L'augmentation du nombre d'interventions chirurgicales et des admissions en unité de soins intensifs (USI) qui en découlent a stimulé la demande de surveillance hémodynamique avancée. Les interventions chirurgicales, qu'elles soient de routine ou complexes, nécessitent souvent une surveillance rigoureuse de l'état hémodynamique du patient afin de garantir des résultats optimaux. La surveillance hémodynamique consiste à évaluer en continu les paramètres cardiovasculaires tels que la pression artérielle, le débit cardiaque et l'état hydrique, fournissant ainsi des informations cruciales sur l'état circulatoire du patient pendant et après l'intervention.

L'augmentation des maladies chroniques, notamment le diabète, l'hypertension et l'obésité, a entraîné un besoin accru d'interventions chirurgicales pour gérer et traiter ces affections. Par exemple, les personnes diabétiques peuvent nécessiter des interventions chirurgicales liées à des complications telles qu'une artériopathie périphérique ou une neuropathie diabétique.

De plus, à mesure que les interventions chirurgicales deviennent plus sophistiquées, le besoin de données hémodynamiques précises devient primordial, notamment pour les interventions telles que les chirurgies cardiaques, les transplantations d'organes et les chirurgies orthopédiques majeures. En soins intensifs, notamment en USI, la surveillance hémodynamique devient cruciale pour la prise en charge des patients présentant des pathologies complexes ou pour leur convalescence postopératoire. Par exemple, selon l'article du NCBI, les principes fondamentaux de la surveillance hémodynamique ont très peu évolué ces dernières années. L'objectif principal de la surveillance hémodynamique chez les patients gravement malades reste l'évaluation correcte du système cardiovasculaire et de sa réponse à la demande tissulaire en oxygène.

Accéder au rapport complet sur https://www.databridgemarketresearch.com/reports/global-hemodynamic-monitoring-market

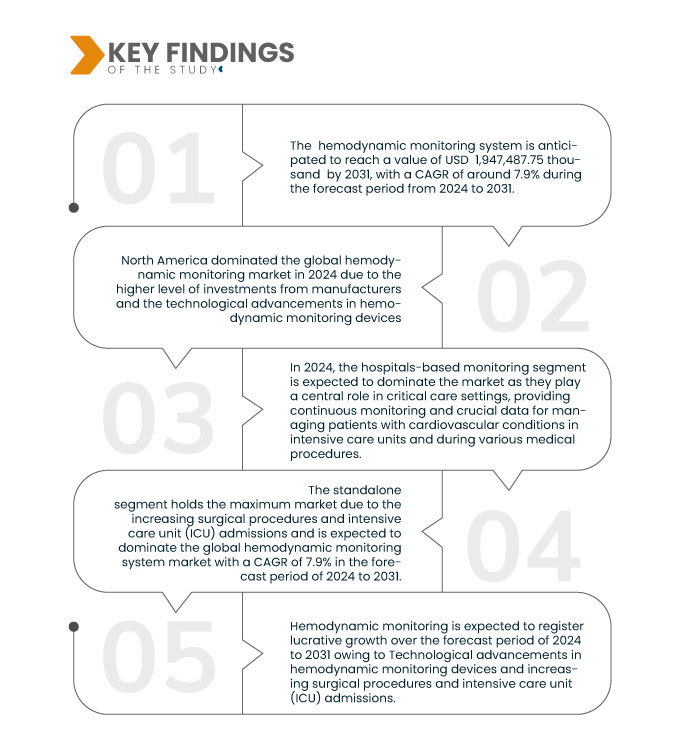

Data Bridge Market Research analyse que le marché mondial de la surveillance hémodynamique devrait croître avec un TCAC de 7,2 % au cours de la période de prévision de 2024 à 2031, et devrait atteindre 3 839 125,07 milliers USD d'ici 2031. En 2024, le segment des systèmes de surveillance hémodynamique devrait dominer le marché en raison de l'augmentation de l'incidence des troubles cardiovasculaires.

Principales conclusions de l'étude

Intégration de la surveillance hémodynamique à la télémédecine

L'intégration de la télémédecine représente une avancée majeure dans le domaine des soins de santé, notamment en matière de surveillance hémodynamique. L'intégration de la surveillance hémodynamique à la télémédecine représente une approche transformatrice de la prestation de soins, exploitant la technologie pour fournir une évaluation et une intervention en temps réel sur la santé cardiovasculaire des patients.

L’intégration avec la télémédecine remodèle les soins de santé,

Par exemple,

Capture de données en temps réel :

La surveillance hémodynamique consiste à mesurer en continu des paramètres cardiovasculaires tels que la pression artérielle, la fréquence cardiaque et la saturation en oxygène. Des dispositifs portables équipés de capteurs capturent ces données en temps réel, offrant ainsi une vision complète de l'état cardiovasculaire du patient.

