Global Hemodynamic Monitoring Market

Market Size in USD Billion

CAGR :

%

USD

2.37 Billion

USD

4.14 Billion

2024

2032

USD

2.37 Billion

USD

4.14 Billion

2024

2032

| 2025 –2032 | |

| USD 2.37 Billion | |

| USD 4.14 Billion | |

| % | |

|

Hemodynamic Monitoring Market Size

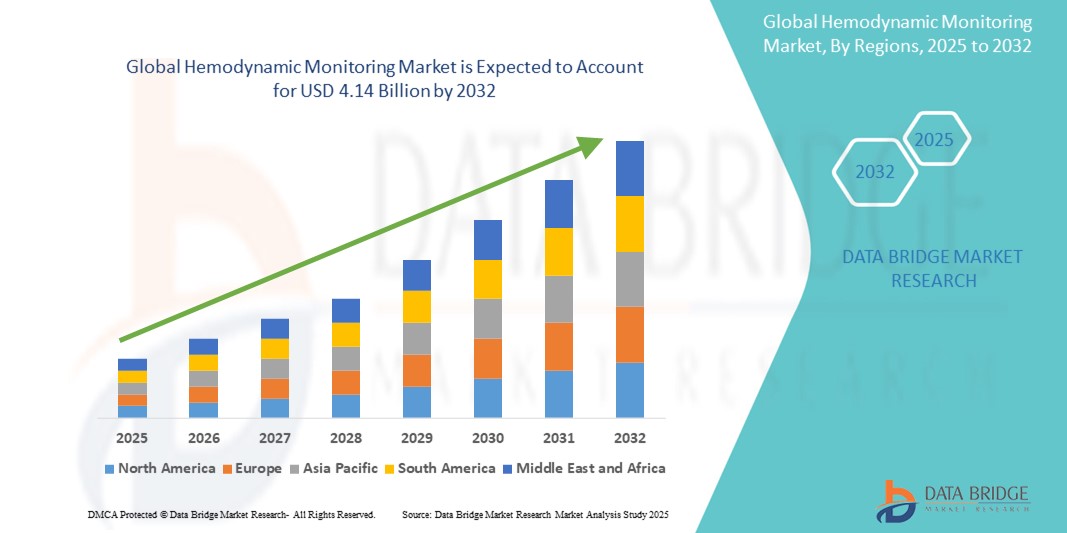

- The global hemodynamic monitoring market size was valued at USD 2.37 billion in 2024 and is expected to reach USD 4.14 billion by 2032, at a CAGR of 7.20% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular disorders and the growing need for accurate, real-time patient monitoring in critical care settings, leading to greater adoption of advanced hemodynamic systems in hospitals and emergency units

- Furthermore, technological advancements in minimally invasive and non-invasive monitoring devices, coupled with the increasing geriatric population and healthcare expenditure, are driving demand for reliable diagnostic tools. These converging factors are accelerating the uptake of hemodynamic monitoring systems, thereby significantly boosting the industry's growth

Hemodynamic Monitoring Market Analysis

- Hemodynamic monitoring, encompassing the measurement of blood pressure, blood flow, and oxygenation within the cardiovascular system, is increasingly integral to modern critical care and surgical procedures due to its ability to deliver real-time insights into a patient’s circulatory health

- The escalating demand for hemodynamic monitoring systems is primarily fueled by the rising incidence of cardiovascular diseases, increasing number of surgeries, and growing awareness about the benefits of early and continuous monitoring in intensive care settings

- North America dominated the hemodynamic monitoring market with the largest revenue share of 39.2% in 2024, driven by well-established healthcare infrastructure, a growing geriatric population, and the early adoption of advanced monitoring technologies across hospitals and specialty clinics, particularly in the U.S., which is witnessing high integration of minimally invasive monitoring tools

- Asia-Pacific is expected to be the fastest growing region in the hemodynamic monitoring market during the forecast period due to expanding healthcare facilities, rising healthcare expenditure, and increasing demand for modern diagnostic solutions in emerging economies

