Europe Bioherbicides Market

Размер рынка в млрд долларов США

CAGR :

%

USD

456.13 Million

USD

675.46 Million

2024

2032

USD

456.13 Million

USD

675.46 Million

2024

2032

| 2025 –2032 | |

| USD 456.13 Million | |

| USD 675.46 Million | |

| % | |

|

Сегментация европейского рынка биогербицидов по типу (микробные, биохимические и другие), способу действия (селективные и неселективные биогербициды), форме (жидкие и сухие), применению (опрыскивание листьев, обработка семян, обработка почвы, послеуборочная обработка, химизация и другие), типу культуры (зерновые, фрукты и овощи, масличные и бобовые, газоны и декоративные растения и другие культуры), каналу сбыта (прямой и косвенный) — тенденции отрасли и прогноз до 2032 года

Размер европейского рынка биогербицидов

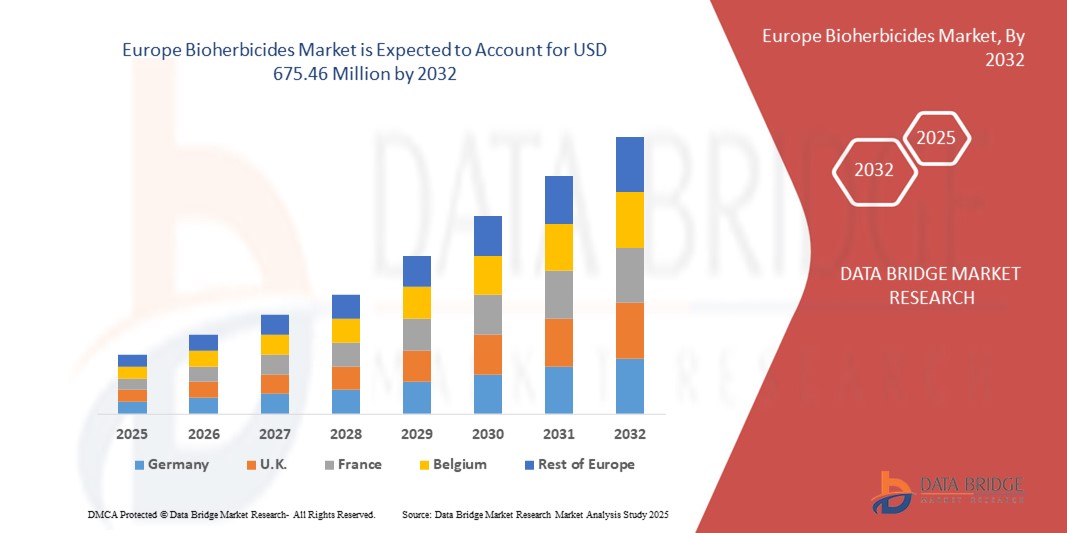

- Объем европейского рынка биогербицидов в 2024 году оценивался в 456,13 млн долларов США, а к 2032 году , как ожидается, он достигнет 675,46 млн долларов США при среднегодовом темпе роста 5,03% в течение прогнозируемого периода.

- Рост рынка во многом обусловлен растущим внедрением устойчивых и экологичных методов ведения сельского хозяйства, а также растущим пониманием воздействия синтетических гербицидов на окружающую среду. Фермеры и агробизнес всё чаще переходят на биологические решения для борьбы с сорняками, одновременно сокращая количество остатков химикатов в посевах и почве.

- Кроме того, растущая нормативная поддержка биологических средств защиты растений и достижения в области микробных и биохимических формул ускоряют разработку и внедрение биогербицидов, тем самым значительно стимулируя рост отрасли.

Анализ рынка биогербицидов в Европе

- Биогербициды – это биологические препараты, получаемые из природных организмов или их метаболитов, используемые для контроля или подавления роста сорняков на сельскохозяйственных полях. Они представляют собой целенаправленную, экологичную альтернативу традиционным химическим гербицидам и могут применяться в различных формах, включая жидкую, сухую и для обработки семян, для различных видов сельскохозяйственных культур.

- Растущий спрос на биогербициды обусловлен, прежде всего, потребностью в устойчивых решениях для борьбы с сорняками, растущей распространенностью устойчивых к гербицидам сорняков и растущим вниманием к сокращению использования химикатов в сельском хозяйстве. Достижения в области разработки формул, простота интеграции в современные методы ведения сельского хозяйства и растущая осведомленность фермеров о долгосрочном здоровье почвы и урожая также способствуют расширению рынка.

