Circumvent the Tariff challenges with an agile supply chain Consulting

Supply Chain Ecosystem Analysis now part of DBMR Reports

Global Semi Autonomous And Autonomous Vehicle Market

Market Size in USD Billion

CAGR :

%

USD

2.22 Billion

USD

2.99 Billion

2024

2032

Forecast Period

2025 –2032

Market Size(Base Year)

USD

2.22 Billion

Market Size (Forecast Year)

USD

2.99 Billion

CAGR

%

Major Markets Players

Mercedes-Benz Group AG Continental AG

Valeo

ZF Friedrichshafen AG

Tesla

Magna International Inc. Waymo LLC

Global Semi-Autonomous and Autonomous Vehicle Market, By Component (Camera, LiDAR, Radar, Ultrasonic Sensor, and Others), ADAS Features (Lane Assist, Crash Warning System, Adaptive Cruise Control, Smart Park Assist, Cross Traffic Alert, Automatic Emergency Braking, and Others), Automation Level (Level 1, Level 2, and Level 3), Propulsion (ICE and Electric), Application (Transportation, Logistics Military, and Defence) - Industry Trends and Forecast to 2032.

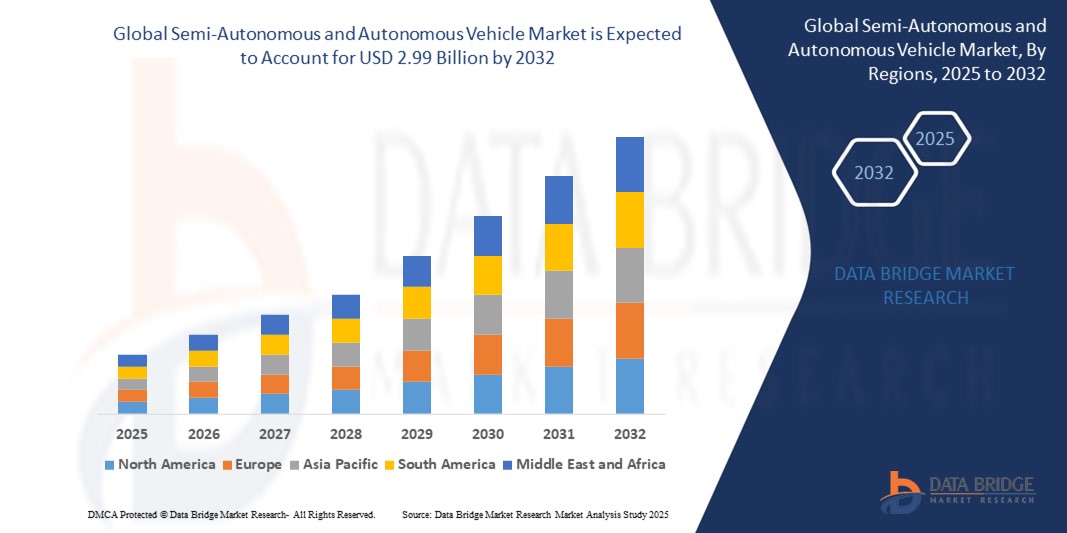

Semi-Autonomous and Autonomous Vehicle Market Size

The global semi-autonomous and autonomous vehicle market size was valued at USD 2.22 billion in 2024 and is expected to reach USD 2.99 billion by 2032,at a CAGR of 3.80% during the forecast period

Market growth is driven by increasing demand for advanced driver assistance systems (ADAS), growing consumer preference for vehicle safety, and advancements in AI and sensor technologies

Rising investments in smart infrastructure, coupled with supportive government regulations for autonomous driving, are further propelling market expansion

Semi-Autonomous and Autonomous Vehicle Market Analysis

The market is experiencing robust growth due to rising consumer demand for enhanced safety, convenience, and fuel efficiency, alongside the push for reduced human error in driving

Technological advancements in LiDAR, radar, and camera systems are enabling manufacturers to develop more reliable and efficient semi-autonomous and autonomous vehicle

Asia-Pacific dominates the global semi-autonomous and autonomous vehicle market with the largest revenue share of 57% in 2024,, driven by high vehicle production, technological adoption, and government initiatives in countries such as China, Japan, and South Korea

North America is projected to be the fastest-developing region during the forecast period, fueled by significant R&D investments, a strong automotive industry, and increasing consumer acceptance of autonomous technologies

The Level 2 segment dominated the market with a revenue share of 52.8% in 2024, driven by its widespread integration in passenger vehicles, offering features such as lane-keeping assist and adaptive cruise control. Level 2 systems balance advanced functionality with affordability, making them popular among OEMs and consumers

Report Scope and Semi-Autonomous and Autonomous Vehicle Market Segmentation

Attributes

Semi-Autonomous and Autonomous Vehicle Key Market Insights

Increasing Adoption of Electric and Autonomous Vehicles in Smart Cities

Growing Partnerships Between OEMS and Technology Companies

Value Added Data Infosets

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis.

