Global Point Of Care Diagnostics Market

市场规模(十亿美元)

CAGR :

%

USD

43.94 Billion

USD

88.21 Billion

2024

2032

USD

43.94 Billion

USD

88.21 Billion

2024

2032

| 2025 –2032 | |

| USD 43.94 Billion | |

| USD 88.21 Billion | |

| % | |

|

Global Point of Care Diagnostics Market Segmentation, By Platform (Lateral Flow Assays, Dipsticks, Microfluidics, Molecular Diagnostics, and Immunoassays), Prescription (Prescription-Based Testing, and OTC Testing), Product (Glucose, Cardio Metabolic, Infectious Disease, Influenza, HIV, Hepatitis C, Sexually Transmitted Disease (STD), Healthcare-Associated Infection (HAI), Respiratory Infection, Tropical Disease, Other Infectious Disease, Coagulation, PT/INR Activated Clotting Time (ACT/APTT), Pregnancy and Fertility, Tumor/Cancer Marker, Urinalysis, Cholesterol, Hematology, Drugs-of-Abuse, Fecal Occult, and Other POC Products), End-User (Professional Diagnostic Centers, Home Care, Research Laboratories, Other End Users)- Industry Trends and Forecast to 2032

Point of Care Diagnostics Market Size

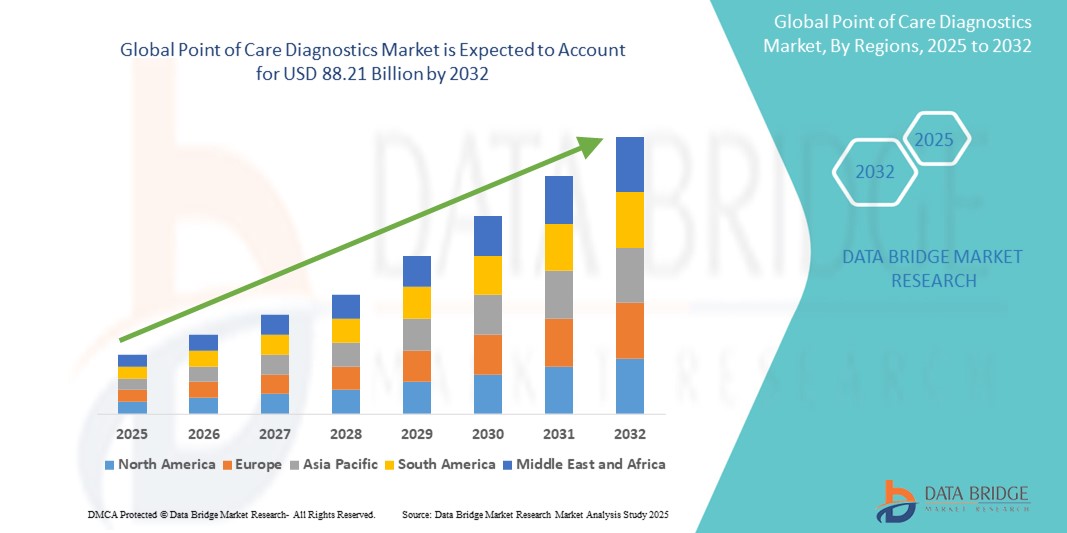

- The global point of care diagnostics market size was valued atUSD 43.94 billion in 2024and is expected to reachUSD 88.21 billion by 2032, at aCAGR of 9.1%during the forecast period

- This growth is driven by factors such as the increasing demand for rapid and accurate diagnostic tests, the rising prevalence of chronic diseases, and advancements in diagnostic technologies that improve patient outcomes and reduce healthcare costs

Point of Care Diagnostics Market Analysis

- Point of care diagnostics are medical testing devices that enable immediate diagnostic results at or near the site of patient care, enhancing rapid decision-making and treatment outcomes

- The demand for point of care diagnostics is significantly driven by the growing need for quick and accurate diagnostic solutions, increasing prevalence of chronic diseases, and advancements in diagnostic technologies

- North America is expected to dominate the point of care diagnostics market with a market share of 44.1 %, due to advanced healthcare infrastructure, high adoption of innovative diagnostic technologies, and the presence of leading healthcare companies

- Asia-Pacific is expected to be the fastest growing region in the point of care diagnostics market with a market share of 23.5%, during the forecast period driven by rapid expansion in healthcare infrastructure, increasing awareness about early disease detection, and rising surgical and diagnostic volumes

