Global Pet Sitting Market

市场规模(十亿美元)

CAGR :

%

USD

4.45 Billion

USD

8.87 Billion

2025

2033

USD

4.45 Billion

USD

8.87 Billion

2025

2033

| 2026 –2033 | |

| USD 4.45 Billion | |

| USD 8.87 Billion | |

| % | |

|

全球寵物寄養市場細分,依應用(日托、遛狗、寵物運輸及其他)、寵物類型(犬、貓、魚、籠養寵物及其他)劃分-產業趨勢及至2033年的預測

寵物寄養市場規模

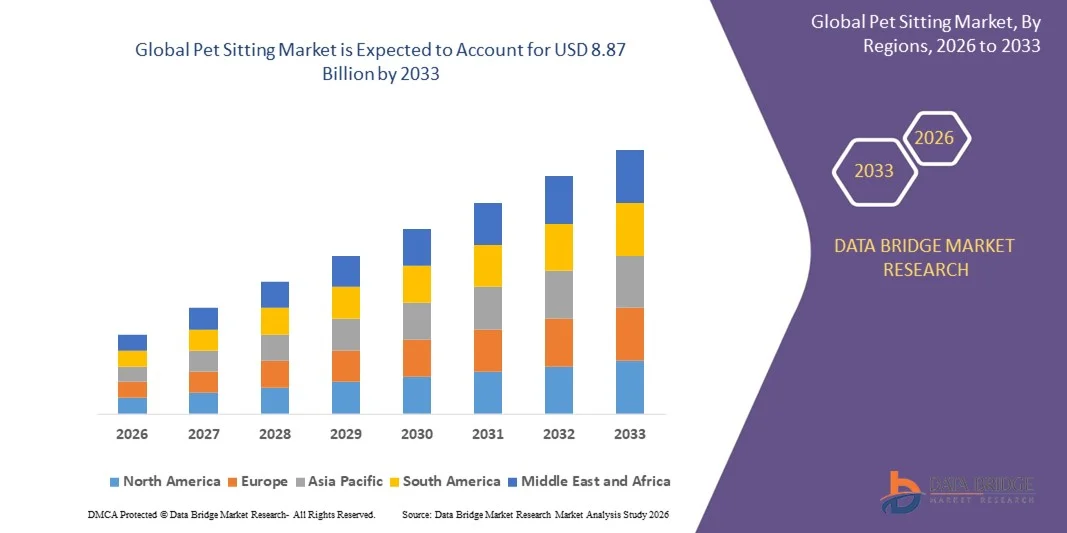

- 2025年全球寵物寄養市場規模為44.5億美元 ,預計 2033年將達88.7億美元,預測期內 複合年增長率為9.00%。

- 市場成長主要得益於寵物飼養率的上升和寵物人性化的日益增強,寵物主人在離家時更加重視個人化和無壓力的照顧方案。

- 可支配收入的成長和生活方式的改變,例如工作時間延長和頻繁出差,促使寵物主人選擇專業的寵物照顧服務,而不是非正式的照顧安排。

寵物寄養市場分析

- 由於人們對寵物健康、安全和情感福祉的意識不斷提高,寵物寄養市場正穩步增長,寵物主人尋求能夠在家中照顧寵物並維持其日常作息的解決方案。

- 服務提供者正專注於加值服務,例如即時更新、寵物活動追蹤和客製化照護方案,這些都能提升客戶滿意度和復購率。

- 2025年,北美在寵物寄養市場佔據主導地位,收入份額最大,這主要得益於寵物擁有率高、寵物護理服務支出強勁以及寵物日益人性化等因素。

- 受生活方式改變、中產階級人口成長以及行動寵物護理平台普及率提高的推動,亞太地區預計將成為全球寵物照顧市場成長最快的地區。

- 2025年,日托服務細分市場佔據最大的市場份額,這主要得益於人們越來越傾向於選擇居家寵物照顧服務,因為這種服務能夠確保寵物的舒適度、日常作息的連續性以及壓力的減輕。日間照顧服務通常包括餵食、玩耍、餵食和陪伴,因此深受尋求可靠且個人化照顧服務的上班族和經常出差人士的青睞。