- The invasive hemodynamic monitoring segment dominated the hemodynamic monitoring market with a market share of 46% in 2024, driven by its clinical accuracy and widespread use in high-risk and critical care procedures

Report Scope and Hemodynamic Monitoring Market Segmentation

|

Attributes |

Hemodynamic Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hemodynamic Monitoring Market Trends

“Adoption of Minimally and Non-Invasive Monitoring Technologies”

- A significant and accelerating trend in the global hemodynamic monitoring market is the growing shift toward minimally invasive and non-invasive technologies, driven by the demand for safer, faster, and more patient-friendly diagnostic procedures in critical care and perioperative settings

- For instance, Edwards Lifesciences’ ClearSight system allows continuous non-invasive blood pressure and cardiac output monitoring, offering real-time hemodynamic insights without the need for catheterization. Similarly, CNSystems' CNAP Monitor provides beat-to-beat blood pressure measurement using a finger cuff, enhancing patient safety during surgeries

- These advanced systems reduce the risk of complications associated with invasive procedures, shorten recovery times, and are easier to deploy in a broader range of clinical settings, including outpatient and ambulatory care

- Integration with digital platforms and electronic health records (EHRs) further enables continuous data recording and remote monitoring capabilities, making it easier for clinicians to track trends and make informed decisions

- This trend is reshaping expectations for patient monitoring, prompting medical device manufacturers to focus on compact, wireless, and AI-enhanced solutions that improve clinical workflow efficiency. For example, Biobeat offers wearable hemodynamic monitors with wireless data transmission for use in both hospital and home-care environments

- As healthcare systems worldwide move toward value-based and patient-centric care, the demand for reliable, non-invasive hemodynamic monitoring is rapidly growing, offering clinicians greater flexibility and improving outcomes in critical care, cardiology, and surgery

Hemodynamic Monitoring Market Dynamics

Driver

“Rising Cardiovascular Disease Burden and Demand for Critical Care Monitoring”

- The growing global burden of cardiovascular diseases (CVDs), such as hypertension, heart failure, and myocardial infarction, is a key driver of the hemodynamic monitoring market. These conditions require accurate and continuous monitoring to guide treatment and improve patient outcomes

- For instance, the World Health Organization reports that CVDs are the leading cause of death globally, accounting for approximately 17.9 million deaths per year. As hospitals and intensive care units (ICUs) increasingly focus on early diagnosis and proactive intervention, hemodynamic monitoring systems play a critical role in risk assessment and therapy optimization

- Technological advancements have made monitoring more precise, with features such as real-time waveform analysis, advanced pressure transducers, and integrated decision support tools that enhance clinician accuracy and efficiency

- Furthermore, the rise in surgical procedures and aging populations globally is contributing to the increased use of hemodynamic monitoring during perioperative care and in patients with multiple comorbidities. Portable and wearable systems are also gaining popularity in ambulatory settings, improving access to timely monitoring and follow-up

Restraint/Challenge

“Invasiveness, Cost, and Technical Complexity Limit Wider Adoption”

- Despite the benefits, the invasive nature of traditional hemodynamic monitoring techniques such as pulmonary artery catheterization poses a challenge to wider adoption, particularly in less critical or resource-limited settings. The risk of complications such as infection, thrombosis, or bleeding can deter usage in non-emergency scenarios

- In addition, the high cost of advanced monitoring systems and associated consumables can be prohibitive for smaller hospitals and healthcare facilities, especially in developing countries with constrained healthcare budgets. For instance, equipment from leading manufacturers such as Edwards Lifesciences or GE HealthCare often requires substantial capital investment

- Technical complexity and the need for specialized training also act as barriers. Accurate operation and interpretation of data demand skilled clinicians, which may not be readily available in all clinical environments

- To overcome these challenges, manufacturers are focusing on developing user-friendly, cost-effective, and non-invasive alternatives. Moreover, investments in clinician education, training programs, and broader healthcare infrastructure improvements are essential for driving adoption and maximizing the benefits of hemodynamic monitoring technologies

Hemodynamic Monitoring Market Scope

The market is segmented on the basis of product, type, modality, application, configuration, age group, end user, and distribution channel.