- Infectious disease segment is expected to dominate the market with a market share of 25.9% due to its the rising global incidence of infectious diseases, including respiratory infections, sexually transmitted diseases, and emerging viral outbreaks

Report Scope and Point of Care Diagnostics Market Segmentation

|

Attributes |

Point of Care Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Point of Care Diagnostics Market Trends

“Advancements in Rapid Diagnostics & Integration of Artificial Intelligence”

- One prominent trend in the evolution of point of care diagnostics is the increasing integration of artificial intelligence (AI) and machine learning (ML) technologies to enhance diagnostic accuracy and speed

- These innovations enable real-time data analysis, allowing for quicker and more reliable diagnostic results, which is particularly valuable in emergency and remote care settings

- For instance, AI-powered diagnostic tools can assist in detecting a wide range of diseases, from infections to chronic conditions such as diabetes, by interpreting results from various testing devices with high precision and minimal human intervention

- These advancements are transforming healthcare delivery, improving patient outcomes, and driving the demand for next-generation point of care diagnostic devices that offer faster, more accurate results with enhanced user-friendly interfaces

Point of Care Diagnostics Market Dynamics

Driver

“Growing Demand Due to Rising Prevalence of Chronic Diseases”

- The increasing prevalence of chronic diseases such as diabetes, cardiovascular diseases, and infectious diseases is significantly contributing to the growing demand for point of care diagnostic devices

- As the global population faces a higher burden of chronic conditions, particularly with the aging population, the need for immediate and accessible diagnostic solutions becomes more urgent

- Chronic disease management requires continuous monitoring, and point of care diagnostics provide a fast and efficient way to monitor patients’ conditions in real-time, enhancing treatment outcomes

For instance,

- In a 2023 report by the World Health Organization, it was noted that approximately 422 million people worldwide suffer from diabetes, and the number is expected to rise, which will drive demand for glucose monitoring and other diagnostic tools

- As a result of the increasing prevalence of chronic diseases, there is a significant surge in the adoption of point of care diagnostics, leading to improved patient care and quicker medical interventions

Opportunity

“Advancing Healthcare with Artificial Intelligence Integration”

- AI-powered point of care diagnostic devices can enhance diagnostic accuracy, automate data analysis, and provide real-time insights, enabling healthcare providers to make more informed decisions and improve patient outcomes

- AI algorithms can analyze diagnostic test results, such as blood glucose levels, ECG readings, or imaging scans, and offer instant feedback, helping clinicians identify potential health risks or abnormalities early on

- Moreover, AI integration can streamline workflows, reduce diagnostic errors, and improve the overall efficiency of point of care testing, enabling healthcare professionals to deliver faster and more accurate care

For instance,

- In February 2025, a study published in Nature Medicine demonstrated that AI algorithms, specifically machine learning models, could accurately predict the onset of sepsis in patients by analyzing real-time data from point of care diagnostic devices. This AI-powered approach can significantly enhance early detection, leading to timely interventions and improved survival rates

- The integration of AI in point of care diagnostics presents a significant opportunity to improve diagnostic speed, reduce healthcare costs, and enhance the quality of patient care, particularly in remote and underserved areas where timely access to healthcare is critical

Restraint/Challenge

“High Equipment and Maintenance Costs Hindering Market Penetration”

- The high cost of point of care diagnostic devices and their maintenance poses a significant challenge to market growth, especially in low-resource settings and developing regions where healthcare budgets are limited

- Advanced point of care diagnostic devices, particularly those integrated with AI or advanced imaging capabilities, can be prohibitively expensive, often reaching several thousand dollars per unit

- This substantial financial barrier can limit the widespread adoption of point of care diagnostic devices, particularly in rural areas and developing countries, where cost-effective healthcare solutions are in high demand

For instance,

- In October 2024, according to a report by Frost & Sullivan, the high upfront costs and maintenance expenses of point of care diagnostic devices are cited as major obstacles to their adoption in emerging markets, potentially hindering access to vital healthcare services

- Consequently, such challenges can lead to limited access to advanced diagnostic technologies, exacerbating healthcare disparities and slowing the market's expansion in underdeveloped regions

Point of Care Diagnostics Market Scope

The market is segmented on the basis of platform, prescription, product and end user

|

Segmentation |

Sub-Segmentation |

|

By Platform |

|

|

By Prescription |

|

|

By Product |

|

|

By End User

|

|

In 2025, the infectious disease is projected to dominate the market with a largest share in product segment