Portée du rapport et segmentation du marché

Rapport métrique

|

Détails

|

Période de prévision

|

2024 à 2031

|

Année de base

|

2023

|

Années historiques

|

2022 (personnalisable pour 2016-2021)

|

Unités quantitatives

|

Chiffre d'affaires en milliers de dollars américains

|

Segments couverts

|

Produit (systèmes de surveillance hémodynamique, moniteurs de signes vitaux, oxymètres de pouls , cathéters, consommables et accessoires), type (surveillance hémodynamique non invasive, surveillance hémodynamique mini-invasive et surveillance hémodynamique invasive), modalité (autonome, de table, portable, portable et autre), application (surveillance en milieu hospitalier, surveillance en laboratoire et surveillance à domicile), configuration (automatisée et manuelle), tranche d'âge (adulte, gériatrique et pédiatrique), utilisateur final (hôpitaux, centres de chirurgie ambulatoire , laboratoires de cathétérisme, maisons de retraite, soins à domicile, établissements médicaux, centres de réadaptation et autres), canal de distribution (hors ligne et en ligne)

|

Pays couverts

|

États-Unis, Canada, Mexique, Allemagne, Royaume-Uni, France, Russie, Italie, Espagne, Turquie, Pologne, Belgique, Pays-Bas, Suisse, Danemark, Suède, Norvège, Finlande, reste de l'Europe, Chine, Japon, Inde, Australie, Corée du Sud, Nouvelle-Zélande, Singapour, Thaïlande, Philippines, Malaisie, Indonésie, Vietnam, Taïwan, reste de l'Asie-Pacifique, Brésil, Argentine, reste de l'Amérique du Sud, Arabie saoudite, Émirats arabes unis, Afrique du Sud, Égypte, Qatar, Koweït, Oman, Bahreïn et reste du Moyen-Orient et de l'Afrique

|

Acteurs du marché couverts

|

Icumedical (États-Unis), Teleflex Incorporated (États-Unis), Koninklijke Philips NV (Pays-Bas), GE HealthCare (États-Unis), Edwards Lifesciences Corporation (États-Unis), Masimo (États-Unis), Baxter (États-Unis), Getinge AB (Suède), CONTEC MEDICAL SYSTEMS CO., LTD (Chine), Nihon Kohden Corporation (Japon), Merit Medical Systems (États-Unis), Drägerwerk AG & Co. KGaA (Allemagne), OSYPKA MEDICAL (Allemagne), Deltex Medical (États-Unis), SC, Schwarzer Cardiotek (Allemagne), Caretaker LLC. (États-Unis), Uscom (Australie), NI-Medical (Israël), CNSystems Medizintechnik GmbH (Autriche) et Argon Medical Devices (États-Unis), entre autres.

|

Points de données couverts dans le rapport

|

Outre les informations sur les scénarios de marché tels que la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux acteurs, les rapports de marché organisés par Data Bridge Market Research incluent également une analyse approfondie des experts, une épidémiologie des patients, une analyse du pipeline, une analyse des prix et un cadre réglementaire.

|

Analyse des segments

Le marché mondial de la surveillance hémodynamique est classé en huit segments notables en fonction du produit, du type, de la modalité, de l'application, de la configuration, de la tranche d'âge, de l'utilisateur final et du canal de distribution.

- Sur la base du produit, le marché est segmenté en systèmes de surveillance hémodynamique, moniteurs de signes vitaux, oxymètres de pouls, cathéters et consommables et accessoires.

En 2024, le segment de la surveillance hémodynamique devrait dominer le marché

En 2024, le segment des systèmes de surveillance hémodynamique devrait dominer le marché avec une part de marché de 48,50 % en raison de l'incidence croissante des troubles cardiovasculaires.

- Sur la base du type, le marché est segmenté en surveillance hémodynamique non invasive, surveillance hémodynamique mini-invasive et surveillance hémodynamique invasive

En 2024, le segment de la surveillance hémodynamique non invasive devrait dominer le marché

En 2024, le segment de la surveillance hémodynamique non invasive devrait dominer le marché avec une part de marché de 61,13 % en raison des avancées technologiques dans les dispositifs de surveillance hémodynamique.

- En fonction de la modalité, le marché est segmenté en appareils autonomes, de table, portables, portables et autres. En 2024, le segment autonome devrait dominer le marché avec une part de marché de 47,92 %.

- En fonction des applications, le marché est segmenté en deux catégories : surveillance en milieu hospitalier, surveillance en laboratoire et surveillance à domicile. En 2024, le segment de la surveillance en milieu hospitalier devrait dominer le marché avec une part de marché de 74,82 %.