報告範圍和寵物寄養市場細分

|

屬性 |

寵物寄養市場關鍵洞察 |

|

涵蓋部分 |

|

|

覆蓋國家/地區 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機遇 |

|

|

加值資料資訊集 |

除了對市場狀況(如市場價值、成長率、細分、地理覆蓋範圍和主要參與者)的洞察之外,Data Bridge Market Research 精心編制的市場報告還包括深入的專家分析、定價分析、品牌份額分析、消費者調查、人口統計分析、供應鏈分析、價值鏈分析、原材料/消耗品概述、供應商選擇標準、PESTLE 分析、波特五力分析和監管框架。 |

寵物寄養市場趨勢

對個人化和居家寵物照護服務的需求不斷增長

- 人們越來越關注寵物的舒適度、情緒健康和日常作息的規律性,這正在顯著影響全球寵物寄養市場,因為寵物主人更傾向於選擇居家照顧而非傳統的寄養機構。寵物寄養服務因其能夠提供個人化的關注、減輕寵物的壓力以及靈活的照顧時間而日益受到歡迎,這與寵物日益擬人化的趨勢不謀而合。

- 人們日益關注寵物的健康、安全和心理健康,這加速了職場人士和經常出差的人士對專業寵物照顧服務的需求。寵物主人積極尋找值得信賴的照顧人員,以便提供個人化的餵食、運動和用藥方案,這也促使服務提供者提升服務品質和可靠性。

- 便利至上的生活方式和數位化普及正在影響消費者的購買決策,他們更傾向於使用提供便利預訂、經過認證的保姆、即時更新和透明定價的應用程式平台。這些功能有助於平台建立信任和長期的客戶關係,同時在競爭激烈的市場中脫穎而出。

- 例如,2024年,美國的Rover和英國的TrustedHousesitters透過推出更完善的居家寵物照顧服務,包括即時寵物動態更新和照顧者背景審核,擴展了其服務範圍。這些措施旨在滿足日益增長的個人化、輕鬆無憂的寵物照顧需求,從而提高用戶參與度和重複預訂率。

- While demand for pet sitting services continues to rise, sustained market growth depends on maintaining service quality, sitter availability, and trust-building mechanisms. Companies are focusing on platform security, training programs, and service standardization to ensure consistent customer experience and long-term adoption

Pet Sitting Market Dynamics

Driver

Growing Preference For Personalized And Stress-Free Pet Care

- Rising pet ownership and increasing emotional attachment between pets and owners are key drivers for the global pet sitting market. Pet owners are increasingly choosing personalized, in-home care solutions to ensure pets remain comfortable and safe in familiar environments, supporting steady demand growth

- Expanding participation of dual-income households and frequent travel patterns are contributing to higher reliance on professional pet sitters. These services provide flexibility, reliability, and peace of mind, enabling owners to balance work and lifestyle commitments without compromising pet care

- Digital platforms and mobile applications are actively promoting pet sitting services through user-friendly interfaces, secure payment systems, and verified caregiver networks. In addition, marketing efforts highlighting trust, transparency, and pet well-being are encouraging wider adoption across urban populations

- For instance, in 2023, Wag! in the U.S. and Pawshake in Australia reported increased bookings for in-home pet sitting services driven by busy lifestyles and rising travel frequency. Both platforms emphasized safety checks, sitter ratings, and real-time pet updates to strengthen consumer trust and platform loyalty

- Despite strong demand drivers, continued growth relies on effective sitter onboarding, training, and service consistency. Investment in technology, customer support, and caregiver quality assurance will remain essential to sustain market momentum

Restraint/Challenge

Trust Concerns And Service Cost Sensitivity

- Trust and safety concerns remain a major challenge in the pet sitting market, as pet owners may hesitate to allow unfamiliar caregivers into their homes. Incidents related to inconsistent service quality or lack of sitter accountability can negatively impact customer confidence and limit repeat usage

- Service cost sensitivity also restricts adoption among price-conscious consumers, particularly when compared to informal care arrangements such as family or friends. Premium pricing for experienced or specialized pet sitters may limit market penetration in certain customer segments

- Operational challenges, such as sitter availability during peak travel seasons and maintaining service standards across platforms, further impact market growth. In addition, managing cancellations, emergencies, and liability issues increases complexity for service providers

- For instance, in 2024, pet sitting platforms operating in urban markets such as New York and London reported customer hesitation due to pricing concerns and trust-related issues, particularly among first-time users. These challenges affected booking conversion rates and required additional investment in customer education and platform security

- Addressing these challenges will require stronger verification systems, transparent communication, competitive pricing models, and enhanced customer education. Collaboration with insurers, training providers, and technology partners can help improve trust, reduce risks, and unlock long-term growth opportunities in the global pet sitting market

Pet Sitting Market Scope

The market is segmented on the basis of application and pet type.

