Global Polyethylene Terephthalate Pet Foam Market

市场规模(十亿美元)

CAGR :

%

USD

434.78 Million

USD

747.03 Million

2025

2033

USD

434.78 Million

USD

747.03 Million

2025

2033

| 2026 –2033 | |

| USD 434.78 Million | |

| USD 747.03 Million | |

| % | |

|

全球聚對苯二甲酸乙二醇酯(PET)泡棉市場細分,依原料(原生聚對苯二甲酸乙二醇酯(PET)及再生聚對苯二甲酸乙二醇酯(PET))、目標(低密度聚對苯二甲酸乙二醇酯( PET)泡沫及高密度聚對苯二甲酸乙二醇酯(PET)泡沫)、終端用戶產業(風能、汽車、航太與國防、船舶、建築與施工、包裝及其他)劃分-產業趨勢及至2033年的預測

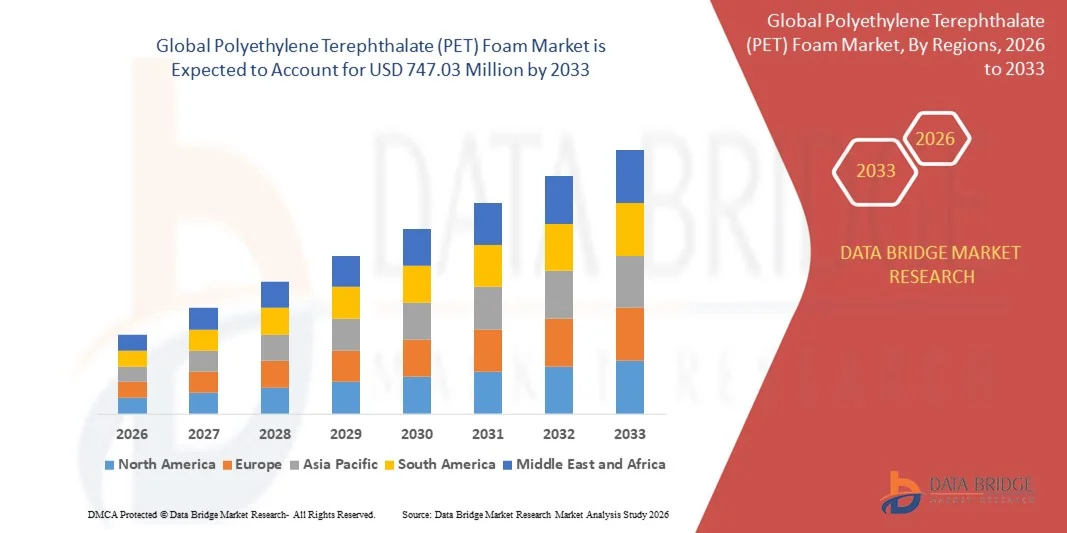

聚對苯二甲酸乙二醇酯(PET)泡沫市場規模

- 2025年全球聚對苯二甲酸乙二醇酯(PET)泡沫市場規模為4.3478億美元,預計到2033年將達到7.4703億美元,預測期內 複合年增長率為7.00%。

- 市場成長主要得益於風能、汽車、船舶和建築等應用領域對輕質高性能芯材的日益普及,而PET泡棉材料在強度、耐久性和可回收性方面實現了最佳平衡。

- 此外,對永續性、輕量化和高性價比複合材料解決方案的日益重視,正使PET泡沫成為傳統芯材的首選替代品,加速其在結構和保溫應用領域的滲透,並顯著推動整體市場成長。

聚對苯二甲酸乙二醇酯(PET)泡沫市場分析

- 聚對苯二甲酸乙二醇酯(PET)泡沫材料作為夾層複合材料的結構芯材,因其高強度重量比、抗疲勞性和耐濕性,已成為現代風力渦輪機葉片、汽車結構、船舶和建築材料的關鍵組成部分。

- 聚對苯二甲酸乙二醇酯(PET)泡沫塑膠需求的成長主要受以下因素驅動:再生能源專案的快速擴張、為提高燃油效率和減少排放而日益重視輕質材料,以及工業應用中可回收和環保材料的日益普及。

