菲律宾私人健康保险市场,按类型(重大疾病保险、个人健康保险、家庭健康保险、疾病特定保险等)、健康计划类别/金属级别(青铜、白银、黄金、铂金等)、提供商类型(健康维护组织 (HMOS)、首选提供商组织 (PPOS)、独家提供商组织 (EPOS)、服务点 (POS) 计划、高免赔额健康计划 (HDHPS) 等)、年龄组(青年期(19-44 岁)、中年期(45-64 岁)和老年期(65 岁及以上))、分销渠道(直接保险公司、保险聚合商等)划分 – 行业趋势和预测到 2029 年。

市场分析和规模

健康保险政策包含多种功能和福利。它为投保人提供针对某些治疗的财务保障。它还提供包括无现金住院、住院前和住院后报销保障和各种附加服务等优势。

在健康保险计划中,有几种类型的保险可供选择,包括无现金和报销索赔。当保单持有人在保险公司的网络医院接受治疗时,可享受无现金福利。如果保单持有人在不在名单网络内的医院接受治疗,在这种情况下,保单持有人将承担所有医疗费用,然后通过提交所有医疗账单向保险公司索赔报销。这种私人健康保险为保单持有人提供财务支持,因为它涵盖了保单持有人住院治疗时的所有医疗费用。

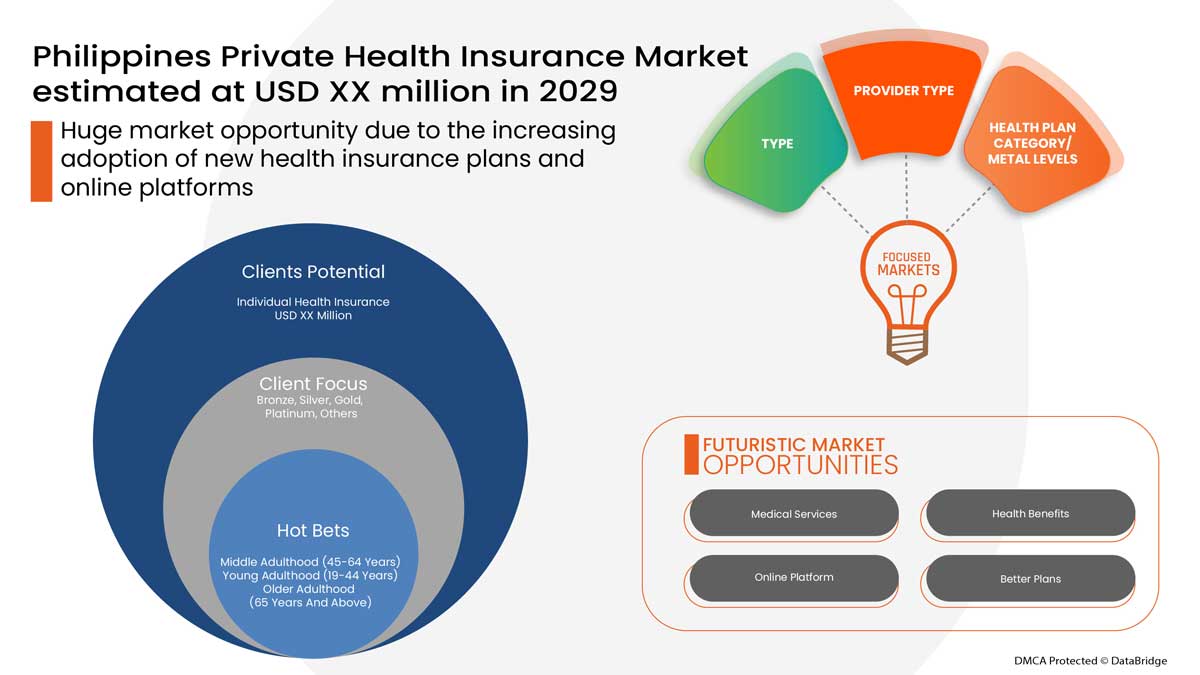

Data Bridge Market Research 分析称,菲律宾私人健康保险市场预计到 2029 年将达到 12.7312 亿美元的价值,预测期内的复合年增长率为 1.2%。由于私人健康保险的兴起,“个人健康保险”在相关市场中占据最突出的类型部分。Data Bridge Market Research 团队策划的市场报告包括深入的专家分析、进出口分析、定价分析、生产消费分析和气候链情景。

