Global Disposable Intravenous Products Market

市场规模(十亿美元)

CAGR :

%

USD

3.16 Billion

USD

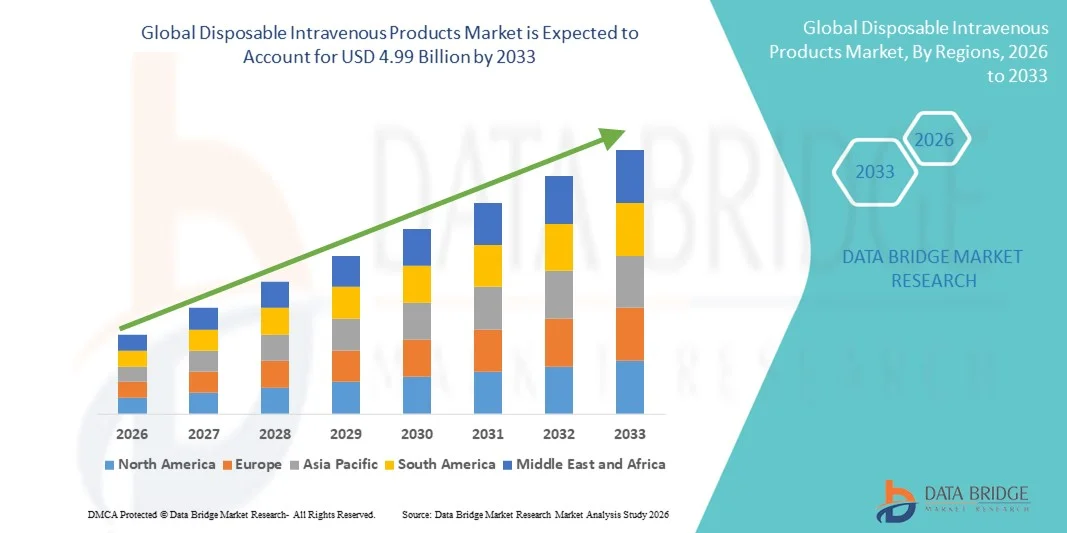

4.99 Billion

2025

2033

USD

3.16 Billion

USD

4.99 Billion

2025

2033

| 2026 –2033 | |

| USD 3.16 Billion | |

| USD 4.99 Billion | |

| % | |

|

全球一次性靜脈輸液產品市場細分,按產品(靜脈導管、輸液器、輸液裝置、固定裝置、止回閥和旋塞、滴注室、無針連接器及其他)、最終用戶(醫院和診所、家庭護理)劃分——行業趨勢及至2033年的預測

一次性靜脈輸液產品市場規模

- 2025年全球一次性靜脈輸液產品市場規模為31.6億美元 ,預計 2033年將達49.9億美元,預測期內 複合年增長率為5.90%。

- 市場成長主要受住院人數增加、慢性病盛行率上升以及急診和長期照護機構對靜脈輸液需求不斷增長的推動,導致醫院、診所和門診中心對一次性靜脈輸液產品的需求增加。

- 此外,對感染預防的日益重視、對病人安全的嚴格監管標準以及對一次性無菌醫療器材的偏好,正使一次性靜脈輸液產品成為現代醫療保健服務的重要組成部分。這些因素共同推動了一次性靜脈輸液產品解決方案的普及,顯著促進了該行業的成長。

一次性靜脈輸液產品市場分析

- 一次性靜脈輸液產品,包括靜脈導管、輸液器、注射器和輸液管,是現代醫療保健服務的重要組成部分,廣泛應用於醫院、診所和門診護理機構,以確保安全、高效、無菌地輸注液體、藥物、血液製品和營養素。

- 一次性靜脈輸液產品需求的不斷增長主要受以下因素驅動:慢性病患病率上升、外科手術和急診手術增多、對感染預防和患者安全日益重視,以及人們強烈傾向於使用一次性醫療器械以最大限度降低交叉感染風險。