- 由於風能裝置容量的快速成長、汽車製造業的蓬勃發展以及輕質複合材料應用的日益普及,亞太地區預計將在2025年佔據聚對苯二甲酸乙二醇酯(PET)泡沫市場的主導地位,市場份額約為35%。

- 由於風能裝置容量增加、汽車和航空航太領域對輕質材料的需求不斷增長,以及對可回收複合材料的重視,預計北美將在預測期內成為聚對苯二甲酸乙二醇酯(PET)泡沫市場成長最快的地區。

- 由於其卓越的機械強度、穩定的品質以及在高負荷結構應用中可靠的性能,預計到2025年,原生聚對苯二甲酸乙二醇酯(PET)將以62.5%的市場份額佔據市場主導地位。製造商更傾向於將原生聚對苯二甲酸乙二醇酯(PET)泡沫用於風能、航空航太和船舶領域,因為其在應力作用下表現出可預測的性能和長期耐久性。其更高的純度確保了與樹脂和複合材料更好的黏合性,這對於安全敏感型應用至關重要。標準化等級的供應進一步鞏固了其在大型工業項目中的主導地位。

報告範圍及聚對苯二甲酸乙二醇酯(PET)泡沫市場細分

|

屬性 |

聚對苯二甲酸乙二醇酯(PET)泡沫市場關鍵洞察 |

|

涵蓋部分 |

|

|

覆蓋國家/地區 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機遇 |

|

|

加值資料資訊集 |

除了對市場狀況(如市場價值、成長率、細分、地理覆蓋範圍和主要參與者)的洞察之外,Data Bridge Market Research 精心編制的市場報告還包括進出口分析、產能概覽、生產消費分析、價格趨勢分析、氣候變遷情境、供應鏈分析、價值鏈分析、原材料/消耗標準概覽、供應商選擇、PESTLE 分析、五力分析和監管框架。 |

聚對苯二甲酸乙二醇酯(PET)泡沫市場趨勢

增加可回收和可持續PET泡沫芯材的使用

- A significant trend in the Polyethylene Terephthalate (PET) foam market is the increasing adoption of recyclable and sustainable core materials across composite-intensive industries, driven by growing environmental regulations and corporate sustainability targets. PET foam is gaining preference over traditional core materials due to its recyclability, lower environmental impact, and ability to meet structural performance requirements in demanding applications

- For instance, Gurit Holding AG has expanded its recyclable PET foam product portfolio for wind energy and marine applications, supporting circular economy objectives while maintaining mechanical strength and durability. Such initiatives are reinforcing PET foam’s position as a sustainable alternative in large-scale composite structures

- The wind energy sector is increasingly integrating PET foam cores in turbine blades as manufacturers seek materials that support lifecycle sustainability without compromising fatigue resistance. This trend is strengthening PET foam adoption in both onshore and offshore wind projects

- Automotive manufacturers are also incorporating recyclable PET foam into lightweight vehicle components to support emission reduction and end-of-life recyclability goals. This is contributing to broader acceptance of PET foam within transportation applications

- Building and construction activities are witnessing rising use of PET foam for insulation and structural panels, where sustainability certifications and energy efficiency standards are becoming decisive purchasing factors. This is expanding PET foam usage in green building projects

- Overall, the growing emphasis on sustainability and recyclability across industries is reinforcing PET foam’s role as a future-ready core material, supporting long-term market expansion

Polyethylene Terephthalate (PET) Foam Market Dynamics

Driver

Rising Demand for Lightweight and High-Strength Composite Structures

- The increasing demand for lightweight yet high-strength composite materials across wind energy, automotive, aerospace, and marine sectors is a primary driver for the PET foam market. PET foam offers an optimal balance of mechanical strength, weight reduction, and durability, making it suitable for load-bearing sandwich structures

- For instance, Toray Industries, Inc. utilizes advanced PET foam solutions in composite applications where weight reduction and structural performance are critical, particularly in aerospace and transportation-related uses. Such adoption highlights the growing reliance on PET foam in performance-driven environments