|

报告指标 |

细节 |

|

预测期 |

2022 至 2029 年 |

|

基准年 |

2021 |

|

历史岁月 |

2020(可定制至 2019 - 2014) |

|

定量单位 |

收入(百万美元) |

|

涵盖的领域 |

按类型(重大疾病保险、个人健康保险、家庭健康保险、疾病特定保险等)、健康计划类别/金属级别(铜、银、金、铂金等)、提供商类型(健康维护组织 (HMOS)、首选提供商组织 (PPOS)、独家提供商组织 (EPOS)、服务点 (POS) 计划、高免赔额健康计划 (HDHPS) 等)、年龄组(青年期(19-44 岁)、中年期(45-64 岁)和老年期(65 岁及以上))、分销渠道(直接保险公司、保险整合商等) |

|

覆盖国家 |

菲律宾 |

|

涵盖的市场参与者 |

Aetna Inc.(CVS Health 旗下子公司)(美国)、友邦保险集团有限公司(香港)、安联(德国)、汇丰集团(香港)、Pacific Cross(菲律宾)、ASSICURAZIONI GENERALI SPA(意大利) |

市场定义

健康保险涵盖所有类型的手术费用以及因疾病或受伤而产生的医疗费用。健康保险适用于全面或有限范围的医疗服务,提供特定服务的全部或部分费用的保险。健康保险为投保人提供财务支持,因为它涵盖投保人住院治疗时的所有医疗费用。健康保险还涵盖住院前和住院后的费用。

监管框架

2013年国民健康保险法规则及条例

为遵循这一原则,国家健康保险计划(NHIP)(以下简称“计划”)的实施细则和条例(IRR)应采用以下指导原则:

国家卫生资源的分配——该计划应强调政府优先考虑卫生作为实现更快经济发展和改善生活质量的战略的重要性;

普及性——该计划应与其他政府卫生计划相结合,为所有公民提供获得卫生服务的经济途径。该计划应将实现全民覆盖作为最高优先事项,至少提供最低限度的基本医疗保险福利;

公平——该计划应提供统一的基本福利。获得医疗服务必须取决于个人的健康需求,而不是支付能力;

COVID-19 对私人健康保险市场影响甚微

2020-2021 年,COVID-19 影响了各种制造业和服务业,导致工作场所关闭、供应链中断和交通限制。然而,供需失衡及其对定价的影响被认为是短期的,预计随着疫情结束,这一影响将会恢复。由于 COVID-19 在全球爆发,对私人医疗保险的需求大幅增加。此外,对疫情的恐惧和医疗服务成本的上涨也推动了医疗保险市场在疫情期间的增长。此外,医疗保险公司推出了套餐和解决方案,以支付治疗感染 covid19 的保险公司的医疗费用。因此,尽管其他行业在 covid19 爆发期间遭受了巨大损失,但私人医疗保险行业却在大幅增长。

私人健康保险市场的市场动态包括:

私人健康保险市场的驱动因素/机遇

- 医疗服务成本不断上涨

健康保险在重病或事故发生时提供经济支持。医疗服务手术和住院费用的增加在世界各地引发了新的金融流行病。医疗服务费用包括手术费用、医生费用、住院费用、急诊室费用和诊断测试费用等。因此,医疗服务成本的增加推动了市场的增长。

- 日托程序数量不断增加

日间护理是指那些主要要求住院时间较短的医疗程序或手术。在日间护理程序中,患者需要在医院停留一小段时间。大多数健康保险公司现在都在其保险计划中涵盖日间护理程序,对于此类手术的索赔,没有强制要求在医院停留 24 小时,这是索赔保险的最低住院时间。虽然大多数健康保险计划涵盖住院和重大手术,但投保人也可以根据其健康保险政策索赔日间护理程序,这推动了市场的需求。