- 北美地區在一次性靜脈輸液產品市場佔據主導地位,預計到2025年將佔據約38.5%的最大市場份額,這得益於其先進的醫療基礎設施、較高的住院率、安全型靜脈輸液裝置的廣泛應用以及嚴格的監管標準。美國之所以佔據主要市場份額,是因為其手術量大,且領先製造商不斷進行產品創新。

- 預計在預測期內,亞太地區將成為一次性靜脈輸液產品市場成長最快的地區,這主要得益於醫療基礎設施的擴張、醫療支出的增長、患者數量的增加以及新興經濟體醫院和急診服務可及性的提高。

- 2025年,靜脈導管細分市場將佔據最大的市場份額,達到36.8%,這主要得益於其在醫院、診所和急診護理機構的廣泛和常規使用。

報告範圍及拋棄式靜脈輸液產品市場細分

|

屬性 |

一次性靜脈輸液產品關鍵市場洞察 |

|

涵蓋部分 |

|

|

覆蓋國家/地區 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

•百特國際公司(美國) |

|

市場機遇 |

|

|

加值資料資訊集 |

除了對市場狀況(如市場價值、成長率、細分、地理覆蓋範圍和主要參與者)的洞察之外,Data Bridge Market Research 精心編制的市場報告還包括深入的專家分析、患者流行病學、產品線分析、定價分析和監管框架。 |

拋棄式靜脈輸液產品市場趨勢

透過創新和安全改進提高效率

- A significant and accelerating trend in the global disposable intravenous products market is the continuous advancement in product design, material quality, and safety mechanisms to reduce infection risks and improve clinical efficiency. Manufacturers are increasingly focusing on needle-free systems, closed IV delivery systems, and improved flow control to enhance patient safety and healthcare worker protection

- For instance, the growing adoption of needle-free IV connectors and safety-engineered infusion sets has helped minimize the risk of needlestick injuries and catheter-related bloodstream infections (CRBSIs). These innovations are being widely implemented across hospitals, ambulatory surgical centers, and home healthcare settings

- Material innovations, including the use of medical-grade plastics and DEHP-free materials, are gaining traction as healthcare providers prioritize patient safety and regulatory compliance. Disposable IV products are also being designed for improved compatibility with automated infusion pumps and modern clinical workflows

- The increasing emphasis on single-use medical devices to prevent cross-contamination has further reinforced demand for disposable intravenous products, particularly in critical care units, oncology, and emergency medicine

- This trend toward safer, more reliable, and user-friendly disposable IV solutions is reshaping purchasing decisions among healthcare providers, encouraging manufacturers to invest in R&D and product differentiation

- Overall, continuous innovation aimed at infection control, ease of use, and regulatory adherence is driving the evolution of the disposable intravenous products market globally

Disposable Intravenous Products Market Dynamics

Driver

Rising Hospitalization Rates and Growing Demand for Infection Control

- The increasing number of hospital admissions, surgical procedures, and chronic disease cases worldwide is a major driver of demand for disposable intravenous products. IV therapy remains a critical component of fluid administration, medication delivery, blood transfusions, and nutritional support

- For instance, the rising prevalence of chronic conditions such as cancer, cardiovascular diseases, and diabetes has significantly increased the need for long-term and repeated IV treatments, thereby boosting the consumption of disposable IV catheters, infusion sets, and accessories

- Heightened awareness regarding hospital-acquired infections (HAIs) has led healthcare facilities to adopt disposable IV products as a standard infection-prevention measure, replacing reusable alternatives wherever possible

- In addition, the rapid growth of home healthcare and outpatient care services has expanded the use of disposable IV products outside traditional hospital settings, further supporting market growth

- Government initiatives, stricter infection-control guidelines, and investments in healthcare infrastructure—particularly in emerging economies—are also contributing to the sustained demand for disposable intravenous products across the globe

Restraint/Challenge

Environmental Concerns and Cost Pressures

- One of the key challenges facing the disposable intravenous products market is the environmental impact associated with the growing volume of medical waste generated by single-use IV catheters, infusion sets, and related accessories. The widespread reliance on disposable products contributes significantly to plastic waste in healthcare systems worldwide