- In the automotive sector, manufacturers are adopting PET foam to achieve lightweighting objectives that improve fuel efficiency and electric vehicle range. PET foam’s compatibility with composite manufacturing processes enhances its appeal for structural and semi-structural components

- Marine and aerospace industries are also driving demand as PET foam provides resistance to moisture, fatigue, and harsh operating conditions. These performance advantages are strengthening its adoption in high-value applications

- The continued shift toward lightweight composite engineering across industries is reinforcing this driver, positioning PET foam as a critical material supporting modern structural design requirements

Restraint/Challenge

High Processing and Initial Manufacturing Costs

- The PET foam market faces challenges related to high initial processing and manufacturing costs, particularly when compared with conventional core materials. Advanced processing requirements and specialized composite integration increase overall production expenses for manufacturers and end users

- For instance, BASF SE highlights that producing high-performance PET foam grades requires controlled processing conditions and precise material formulation, which adds to capital and operational costs. These cost factors can limit adoption in price-sensitive applications

- Manufacturing PET foam for structural uses involves energy-intensive processes and strict quality control standards to ensure consistent density and mechanical performance. These requirements raise production complexity and cost structures

- Small and mid-sized manufacturers may face difficulties scaling PET foam production due to the need for specialized equipment and skilled labor. This can constrain supply and affect market penetration in emerging regions

- As a result, high initial costs remain a key challenge, requiring manufacturers to focus on process optimization, economies of scale, and technological advancements to improve cost competitiveness while maintaining product performance

Polyethylene Terephthalate (PET) Foam Market Scope

The market is segmented on the basis of raw material, target density, and end use industry.

- By Raw Material

On the basis of raw material, the Polyethylene Terephthalate (PET) foam market is segmented into virgin Polyethylene Terephthalate (PET) and recycled Polyethylene Terephthalate (PET). The virgin Polyethylene Terephthalate (PET) segment dominated the market with the largest revenue share of 62.5% in 2025, driven by its superior mechanical strength, consistent quality, and reliable performance across high-load structural applications. Manufacturers prefer virgin Polyethylene Terephthalate (PET) foam for wind energy, aerospace, and marine uses due to its predictable behavior under stress and long-term durability. Its higher purity ensures better bonding with resins and composites, which is critical for safety-sensitive applications. The availability of standardized grades further supports its dominance in large-scale industrial projects.

The recycled Polyethylene Terephthalate (PET) segment is expected to register the fastest growth from 2026 to 2033, supported by increasing sustainability mandates and circular economy initiatives across manufacturing industries. Growing emphasis on reducing carbon footprints is encouraging end users to adopt recycled Polyethylene Terephthalate (PET) foam without compromising structural integrity. Advancements in recycling technologies are improving material consistency, making recycled Polyethylene Terephthalate (PET) suitable for automotive, construction, and packaging applications. Cost advantages over virgin material and strong regulatory support are accelerating adoption across emerging and developed markets.

- By Target

On the basis of target density, the Polyethylene Terephthalate (PET) foam market is segmented into low-density Polyethylene Terephthalate (PET) foam and high-density Polyethylene Terephthalate (PET) foam. The high-density Polyethylene Terephthalate (PET) foam segment accounted for the dominant revenue share in 2025, driven by its high compressive strength, excellent fatigue resistance, and suitability for load-bearing structures. This segment is widely used in wind turbine blades, marine hulls, and aerospace components where structural stability and long service life are essential. Its resistance to moisture and chemicals further enhances performance in harsh operating environments. Strong demand from renewable energy and defense sectors continues to reinforce its market leadership.

The low-density Polyethylene Terephthalate (PET) foam segment is projected to witness the fastest growth during the forecast period, fueled by rising demand for lightweight materials in automotive interiors, building insulation, and packaging. Low-density Polyethylene Terephthalate (PET) foam offers weight reduction benefits while maintaining adequate thermal and acoustic insulation properties. Its ease of processing and cost efficiency make it attractive for high-volume applications. Increasing focus on energy-efficient buildings and lightweight vehicle design is supporting rapid expansion of this segment.