- 强制选择公共和私营部门的健康保险

购买医疗保险是公共部门和私营部门员工的强制性规定。医疗保险提供员工在公司工作期间可以享受的重要医疗福利。如果出现任何紧急情况或医疗问题,医疗保险对于支付治疗费用非常有用。员工医疗保险是个人雇主为其员工提供的一项延伸福利。所提供的医疗保险不仅涵盖员工,还涵盖同一保单计划下的家庭成员。此外,在某些情况下,雇主可能会支付医疗保险保费或保险金额的一部分。

- 老年人口不断增加

由于衰老和免疫系统较弱,老年人可能会出现更多健康问题,包括牙齿问题、心脏病、癌症问题和绝症。一份好的老年人健康保险可以帮助老年人选择好的健康保险服务,以减少未来的财务担忧。因此,老年人口的增加可以促进健康保险市场的增长。

- 提高对健康保险好处的认识

面对医疗紧急情况,健康保险可以让消费者从与医疗费用相关的压力中解脱出来,专注于治疗。无论我们目前的身体状况如何或有规律的生活方式,医疗紧急情况都可能随时发生。因此,重要的是要为我们的家人和我们自己做好计划,保护他们免受任何不可预见的医疗情况的影响,尤其是当家里有年迈的父母时,因为他们更容易受到感染或其他疾病的影响。

菲律宾私人健康保险市场面临的限制/挑战

- 保费成本高

健康保险涵盖所有类型的医疗费用。它为投保人提供财务支持,因为它涵盖投保人住院治疗时的所有医疗费用。健康保险还涵盖住院前和住院后的费用。要购买健康保险,投保人必须定期支付保险费以保持健康保险单有效。在大多数情况下,保险费的成本很高,这取决于保险计划,这阻碍了市场的增长。

- 缺乏健康保险意识

在医疗保健领域,世界上很大一部分人口仍然不知道健康保险的好处。随着医疗领域的进步,世界各地的医疗费用正在增加。通过技术的进步,医疗保健行业是增长最快的领域之一,然而,由于缺乏对健康保险的好处的认识,健康保险的普及率仍然很低

这份菲律宾私人健康保险市场报告详细介绍了最新发展、贸易法规、进出口分析、生产分析、价值链优化、市场份额、国内和本地市场参与者的影响,分析了新兴收入来源、市场法规变化、战略市场增长分析、市场规模、类别市场增长、应用领域和主导地位、产品批准、产品发布、地域扩展、市场技术创新等方面的机会。如需了解有关私人健康保险市场的更多信息,请联系 Data Bridge Market Research 获取分析师简报。我们的团队将帮助您做出明智的市场决策,以实现市场增长。

最新动态

- 2022 年 2 月,Assicuranzioni Generali SPA 签署了收购 La Me´dicale 的协议,La Me´dicale 是一家医疗专业人士保险公司。此举还预示着 Predica 1 死亡保险组合的出售,该组合由 La Me´dicale 营销和管理。

- 2022 年 3 月,全球最大的房地产投资管理公司之一安联房地产代表安联房地产亚太日本多户型基金签署协议,以约 9000 万美元收购东京优质多户型住宅资产组合。这反过来又帮助该公司在长期内赚取了更多利润。

菲律宾私人健康保险市场范围

菲律宾私人健康保险市场根据类型、健康计划类别/金属级别、提供商类型、年龄组和分销渠道进行细分。这些细分市场之间的增长将帮助您分析行业中的增长细分市场,并为用户提供有价值的市场概览和市场洞察,帮助他们做出战略决策,确定核心市场应用。

类型

- 重大疾病保险

- 个人健康保险

- 家庭健康保险

- 特定疾病保险

- 其他的

根据类型,菲律宾私人健康保险市场分为重疾保险、个人健康保险、家庭健康保险、特定疾病保险和其他。

健康计划类别/金属级别

- 青铜

- 银

- 金子

- 铂

- 其他的

根据健康计划类别/金属级别,菲律宾私人健康保险市场分为青铜级、白银级、黄金白金级和其他级。

提供商类型

- 健康维护组织(HMOS)

- 首选医疗机构 (PPOS)

- 独家供应商组织 (EPOS)

- 服务点 (POS) 计划

- 高免赔额健康计划(HDHPS)