- By Product

On the basis of product, the hemodynamic monitoring market is segmented into hemodynamic monitoring systems, vital sign monitors, pulse oximeters, catheters, and consumables and accessories. The hemodynamic monitoring systems segment held the largest market revenue share in 2024, driven by their critical role in providing real-time cardiovascular function data, especially in intensive care and surgical settings. These systems support advanced clinical decision-making and are widely used in hospitals, particularly for managing high-risk cardiac patients.

The pulse oximeters segment is projected to witness the fastest CAGR from 2025 to 2032, owing to their growing use in home monitoring and outpatient care, especially during respiratory illness surges such as COVID-19. Their portability, affordability, and ease of use make them highly accessible across healthcare settings.

- By Type

On the basis of type, the hemodynamic monitoring market is segmented into non-invasive hemodynamic monitoring, minimally invasive hemodynamic monitoring, and invasive hemodynamic monitoring. The invasive hemodynamic monitoring segment dominated the market in 2024 with a market share of 46% due to its clinical accuracy and relevance in complex surgical and ICU environments. Invasive methods such as pulmonary artery catheterization remain the gold standard for critical hemodynamic data collection.

The non-invasive hemodynamic monitoring segment is expected to grow at the fastest rate, supported by increasing demand for patient safety, reduced risk of infection, and technological advancements that provide reliable non-invasive alternatives with real-time results.

- By Modality

On the basis of modality, the hemodynamic monitoring market is segmented into standalone, table top, portable, wearable, and others. The table top segment accounted for the largest revenue share in 2024, as these are commonly used in hospital and critical care settings for continuous bedside monitoring. Their reliability, high-resolution displays, and advanced integration capabilities make them the primary choice for complex clinical use.

The wearable segment is projected to register the fastest growth through 2032, driven by increasing interest in continuous, real-time monitoring for chronic disease management and the rise of remote patient monitoring (RPM) in post-acute and home-care settings.

- By Application

On the basis of application, the hemodynamic monitoring market is segmented into hospital-based monitoring, laboratory-based monitoring, and home-based monitoring. The hospital-based monitoring segment led the market in 2024, underpinned by high patient volume, availability of skilled professionals, and the need for precise monitoring during surgeries and intensive care.

The home-based monitoring segment is expected to witness the highest growth during the forecast period, propelled by the shift toward decentralized care, increasing use of portable and wearable monitors, and the aging population requiring regular cardiovascular assessment at home.

- By Configuration

On the basis of configuration, the hemodynamic monitoring market is segmented into automated and manual systems. The automated segment held the largest share in 2024, driven by increasing adoption of AI-driven and digital hemodynamic monitoring platforms that enable data-driven clinical decision-making and reduce human error.

The manual segment, is expected to witness fastest growth in market during forecast period, due to the global shift toward automation and precision medicine.

- By Age Group

On the basis of age group, the hemodynamic monitoring market is segmented into adult, geriatric, and pediatric. The adult segment dominated the market in 2024 due to the high prevalence of lifestyle-related cardiovascular conditions in the adult population, such as hypertension and coronary artery disease.

The geriatric segment is projected to grow at the fastest rate through 2032, supported by the expanding elderly population and increasing vulnerability of this group to hemodynamic instability, necessitating routine and precise monitoring.

- By End User

On the basis of end user, the hemodynamic monitoring market is segmented into hospitals, ambulatory surgical centers, catheterization labs, nursing homes, homecare, medical institutions, rehabilitation centers, and others. The hospital segment accounted for the largest revenue share in 2024 due to the concentration of advanced monitoring technologies and skilled clinical staff in tertiary care centers.