- By Application

On the basis of application, the global pet sitting market is segmented into Day Care Visits, Dog Walking, Pet Transportation, and Others. The Day Care Visits segment held the largest market revenue share in 2025 driven by the growing preference for in-home pet care that ensures comfort, routine continuity, and reduced stress for pets. Day care visit services typically include feeding, playtime, medication administration, and companionship, making them a widely preferred option among working professionals and frequent travelers seeking reliable and personalized care.

The Dog Walking segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing urbanization, busy lifestyles, and rising awareness of pet physical fitness and mental stimulation. Dog walking services are gaining popularity due to their flexibility, affordability, and suitability for daily care needs, particularly among apartment-dwelling pet owners who require regular outdoor activity support for their pets.

- By Pet Type

On the basis of pet type, the global pet sitting market is segmented into Dogs, Cats, Fish, Cage Pets, and Others. The Dogs segment accounted for the largest market share in 2025 owing to higher dog ownership rates and the greater need for regular supervision, exercise, and social interaction. Dog owners are more inclined to seek professional pet sitting services to meet daily care requirements, including walking, feeding, and behavioral monitoring.

The Cats segment is expected to witness the fastest growth rate from 2026 to 2033, supported by rising cat adoption and the increasing preference for in-home care that minimizes environmental changes. Cat owners often opt for pet sitting services to ensure feeding, litter maintenance, and companionship without relocating pets, supporting consistent demand across urban and suburban households.

Pet Sitting Market Regional Analysis

- North America dominated the pet sitting market with the largest revenue share in 2025, driven by high pet ownership rates, strong spending on pet care services, and the growing humanisation of pets

- 該地區的寵物主人非常重視便利性、可靠性和個人化的居家照顧,他們更傾向於選擇專業的寵物照顧服務,而不是傳統的寄養機構。

- 快節奏的生活方式、頻繁的旅行以及提供經過認證的保姆、即時更新和靈活服務選項的應用程式平台的蓬勃發展,進一步推動了這種服務的廣泛普及。

美國寵物寄養市場洞察

2025年,美國寵物寄養市場在北美地區佔據最大的市場份額,這主要得益於寵物擁有量的增加、可支配收入的提高以及人們對高端寵物護理的重視。寵物主人越來越傾向於選擇個人化、無壓力的照顧方案,讓寵物能夠留在熟悉的環境中。數位平台的廣泛應用,以及對經過背景調查的寄養人員和行動應用程式整合的需求,持續推動市場擴張。此外,寵物擬人化的趨勢以及國內旅行的頻繁進行,也進一步增強了對專業寵物寄養服務的需求。

歐洲寵物寄養市場洞察

預計2026年至2033年間,歐洲寵物寄養市場將保持穩定成長,主要驅動力在於人們對寵物福祉的日益關注以及城市居民生活方式的改變。單身家庭和專業人士數量的增長也推動了對可靠寵物照顧服務的需求。歐洲消費者傾向於結構化、標準化且以信任為基礎的服務模式,促進了專業寵物寄養平台在住宅環境中的普及。

英國寵物寄養市場洞察

受寵物領養率上升和人們對居家寵物照顧服務需求日益增長的推動,英國寵物寄養市場預計將在2026年至2033年間迎來顯著增長。寵物主人對寵物焦慮、安全以及日常生活被打亂等問題的擔憂,促使他們選擇寵物保母而非寵物寄養中心。此外,英國強大的數位基礎設施和線上預訂平台的高使用率也進一步促進了市場成長。

德國寵物寄養市場洞察

德國寵物寄養市場預計將在2026年至2033年間實現最快成長,這主要得益於人們對動物福利的高度重視、標準化的寵物照顧模式以及日益增長的城市化進程。德國寵物主人更傾向於選擇組織有序、值得信賴的照顧服務,從而推動了對經過認證和培訓的寵物寄養員的需求。此外,越來越多的專業人士參與寵物寄養服務以及頻繁的出行也為市場需求的持續成長提供了支撐。

