидерланды, Швейцария, Бельгия, Россия, Италия, Испания, Швеция, Дания, Польша, Норвегия, Финляндия, Турция, Остальная Европа, Китай, Япония, Индия, Южная Корея, Сингапур , Малайзия, Австралия, Таиланд, Индонезия, Филиппины, Новая Зеландия, Тайвань, Вьетнам, остальные страны Азиатско-Тихоокеанского региона, Саудовская Аравия, ОАЭ, Южная Африка, Египет, Израиль, Катар, Бахрейн, Кувейт, Оман, остальные страны Ближнего Востока и Африки. , Бразилия, Аргентина и остальная часть Южной Америки

|

|

Охваченные игроки рынка

|

Siemens (Германия), Analog Devices, Inc. (США), Schneider Electric (Франция), General Electric Company (США), Mitsubishi Electric Corporation (Япония), FANUC America Corporation (США), Honeywell International Inc. (США), AMETEK Inc. (США), ABB (Швейцария), KEYENCE CORPORATION (Япония), Hitachi Vantara LLC (США), Rockwell Automation (США), Emerson Electric Co (США), Yokogawa Electric Corporation (Япония), Delta Electronics, Inc. ( Тайвань), Fuji Electric Co., Ltd. (Япония), Endress+Hauser Group Services AG (Швейцария), OMRON Corporation (Япония), KUKA AG (Германия), Bosch Rexroth Corporation (Германия), Concept Systems (США) и MachineMetrics (США) и другие

|

|

Точки данных, включенные в отчет

|

В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географический охват и основные игроки, рыночные отчеты, подготовленные Data Bridge Market Research, также включают углубленный экспертный анализ, географически представленное производство по компаниям и мощность, схема сети дистрибьюторов и партнеров, подробный и обновленный анализ ценовых тенденций и анализ дефицита цепочки поставок и спроса.

|

Сегментный анализ

Мировой рынок промышленной автоматизации разделен на шесть заметных сегментов, которые основаны на компонентах, способах автоматизации, системах, решениях, типах и конечных пользователях.

- В зависимости от компонентов мировой рынок промышленной автоматизации сегментирован на датчики, промышленных роботов, промышленные ПК, машинное зрение, промышленную 3D-печать, человеко-машинный интерфейс (HMI), полевые приборы, регулирующие клапаны и другие.

В 2024 году датчики Ожидается, что этот сегмент будет доминировать на мировом рынке промышленной автоматизации.

Ожидается, что в 2024 году сегмент датчиков будет доминировать на мировом рынке промышленной автоматизации с долей рынка 23,97% из-за растущего спроса на автоматизацию для надежного и эффективного производства.

- В зависимости от способа автоматизации мировой рынок промышленной автоматизации подразделяется на полуавтоматические и полностью автоматизированные. Ожидается, что в 2024 году сегмент полуавтоматизации будет доминировать на рынке с долей рынка 64,06%.

- В зависимости от систем мировой рынок промышленной автоматизации сегментирован на ПИД-регулирование, управление на основе моделей и другие. Ожидается, что в 2024 году сегмент PID будет доминировать на рынке с долей рынка 72,56%.

- В зависимости от решения мировой рынок промышленной автоматизации сегментируется на программируемый логический контроллер (ПЛК), распределенную систему управления (DCS), диспетчерское управление и сбор данных (SCADA), средства управления уровня предприятия, программируемое управление автоматизацией (PAC), активы предприятия. Управление (ПАМ), цифровизация, функциональная безопасность и контроль выбросов. Ожидается, что в 2024 году сегмент программируемых логических контроллеров (ПЛК) будет доминировать на рынке с долей рынка 27,92%.

- В зависимости от типа мировой рынок промышленной автоматизации сегментируется на программируемую автоматизацию, фиксированную или аппаратную автоматизацию, интегрированную автоматизацию и гибкую или мягкую автоматизацию.

Ожидается, что в 2024 году сегмент программируемой автоматизации будет доминировать на мировом рынке промышленной автоматизации.

Ожидается, что в 2024 году сегмент программируемой автоматизации будет доминировать на рынке с долей рынка 40,61% благодаря технологическому прогрессу в области промышленной автоматизации.

- В зависимости от конечного пользователя мировой рынок промышленной автоматизации сегментирован на перерабатывающие и дискретные отрасли. Ожидается, что в 2024 году сегмент перерабатывающей промышленности будет доминировать на рынке с долей рынка 71,28%.

Основные игроки

Исследование рынка мостов данных анализирует Siemens (Германия), Schneider Electric (Франция), General Electric (США), FANUC America Corporation (США), Mitsubishi Electric Corporation (Япония) как основных игроков, работающих на мировом рынке промышленной автоматизации.