- By End Use Industry

On the basis of end use industry, the Polyethylene Terephthalate (PET) foam market is segmented into wind energy, automotive, aerospace and defense, marine, building and construction, packaging, and others. The wind energy segment dominated the market in 2025, driven by the extensive use of Polyethylene Terephthalate (PET) foam as a core material in wind turbine blades. Polyethylene Terephthalate (PET) foam provides high strength-to-weight ratio, fatigue resistance, and recyclability, which are essential for large and durable turbine structures. Rising investments in onshore and offshore wind projects globally are sustaining strong demand. Its compatibility with automated manufacturing processes further supports widespread adoption in this segment.

預計在2026年至2033年期間,汽車產業將以最快的速度成長,這主要得益於市場對輕量化、節能型和電動車日益增長的需求。聚對苯二甲酸乙二醇酯(PET)泡棉材料因其抗衝擊性和熱穩定性,在汽車結構件、內裝和電池外殼等領域正得到越來越廣泛的應用。汽車製造商正越來越多地使用PET泡沫材料來實現減排目標並提高車輛續航里程。泡沫加工製程的持續創新和設計靈活性的提升,正在加速PET泡沫材料在汽車產業的滲透。

聚對苯二甲酸乙二醇酯(PET)泡沫市場區域分析

- 亞太地區在聚對苯二甲酸乙二醇酯(PET)泡棉市場佔據主導地位,預計到2025年將佔據約35%的市場份額,這主要得益於風能裝置容量的快速增長、汽車製造業的蓬勃發展以及輕質複合材料應用的日益普及。

- 該地區強大的製造業基礎、低成本原材料的供應以及對再生能源和基礎設施項目不斷增長的投資,正在加速PET泡沫的需求成長。

- 政府的支持性政策、不斷擴大的複合材料製造能力以及發展中經濟體的快速工業化,正在推動PET泡沫材料在結構和保溫領域的應用。

中國聚對苯二甲酸乙二酯(PET)泡沫市場洞察

預計到2025年,中國將佔亞太地區聚對苯二甲酸乙二醇酯(PET)泡沫市場最大份額,這主要得益於其在風力渦輪機製造、大規模建築活動以及強大的複合材料生產能力方面的優勢。中國大力發展再生能源和輕量交通材料,也持續推動市場需求。此外,完善的供應鏈和國內產能也鞏固了中國的領先地位。

印度聚對苯二甲酸乙二醇酯(PET)泡沫市場洞察

印度正經歷亞太地區最快的成長,這主要得益於風能項目的快速發展、汽車產量的提升以及建築領域對輕質材料的日益廣泛應用。政府支持再生能源產能擴張和基礎建設的各項舉措,正在推動聚對苯二甲酸乙二醇酯(PET)泡沫材料的普及應用。國內複合材料製造業投資的不斷成長,也進一步促進了市場的強勁發展動能。

歐洲聚對苯二甲酸乙二醇酯(PET)泡沫市場洞察

在歐洲,聚對苯二甲酸乙二醇酯(PET)泡沫市場穩步成長,這主要得益於嚴格的可持續發展法規、可回收芯材的高普及率以及風能和汽車行業的強勁需求。該地區尤其註重結構應用領域輕質、高性能且符合環保標準的材料。離岸風電項目和電動車領域投資的不斷增長也為市場的長期發展提供了支撐。

德國聚對苯二甲酸乙二醇酯(PET)泡沫市場洞察

德國的聚對苯二甲酸乙二醇酯(PET)泡沫市場受益於其先進的汽車產業、強大的風能基礎設施以及在複合材料工程領域的領先地位。德國對輕量化汽車設計、能源效率和可回收材料的重視,推動了PET泡棉的使用。強大的研發能力和產業合作進一步促進了PET泡沫在多個終端應用產業的普及。

英國聚對苯二甲酸乙二醇酯(PET)泡沫市場洞察

英國市場受惠於海上風能計畫的蓬勃發展、對永續建築材料需求的成長以及先進複合材料的日益普及。對再生能源目標和輕質結構材料的重視,正在推動聚對苯二甲酸乙二醇酯(PET)泡沫材料的需求成長。對海洋和風能應用領域的投資也持續支撐著市場擴張。

