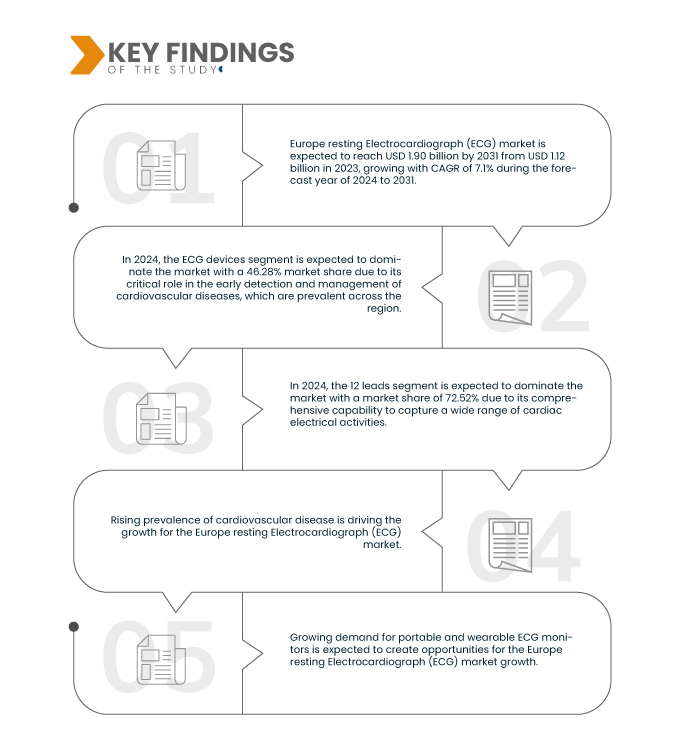

歐洲靜止心電圖 (ECG) 市場正在經歷顯著擴張,這主要是由於心血管疾病盛行率的上升,心血管疾病仍然是整個歐洲大陸死亡的主要原因。人口老化、早期診斷意識的增強以及高血壓和糖尿病等慢性病的增加,推動了對心電圖機等先進診斷工具的需求。靜息心電圖以其簡單性和可靠性而聞名,在早期檢測中發揮至關重要的作用,這對於降低長期醫療成本和改善患者預後至關重要。

無線、數位和便攜式心電圖設備等技術進步正在改變這一格局,提高診斷準確性和患者舒適度。此外,與人工智慧(AI)的結合可以實現更快的分析和更精確的結果,對臨床醫生和患者都有吸引力。然而,監管挑戰,特別是歐盟對醫療器材的嚴格監管,以及對資料隱私和安全的擔憂,對市場成長構成了障礙。在歐盟政府措施的支持下,數位醫療的轉變有望為該市場的投資和創新開闢新的途徑。

訪問完整報告@ https://www.databridgemarketresearch.com/reports/europe-resting-electrocardiograph-ecg-market

Data Bridge Market Research 分析稱,歐洲靜息心電圖 (ECG) 市場預計將從 2023 年的 11.2 億美元增至 2031 年的 19.0 億美元,在 2024 年至 2031 年的預測期內,複合年增長率為 7.1%。

研究的主要發現

心電圖技術不斷進步

心電圖 (ECG) 技術的不斷進步是歐洲靜息心電圖市場成長的主要驅動力,因為創新提高了這些診斷設備的準確性、效率和可用性。數位心電圖系統、用於解釋心臟訊號的先進演算法以及基於雲端的資料管理等發展正在改變傳統的心電圖實踐,從而可以更精確、更及時地診斷心臟狀況。此外,人工智慧 (AI) 和機器學習在心電圖分析中的整合使醫療保健提供者能夠更自信地檢測異常,從而降低人為錯誤的可能性並改善患者的治療效果。

此外,便攜式和穿戴式心電圖設備的出現使得心臟監測更加容易,可以實現遠端患者監測並促進早期幹預。隨著醫療保健系統越來越重視遠距醫療和遠距照護解決方案,兼具功能性和便利性的技術先進的心電圖設備的需求也不斷增加。這些進步不僅簡化了臨床環境中的工作流程,而且還使患者能夠積極地管理自己的心臟健康,最終推動市場向前發展,因為供應商尋求採用尖端的心血管護理解決方案。