- 其他的

根据提供商类型,菲律宾私人健康保险市场分为健康维护组织(HMOS)、优先提供商组织(PPOS)、独家提供商组织(EPOS)、服务点(POS)计划、高免赔额健康计划(HDHPS)等。

年龄组

- 青年期(19-44 岁)

- 中年(45-64岁)

- 老年人(65 岁及以上)

根据年龄组,菲律宾私人健康保险市场分为青年期(19-44岁)、中年期(45-64岁)和老年期(65岁及以上)。

分销渠道

- 直接保险公司

- 保险聚合商

- 其他的

根据分销渠道,菲律宾私人健康保险市场分为直接保险公司、保险聚合商和其他公司。

竞争格局和私人健康保险市场份额分析

菲律宾私人健康保险市场竞争格局提供了竞争对手的详细信息。详细信息包括公司概况、公司财务状况、产生的收入、市场潜力、研发投资、新市场计划、菲律宾业务、生产基地和设施、生产能力、公司优势和劣势、产品发布、产品宽度和广度、应用主导地位。以上提供的数据点仅与公司对菲律宾私人健康保险市场的关注有关。

私人健康保险市场的一些主要参与者包括 Aetna Inc.(CVS Health 的子公司)(美国)、友邦保险集团有限公司(香港)、安联(德国)、汇丰集团(香港)、Pacific Cross(菲律宾)、ASSICURAZIONI GENERALI SPA(意大利)等。

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

目录

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF PHILIPPINES PRIVATE HEALTH INSURANCE MARKET

1.4 LIMITATION

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 AGE GROUP LIFE LINE CURVE

2.7 MULTIVARIATE MODELING

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 DBMR MARKET CHALLENGE MATRIX

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 SOUTH EAST ASIA PRIVATE HEALTH INSURANCE MARKET- PESTEL ANALYSIS

4.1.1 OVERVIEW

4.1.2 POLITICAL FACTORS

4.1.3 ENVIRONMENTAL FACTORS

4.1.4 SOCIAL FACTORS

4.1.5 TECHNOLOGICAL FACTORS

4.1.6 ECONOMICAL FACTORS

4.1.7 LEGAL FACTORS

4.1.8 CONCLUSION

4.2 PORTER’S FIVE FORCES:

4.2.1 THREAT OF NEW ENTRANTS:

4.2.2 THREAT OF SUBSTITUTES:

4.2.3 CUSTOMER BARGAINING POWER:

4.2.4 SUPPLIER BARGAINING POWER:

4.2.5 INTERNAL COMPETITION (RIVALRY):

4.3 SOUTH EAST ASIA INSURANCE SCENARIO VS GLOBAL

4.4 CUSTOMIZED DELIVERABLE

4.4.1 HOW ARE INSURANCE CLAIMS EVALUATED (I.E., PROCESS FOR FILING FROM HOSPITALS, PHYSICIAN JUSTIFICATION)

4.4.2 DATA INTERPRETATION

5 INDUSTRY INSIGHTS

5.1 DEMOGRAPHIC TRENDS:-

5.1.1 AGE

5.1.2 GENDER

5.1.3 OCCUPATION

5.1.4 FAMILY SIZE

5.2 NUMBER OF CLAIMS BY TYPE

5.2.1 CASHLESS VS. REIMBURSEMENT CLAIMS

5.3 EXTRA CARE/TOP-UP INSURANCE OFFERINGS BY COMPANIES

5.4 INVESTMENT & FUNDING

5.5 PENETRATION OF PRIVATE INSURANCE & DENSITY

5.6 INTERVIEWS WITH KEY HOSPITALS AND INSURANCE COMPANIES

5.7 POLICY SUPPORT FOR LIFE INSURANCE IN SOUTH EAST ASIA

5.7.1 MALAYSIA

5.7.2 PHILIPPINES

5.7.3 THAILAND

5.7.4 VIETNAM

5.8 PUBLIC VS PRIVATE HEALTH INSURANCE

5.9 OTHER KOL SNAPSHOTS

5.1 PREMIUM/COPAY/COINSURANCE

6 REGULATORY FRAMWORK

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 INCREASING COST FOR MEDICAL SERVICES

