Circumvent the Tariff challenges with an agile supply chain Consulting

Supply Chain Ecosystem Analysis now part of DBMR Reports

Global Shared Mobility Market

Market Size in USD Billion

CAGR :

%

USD

6.18 Billion

USD

52.50 Billion

2024

2032

Forecast Period

2025 –2032

Market Size(Base Year)

USD

6.18 Billion

Market Size (Forecast Year)

USD

52.50 Billion

CAGR

%

Major Markets Players

Avis budget group

car2go NALLC

Beijing Xiaoju Technology CoLtd.

Mobiag

movmi Shared Transportation Services Inc.

Global Shared Mobility Market Segmentation, By Service Model (Ride Hailing, Bike Sharing, Ride Sharing, Car Sharing, and Others), Vehicle Type (Cars, Two-Wheelers, and Others), Business Model (Peer-To-Peer (P2P), Business-To-Business (B2B), and Business-To-Consumer (B2C)), Sector Type (Unorganized and Organized), Autonomy Level (Manual, Autonomous, and Semi-Autonomous), Power Source (Fuel Powered and Hybrid Electric Vehicle (HEV), Plug-in Hybrid Electric Vehicle (PHEV), and Battery Electric Vehicle (BEV)) - Industry Trends and Forecast to 2032

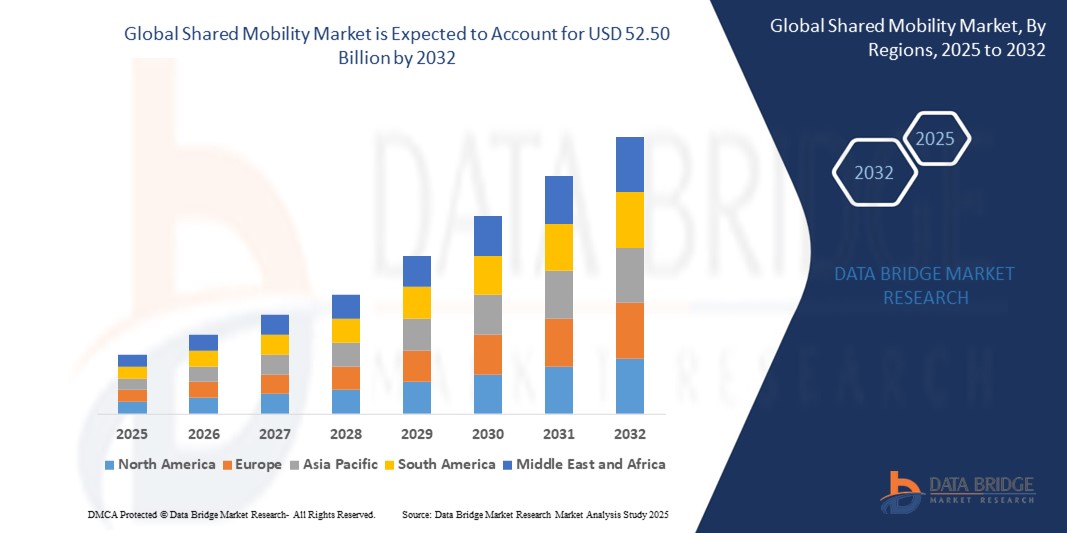

Global Shared Mobility Market Size

The global shared mobility market was valued at USD 6.18 billion in 2024 and is expected to reach USD 52.50 billion by 2032

During the forecast period of 2025 to 2032, the global Shared Mobility market is likely to grow at a CAGR of 31.70%, primarily driven by the rising demand for cost-effective and sustainable urban transportation solutions.

This growth is fueled by factors such as increasing urbanization, rising traffic congestion, growing environmental concerns, advancements in mobile and GPS technologies, and supportive government initiatives promoting shared and green mobility options.

Global Shared Mobility Market Analysis

The shared mobility market has experienced significant growth, driven by advancements in technology and shifting consumer preferences towards sustainable transportation options. Key developments in this sector include the integration of electric vehicles (EVs) and autonomous driving technology, enhancing the appeal and efficiency of shared mobility solutions

Major players such as Uber and Lyft are expanding their service offerings to include bike and scooter sharing, while companies such as Zipcar and car2go are evolving their car-sharing models to cater to urban populations seeking flexibility and convenience

Asia-Pacific leads the shared mobility market in revenue growth with market share 39.51% due to the rising costs associated with vehicle ownership and the growing traffic congestion in countries such as India and China. High urbanization rates and the push for sustainable transportation solutions have further fueled the adoption of shared mobility services across the region.