報告範圍和市場細分

報告指標

|

細節

|

預測期

|

2024-2031

|

基準年

|

2023

|

歷史性的一年

|

2022(可自訂為 2016 - 2021)

|

定量單位

|

收入(十億美元)

|

涵蓋的領域

|

產品(心電圖設備、監視器、軟體和服務、植入式循環記錄器和行動心臟遙測設備)、導聯數(12 導聯、15 導聯、18導聯及其他)、技術(數位和類比)、模態(固定和移動)、設備尺寸(大、中、小)、連接性(有線和無線)、操作模式(自動、半自動和手動)、最終用戶(醫院、專科診所、門診手術中心、家庭護理環境及其他)

|

覆蓋國家

|

德國、英國、法國、義大利、西班牙、俄羅斯、土耳其、比利時、荷蘭、瑞士、波蘭、捷克共和國、斯洛伐克和歐洲其他地區

|

涵蓋的市場參與者

|

GE Healthcare(美國)、Koninklijke Philips NV(荷蘭)、Baxter(美國)、SCHILLER AG(瑞士)、Cardioline SPA(義大利)、EDAN Instruments, Inc.(中國)、FUKUDA DENSHI(日本)、Personal MedSystems GmbH(德國)、VravIRE MEDIP. Systems, Inc. (Spacelabs Healthcare)(美國)、樂普醫療科技(北京)有限公司(中國)、Dawei medical(中國)、Gima SPA(義大利)、Zimmer Benelux BV(德國)、AMEDTEC Medizintechnik Aue GmbH(德國)、BTL(印度)和Contec Systems Co.

|

報告涵蓋的數據點

|

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深入的專家分析、患者流行病學、管道分析、定價分析和監管框架。

|

細分分析

歐洲靜息心電圖 (ECG) 市場根據產品、導線數量、技術、模式、設備尺寸、連接性、操作模式和最終用戶分為幾個值得注意的細分市場。

- 根據產品,歐洲靜息心電圖 (ECG) 市場細分為 ECG 設備、監視器、軟體和服務、植入式循環記錄器和行動心臟遙測設備

2024 年,心電圖設備領域預計將主導歐洲靜息心電圖 (ECG) 市場

到 2024 年,心電圖設備領域預計將佔據 46.28% 的市場份額,這得益於其在該地區普遍存在的心血管疾病的早期發現和管理中發揮的關鍵作用。

- 根據導聯數量,歐洲靜息心電圖 (ECG) 市場細分為 12 導程、15 導程、18 導程和其他

2024 年,12 導聯市場預計將佔據歐洲靜息心電圖 (ECG) 市場的主導地位

到 2024 年,12 導聯領域預計將佔據市場主導地位,市場份額達到 72.52%,因為它具有全面捕捉各種心臟電活動的能力。

- 根據技術,歐洲靜息心電圖 (ECG) 市場分為數位和類比。預計到 2024 年,數位領域將佔據市場主導地位,市佔率達 77.87%

- 根據模式,歐洲靜息心電圖 (ECG) 市場分為固定式和移動式。預計到 2024 年,固定市場將佔據主導地位,市佔率達到 70.72%

- 根據設備尺寸,歐洲靜息心電圖 (ECG) 市場分為大、中、小型。預計到 2024 年,大型細分市場將佔據主導地位,市佔率達到 60.91%

- 根據連接性,歐洲靜息心電圖 (ECG) 市場分為有線和無線。預計到 2024 年,有線市場將佔據主導地位,市佔率達 63.28%

- 根據操作模式,歐洲靜息心電圖 (ECG) 市場分為自動、半自動和手動。預計到 2024 年,自動擋汽車將佔據主導地位,市佔率達 71.51%

- 根據最終用戶,歐洲靜息心電圖 (ECG) 市場分為醫院、專科診所、門診手術中心、家庭護理機構和其他。到 2024 年,醫院部門預計將佔據市場主導地位,市佔率達到 35.05%