7.1.2 GROWING NUMBER OF DAY CARE PROCEDURES

7.1.3 MANDATORY OPTING FOR HEALTH INSURANCE IN PUBLIC AND PRIVATE SECTOR

7.1.4 INCREASING OLD AGE POPULATION

7.2 RESTRAINTS

7.2.1 HIGH COST OF PREMIUM

7.2.2 STRICT DOCUMENTATION PROCESS FOR CLAIM REIMBURSEMENT

7.3 OPPORTUNITIES

7.3.1 INCREASING AWARENESS ABOUT THE BENEFITS OF HEALTH INSURANCE

7.3.2 INCREASING HEALTH CARE EXPENDITURE

7.3.3 GROWING MEDICAL TOURISM AMONG COUNTRIES

7.4 CHALLENGE

7.4.1 LACK OF AWARENESS REGARDING HEALTH INSURANCE

8 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY TYPE

8.1 OVERVIEW

8.2 INDIVIDUAL HEALTH INSURANCE

8.3 FAMILY HEALTH INSURANCE

8.4 CRITICAL ILLNESS INSURANCE

8.5 DISEASE-SPECIFIC INSURANCE

8.6 OTHERS

9 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY HEALTH PLAN CATEGORY/METAL LEVELS

9.1 OVERVIEW

9.2 BRONZE

9.3 SILVER

9.4 GOLD

9.5 PLATINUM

9.6 OTHERS

10 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY PROVIDER TYPE

10.1 OVERVIEW

10.2 HEALTH MAINTENANCE ORGANIZATIONS (HMOS)

10.3 PREFERRED PROVIDER ORGANIZATIONS (PPOS)

10.4 EXCLUSIVE PROVIDER ORGANIZATIONS (EPOS)

10.5 POINT-OF-SERVICE (POS) PLANS

10.6 HIGH-DEDUCTIBLE HEALTH PLANS (HDHPS)

10.7 OTHERS

11 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY AGE GROUP

11.1 OVERVIEW

11.2 MIDDLE ADULTHOOD (45-64 YEARS)

11.3 YOUNG ADULTHOOD (19-44 YEARS)

11.4 OLDER ADULTHOOD (65 YEARS AND ABOVE)

12 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY DISTRIBUTION CHANNEL

12.1 OVERVIEW

12.2 DIRECT INSURANCE COMPANIES

12.3 INSURANCE AGGREGATORS

12.4 OTHERS

13 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY COUNTRY

13.1 PHILIPPINES

14 PHILIPPINES PRIVATE HEALTH INSURANCE THERMAL INSULATION PACKAGING MARKET, COMPANY LANDSCAPE

14.1 COMPANY SHARE ANALYSIS: PHILIPPINES

14.2 MERGER & ACQUISITION

14.3 EXPANSIONS

14.4 NEW PRODUCT DEVELOPMENT

14.5 PARTNERSHIP

15 SWOT ANALYSIS

16 COMPANY PROFILE

16.1 AETNA INC. (A SUBSIDIARY OF CVS HEALTH)

16.1.1 COMPANY SNAPSHOT

16.1.2 REVENUE ANALYSIS

16.1.3 PRODUCT PORTFOLIO

16.1.4 RECENT DEVELOPMENTS

16.2 CIGNA

16.2.1 COMPANY SNAPSHOT

16.2.2 REVENUE ANALYSIS

16.2.3 PRODUCT PORTFOLIO