- Германия доминировала на рынке биогербицидов в 2024 году благодаря своему развитому сельскохозяйственному сектору, сильному акценту на устойчивое земледелие и растущему внедрению экологически чистых решений по защите растений.

- Ожидается, что Великобритания станет регионом с самыми быстрыми темпами роста на рынке биогербицидов в течение прогнозируемого периода благодаря более широкому внедрению методов устойчивого и органического земледелия и усилению внимания к сокращению использования химикатов в растениеводстве.

- В 2024 году сегмент жидких препаратов доминировал на рынке, достигнув доли 57,6% благодаря простоте применения, быстрому всасыванию и равномерному распределению по целевым областям. Жидкие противовирусные препараты особенно подходят для опрыскивания листьев и обработки семян, обеспечивая эффективную доставку активных веществ. Гибкость их формул и совместимость с автоматизированными системами внесения делают их весьма привлекательными для коммерческого использования. Кроме того, жидкие препараты обеспечивают точное дозирование и быстрое реагирование на возникающие вирусные угрозы, повышая их эффективность при широкомасштабной защите сельскохозяйственных культур. Их адаптируемость к различным типам культур и условиям окружающей среды дополнительно способствует их внедрению на рынке.

Область применения отчета и сегментация рынка биогербицидов

|

Атрибуты |

Ключевые данные о рынке биогербицидов |

|

Охваченные сегменты |

|

|

Охваченные страны |

Европа

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

Помимо информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географический охват и основные игроки, рыночные отчеты, подготовленные Data Bridge Market Research, также включают анализ импорта и экспорта, обзор производственных мощностей, анализ потребления продукции, анализ ценовых тенденций, сценарий изменения климата, анализ цепочки поставок, анализ цепочки создания стоимости, обзор сырья/расходных материалов, критерии выбора поставщиков, анализ PESTLE, анализ Портера и нормативную базу. |

Тенденции европейского рынка биогербицидов

Растущий спрос на органическое и устойчивое земледелие

- Ускоренный переход к органическому и устойчивому земледелию повышает спрос на биогербициды, поскольку они представляют собой экологичную альтернативу синтетическим химическим средствам борьбы с сорняками. Фермеры и производители всё чаще ищут натуральные средства, которые минимизируют ущерб окружающей среде, сохраняя при этом продуктивность.

- Например, компания Marrone Bio Innovations разработала биогербицидные продукты, предназначенные для борьбы с сорняками, с использованием природных микроорганизмов и растительных компонентов. Их портфолио демонстрирует, как устойчивые решения могут эффективно бороться с сорняками, одновременно способствуя росту рынка, основанному на органических удобрениях.

- Растущий спрос потребителей на продукты питания без химикатов подталкивает фермеров к использованию ресурсов, соответствующих сертификатам устойчивого развития. Биогербициды, не оставляющие остатков и биоразлагаемые, способствуют соблюдению стандартов органического земледелия и отвечают требованиям потребителей к более безопасным методам ведения сельского хозяйства.

- Кроме того, осведомлённость о здоровье почвы и биоразнообразии повлияла на стратегии ведения сельского хозяйства. Биогербициды способствуют достижению этих целей, снижая накопление химических веществ, усиливая микробную активность и способствуя долгосрочной устойчивости сельскохозяйственных угодий по сравнению с синтетическими гербицидами.

- Растущий сектор органического земледелия создает благоприятные условия для применения биогербицидов. В условиях растущих проблем с продовольственной безопасностью устойчивая борьба с сорняками с помощью биологических методов становится ключевым приоритетом для сельскохозяйственной экосистемы.

- В целом, тенденция к органическому и устойчивому земледелию подкрепляет ключевую роль биогербицидов. Их способность отвечать ожиданиям потребителей, улучшать качество почвы и соответствовать нормативным и экологическим требованиям делает их важнейшей частью сельского хозяйства будущего.

Динамика рынка биогербицидов в Европе

Водитель

Нормативная поддержка и государственные инициативы

- Глобальная нормативно-правовая база и государственная политика играют решающую роль в стимулировании внедрения биогербицидов. Политика, направленная на снижение использования химических гербицидов, способствует переходу к устойчивым альтернативам в традиционном сельском хозяйстве.

- Например, Европейский союз ввёл более строгие правила в отношении синтетических пестицидов, создав возможности для внедрения биогербицидов. Такие компании, как BioWorks, используют эти изменения в политике, масштабируя производство биологических решений, соответствующих нормативным требованиям для повышения безопасности сельского хозяйства.