For instance, In September 2023, Kellogg Company took a significant step by officially gaining approval from its Board of Directors for the planned separation into two distinct publicly traded companies, Kellanova and WK Kellogg Co. With separate entities focusing on distinct product categories optimized the supply chains. Each entity tailored its own logistics strategies to the specific needs of its products, leading to more efficient transportation routes, inventory management, and distribution networks

Globally, Shared Mobility services are recognized as a sustainable and cost-effective transportation solution that reduces traffic congestion, lowers carbon emissions, and optimizes vehicle utilization through models like car-sharing, ride-hailing, bike-sharing, and scooter-sharing, especially in urban environments.

Report Scope and Shared Mobility Market Segmentation

Attributes

Shared Mobility Key Market Insights

Segments Covered

By Service Model: Ride Hailing, Bike Sharing, Ride Sharing, Car Sharing, and Others

By Vehicle Type: Heating and Plumbing, HVAC, Refrigeration, Industrial Processes, and Acoustic

By Business Model: Peer-To-Peer (P2P), Business-To-Business (B2B), and Business-To-Consumer (B2C)

By Sector Type: Unorganized and Organized

By Autonomy Level Manual, Autonomous, and Semi-Autonomous:

By Power Source: Fuel Powered and Hybrid Electric Vehicle (HEV), Plug-in Hybrid Electric Vehicle (PHEV), and Battery Electric Vehicle (BEV)

Countries Covered

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Netherlands

Switzerland

Belgium

Russia

Italy

Spain

Turkey

Rest of Europe

Asia-Pacific

China

Japan

India

South Korea

Singapore

Malaysia

Australia

Thailand

Indonesia

Philippines

Rest of Asia-Pacific

Middle East and Africa

Saudi Arabia

U.A.E.

South Africa

Egypt

Israel

Rest of Middle East and Africa

South America

Brazil

Argentina

Rest of South America

Key Market Players

Avis Budget Group (U.S.)

Daimler Truck North America LLC (U.S.)

DiDi Global Inc (China)

Mobiag (Portugal)

Movmi LLC (Canada)

Uber Technologies Inc. (U.S.)

Ola Electric Mobility Pvt Ltd (India)

Lyft, Inc. (U.S.)

Careem (U.A.E.)

Bolt Technology OÜ (Estonia)

Gett (U.K.)

The Hertz Corporation (U.S.)

Aptiv (Ireland)

Enterprise Holdings Inc. (U.S.)

MOBIKO (Germany)

Europcar (France)

Curb Mobility, LLC (U.S.)

BlaBlaCar (France)

Wingz (U.S.)

Market Opportunities

Growing Technological Advancements

Increasing Government Support and Funding

Value Added Data Infosets

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

Shared Mobility Market Trends

“Urbanization and Digital Innovation Reshape Shared Mobility Landscape”

The rapid pace of urbanization and evolving consumer preferences are accelerating demand for convenient, cost-effective, and eco-friendly mobility solutions, fueling the growth of shared mobility services globally.

Commuters now seek seamless, integrated mobility options through apps that combine ride-hailing, carpooling, bike-sharing, e-scooters, and public transit.

For instance, On March 20, 2025, Blue Dart and Delhi Metro Rail Corporation (DMRC) launched a first-of-its-kind urban freight service in South Asia Pacific. Cargo will be transported via metro trains during non-peak hours, easing road congestion and reducing emissions. The initiative supports sustainable logistics while optimizing metro capacity. DMRC is also engaging with Madrid Metro to share best practices in eco-friendly urban freight transport. .

Technology adoption—like AI-based demand prediction, real-time fleet tracking, and digital payment solutions—has enhanced the accessibility and scalability of shared mobility platforms.

Additionally, sustainability goals are pushing providers to adopt electric vehicles, carbon-neutral operations, and shared ride incentives to reduce emissions and road congestion.

Global Shared Mobility Market Dynamics

Driver

“Rapid Urbanization and Increasing Population”

Urbanization serves as a crucial market driver for shared mobility, with the global urban population projected to reach approximately 5 billion by 2030, according to the United Nations.