16.2.4 RECENT DEVELOPMENTS

16.3 AIA GROUP LIMITED

16.3.1 COMPANY SNAPSHOT

16.3.2 REVENUE ANALYSIS

16.3.3 PRODUCT PORTFOLIO

16.3.4 RECENT UPDATE

16.4 HCF

16.4.1 COMPANY SNAPSHOT

16.4.2 REVENUE ANALYSIS

16.4.3 PRODUCT PORTFOLIO

16.4.4 RECENT UPDATES

16.5 ALLIANZ

16.5.1 COMPANY SNAPSHOT

16.5.2 REVENUE ANALYSIS

16.5.3 PRODUCT PORTFOLIO

16.5.4 RECENT UPDATES

16.6 SUNCORP GROUP

16.6.1 COMPANY SNAPSHOT

16.6.2 REVENUE ANALYSIS

16.6.3 PRODUCT PORTFOLIO

16.6.4 RECENT UPDATES

16.7 MEDIBANK PRIVATE LIMITED

16.7.1 COMPANY SNAPSHOT

16.7.2 REVENUE ANALYSIS

16.7.3 PRODUCT PORTFOLIO

16.7.4 RECENT DEVELOPMENTS

16.8 DAI-ICHI LIFE VIETNAM

16.8.1 COMPANY SNAPSHOT

16.8.2 PRODUCT PORTFOLIO

16.8.3 RECENT UPDATE

16.9 HSBC GROUP

16.9.1 COMPANY SNAPSHOT

16.9.2 REVENUE ANALYSIS

16.9.3 PRODUCT PORTFOLIO

16.9.4 RECENT UPDATE

16.1 ACCURO HEALTH INSURANCE

16.10.1 COMPANY SNAPSHOT

16.10.2 PRODUCT PORTFOLIO

16.10.3 RECENT UPDATE

16.11 AIG ASIA PACIFIC INSURANCE PTE. LTD

16.11.1 COMPANY SNAPSHOT

16.11.2 PRODUCT PORTFOLIO

16.11.3 RECENT UPDATE

16.12 ASSICURANZIONI GENERALI S.P.A.

16.12.1 COMPANY SNAPSHOT

16.12.2 FINANCIAL ANALYSIS

16.12.3 PRODUCT PORTFOLIO

16.12.4 RECENT UPDATES

16.13 AXA

16.13.1 COMPANY SNAPSHOT

16.13.2 REVENUE ANALYSIS

16.13.3 PRODUCT PORTFOLIO

16.13.4 RECENT UPDATE

16.14 BNI LIFE

16.14.1 COMPANY SNAPSHOT

16.14.2 REVENUE ANALYSIS

16.14.3 PRODUCT PORTFOLIO

16.14.4 RECENT UPDATES

16.15 BUPA GLOBAL

16.15.1 COMPANY SNAPSHOT

16.15.2 PRODUCT PORTFOLIO

16.15.3 RECENT UPDATE

16.16 ETIQA

16.16.1 COMPANY SNAPSHOT

16.16.2 PRODUCT PORTFOLIO

16.16.3 RECENT UPDATE

16.17 GREAT EASTERN HOLDINGS LIMITED

16.17.1 COMPANY SNAPSHOT

16.17.2 PRODUCT PORTFOLIO

16.17.3 RECENT UPDATE

16.18 HONG LEONG ASSURANCE BERHAD

16.18.1 COMPANY SNAPSHOT

16.18.2 PRODUCT PORTFOLIO

16.18.3 RECENT UPDATES

16.19 INCOME

16.19.1 COMPANY SNAPSHOT

16.19.2 PRODUCT PORTFOLIO

16.19.3 RECENT UPDATES

16.2 MANULIFE HOLDINGS BERHAD

16.20.1 COMPANY SNAPSHOT

16.20.2 REVENUE ANALYSIS

16.20.3 PRODUCT PORTFOLIO

16.20.4 RECENT UPDATES

16.21 NIB NZ LIMITED

16.21.1 COMPANY SNAPSHOT

16.21.2 PRODUCT PORTFOLIO