- Финансируемые государством исследовательские программы и субсидии способствуют дальнейшему внедрению биопестицидов. Многие страны инвестируют в разработку биопестицидов и предлагают фермерам стимулы для интеграции биопрепаратов в комплексные системы борьбы с сорняками.

- Кроме того, акцент на достижении Целей устойчивого развития ООН (ЦУР) усилил поддержку экологически безопасных методов ведения сельского хозяйства. Биогербициды тесно связаны как с мерами по борьбе с изменением климата, так и с целями по устойчивому развитию сельского хозяйства.

- В целом, регулирующая поддержка, политические стимулы и институциональное финансирование создают прочную основу для широкого внедрения биогербицидов на рынок. Ожидается, что эти механизмы поддержки будут способствовать росту спроса и стимулированию инноваций в секторе.

Сдержанность/Вызов

Ограниченная осведомленность фермеров о преимуществах биогербицидов

- Серьёзной проблемой на рынке биогербицидов является низкая осведомлённость фермеров об их эффективности по сравнению с традиционными химикатами. Многие фермеры по-прежнему сомневаются в их эффективности из-за опасений по поводу эффективности, процесса применения и ограниченной доступности продукта на местных рынках.

- Например, исследования в странах с развивающейся экономикой показывают, что агропромышленные компании, такие как BASF Biologicals, сталкиваются с трудностями в убеждении фермеров использовать биогербициды вместо традиционных гербицидов из-за предполагаемых рисков для урожайности и эффективности контроля.

- Отсутствие эффективных служб распространения знаний и программ обучения фермеров часто препятствует распространению знаний о биогербицидах. Отсутствие чётких рекомендаций и демонстрационных материалов ещё больше способствует низкому уровню внедрения, особенно среди мелких и средних фермеров.

- Кроме того, более высокая стоимость и ограниченная коммерческая доступность по сравнению с синтетическими гербицидами ограничивают доступ на рынках, чувствительных к цене. Фермеры с ограниченным бюджетом, скорее всего, продолжат использовать традиционные химикаты, которые дают быстрые и предсказуемые результаты.

- Преодоление этих проблем требует широкого обучения фермеров, проведения демонстрационных проектов и поддерживаемых государством информационных кампаний. Устранение этих пробелов будет иметь решающее значение для повышения доверия, расширения внедрения и полной реализации потенциала биогербицидов в устойчивом сельском хозяйстве.

Объем европейского рынка биогербицидов

Рынок сегментирован по типу, способу действия, форме, применению, типу сельскохозяйственной культуры и каналу сбыта.

- По типу

По типу рынок противовирусных препаратов сегментируется на микробные, биохимические и прочие. В 2024 году микробный сегмент занял наибольшую долю рынка благодаря своей доказанной эффективности в борьбе с вирусными патогенами и совместимости с сельскохозяйственными и медицинскими препаратами. Микробные противовирусные препараты пользуются популярностью благодаря своей экологичности и минимальному воздействию на нецелевые организмы, что делает их предпочтительным выбором для устойчивого лечения заболеваний. Активные исследования и разработки в области микробных составов дополнительно повысили их стабильность, эффективность и простоту применения. Их способность интегрироваться с существующими протоколами защиты растений и здравоохранения также способствует их внедрению.

Ожидается, что биохимический сегмент будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год, что обусловлено достижениями в области молекулярных противовирусных соединений и возросшим спросом на высокоточные решения. Биохимические противовирусные препараты высокоэффективны в подавлении репликации вирусов, обеспечивая специфичность действия, которая снижает сопутствующий ущерб полезным организмам. Рост инвестиций в биотехнологии и растущая осведомленность об альтернативных лекарственных средствах без использования химических веществ как в сельском хозяйстве, так и в здравоохранении дополнительно стимулируют расширение рынка.

- По способу действия

По механизму действия рынок противовирусных препаратов сегментируется на селективные и неселективные биогербициды. Сегмент селективных биогербицидов обеспечил наибольшую долю рынка в 2024 году, поскольку он воздействует на конкретные вирусные патогены, не затрагивая другие организмы, что снижает непреднамеренный ущерб сельскохозяйственным культурам или микробным сообществам. Эта специфичность обеспечивает более безопасные и предсказуемые результаты как в сельском хозяйстве, так и в здравоохранении. Регуляторная поддержка селективных решений и растущее внедрение в практику точного земледелия также способствуют его лидирующей позиции на рынке.