Semi-Autonomous and Autonomous Vehicle Market Trends

“Growing Adoption of Advanced Driver Assistance Systems (ADAS)”

The integration of ADAS features, such as Adaptive Cruise Control, Lane Assist, and Automatic Emergency Braking, is driving demand for semi-autonomous vehicles, particularly in Level 1 and Level 2 automation

These features enhance driver safety and convenience, appealing to consumers in urban areas with heavy traffic, such as in the U.S. and Japan

Automakers such as Toyota and Volvo are embedding advanced ADAS in their mid-range and premium models, boosting market penetration

For instance, Tesla’s Full Self-Driving (FSD) suite includes advanced ADAS capabilities, positioning it as a leader in semi-autonomous technology

The rise of electric vehicles (EVs) with integrated ADAS, such as those from Rivian and BYD, is further accelerating adoption due to synergies with autonomous driving systems

Dealerships are increasingly offering ADAS-equipped vehicles as standard or optional packages, especially in North America and Europe

Semi-Autonomous and Autonomous Vehicle Market Dynamics

Driver

“Increasing Demand for Safety and Efficiency in Transportation”

Rising consumer awareness of road safety and the need for efficient driving solutions is fueling demand for semi-autonomous and autonomous vehicle

Features such as Crash Warning Systems, Cross Traffic Alerts, and Smart Park Assist reduce accident risks and improve driver confidence, particularly in congested cities such as Dubai and Mumbai

Autonomous vehicles, especially at Level 3 automation, promise reduced driver fatigue and enhanced fuel or battery efficiency, aligning with sustainability goals in regions such as Europe and Asia Pacific

Automakers are responding by integrating advanced components such as LiDAR, Radar, and Cameras into their vehicles to support higher automation levels

For instance, Mercedes-Benz has introduced Level 3 autonomous driving in its S-Class models, allowing conditional automation in specific scenarios

Restraint/Challenge

“Regulatory and Safety Concerns Surrounding Autonomous Driving”

Stringent regulations governing the deployment of autonomous vehicles, particularly for Level 3 and above, pose challenges to market expansion

Different regions have varying standards for autonomous driving, complicating global standardization for manufacturers such as General Motors and Volkswagen

Safety concerns, such as the reliability of sensors in adverse weather conditions, limit consumer and regulatory trust in fully autonomous systems

For instance, in the U.S., the National Highway Traffic Safety Administration (NHTSA) imposes strict guidelines on autonomous vehicle testing, slowing deployment

High costs associated with advanced components such as LiDAR and the need for extensive testing deter widespread adoption, particularly in price-sensitive markets such as India

Semi-Autonomous and Autonomous Vehicle Market Scope

The market is segmented on the basis of component, ADAS features, automation level, propulsion, and application.

By Component

On the basis of component, the market is segmented into camera, LiDAR, radar, ultrasonic sensor, and others. The camera segment held the largest market revenue share of 38.2% in 2024, driven by its critical role in providing visual data for advanced driver-assistance systems (ADAS) and autonomous driving functions, such as lane detection and object recognition. Cameras are cost-effective and widely integrated across vehicle types, supporting their dominance.

The LiDAR segment is expected to witness the fastest growth rate of 22.4% from 2025 to 2032, fueled by its high-precision 3D mapping capabilities essential for higher automation levels (Level 3 and above). Advancements in solid-state LiDAR technology and decreasing costs are accelerating its adoption in autonomous vehicles.

By ADAS Features

On the basis of ADAS features, the market is segmented into lane assist, crash warning system, adaptive cruise control, smart park assist, cross traffic alert, automatic emergency braking, and others. The adaptive cruise control segment accounted for the largest market revenue share of 34.7% in 2024, driven by its widespread adoption in semi-autonomous vehicles for enhancing driver convenience and safety through automated speed and distance management.