16.21.3 RECENT UPDATE

16.22 NOW HEALTH INTERNATIONAL

16.22.1 COMPANY SNAPSHOT

16.22.2 PRODUCT PORTFOLIO

16.22.3 RECENT DEVELOPMENTS

16.23 PACIFIC CROSS

16.23.1 COMPANY SNAPSHOT

16.23.2 PRODUCT PORTFOLIO

16.23.3 RECENT UPDATE

16.24 PARTNERS LIFE

16.24.1 COMPANY SNAPSHOT

16.24.2 PRODUCT PORTFOLIO

16.24.3 RECENT UPDATES

16.25 PRUDENTIAL ASSURANCE MALAYSIA BERHAD

16.25.1 COMPANY SNAPSHOT

16.25.2 PRODUCT PORTFOLIO

16.25.3 RECENT UPDATE

16.26 RAFFLES MEDICAL GROUP

16.26.1 COMPANY SNAPSHOT

16.26.2 REVENUE ANALYSIS

16.26.3 PRODUCT PORTFOLIO

16.26.4 RECENT UPDATE

16.27 SOUTHERN CROSS

16.27.1 COMPANY SNAPSHOT

16.27.2 PRODUCT PORTFOLIO

16.27.3 RECENT UPDATES

16.28 THE ROYAL AUTOMOBILE CLUB OF WA (INC.).

16.28.1 COMPANY SNAPSHOT

16.28.2 PRODUCT PORTFOLIO

16.28.3 RECENT UPDATES

16.29 TOKIO MARINE

16.29.1 COMPANY SNAPSHOT

16.29.2 PRODUCT PORTFOLIO

16.29.3 RECENT UPDATE

16.3 UNIMED

16.30.1 COMPANY SNAPSHOT

16.30.2 PRODUCT PORTFOLIO

16.30.3 RECENT UPDATES

16.31 ZURICH

16.31.1 COMPANY SNAPSHOT

16.31.2 REVENUE ANALYSIS

16.31.3 PRODUCT PORTFOLIO

16.31.4 RECENT UPDATES

17 QUESTIONNAIRES

18 RELATED REPORTS

表格列表

TABLE 1 NUMBER OF ADULTS HAVE PRIVATE HEALTH INSURANCE, BY AGE GROUP, MILLION, 2021

TABLE 2 NUMBER OF ADULTS HAVE PRIVATE HEALTH INSURANCE, BY INSURANCE COMPANY, MILLION, 2021

TABLE 3 NUMBER OF ADULTS HAVE PRIVATE HEALTH INSURANCE, BY PROVIDER TYPE, MILLION, 2021

TABLE 4 NEW ZEALAND PRIVATE HEALTH INSURANCE MARKET, BY AGE GROUP, 2020-2029 (USD MILLION)

TABLE 5 DETAILS OF AETNA INC. (A SUBSIDIARY OF CVS HEALTH) OF HEALTH MAINTENANCE ORGANIZATIONS (HMOS), BY TYPE , USD MILLION, 2021

TABLE 6 DETAILS OF AETNA INC. (A SUBSIDIARY OF CVS HEALTH) OF PREFERRED PROVIDER ORGANIZATIONS (PPOS), BY TYPE , USD MILLION, 2021

TABLE 7 DETAILS OF AETNA INC. (A SUBSIDIARY OF CVS HEALTH) OF EXCLUSIVE PROVIDER ORGANIZATIONS (EPOS), BY TYPE , USD MILLION, 2021

TABLE 8 DETAILS OF AETNA INC. (A SUBSIDIARY OF CVS HEALTH) OF POINT-OF-SERVICE (POS) PLANS, BY TYPE , USD MILLION, 2021

TABLE 9 DETAILS OF AETNA INC. (A SUBSIDIARY OF CVS HEALTH) OF HIGH-DEDUCTIBLE HEALTH PLANS (HDHPS), BY TYPE , USD MILLION, 2021