This rapid growth in urban areas intensifies the demand for efficient and accessible transportation solutions to accommodate the increasing number of residents.

Shared mobility services, such as ride-hailing and car-sharing, provide a practical alternative for city dwellers who often encounter high costs associated with vehicle ownership, including maintenance, insurance, and parking fees. For instance, a study found that car-sharing services can reduce the number of vehicles on the road by as much as 10% in densely populated areas.

For instance,

On August 8, 2024, rising urbanization and congestion are driving cities to adopt sustainable, integrated transport solutions like Mobility-as-a-Service (MaaS). Growth opportunities include regulatory support for green mobility, strategic partnerships for shared mobility innovations, and integration of autonomous technologies. Cities are redesigning transport frameworks, leveraging data sharing, and embracing tech-driven solutions to enhance urban connectivity, reduce emissions, and meet evolving mobility demands while fostering smarter, more efficient transit ecosystems.

As cities continue to expand, shared mobility solutions will play a pivotal role in addressing the transportation needs of growing populations, solidifying their position as a key driver in the shared mobility market.

Opportunity

“Growing Technological Advancements”

Technological advancements represent a crucial market opportunity for shared mobility services, particularly through the integration of artificial intelligence (AI), machine learning, and the Internet of Things (IoT).

These innovations can significantly enhance operational efficiency and elevate the user experience. For instance, AI algorithms can analyze vast datasets to optimize route planning, leading to quicker and more cost-effective journeys while minimizing fuel consumption.

In addition, IoT devices installed in vehicles provide real-time data on vehicle performance, enabling proactive maintenance and reducing downtime. This ensures vehicle reliability and enhances customer satisfaction.

For instance,

On March 18, 2025, Trackon announced plans to onboard over 750 new franchise partners in South India to boost last-mile delivery and meet rising logistics demand in states like Tamil Nadu and Karnataka. With over 6,500 franchises and ₹500+ crore turnover, the company aims to add 1,500 franchises this year, strengthening its presence in urban and rural areas.

Shared mobility providers can develop personalized services based on user preferences, offering customized ride options or tailored promotions that resonate with individual users. By leveraging these technologies, companies can streamline operations and offer superior services, positioning themselves to capture a larger share of the market.

Restraint/Challenge

“Safety and Security Concerns”

Safety and security concerns significantly impact the shared mobility market, as issues such as accidents and criminal activity can deter potential users from utilizing these services.

Ensuring the safety of both passengers and drivers is paramount, as any incidents can lead to negative perceptions and a subsequent decline in demand. For instance, in 2019, a highly publicized incident involving a ride-hailing driver in the U.S. who was implicated in a series of assaults sparked widespread fear and skepticism regarding the safety of ride-hailing services.

Following this event, companies such as Uber and Lyft implemented enhanced safety measures, such as background checks, in-app emergency features, and driver training programs, to rebuild consumer trust.

For instance,

On April 14, 2025, shared mobility services like e-scooters, bikes, and ride-hailing apps flourish in major cities, yet remain largely inaccessible to low-income, elderly, or disabled individuals. These services often cater to affluent, able-bodied users, limiting inclusivity. Experts emphasize that for shared mobility to be sustainable and impactful, it must replace private car use and serve all demographics, with initiatives underway to bridge access gaps and promote equity in urban mobility.

However, despite these efforts, safety concerns remain a barrier to entry for many potential users, particularly among demographics such as women and older adults, who may feel more vulnerable using shared mobility services. As a result, hampering overall market growth.

Shared Mobility Market Scope

The market is segmented on the basis product type, and applications.

Segmentation

Sub-Segmentation

By Service Model

Ride Hailing

Bike Sharing

Ride Sharing

Car Sharing

Others

By Vehicle Type

Cars

Two-Wheelers

Others

By Business Model

Peer-To-Peer (P2P)

Business-To-Business (B2B)

Business-To-Consumer (B2C)

By Sector Type

Unorganized

Organized

By Autonomy Level

Manual

Autonomous

Semi-Autonomous

By Power Source

Fuel Powered

Hybrid Electric Vehicle (HEV)

Plug-in Hybrid Electric Vehicle (PHEV)

Battery Electric Vehicle (BEV)

Shared Mobility Market Regional Analysis

“Asia-Pacific is the Dominant Region in the Shared Mobility Market”

Asia-Pacific dominates and is the fastest growing region in the global Shared Mobility market with the market share 39.51% due to rapid urbanization, high population density, increasing smartphone penetration, and strong government support for sustainable transport alternatives.