- For instance, according to reports published by the World Health Organization (WHO), healthcare activities generate millions of tons of medical waste annually, with a substantial portion attributed to disposable medical devices such as intravenous products, prompting hospitals and regulators to reassess waste management practices and sustainability policies

- Disposal and waste management costs associated with disposable IV products can place a financial burden on healthcare facilities, particularly in regions with strict environmental regulations and limited waste-processing infrastructure

- In addition, pricing pressures and reimbursement constraints faced by hospitals and healthcare providers can limit the adoption of premium disposable IV products, especially in cost-sensitive markets

- In low- and middle-income countries, budget limitations often restrict access to advanced disposable IV technologies, leading some facilities to prioritize affordability over enhanced safety or sustainability features

- Addressing these challenges through the development of eco-friendly materials, recyclable components, and cost-efficient manufacturing processes will be critical for sustaining long-term growth in the disposable intravenous products market

Disposable Intravenous Products Market Scope

The market is segmented on the basis of product and end user.

- By Product

根據產品類型,一次性靜脈輸液產品市場可細分為靜脈導管、輸液器、輸液裝置、固定裝置、止回閥和三通閥、滴壺、無針連接器及其他產品。 2025年,靜脈導管細分市場佔據最大的市場份額,達到36.8%,這主要得益於其在醫院、診所和急診等場所的廣泛應用。靜脈導管對於輸液、給藥、輸血和營養支持至關重要,因此在急性和慢性照護中都不可或缺。住院率上升、手術量增加以及慢性病盛行率上升顯著鞏固了該細分市場的主導地位。安全工程導管和抗菌塗層導管等技術進步進一步促進了其應用。每位患者的高使用頻率和頻繁更換的需求也推動了收入成長。急診和重症監護室的強勁需求也促進了市場成長。此外,對感染預防的日益重視也促使醫療機構使用高品質的一次性靜脈導管。

由於人們對預防針刺傷和控制醫院感染的意識不斷提高,預計2026年至2033年間,無針連接器市場將以19.6%的複合年增長率實現最快增長。這些設備可降低血液傳播病原體的風險,並提高病患和醫護人員的安全。監管機構對安全型醫療器材日益重視,也促進了其快速普及。長期靜脈輸液治療和家庭護理環境中日益廣泛的應用進一步加速了市場成長。技術進步提高了輸液效率,並增強了與多種靜脈輸液系統的兼容性,這些都有助於推動市場成長。全球門診護理和輸液治療服務的擴展也進一步鞏固了強勁的複合年增長率。

- 最終用戶

根據最終用戶,一次性靜脈輸液產品市場可分為醫院和診所以及家庭護理兩大類。到2025年,醫院和診所細分市場將佔據最大的市場份額,達到72.4%,這主要得益於患者數量龐大、手術量巨大以及靜脈輸液療法的廣泛應用。醫院高度依賴一次性靜脈輸液產品來維持嚴格的感染控制標準並遵守監管指南。住院人數、急診病例和重症監護治療數量的不斷增長顯著鞏固了該細分市場的主導地位。三級醫院對先進靜脈輸液系統的日益普及也促進了市場份額的成長。此外,熟練的醫護人員和先進的基礎設施也維持了產品的高消費量。醫院擴建和現代化改造投資的增加進一步鞏固了該細分市場的領先地位。

受居家治療和長期靜脈輸液療法日益增長的需求推動,預計2026年至2033年間,居家護理領域將以21.2%的複合年增長率實現最快增長。癌症、糖尿病和腎臟疾病等慢性病盛行率的上升也支撐了對居家輸液服務的需求。便捷安全的輸液產品的進步使得這些產品在非臨床環境中得到更廣泛的應用。與住院治療相比,居家照護的成本優勢也加速了這一成長。老年人口的增長以及對患者舒適度的日益重視進一步推動了需求。居家醫療保健服務提供者的增加和有利的報銷政策也為該領域的持續高速成長做出了貢獻。