The automatic emergency braking segment is anticipated to experience the fastest growth rate from 2025 to 2032, propelled by increasing regulatory mandates for safety features and growing consumer demand for collision avoidance systems. Advancements in sensor fusion and AI algorithms further enhance the accuracy and reliability of these systems.

By Automation Level

On the basis of automation level, the market is segmented into Level 1, Level 2, and Level 3. The Level 2 segment dominated the market with a revenue share of 52.8% in 2024, driven by its widespread integration in passenger vehicles, offering features such as lane-keeping assist and adaptive cruise control. Level 2 systems balance advanced functionality with affordability, making them popular among OEMs and consumers.

The Level 3 segment is expected to witness the fastest growth rate of 25.8% from 2025 to 2032, as automakers and technology providers advance toward conditional automation. Increasing consumer trust in autonomous systems and supportive regulatory frameworks are key drivers for Level 3 adoption.

By Propulsion

On the basis of propulsion, the market is segmented into internal combustion engine (ICE) and electric. The ICE segment held the largest market revenue share of 68.4% in 2024, attributed to the high global volume of ICE-based vehicles and their established infrastructure. Semi-autonomous features are widely integrated into ICE vehicles, supporting their market dominance.

The electric segment is projected to grow at the fastest rate of 20.1% from 2025 to 2032, driven by the rising adoption of electric vehicles (EVs) and their synergy with autonomous technologies. EVs benefit from advanced power management and connectivity, making them ideal for integrating autonomous driving systems.

By Application

On the basis of application, the market is segmented into transportation, logistics, military, and defense. The transportation segment accounted for the largest market revenue share of 78.6% in 2024, driven by the high demand for semi-autonomous and autonomous passenger vehicles for personal mobility and ride-sharing services.

The logistics segment is expected to witness the fastest growth rate of 23.5% from 2025 to 2032, fueled by the increasing adoption of autonomous trucks and delivery vehicles for last-mile logistics and freight transport. The need for operational efficiency and cost reduction in logistics drives this growth.

Semi-Autonomous and Autonomous Vehicle Market Regional Analysis

Asia-Pacific dominates the global semi-autonomous and autonomous vehicle market with the largest revenue share of 57% in 2024,, driven by high vehicle production, technological adoption, and government initiatives in countries such as China, Japan, and South Korea

Consumers in the region show a strong inclination towards adopting cutting-edge automotive technologies, valuing enhanced safety, efficiency, and the promise of future autonomous mobility solutions

This growth is further fueled by increasing consumer demand for advanced safety features, convenience, and the potential for new mobility services, establishing Asia Pacific as a leader in the adoption and development of future vehicle technologies

U.S. Semi-Autonomous and Autonomous Vehicle Market Insight

The U.S. is expected to witness the fastest growth rate in the North America semi-autonomous and autonomous vehicle market, fueled by robust automotive production, rapid technology adoption, and strong OEM presence in countries such as China, Japan, and South Korea. Government initiatives promoting smart mobility, coupled with high consumer demand for advanced safety and connectivity features, further solidify the region’s leadership.

Europe Semi-Autonomous and Autonomous Vehicle Market Insight

The Europe market is expected to witness significant growth, driven by stringent safety regulations, such as the EU’s General Safety Regulation, mandating ADAS features in new vehicles. Countries such as Germany and France lead adoption due to their advanced automotive industries and consumer preference for premium vehicles with autonomous features. The focus on sustainability also boosts the integration of autonomous systems in electric vehicles.

U.K. Semi-Autonomous and Autonomous Vehicle Market Insight

The U.K. market is anticipated to experience robust growth, driven by demand for enhanced safety, comfort, and connectivity in urban and suburban settings. Government support for autonomous vehicle testing and smart city initiatives, combined with consumer interest in ADAS features such as automatic emergency braking and smart park assist, accelerates market growth.

Germany Semi-Autonomous and Autonomous Vehicle Market Insight

Germany is expected to see significant growth, supported by its leadership in automotive innovation and high consumer demand for advanced vehicle technologies. The integration of semi-autonomous and autonomous systems in premium vehicles, coupled with aftermarket solutions, drives market expansion. Energy efficiency and safety-focused regulations further enhance adoption.

Asia-Pacific Semi-Autonomous and Autonomous Vehicle Market Insight

The Asia-Pacific region maintains its dominance with a revenue share of 55.8% in 2024, led by China, Japan, and South Korea. Rapid urbanization, increasing vehicle ownership, and government policies promoting intelligent transportation systems drive demand. The region’s strong OEM presence and investments in EV and autonomous technology development further support market growth.