- En fonction de la configuration, le marché est segmenté en machines automatisées et manuelles. En 2024, le segment automatisé devrait dominer le marché avec une part de marché de 73,63 %.

- Le marché est segmenté en fonction de l'âge : adulte, gériatrique et pédiatrique. En 2024, le segment féminin devrait dominer le marché avec une part de marché de 66,51 %.

- En fonction de l'utilisateur final, le marché est segmenté en hôpitaux, centres de chirurgie ambulatoire, laboratoires de cathétérisme, maisons de retraite, soins à domicile, établissements médicaux, centres de rééducation, etc. En 2024, le segment des hôpitaux et cliniques devrait dominer le marché avec une part de marché de 66,64 %.

- En fonction du canal de distribution, le marché est segmenté en « hors ligne » et « hors ligne ». En 2024, le segment des appels d'offres directs devrait dominer le marché avec une part de marché de 84,04 %.

Acteurs majeurs

Data Bridge Market Research analyse Edwards Lifesciences Corporation (États-Unis), Masimo (États-Unis), Getinge AB (Suède), Baxter (États-Unis), Teleflex Incorporated (États-Unis) comme les principales entreprises du marché mondial de la surveillance hémodynamique.

Évolution du marché

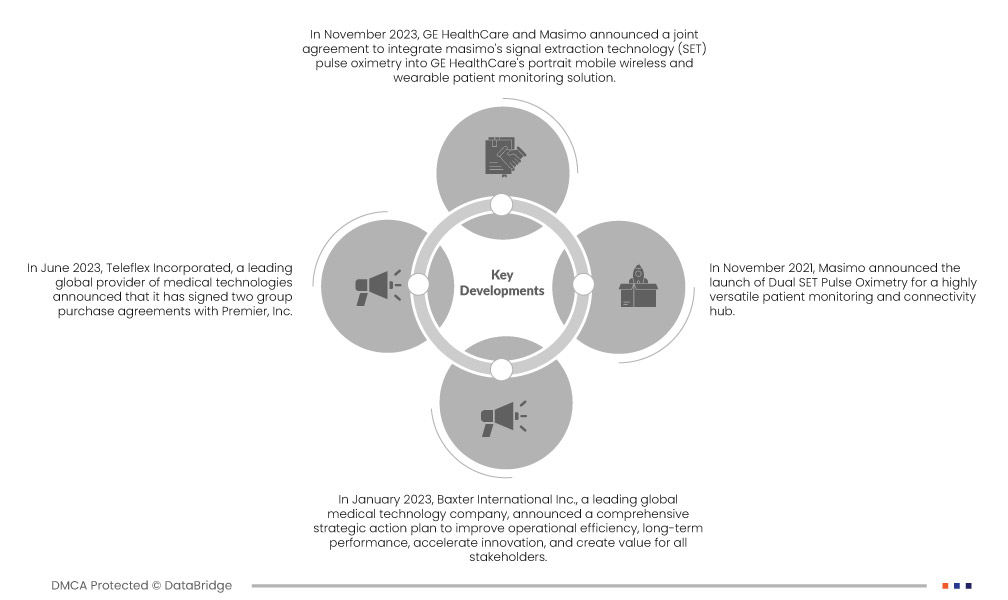

- En mai 2024, Bristol Myers Squibb (NYSE : BMY), en partenariat avec Janssen Pharmaceuticals, Inc., l'une des sociétés pharmaceutiques Janssen de Johnson & Johnson (Janssen), a annoncé que les trois indications potentielles du Milvexian, un inhibiteur oral expérimental du facteur XIa (FXIa), avaient désormais reçu la désignation accélérée de la Food and Drug Administration (FDA) américaine. Ces indications incluent les trois essais cliniques de phase 3 de Librexia (Librexia HEMODYNAMIC MONITORING, Librexia ACS et Librexia AF), tous administrés à des patients. Le programme Librexia est un programme de développement clinique complet et sans équivalent pour le FXIa, fournissant des données exhaustives provenant de près de 50 000 patients. Cela ouvre la voie à une nouvelle catégorie de patients actuellement négligés en raison du risque hémorragique.

- En janvier 2024, Penumbra, Inc., entreprise mondiale de santé spécialisée dans les thérapies innovantes, a annoncé l'approbation et le lancement par la Food and Drug Administration (FDA) américaine de Lightning Flash, le système de thrombectomie mécanique le plus avancé et le plus puissant du marché. Lightning Flash intègre la nouvelle technologie d'aspiration intelligente Lightning de Penumbra, qui intègre désormais deux algorithmes de détection de caillots. Associé à une technologie de cathéter innovante, le Lightning Flash est conçu pour éliminer rapidement les gros caillots sanguins, notamment ceux liés à l'embolie veineuse et à l'embolie pulmonaire (EP). Ce lancement permettra à l'entreprise d'élargir son portefeuille de produits grâce à la traçabilité exceptionnelle des résultats avancés de cette nouvelle technologie et à sa capacité unique à différencier le sang circulant des caillots.