一次性靜脈輸液產品市場區域分析

- 北美地區在一次性靜脈輸液產品市場佔據主導地位,預計2025年將佔據約38.5%的最大市場份額。這主要得益於先進的醫療基礎設施、較高的住院率以及醫院和門診機構對安全型靜脈輸液裝置的廣泛應用。

- 該地區受益於嚴格的感染控制法規、一次性醫療產品的廣泛使用以及高額的醫療保健支出,尤其是在急診和重症監護領域。

- 持續的產品創新、領先製造商的強大實力以及高手術量進一步鞏固了北美在醫院和門診護理領域的領先地位。

美國一次性靜脈輸液產品市場洞察

2025年,美國一次性靜脈輸液產品市場將佔據北美最大的收入份額,這主要得益於美國大量的外科手術、急診入院以及需要靜脈輸液治療的慢性病管理。美國完善的醫院網路和對病人安全的高度重視,加速了先進的一次性靜脈導管、無針連接器和輸液配件的普及應用。有利的報銷機制和嚴格的FDA監管促進了安全型醫療器材的使用。居家照護和門診輸液中心靜脈輸液治療的日益普及也進一步推動了市場成長。美國本土製造商對醫療保健現代化持續投入和不斷創新,也持續增強了美國市場的優勢。

歐洲一次性靜脈輸液產品市場洞察

受醫療保健需求成長以及公立和私立醫療系統嚴格的感染防治政策的推動,預計歐洲一次性靜脈輸液產品市場在預測期內將保持穩定的複合年增長率。手術量的增加、人口老化以及慢性病盛行率的上升,都支撐了對一次性靜脈輸液產品的持續需求。歐洲醫療機構強調使用一次性醫療器械,以降低交叉感染風險並符合監管標準。門診護理和住院治療中心的擴張也促進了市場成長。政府對醫療品質和病人安全的大力支持進一步推動了該地區一次性靜脈輸液產品的普及。

英國一次性靜脈輸液產品市場洞察

預計在預測期內,英國一次性靜脈輸液產品市場將以顯著的複合年增長率增長,這主要得益於英國國民醫療服務體系 (NHS) 支出的增加以及對醫院和急診護理服務需求的增長。一次性靜脈輸液裝置的日益普及符合國家感染控制措施和病人安全指南。慢性疾病和癌症治療需要輸液治療,其負擔日益加重,也支持了產品需求。居家照護和門診輸液服務的擴展也推動了市場成長。醫院基礎設施的持續升級和先進靜脈輸液耗材的採購進一步增強了市場前景。

德國一次性靜脈輸液產品市場洞察

德國一次性靜脈輸液產品市場預計將以可觀的複合年增長率成長,這主要得益於其健全的醫療保健體係以及高標準的醫療安全和衛生要求。德國高度重視感染預防和監管合規,加速了醫院和專科診所對一次性靜脈輸液產品的採用。手術量的增加和輸液療法使用量的提高也為市場擴張提供了支持。德國對技術先進的醫療耗材和永續醫療保健實踐的重視也促進了市場的穩定需求。持續的醫院現代化投資進一步鞏固了市場成長。

亞太地區一次性靜脈輸液產品市場洞察

受醫療基礎設施擴張和患者群體快速成長的推動,預計亞洲一次性靜脈輸液產品市場在預測期內將實現最快的複合年增長率。醫療支出增加、住院率上升以及急診和重症監護服務可近性的提高,都推動了市場成長。該地區各國政府正大力投資醫院擴建和感染控制措施。醫療旅遊的興起和衛生意識的提高進一步刺激了對一次性靜脈輸液產品的需求。為預防醫院感染而轉向使用一次性醫療器械,也為該地區市場成長提供了強有力的支持。

日本一次性靜脈輸液產品市場洞察

The Japan disposable intravenous products market is witnessing steady growth, supported by an aging population and increasing demand for long-term and acute care services. High healthcare quality standards and strict infection control practices drive the use of disposable IV consumables. Rising prevalence of chronic conditions requiring continuous infusion therapy supports sustained demand. Japan’s technologically advanced healthcare system enables rapid adoption of safety-engineered IV devices. Expansion of home healthcare services also contributes to market growth.