Japan Semi-Autonomous and Autonomous Vehicle Market Insight

Japan’s market is expected to witness strong growth, driven by consumer preference for high-quality, technologically advanced vehicles with ADAS and autonomous features. Major automakers such as Toyota and Honda are integrating these systems into OEM vehicles, while aftermarket solutions gain traction. Government support for smart mobility and safety regulations boosts market penetration.

China Semi-Autonomous and Autonomous Vehicle Market Insight

China holds the largest share of the Asia-Pacific market, fueled by rapid urbanization, rising vehicle ownership, and strong government backing for smart mobility and autonomous driving. Domestic OEMs and tech giants such as Baidu are advancing autonomous vehicle development, while competitive pricing and a growing middle class enhance market accessibility.

Semi-Autonomous and Autonomous Vehicle Market Share

The semi-autonomous and autonomous vehicle industry is primarily led by well-established companies, including:

Latest Developments in Global Semi-Autonomous and Autonomous Vehicle Market

In January 2025, Waymo launched its sixth-generation Waymo Driver technology, integrated into Hyundai’s IONIQ 5 electric SUV for autonomous ride-hailing services. This advanced system enhances Level 4 autonomy with improved AI algorithms and sensor capabilities, offering safer and more efficient driverless transportation. The launch strengthens Waymo’s position in the autonomous vehicle market, particularly in urban mobility solutions, and targets expansion in North American cities such as Phoenix and San Francisco

In February 2025, Volvo partnered with Waabi to integrate Waabi’s virtual driver system into autonomous trucks at Volvo’s New River Valley factory in Virginia. This collaboration focuses on developing Level 4 autonomous trucks for commercial logistics, addressing driver shortages and improving freight efficiency. The partnership leverages Waabi’s AI-driven simulation technology to enhance safety and scalability, positioning Volvo as a leader in autonomous commercial vehicles

In October 2024, Hyundai Motor Company announced a multi-year partnership with Waymo to incorporate Waymo’s autonomous driving technology into its electric vehicle lineup. The collaboration aims to produce Level 4 autonomous vehicles for ride-hailing, starting with the IONIQ 5, with plans to scale production for global markets. This strategic move strengthens Hyundai’s presence in the autonomous vehicle sector and accelerates the deployment of self-driving technology

In April 2024, Nuro, Inc. and Foretellix partnered to accelerate the deployment of autonomous delivery vehicles. This collaboration focuses on enhancing virtual testing capabilities for Nuro’s Level 4 autonomous delivery systems, using Foretellix’s advanced simulation platforms to improve safety and efficiency. The partnership aims to expand Nuro’s autonomous delivery services in urban and suburban areas, targeting the growing demand for last-mile logistics solutions

In May 2023, Valeo and DiDi Autonomous Driving entered a strategic collaboration and investment agreement to develop intelligent safety solutions for Level 4 robotaxis. This partnership focuses on integrating advanced sensors and AI-driven safety systems to enhance the reliability of DiDi’s autonomous ride-hailing services. The collaboration strengthens Valeo’s role in the autonomous vehicle market and supports DiDi’s expansion in Asia-Pacific markets

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

Interactive Data Analysis Dashboard

Company Analysis Dashboard for high growth potential opportunities

Research Analyst Access for customization & queries

Competitor Analysis with Interactive dashboard

Latest News, Updates & Trend analysis

Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.

Frequently Asked Questions

What are the primary segments covered in the Global Semi Autonomous And Autonomous Vehicle Market report?

The market is segmented based on Global Semi-Autonomous and Autonomous Vehicle Market, By Component (Camera, LiDAR, Radar, Ultrasonic Sensor, and Others), ADAS Features (Lane Assist, Crash Warning System, Adaptive Cruise Control, Smart Park Assist, Cross Traffic Alert, Automatic Emergency Braking, and Others), Automation Level (Level 1, Level 2, and Level 3), Propulsion (ICE and Electric), Application (Transportation, Logistics Military, and Defence) - Industry Trends and Forecast to 2032.

.

What is the current market size of the Global Semi Autonomous And Autonomous Vehicle Market?

The Global Semi Autonomous And Autonomous Vehicle Market size was valued at USD 2.22 USD Billion in 2024.

What is the expected growth rate of the Global Semi Autonomous And Autonomous Vehicle Market?

The Global Semi Autonomous And Autonomous Vehicle Market is projected to grow at a CAGR of 3.8% during the forecast period of 2025 to 2032.