The region is home to several leading shared mobility providers and tech startups offering ride-hailing, bike-sharing, and carpooling services, particularly in countries like China, India, and Indonesia, which are driving market expansion.

The rise of app-based mobility platforms, growing environmental awareness, and integration of electric vehicles into shared fleets are accelerating adoption across urban centers.

In addition, the region's strong economic growth, expanding middle-class population, and demand for affordable, convenient transportation further reinforce its leadership in the global Shared Mobility industry.

“Europe is Projected to Register the Highest Growth Rate”

The Europe region is projected to register the highest growth rate in the Shared Mobility market with the market share 27.67%, driven by increasing environmental consciousness, widespread urban mobility initiatives, and strong regulatory support for reducing vehicle emissions and congestion.

Government initiatives promoting sustainable transport, expansion of low-emission zones, and investments in public-private mobility partnerships have further fueled market expansion across key European cities.

Additionally, the rapid integration of digital technologies—such as AI for demand prediction, blockchain for transparent ride transactions, and IoT-enabled fleet tracking—has significantly enhanced service reliability and user experience.

Germany dominates the market share in Europe due to its strong automotive industry, advanced urban infrastructure, and early adoption of shared mobility solutions. The country’s commitment to reducing carbon emissions, combined with widespread use of mobility-as-a-service (MaaS) platforms and government support for electric and sustainable transport, continues to drive its leadership in the European Shared Mobility market.

Shared Mobility Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

Avis Budget Group (U.S.)

Daimler Truck North America LLC (U.S.)

DiDi Global Inc (China)

Mobiag (Portugal)

Movmi LLC (Canada)

Uber Technologies Inc. (U.S.)

Ola Electric Mobility Pvt Ltd (India)

Lyft, Inc. (U.S.)

Careem (U.A.E)

Bolt Technology OÜ (Estonia)

Gett (U.K.)

The Hertz Corporation (U.S.)

Aptiv (Ireland)

Enterprise Holdings Inc. (U.S.)

MOBIKO (Germany)

Europcar (France)

Curb Mobility, LLC (U.S.)

BlaBlaCar (France)

Wingz (U.S.)

Latest Developments in Global Shared Mobility Market

In February 2025, according to the news published by Frost & Sullivan, India’s shared mobility market is accelerating due to urban congestion, EV adoption, and digital innovation. Segments like ride-sharing, bike taxis, car subscriptions, and auto-rickshaw aggregation are rapidly expanding. Companies such as BluSmart and Zoomcar are leveraging sustainable models and tech-driven services, while government support and shifting consumer preferences open doors for strategic growth across tier 1, 2, and 3 cities.

In November 2023, Italy’s shared mobility market grew 38% in 2022, reaching USD180 million in revenue. Italians made 49 million trips covering 200 million kilometers, with micromobility (bikes, scooters, mopeds) accounting for 87% of use. Rome introduced new fleet requirements and selected Bird, Dott, and Lime to operate 9,000 scooters. Despite wider access, profitability concerns arise due to suburban deployment. Scooter accidents also declined, reflecting improved micromobility safety.

In April 2025 Lyft, Inc. announced its acquisition of FreeNow, a leading European multi-mobility app, for €175 million ($197 million) in cash from BMW Group and Mercedes-Benz Mobility. The deal, expected to close in late 2025, expands Lyft into 9 European countries, doubling its addressable market to 300 billion trips annually. FreeNow will retain its team and operations, supporting Lyft’s global growth and diversification strategy.

In July 2023, Grab announced its acquisition of Singapore-based taxi operator Trans-cab. This deal includes Trans-cab’s maintenance workshop, fuel pump services, and car rental operations, along with the launch of the Grab Driver app, which will be integrated into mobile display units within Trans-cab taxis

In March 2023, Zipcar, Inc. advanced its carshare program in New York City, introducing services in Kew Gardens Hills (Queens), West Village (Manhattan), and Bedford Park (Bronx), expanding its presence across key neighborhoods

In March 2022, Lyft teamed up with Spin to integrate Spin scooters into the Lyft app across 60 U.S. markets. This collaboration aims to streamline access to multiple mobility options, including car-sharing, through a single platform. By adding Spin scooters, Lyft is expanding its range of transportation solutions, making it more convenient for users to choose from various options within the app

In January 2022, The Toro Company, a leader in innovative outdoor solutions, acquired The Intimidator Group Inc., a U.S.-based manufacturer of side-by-side vehicles. This acquisition is part of Toro’s strategy to strengthen its presence in the zero-turn mower market and establish itself as a key player in the global market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

Interactive Data Analysis Dashboard

Company Analysis Dashboard for high growth potential opportunities

Research Analyst Access for customization & queries

Competitor Analysis with Interactive dashboard

Latest News, Updates & Trend analysis

Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.