北美聚對苯二甲酸乙二醇酯(PET)泡沫市場洞察

預計2026年至2033年間,北美將以最快的複合年增長率成長,主要驅動力包括風能裝置容量的增加、汽車和航空航太領域對輕質材料需求的日益增長,以及對可回收複合材料的大力發展。對再生能源基礎設施和先進製造技術的投資不斷增長,也是關鍵的成長動力。

美國聚對苯二甲酸乙二醇酯(PET)泡沫市場洞察

預計到2025年,美國將佔據北美聚對苯二甲酸乙二醇酯(PET)泡棉市場最大份額,這主要得益於其龐大的風能裝置容量、強勁的航空航太和汽車產業,以及對結構芯材的旺盛需求。對永續性、輕量化和本土複合材料製造的重視,正在加速聚對苯二甲酸乙二醇酯(PET)泡沫的普及應用。成熟的製造商和先進的生產能力進一步鞏固了美國的領先地位。

聚對苯二甲酸乙二醇酯(PET)泡沫市場份額

聚對苯二甲酸乙二醇酯(PET)泡沫產業主要由一些成熟企業主導,其中包括:

- JSP株式會社(日本)

- 阿樂斯國際有限公司(盧森堡)

- 陶氏公司(美國)

- Zotefoams Plc(英國)

- 希悅爾公司(美國)

- Carbon-Core 公司(美國)

- 巴斯夫股份公司(德國)

- 日本INOAC株式會社

- 威斯康辛州泡棉產品(美國)

- 亨斯邁國際有限責任公司(美國)

- Palziv有限公司(以色列)

- Trecolan GmbH(德國)

- Pregis LLC(美國)

- 三井化學美國公司(美國)

- 金卡株式會社(日本)

- 東麗株式會社(日本)

- Gurit Holding AG(瑞士)

全球聚對苯二甲酸乙二醇酯(PET)泡棉市場最新發展動態

- 2025年10月,3M公司與領先的汽車製造商啟動了一項合作開發計劃,旨在研發先進的PET泡棉解決方案,以提升車輛性能和燃油效率。此次合作透過加速下一代汽車採用輕質芯材,加強了PET泡棉市場的創新管道。該合作將3M的材料專長與汽車製造商(OEM)的需求結合,提升了3M的市場地位,同時也拓展了PET泡棉在汽車領域的應用範圍。

- 2025年9月,沙烏地基礎工業公司(SABIC)推出了一系列全新的永續PET泡棉產品,專為注重環保的產業量身打造。此舉反映了市場對可回收和低碳材料的日益增長的需求,進一步鞏固了PET泡沫作為傳統芯材可持續替代品的地位。透過滿足永續發展驅動的需求,SABIC正在增強其競爭優勢,並支持PET泡沫在建築、運輸和工業應用領域的更廣泛應用。

- 2025年8月,東麗株式會社宣布對新建PET泡沫生產設施進行重大投資,以擴大其產能。此舉將直接滿足全球日益增長的需求,尤其是在航空航太領域,輕質高強度材料至關重要。此次擴建將提升供應鏈的韌性,並使東麗得以佔據更高價值PET泡棉應用市場更大的份額。

- 2025年6月,阿姆斯勒(Armacell)擴展了其PET泡沫產品系列,新增了專為風能和海洋應用設計的高性能等級產品。此舉滿足了大型複合材料結構對耐用、抗疲勞芯材的需求,從而增強了市場競爭力。擴展後的產品組合使阿姆斯勒能夠進一步鞏固其在再生能源項目和高成長海洋領域的市場地位。

- 2025年4月,Gurit Holding AG透過升級生產線,提升了其PET泡沫的生產能力,並提升了生產效率與產品品質穩定性。這項策略性舉措旨在滿足風能和交通運輸業日益增長的需求,同時降低生產成本。此次升級增強了Gurit大規模生產高品質PET泡沫的能力,有助於其在快速成長的市場中保持更強的競爭力。

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。