The homecare segment is expected to witness the fastest CAGR, owing to rising healthcare consumerism, growing adoption of telehealth, and the need for continuous monitoring in chronic disease and post-discharge scenarios.

- By Distribution Channel

On the basis of distribution channel, the hemodynamic monitoring market is segmented into offline and online channels. The offline segment dominated the market in 2024, as institutional buyers and healthcare providers traditionally rely on direct sales representatives and authorized distributors for medical devices.

The online segment is poised for rapid growth during forecast period, due to the increasing digitalization of procurement, expanding e-commerce platforms, and demand for cost-effective and convenient purchasing channels, particularly for portable and wearable devices used in homecare.

Hemodynamic Monitoring Market Regional Analysis

- North America dominated the hemodynamic monitoring market with the largest revenue share of 39.2% in 2024, driven by well-established healthcare infrastructure, a growing geriatric population, and the early adoption of advanced monitoring technologies across hospitals and specialty clinics

- Healthcare providers in the region prioritize accurate and continuous patient monitoring, with widespread adoption of advanced hemodynamic technologies across hospitals, ICUs, and surgical centers to enhance patient outcomes

- This leadership position is further supported by a growing geriatric population, increasing healthcare expenditure, and the presence of major market players offering innovative and AI-integrated monitoring systems, positioning North America as a key hub for both innovation and usage of hemodynamic monitoring solutions

U.S. Hemodynamic Monitoring Market Insight

The U.S. hemodynamic monitoring market captured the largest revenue share of 82% in 2024 within North America, driven by the country’s advanced healthcare infrastructure, high incidence of cardiovascular diseases, and significant investments in critical care technologies. Hospitals and specialty clinics widely utilize invasive and non-invasive monitoring systems to support patient care in ICUs and surgical environments. In addition, increasing adoption of AI-enhanced and remote monitoring devices, alongside favorable reimbursement policies, continues to strengthen market growth across both public and private healthcare sectors.

Europe Hemodynamic Monitoring Market Insight

The Europe hemodynamic monitoring market is projected to expand at a substantial CAGR throughout the forecast period, primarily fueled by the region’s aging population and the high burden of cardiac and chronic illnesses. Government initiatives promoting early diagnosis and preventive care are encouraging the adoption of advanced monitoring systems across hospitals and rehabilitation centers. Moreover, European healthcare providers prioritize clinical accuracy and minimally invasive procedures, supporting the growth of portable and non-invasive hemodynamic monitoring devices in both inpatient and outpatient care settings.

U.K. Hemodynamic Monitoring Market Insight

The U.K. hemodynamic monitoring market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by a strong focus on improving patient outcomes and healthcare system efficiency. The National Health Service (NHS) has been increasing investment in intensive and post-operative care infrastructure, supporting the adoption of advanced monitoring systems. In addition, growing demand for remote and home-based monitoring for heart failure and elderly care is fueling the uptake of wearable and non-invasive technologies.

Germany Hemodynamic Monitoring Market Insight

The Germany hemodynamic monitoring market is expected to expand at a considerable CAGR during the forecast period, bolstered by the country’s strong emphasis on medical innovation and quality healthcare delivery. Germany's extensive hospital network and advanced surgical care capabilities create sustained demand for invasive and minimally invasive monitoring systems. Moreover, initiatives promoting digital health integration and personalized medicine are driving interest in smart monitoring devices with AI and data analytics capabilities.

Asia-Pacific Hemodynamic Monitoring Market Insight

The Asia-Pacific hemodynamic monitoring market is poised to grow at the fastest CAGR of 23.5% during the forecast period of 2025 to 2032, fueled by expanding healthcare infrastructure, growing medical tourism, and increased investments in critical care across countries such as China, India, and Japan. The shift toward preventive cardiology and real-time monitoring in emerging economies, alongside government support for healthcare digitalization, is significantly boosting market growth. Rising awareness and availability of affordable, portable monitoring systems are further broadening access to advanced care across diverse populations.