- En juillet 2024, Roche a annoncé un nouveau partenariat avec Alnylam pour le développement et la commercialisation du zilebesir, un traitement expérimental par ARN interférent actuellement en phase II pour le traitement de l'hypertension artérielle. Cette collaboration allie l'expérience éprouvée d'Alnylam en matière de traitement par ARN interférent à la portée commerciale mondiale de Roche, à son engagement en faveur de l'innovation et à sa volonté de transformer le quotidien des patients atteints de maladies cardiovasculaires graves.

- En février 2021, Plavix (clopidogrel) de Sanofi a été approuvé par la Commission européenne pour son utilisation en association avec l'aspirine chez les patients adultes présentant un accident ischémique transitoire (AIT) à risque modéré ou élevé (score ABCD2 ≥ 4) ou une surveillance hémodynamique ischémique légère (SI). Vingt-quatre heures après un AIT ou un SI. Dans cette nouvelle indication, le traitement peut être poursuivi pendant 21 jours, suivi d'un traitement antiplaquettaire unique au long cours. Cette indication supplémentaire repose sur les résultats d'une étude de phase III randomisée, en double aveugle, contrôlée par placebo et initiée par deux investigateurs, portant sur plus de 10 000 patients. Des études ont montré que l'association clopidogrel-aspirine, commencée dans les 24 heures, est plus efficace que l'aspirine pour réduire le risque de SI ultérieure et présente un profil de sécurité généralement acceptable. Cette nouvelle autorisation témoigne de l'engagement indéfectible des entreprises en faveur de l'amélioration des soins cardiovasculaires.

- En septembre 2020, Daiichi Sankyo Company Limited a annoncé avoir déposé une demande complémentaire au Japon pour l'extension de l'autorisation de mise sur le marché de l'anticoagulant edoxaban (benzoate d'edoxaban hydraté) chez les patients âgés présentant une régurgitation non valvulaire et un risque hémorragique sévère. Cette demande s'appuie sur les résultats d'un essai clinique japonais de phase III (essai ELDERCARE-AF) mené auprès de 984 patients atteints de fibrillation atriale non valvulaire, âgés d'au moins 80 ans, présentant un risque hémorragique élevé et ne répondant pas aux autres traitements anticoagulants disponibles. Daiichi Sankyo entend contribuer au traitement des patients âgés atteints de fibrillation atriale non valvulaire en proposant une nouvelle option thérapeutique.

Analyse régionale

Géographiquement, les pays couverts par le rapport sur le marché mondial de la surveillance hémodynamique sont les États-Unis, le Canada, le Mexique, l'Allemagne, le Royaume-Uni, la France, la Russie, l'Italie, l'Espagne, la Turquie, la Pologne, la Belgique, les Pays-Bas, la Suisse, le Danemark, la Suède, la Norvège, la Finlande, le reste de l'Europe, la Chine, le Japon, l'Inde, l'Australie, la Corée du Sud, la Nouvelle-Zélande, Singapour, la Thaïlande, les Philippines, la Malaisie, l'Indonésie, le Vietnam, Taïwan, le reste de l'Asie-Pacifique, le Brésil, l'Argentine, le reste de l'Amérique du Sud, l'Arabie saoudite, les Émirats arabes unis, l'Afrique du Sud, l'Égypte, le Qatar, le Koweït, Oman, Bahreïn et le reste du Moyen-Orient et de l'Afrique, selon l'analyse de Data Bridge Market Research :

L’Amérique du Nord devrait dominer le marché mondial de la surveillance hémodynamique

L'Amérique du Nord devrait dominer le marché en raison de la forte demande de surveillance hémodynamique dans la région et de la hausse des dépenses de santé. L'Amérique du Nord continuera de dominer le marché de la surveillance hémodynamique en termes de parts de marché et de chiffre d'affaires, et continuera de consolider sa domination au cours de la période de prévision.

L'Asie-Pacifique est considérée comme la région connaissant la croissance la plus rapide sur le marché mondial de la surveillance hémodynamique.

L'Asie-Pacifique devrait être la région à la croissance la plus rapide du marché pour la période de prévision, en raison de l'adoption croissante de technologies de pointe et du lancement de nouveaux produits dans cette région.

Pour plus d'informations sur le rapport sur le marché mondial de la surveillance hémodynamique, cliquez ici : https://www.databridgemarketresearch.com/reports/global-hemodynamic-monitoring-market