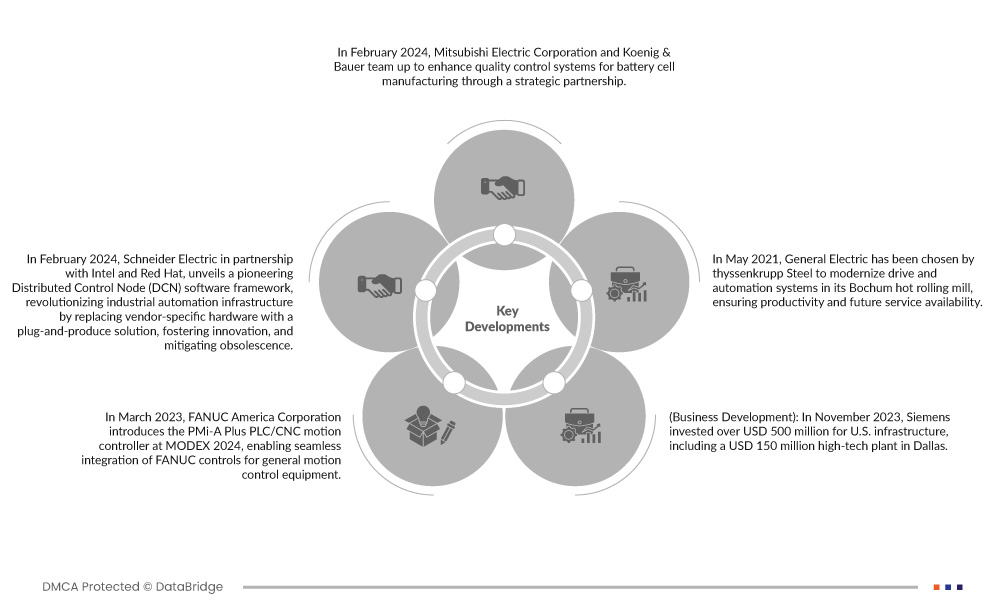

Развитие рынка

- В феврале 2024 года Mitsubishi Electric Corporation и Koenig & Bauer объединяются для совершенствования систем контроля качества при производстве аккумуляторных элементов в рамках стратегического партнерства. Используя опыт Mitsubishi Electric в странах СНГ и линейные системы машинного зрения Koenig & Bauer, сотрудничество направлено на оптимизацию производства электродной фольги для повышения эффективности и надежности производства аккумуляторов.

- В феврале 2024 года Schneider Electric в партнерстве с Intel и Red Hat представляет новаторскую программную среду распределенного узла управления (DCN), которая революционизирует инфраструктуру промышленной автоматизации за счет замены аппаратного обеспечения конкретного поставщика на решение «подключи и работай», способствуя инновациям и снижая риски. устаревание. Эти совместные усилия воплощают в себе дальновидное видение, согласующееся с целями Открытого форума по автоматизации процессов: предоставить промышленным предприятиям возможность использовать совместимые портативные технологии, формируя будущее промышленных систем управления.

- В марте 2023 года корпорация FANUC America представляет на выставке MODEX 2024 контроллер движения PMi-A Plus PLC/CNC, обеспечивающий плавную интеграцию элементов управления FANUC для общего оборудования управления движением. Эта демонстрация демонстрирует синергию между линиями автоматизации производства FANUC и коботами, предлагая комплексное автоматизированное складское решение для отрасли цепочки поставок.

- В ноябре 2023 года Siemens инвестировала более 500 миллионов долларов США в инфраструктуру США, включая высокотехнологичный завод в Далласе стоимостью 150 миллионов долларов США. Инвестиции поддержат американскую центры обработки данных и критически важная инфраструктура, удовлетворяя растущий спрос, вызванный внедрением генеративного искусственного интеллекта. Роланд Буш, генеральный директор Siemens AG, подчеркивает важность этого шага для поддержки экономики и прогресса в декарбонизации.

- В мае 2021 года компания Thyssenkrupp Steel выбрала General Electric для модернизации систем привода и автоматизации на своем стане горячей прокатки в Бохуме, чтобы обеспечить производительность и доступность услуг в будущем. Поскольку проект охватывает три этапа, включая замену приводных преобразователей и систем управления, модернизация повысит эффективность и сведет к минимуму время простоя, что имеет решающее значение для поддержания целостности производства и сокращения задержек.

Региональный анализ

Географически в отчет о мировом рынке промышленной автоматизации включены следующие страны: США, Канада, Мексика, Германия, Франция, Великобритания, Нидерланды, Швейцария, Бельгия, Россия, Италия, Испания, Швеция, Дания, Польша, Норвегия, Финляндия, Турция, остальные страны. Европы, Китая, Японии, Индии, Южной Кореи, Сингапура, Малайзии, Австралии, Таиланда, Индонезии, Филиппин, Новой Зеландии, Тайваня, Вьетнама, остальных стран Азиатско-Тихоокеанского региона, Саудовской Аравии, ОАЭ, Южной Африки, Египта, Израиля, Катара. , Бахрейн, Кувейт, Оман, остальные страны Ближнего Востока и Африки, Бразилия, Аргентина и остальная часть Южной Америки.

Согласно анализу исследования рынка Data Bridge:

Ожидается, что Азиатско-Тихоокеанский регион станет доминирующим и наиболее быстрорастущим регионом на мировом рынке промышленной автоматизации.

Ожидается, что Азиатско-Тихоокеанский регион станет доминирующим и наиболее быстрорастущим регионом в мире. рынок промышленной автоматизации благодаря быстро расширяющемуся производственному сектору, технологическим достижениям и растущему внедрению решений по автоматизации. Это доминирование еще более усиливается правительственными инициативами, продвигающими Индустрию 4.0, создавая благоприятную среду для внедрения автоматизации в различных секторах, укрепляя позиции Азиатско-Тихоокеанского региона как ключевого игрока на глобальном рынке промышленной автоматизации.

Для получения более подробной информации о мировом рынке промышленной автоматизации отчет, нажмите здесь –https://www.databridgemarketresearch.com/reports/global-industrial-automation-market