TABLE 10 DETAILS OF AETNA INC. (A SUBSIDIARY OF CVS HEALTH) OF OTHERS, BY TYPE , USD MILLION, 2021

TABLE 11 DETAILS OF CIGNA OF HEALTH MAINTENANCE ORGANIZATIONS (HMOS), BY TYPE , USD MILLION, 2021

TABLE 12 DETAILS OF CIGNA OF PREFERRED PROVIDER ORGANIZATIONS (PPOS), BY TYPE , USD MILLION, 2021

TABLE 13 DETAILS OF CIGNA OF EXCLUSIVE PROVIDER ORGANIZATIONS (EPOS), BY TYPE , USD MILLION, 2021

TABLE 14 DETAILS OF CIGNA OF POINT-OF-SERVICE (POS) PLANS, BY TYPE , USD MILLION, 2021

TABLE 15 DETAILS OF CIGNA OF HIGH-DEDUCTIBLE HEALTH PLANS (HDHPS), BY TYPE , USD MILLION, 2021

TABLE 16 DETAILS OF CIGNA OF OTHERS, BY TYPE , USD MILLION, 2021

TABLE 17 DETAILS OF AIA GROUP LIMITED OF HEALTH MAINTENANCE ORGANIZATIONS (HMOS), BY TYPE , USD MILLION, 2021

TABLE 18 DETAILS OF AIA GROUP LIMITED OF PREFERRED PROVIDER ORGANIZATIONS (PPOS), BY TYPE , USD MILLION, 2021

TABLE 19 DETAILS OF AIA GROUP LIMITED OF EXCLUSIVE PROVIDER ORGANIZATIONS (EPOS), BY TYPE , USD MILLION, 2021

TABLE 20 DETAILS OF AIA GROUP LIMITED OF POINT-OF-SERVICE (POS) PLANS, BY TYPE , USD MILLION, 2021

TABLE 21 DETAILS OF AIA GROUP LIMITED OF HIGH-DEDUCTIBLE HEALTH PLANS (HDHPS), BY TYPE , USD MILLION, 2021

TABLE 22 DETAILS OF AIA GROUP LIMITED OF OTHERS, BY TYPE , USD MILLION, 2021

TABLE 23 CHIEF MEDICAL OFFICER

TABLE 24 LIST OF DAY CARE PROCEDURES

TABLE 25 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 26 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY HEALTH PLAN CATEGORY/METAL LEVELS, 2020-2029 (USD MILLION)

TABLE 27 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY PROVIDER TYPE, 2020-2029 (USD MILLION)

TABLE 28 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY AGE GROUP, 2020-2029 (USD MILLION)

TABLE 29 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 30 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 31 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 32 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY HEALTH PLAN CATEGORY/METAL LEVELS, 2020-2029 (USD MILLION)

TABLE 33 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY PROVIDER TYPE, 2020-2029 (USD MILLION)

TABLE 34 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY AGE GROUP, 2020-2029 (USD MILLION)

TABLE 35 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

图片列表

FIGURE 1 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: SEGMENTATION

FIGURE 2 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: DATA TRIANGULATION

FIGURE 3 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: DROC ANALYSIS

FIGURE 4 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: PHILIPPINES VS. REGIONAL MARKET ANALYSIS

FIGURE 5 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: THE AGE GROUP LIFE LINE CURVE

FIGURE 7 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: MULTIVARIATE MODELLING

FIGURE 8 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 9 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: DBMR MARKET POSITION GRID

FIGURE 10 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: THE MARKET CHALLENGE MATRIX

FIGURE 11 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: VENDOR SHARE ANALYSIS

FIGURE 12 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: SEGMENTATION

FIGURE 13 MANDATORY OPTING FOR HEALTH INSURANCE IN PUBLIC AND PRIVATE SECTOR IS DRIVING THE PHILIPPINES PRIVATE HEALTH INSURANCE MARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 14 INDIVIDUAL HEALTH INSURANCE SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE PHILIPPINES PRIVATE HEALTH INSURANCE MARKET IN 2022 & 2029

FIGURE 15 SOUTH EAST ASIA PRIVATE HEALTH INSURANCE MARKET: PESTEL ANALYSIS

FIGURE 16 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGE OF PHILIPPINES PRIVATE HEALTH INSURANCE MARKET

FIGURE 17 HEALTHCARE EXPENDITURE IN MALAYSIA, (RM MILLION)

FIGURE 18 MALAYSIA REVENUE TRAVEL INDUSTRY SIZE, BY REVENUE (RM MILLION)

FIGURE 19 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY TYPE, 2021

FIGURE 20 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY HEALTH PLAN CATEGORY/METAL LEVELS, 2021

FIGURE 21 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY PROVIDER TYPE, 2021

FIGURE 22 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY AGE GROUP, 2021

FIGURE 23 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY DISTRIBUTION CHANNEL, 2021

FIGURE 24 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: SNAPSHOT (2021)

FIGURE 25 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY COUNTRY (2021)

FIGURE 26 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY COUNTRY (2022 & 2029)

FIGURE 27 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY COUNTRY (2021 & 2029)

FIGURE 28 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: BY TYPE (2022-2029)

FIGURE 29 PHILIPPINES PRIVATE HEALTH INSURANCE MARKET: COMPANY SHARE 2021 (%)

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。