Claudio Rondena

Group Business Development & Strategic Marketing Director, C.O.C Farmaceutici SRL

"This morning we were involved in the first part, the data presentation of MKT analysis, selected abstract from your work. The board team was really impressed and very appreciated, as well."

David Manning - Thermo Fisher Scientific

Director, Global Strategic Accounts,

Dear Ricky, I want to thank you for the excellent market analysis (LIMS INSTALLED BASE DATA) that you and your team delivered, especially end of year on short notice.

Sachin and Shraddha captured the requirements, determined their path forward and executed quickly.

You, Sachin and Shraddha have been a pleasure to work with – very responsive, professional and thorough.

Your work is much appreciated.

Manager - Market Analytics,

Uriah D. Avila - Zeus Polymer Solutions

Thank you for all the assistance and the level of detail in the market report. We are very pleased with the results and the customization. We would like to continue to do business.

Business Development Manager,

(Pharmaceuticals Partner for Nasal Sprays) | Renaissance Lakewood LLC

DBMR was attentive and engaged while discussing the Global Nasal Spray Market. They understood what we were looking for and was able to provide some examples from the report as requested. DBMR Service team has been responsive as needed. Depending on what my colleagues were looking for, I will recommend your services and would be happy to stay connected in case we can utilize your research in the future.

Business Intelligence and Analytics,

Ipsen Biopharm Limited

We are impressed by the CENTRAL PRECOCIOUS PUBERTY (CPP) TREATMENT report - so a BIG thanks to you colleagues.

Competition Analyst,

Basler Web

I just wanted to share a quick note and let you know that you guys did a really good job. I’m glad I decided to work with you. I shall continue being associated with your company as long as we have market intelligence needs.

Marketing Director,

Buhler Group

It was indeed a good experience, would definitely recommend and come back for future prospects.

COO,

A global leader providing Drug Delivery Services

DBMR did an outstanding job on the Global Drug Delivery project, We were extremely impressed by the simple but comprehensive presentation of the study and the quality of work done. This report really helped us to access untapped opportunities across the globe.

Marketing Director,

Philips Healthcare

The study was customized to our targets and needs with well-defined milestones. We were impressed by the in-depth customization and inclusion of not only major but also minor players across the globe. The DBMR Market position grid helped us to analyze the market in different dimension which was very helpful for the team to get into the minute details.

Product manager,

Fujifilms

Thankful to the team for the amazing coordination, and helping me at the last moment with my presentation. It was indeed a comprehensive report that gave us revenue impacting solution enabling us to plan the right move.

Investor relations,

GE Healthcare

Thank you for the report, and addressing our needs in such short time. DBMR has outdone themselves in this project with such short timeframe.

Market Analyst,

Medincell

We found the results of this study compelling and will help our organization validate a market we are considering to enter. Thank you for a job well done.

Andrew - Senior Global Marketing Manager,

Medtronic (US)

I want to thank you for your help with this report – It’s been very helpful in our business planning and it well organized.

Amarildo - Manager, Global Strategic Alignment

MasterCard

We believe the work done by Data Bridge Team for our requirements in the North America Loyalty Management Market was fantastic and would love to continue working with your team moving forward.

Tor Hammer

Green Nexus LLc

Thank you for your quick response to this unfortunate circumstance. Please extend my thanks to your reach team. I will be contacting you in the future with further projects

I acknowledge the difficulty given by the very short warning for this report, and I think that its quality and your delivering time have been very satisfying.

Obviously, as a provider Data Bridge Market Research will be considered as a plus for future needs of Nippon Gases.

Yuki Kopyl (Asian Business Development Department)

UENO FOOD TECHNO INDUSTRY, LTD. (JAPAN)

Xylose report was very useful for our team. Thank you very much & hope to work with you again in the future