亞太地區寵物寄養市場洞察

受中國、日本和印度等國家寵物擁有量上升、可支配收入增加以及快速城市化進程的推動,亞太地區的寵物寄養市場預計將在2026年至2033年間實現最快增長。生活方式的改變和人們對專業寵物照護服務日益增長的認知度也促進了寵物寄養服務的普及。此外,行動服務平台的擴展和社交媒體的普及也提高了該地區寵物寄養服務的市場可及性。

日本寵物寄養市場洞察

由於城市密度高、居住空間縮小以及人口老化,預計日本寵物寄養市場將在2026年至2033年間保持穩定成長。寵物主人越來越尋求便捷可靠的照顧方案,以最大程度地減少對寵物日常生活的干擾。對衛生、安全和科技融合的高度重視,推動了對專業寵物寄養服務的需求,尤其是在城市住宅區。

中國寵物寄養市場洞察

到2025年,中國寵物寄養市場在亞太地區將佔據顯著的市場份額,這主要得益於快速的城市化進程、中產階級收入水平的提高以及寵物飼養量的增加。伴侶動物日益普及和數位化服務平台的擴張,使得寵物寄養服務更加便捷易用。此外,年輕專業人士數量的成長以及頻繁的出行習慣,也推動了各大城市對靈活可靠的寵物照顧解決方案的需求。

寵物寄養市場份額

寵物寄養產業主要由一些成熟的公司主導,其中包括:

• A Place for Rover, Inc.(美國)

• DogVacay(美國)

• Holidog, Inc.(法國)

• Care.com, Inc.(美國)

• Fetch! Pet Care(美國)

• Swifto Inc.(美國)

• Chicago Dog Walkers(美國) •

Best Friends Pet Care (

美國) • Camp Bow Wow

(美國)

•

PetC

(美國) Ltd.

Petfoods(加拿大)

• Colgate-Palmolive Company(美國)

• Heristo Aktiengesellschaft(德國)

• Mars, Incorporated(美國)

• Nestlé(瑞士)

• Doskocil Manufacturing Company, Inc.(美國)

• Petco Animal Supplies, Inc.(美國)

• PetSmart Inc.(美國)

全球寵物寄養市場最新發展動態

- 2023年11月,Rover集團與黑石集團達成最終收購協議,此舉標誌著一項旨在增強財務穩定性並加速平台擴張的策略整合措施。這項價值約23億美元的全現金交易預計將支持Rover在技術、服務品質和全球覆蓋率方面的長期投資,從而鞏固其在寵物照顧市場的領先地位。

- • 2023年9月,Wag! 與一家寵物健康科技公司合作,在其行動應用程式中整合健康監測功能。此舉透過提供即時寵物健康狀況信息,提升了用戶體驗,順應了人們日益重視的寵物預防保健理念,並有助於提高其在註重寵物健康的寵物主人中的市場滲透率。

- 2023年8月,Rover宣布推出訂閱服務,為用戶提供專屬折扣和優先預約寵物照顧者的服務。此舉旨在提高客戶留存率,創造持續收入,並透過加值服務提升Rover的差異化優勢,從而積極影響其在寵物護理行業的競爭地位。

- 2023年7月,PetBacker拓展服務範圍,在新加坡新增寵物美容訓練服務。此多元化策略旨在滿足不斷變化的消費者需求,將公司定位為綜合性寵物護理服務提供者,並增強其在東南亞寵物服務市場的競爭力。

- 2022年9月,PetSmart與室內設計師Nate Berkus和Jeremiah Brent合作,推出了一系列全新的寵物家具,包括沙發、床和支架。此次新品發表旨在提升寵物的舒適度,同時兼顧寵物主人的家居美學,助力PetSmart拓展其以生活方式為導向的產品線,並加強與客戶的互動。

- 2022年5月,金普頓酒店及餐廳與Wag!合作,為全美各地的酒店客人提供酒店內和居家寵物遛狗及上門服務。此次合作旨在提升寵物友善飯店體驗,提高服務可近性,並推動跨產業對專業寵物照護解決方案的需求。

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。