China Disposable Intravenous Products Market Insight

The China disposable intravenous products market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid expansion of healthcare infrastructure and increasing patient volumes. Rising government investments in hospital development and public health programs support strong demand for disposable IV products. Growing awareness of infection prevention and adoption of single-use medical devices accelerate market penetration. Increasing surgical procedures and emergency care utilization further strengthen demand. The presence of domestic manufacturers offering cost-effective IV consumables also supports widespread adoption across healthcare facilities.

Disposable Intravenous Products Market Share

The Disposable Intravenous Products industry is primarily led by well-established companies, including:

• Baxter International Inc. (U.S.)

• Terumo Corporation (Japan)

• Fresenius Kabi (Germany)

• ICU Medical, Inc. (U.S.)

• Smiths Medical (U.K.)

• Nipro Corporation (Japan)

• Cardinal Health (U.S.)

• Vygon SA (France)

• Teleflex Incorporated (U.S.)

• Merit Medical Systems (U.S.)

• Zhejiang Weigao Group (China)

• Polymedicure Ltd. (India)

• Hindustan Syringes & Medical Devices (India)

• Medtronic plc (Ireland)

• AngioDynamics (U.S.)

• CODAN Medizinische Geräte GmbH (Germany)

• Renax Biomedical (India)

• Sarstedt AG & Co. (Germany)

Latest Developments in Global Disposable Intravenous Products Market

- In July 2021, Becton Dickinson & Company (BD) announced the acquisition of Tepha, Inc., strengthening BD’s capabilities in advanced biomaterials and supporting the development of next-generation resorbable medical devices relevant to disposable IV components

- In May 2022, Fresenius Kabi completed the acquisition of Ivenix, Inc., expanding its portfolio of infusion therapy solutions and enhancing its ability to deliver disposable IV administration sets and infusion system components across global healthcare settings

- 2023年11月,史密斯醫療與美國主要醫院機構合作,採用無針連接器連接靜脈輸液管,旨在減少針刺傷,提高臨床工作流程中使用的一次性靜脈輸液產品的安全性。

- 2023年12月,貝朗醫療股份公司推出了一系列整合人工智慧的智慧輸液泵,旨在提高藥物輸送的精準度並與電子健康記錄系統整合——這些進步將推動相容的一次性輸液器及配件的更高效利用。

- 2024年1月,BD(貝克頓·迪金森公司)推出了新一代封閉式靜脈導管系統,進一步拓展了其靜脈輸液解決方案產品組合。該系統旨在最大限度地減少血液感染,並提高靜脈輸液治療期間的患者安全性。

- 2024年5月,Vygon推出了一款新型封閉式靜脈輸液器,採用抗菌連接器,旨在降低醫院和急診中心的感染風險,這體現了業界對一次性產品感染控制的重視。

- 2024 年 7 月,貝克頓·迪金森公司 (BD) 完成了對 Tepha, Inc. 的收購(一些業內人士指出,這是對支持一次性產品的先進靜脈輸液連接材料的策略性擴張)。

- 2025年4月,BD推出了HemoSphere Alta平台,該平台具備先進的臨床決策支援功能,可用於血流動力學監測;其應用推動了與靜脈輸液治療相關的各種一次性壓力感測器、感測器組件和液體管理配件的廣泛使用。

- 2025年5月,費森尤斯卡比完成了對Ivenix的收購,進一步豐富了其輸液治療產品組合,並在全球範圍內拓展了兼容的一次性靜脈輸液管路套裝和連接器產品,這些產品是現代靜脈輸液的重要組成部分。

- 2025年3月,ICU Medical擴展了其產品組合,新增了預混靜脈輸液產品,包括專為門診輸液中心設計的新型即用型電解質輸液袋和平衡晶體輸液袋,從而支持一次性靜脈輸液袋及相關配件產品的更廣泛應用。

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。