主要參與者

Data Bridge Market Research 分析了以下公司作為歐洲靜息心電圖 (ECG) 市場的主要公司,包括 GE Healthcare(美國)、Koninklijke Philips NV(荷蘭)、Baxter(美國)、SCHILLER AG(瑞士)和 Cardioline SPA(義大利)等。

市場發展

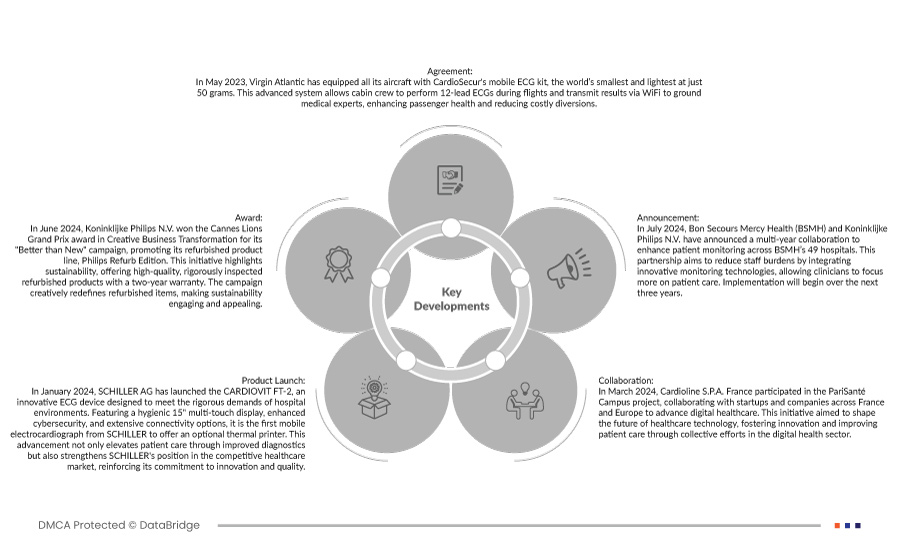

- 2024 年 7 月,Bon Secours Mercy Health (BSMH) 和荷蘭皇家飛利浦公司宣佈建立多年合作關係,以加強 BSMH 旗下 49 家醫院的病患監測。此次合作旨在透過整合創新監測技術來減輕員工負擔,使臨床醫生能夠更專注於病患照護。實施將在未來三年內開始

- 2024 年 1 月,SCHILLER AG 推出了 CARDIOVIT FT-2,這是一款創新的心電圖設備,旨在滿足醫院環境的嚴格要求。它配備 15 吋衛生級多點觸控顯示器、增強的網路安全性和豐富的連接選項,是 SCHILLER 首款可選配熱敏印表機的行動心電圖儀。這項進步不僅透過改進診斷來提升病患照護水平,還鞏固了 SCHILLER 在競爭激烈的醫療保健市場中的地位,強化了其對創新和品質的承諾。

- 2024 年 3 月,Cardioline SPA France 參與了 PariSanté Campus 項目,與法國和歐洲各地的新創公司和公司合作,推動數位醫療保健的發展。該計劃旨在透過數位醫療領域的共同努力,塑造醫療技術的未來,促進創新並改善患者護理

- 2022 年 5 月,福田電子向美國客戶推出了其網站,提供即時的產品支援。該網站提供產品資訊、教學影片、手冊和新聞,增強用戶體驗並幫助他們優化設備使用

- 2023 年 5 月,維珍航空與 CardioSecur 合作,為所有航班配備世界上最小的行動心電圖套件,以提高機上安全性。該系統使機組人員能夠記錄 12 導程心電圖並將結果傳輸至地面醫療服務,提供重要的回饋並減少因心血管事件而導致航班改道的需要

有關歐洲靜息心電圖 (ECG) 市場的更多詳細信息,請點擊此處 - https://www.databridgemarketresearch.com/reports/europe-resting-electrocardiograph-ecg-market