The infectious disease segment is expected to dominate the point of care diagnostics market with the largest share of 25.9% in 2024 due to the rising global incidence of infectious diseases, including respiratory infections, sexually transmitted diseases, and emerging viral outbreaks. Point of care diagnostic tests offer rapid and accurate results, making them critical for timely diagnosis and treatment, especially in remote or resource-limited areas. The increasing focus on infectious disease management, coupled with the need for faster detection and prevention strategies, is driving the growth of this segment

The lateral flow assays is expected to account for the largest share during the forecast period in platform market

In 2025, the lateral flow assays segment is expected to dominate the market with the largest market share of 41% due to its simplicity, rapid turnaround time, and cost-effectiveness. These assays are widely used for infectious disease detection, pregnancy testing, and chronic disease monitoring. Their ease of use, minimal need for specialized equipment, and suitability for both clinical and home settings contribute to their widespread adoption globally.

Point of Care Diagnostics Market Regional Analysis

“North America Holds the Largest Share in the Point of Care Diagnostics Market”

- North America dominates thepoint of care diagnostics market with a market share of estimated 44.1%, driven, by advanced healthcare infrastructure, high adoption of innovative diagnostic technologies, and the presence of leading healthcare companies

- U.S.holds a market share of 45.5%, due to the high demand for rapid diagnostics in emergency care, the increasing prevalence of chronic diseases such as diabetes and cardiovascular conditions, and continuous advancements in diagnostic technology

- The availability of robust reimbursement policies and ongoing investments in research and development by leading diagnostic manufacturers further strengthen the market

- In addition, the increasing number of testing procedures, including glucose monitoring, infectious disease testing, and pregnancy tests, is fueling market expansion across the region

“Asia-Pacific is Projected to Register the Highest CAGR in the Point of Care Diagnostics Market”

- Asia-Pacific is expected to witness the highest growth rate in the Point of Care Diagnostics market with a market share of 23.5%, driven by rapid expansion in healthcare infrastructure, increasing awareness about early disease detection, and rising surgical and diagnostic volumes

- Countries such as China, India, and Japan are emerging as key markets due to the growing aging population and the rising burden of chronic and infectious diseases

- Japan, with its advanced medical technology and strong healthcare system, continues to lead in the adoption of innovative diagnostic tools, making it a crucial market for point of care diagnostics

- India is projected to register the highest CAGR in the point of care diagnostics market, driven by expanding healthcare infrastructure, rising healthcare needs due to a growing population, and increasing demand for affordable and efficient diagnostic solutions

Point of Care Diagnostics Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Abbott(U.S.)

- Siemens Healthineers AG(Germany)

- QuidelOrtho Corporation.(U.S.)

- F. Hoffman-La Roche Ltd.(Switzerland)

- Danaher Corporation (U.S.)

- BD (U.S.)

- Chembio Diagnostics, Inc. (U.S.)

- EKF Diagnostics Holdings plc. (U.K.)

- Trinity Biotech (Ireland)

- Nova Biomedical (U.S.)

- PTS Diagnostics (U.S.)

- SEKISUI Diagnostics (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- bioMérieux S.A. (France)

- DiaSorin S.p.A (Italy)

- AccuBioTech Co., Ltd. (China)

- Meridian Bioscience, Inc. (U.S.)

- Biocartis (Europe)

- Terumo Corporation (Japan)

- Grifols, S.A. (Spain)

Latest Developments in Global Point of Care Diagnostics Market

- In February 2024, GE HealthCare launched the LOGIQ ultrasound portfolio, including the LOGIQ Totus, offering high-quality imaging and AI-powered diagnostic support to improve precision in point of care diagnostics

- In April 2024, Abbott's i-STAT TBI cartridge was approved for use with whole blood, enhancing rapid traumatic brain injury diagnostics at the point of care

- In January 2024, Rutgers University developed the CytoTracker Leukometer, a device that rapidly counts white blood cells from a single blood drop, aiding in swift sepsis detection and chemotherapy management

- In February 2022, Sense Biodetection entered into a strategic agreement with Una Health (Una) for the United Kingdom distribution of the Veros Covid-19 test

- In December 2021, FIND invested USD 21 million in Biomeme, Bioneer, Qlife, and SD Biosensor to accelerate the development, manufacturing, and launch of affordable point-of-care molecular diagnostic platforms that can detect multiple pathogens that cause diseases including COVID-19

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。