Who are the key players in the Global Semi Autonomous And Autonomous Vehicle Market?

The major players operating in the market include Mercedes-Benz Group AG Continental AG , Valeo , ZF Friedrichshafen AG , Tesla , Magna International Inc. Waymo LLC , BMW AG , Texas Instruments Incorporated. , General Motors , Audi AG , NXP Semiconductor , Ford Motor Company , Volkswagen , Toyota Kirloskar Motor . DENSO Corporation , Robert Bosch GmbH , Infineon Technologies AG , AB Volvo , Renesas Electronics Corporation , and Visteon Corporation .

Which countries are analyzed in the Global Semi Autonomous And Autonomous Vehicle Market report?

The market report covers data from the North America.

Claudio Rondena

Group Business Development & Strategic Marketing Director, C.O.C Farmaceutici SRL

"This morning we were involved in the first part, the data presentation of MKT analysis, selected abstract from your work. The board team was really impressed and very appreciated, as well."

David Manning - Thermo Fisher Scientific

Director, Global Strategic Accounts,

Dear Ricky, I want to thank you for the excellent market analysis (LIMS INSTALLED BASE DATA) that you and your team delivered, especially end of year on short notice.

Sachin and Shraddha captured the requirements, determined their path forward and executed quickly.

You, Sachin and Shraddha have been a pleasure to work with – very responsive, professional and thorough.

Your work is much appreciated.

Manager - Market Analytics,

Uriah D. Avila - Zeus Polymer Solutions

Thank you for all the assistance and the level of detail in the market report. We are very pleased with the results and the customization. We would like to continue to do business.

Business Development Manager,

(Pharmaceuticals Partner for Nasal Sprays) | Renaissance Lakewood LLC

DBMR was attentive and engaged while discussing the Global Nasal Spray Market. They understood what we were looking for and was able to provide some examples from the report as requested. DBMR Service team has been responsive as needed. Depending on what my colleagues were looking for, I will recommend your services and would be happy to stay connected in case we can utilize your research in the future.

Business Intelligence and Analytics,

Ipsen Biopharm Limited

We are impressed by the CENTRAL PRECOCIOUS PUBERTY (CPP) TREATMENT report - so a BIG thanks to you colleagues.

Competition Analyst,

Basler Web

I just wanted to share a quick note and let you know that you guys did a really good job. I’m glad I decided to work with you. I shall continue being associated with your company as long as we have market intelligence needs.

Marketing Director,

Buhler Group

It was indeed a good experience, would definitely recommend and come back for future prospects.

COO,

A global leader providing Drug Delivery Services

DBMR did an outstanding job on the Global Drug Delivery project, We were extremely impressed by the simple but comprehensive presentation of the study and the quality of work done. This report really helped us to access untapped opportunities across the globe.

Marketing Director,

Philips Healthcare

The study was customized to our targets and needs with well-defined milestones. We were impressed by the in-depth customization and inclusion of not only major but also minor players across the globe. The DBMR Market position grid helped us to analyze the market in different dimension which was very helpful for the team to get into the minute details.

Product manager,

Fujifilms

Thankful to the team for the amazing coordination, and helping me at the last moment with my presentation. It was indeed a comprehensive report that gave us revenue impacting solution enabling us to plan the right move.

Investor relations,

GE Healthcare

Thank you for the report, and addressing our needs in such short time. DBMR has outdone themselves in this project with such short timeframe.

Market Analyst,

Medincell

We found the results of this study compelling and will help our organization validate a market we are considering to enter. Thank you for a job well done.

Andrew - Senior Global Marketing Manager,

Medtronic (US)

I want to thank you for your help with this report – It’s been very helpful in our business planning and it well organized.

Amarildo - Manager, Global Strategic Alignment

MasterCard

We believe the work done by Data Bridge Team for our requirements in the North America Loyalty Management Market was fantastic and would love to continue working with your team moving forward.

Tor Hammer

Green Nexus LLc

Thank you for your quick response to this unfortunate circumstance. Please extend my thanks to your reach team. I will be contacting you in the future with further projects

I acknowledge the difficulty given by the very short warning for this report, and I think that its quality and your delivering time have been very satisfying.

Obviously, as a provider Data Bridge Market Research will be considered as a plus for future needs of Nippon Gases.

Yuki Kopyl (Asian Business Development Department)

UENO FOOD TECHNO INDUSTRY, LTD. (JAPAN)

Xylose report was very useful for our team. Thank you very much & hope to work with you again in the future