Japan Hemodynamic Monitoring Market Insight

The Japan hemodynamic monitoring market is gaining momentum due to its rapidly aging population and a high national focus on cardiovascular health management. The country’s advanced hospital systems are integrating innovative, minimally invasive monitoring technologies into routine care, particularly for surgical and intensive care applications. The growing adoption of smart medical devices and AI-based diagnostic tools is further propelling the market, supported by a strong culture of technological innovation and precision medicine.

India Hemodynamic Monitoring Market Insight

The India hemodynamic monitoring market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to increasing investments in hospital infrastructure, rising cardiovascular disease prevalence, and expanding critical care services. The government’s focus on upgrading public healthcare facilities and promoting medical device manufacturing under initiatives such as “Make in India” is contributing to rapid adoption. In addition, the availability of cost-effective non-invasive systems and increasing awareness about early cardiac diagnostics are driving growth across both urban and semi-urban regions.

Hemodynamic Monitoring Market Share

The Hemodynamic Monitoring industry is primarily led by well-established companies, including:

- Edwards Lifesciences Corporation (U.S.)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Baxter International Inc. (U.S.)

- Medtronic (Ireland)

- Nihon Kohden Corporation (Japan)

- Smiths Group plc (U.K.)

- Drägerwerk AG & Co. KGaA (Germany)

- Osypka Medical GmbH (Germany)

- LiDCO Group Ltd. (U.K.)

- ICU Medical, Inc. (U.S.)

- Masimo Corporation (U.S.)

- Cheetah Medical, Inc. (U.S.)

- Mindray Medical International Limited (China)

- Getinge AB (Sweden)

- Terumo Corporation (Japan)

- ConvaTec Group PLC (U.K.)

- Schiller AG (Switzerland)

- Biobeat Technologies Ltd. (Israel)

- CNSystems Medizintechnik GmbH (Austria)

What are the Recent Developments in Global Hemodynamic Monitoring Market?

- In April 2023, Edwards Lifesciences Corporation, a global leader in hemodynamic monitoring technologies, launched an advanced version of its HemoSphere platform, incorporating AI-powered analytics for early detection of hemodynamic instability. This upgrade enhances real-time clinical decision-making in critical care environments, demonstrating the company’s continued investment in intelligent, data-driven monitoring solutions that improve patient outcomes in high-acuity settings

- In March 2023, GE HealthCare Technologies Inc. unveiled its CARESCAPE R860 upgrade, a critical care monitor integrated with advanced hemodynamic parameters and cloud connectivity for continuous data capture and remote consultation. This development reflects GE HealthCare’s strategy to expand its portfolio of connected monitoring systems, supporting hospitals in managing critically ill patients with greater efficiency and precision

- In March 2023, Baxter International Inc. announced the acquisition of Hillrom’s hemodynamic monitoring assets to strengthen its critical care offerings. This strategic move is aimed at enhancing Baxter’s position in the acute care segment by combining monitoring expertise with Baxter’s therapeutic solutions. The integration signals growing consolidation in the market and the importance of comprehensive patient monitoring ecosystems

- In February 2023, Osypka Medical GmbH, a Germany-based medical technology firm, introduced the CardioMonX, a compact, non-invasive hemodynamic monitoring device tailored for outpatient and ambulatory care use. This innovation aligns with the global trend toward decentralized healthcare and expanding access to continuous cardiovascular monitoring outside traditional hospital settings, especially in aging populations

- In January 2023, LiDCO Group Ltd., a UK-based manufacturer specializing in minimally invasive hemodynamic monitoring, launched LiDCOrapidv3 with a redesigned user interface and real-time data visualization capabilities. Designed for operating rooms and high-dependency units, this product enhances clinician usability and supports rapid assessment of fluid responsiveness, reinforcing LiDCO’s role in perioperative hemodynamic optimization

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.