Ожидается, что сегмент неселективных биогербицидов будет демонстрировать самые высокие среднегодовые темпы роста в период с 2025 по 2032 год, что обусловлено растущей потребностью в противовирусных препаратах широкого спектра действия в регионах, подверженных множественным вирусным штаммам и частым вспышкам заболеваний. Эти противовирусные препараты обеспечивают быстрый и комплексный контроль, эффективно воздействуя на широкий спектр патогенов и снижая риск потерь урожая. Их способность обеспечивать стабильную защиту в различных условиях окружающей среды делает их особенно подходящими для крупномасштабной защиты сельскохозяйственных культур и экстренного реагирования на вспышки заболеваний. Росту их применения также способствуют достижения в технологиях разработки рецептур, которые повышают стабильность, эффективность и простоту применения.

- По форме

По форме рынок противовирусных препаратов сегментирован на жидкие и сухие. В 2024 году жидкий сегмент обеспечил наибольшую долю рынка – 57,6% – благодаря простоте применения, быстрому всасыванию и равномерному распределению по целевым областям. Жидкие противовирусные препараты особенно подходят для опрыскивания листьев и обработки семян, обеспечивая эффективную доставку активных веществ. Гибкость их формул и совместимость с автоматизированными системами внесения делают их весьма привлекательными для коммерческого использования. Кроме того, жидкие формы позволяют точно дозировать и быстро реагировать на возникающие вирусные угрозы, повышая их эффективность при широкомасштабной защите сельскохозяйственных культур. Их адаптивность к различным видам культур и условиям окружающей среды дополнительно способствует их внедрению на рынке.

Прогнозируется, что сегмент сухих препаратов будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год благодаря таким преимуществам, как более длительный срок годности, простота хранения и экономичная транспортировка. Сухие противовирусные препараты можно восстанавливать по мере необходимости, что сокращает потери и способствует устойчивому применению. Их стабильность в различных условиях окружающей среды делает их подходящими для регионов с ограниченной инфраструктурой холодовой цепи. Удобство использования и точное дозирование дополнительно повышают их привлекательность для фермеров и сельскохозяйственных операторов. Кроме того, ожидается, что растущий спрос в отдаленных или ограниченных по ресурсам регионах, где жидкие препараты могут быть менее практичны, ускорит внедрение сухих противовирусных препаратов. Растущая осведомленность об устойчивых и эффективных методах защиты растений также способствует расширению рынка.

- По применению

По области применения рынок противовирусных препаратов сегментируется на следующие категории: опрыскивание листьев, обработка семян, обработка почвы, послеуборочная обработка, химизация и другие. Сегмент опрыскивания листьев занял наибольшую долю рынка в 2024 году благодаря его непосредственному нанесению на сельскохозяйственные культуры, обеспечивая немедленный контроль вирусов и сокращая распространение инфекций. Опрыскивание листьев обеспечивает точное дозирование и равномерное покрытие, повышая эффективность обработки при минимальном воздействии на окружающую среду. Совместимость с автоматизированными системами опрыскивания и методами точного земледелия еще больше укрепляет их внедрение в коммерческом сельском хозяйстве. Кроме того, опрыскивание листьев универсальны и подходят для различных типов культур и климатических условий, что делает их предпочтительным выбором для крупномасштабных и высокодоходных сельскохозяйственных операций. Растущая осведомленность о своевременной и эффективной борьбе с болезнями также стимулирует рыночный спрос.

Ожидается, что сегмент обработки семян будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год, что обусловлено его ролью в защите от вирусных патогенов на ранней стадии, повышении устойчивости и урожайности сельскохозяйственных культур. Протравка семян набирает популярность благодаря своей эффективности, снижению потребности в химикатах и совместимости с современными методами ведения сельского хозяйства, что способствует развитию превентивных стратегий борьбы с болезнями. Способность протравливать семена на критической стадии прорастания снижает риск неурожая и повышает общую урожайность. Более того, ожидается, что развитие технологий покрытия семян и растущее внедрение устойчивых методов ведения сельского хозяйства будут способствовать дальнейшему ускорению роста этого сегмента. Растущий спрос со стороны регионов, ориентированных на производство высококачественной и безболезненной сельскохозяйственной продукции, также стимулирует внедрение.

- По типу культуры

По типу сельскохозяйственных культур рынок противовирусных препаратов сегментирован на зерновые, фрукты и овощи, масличные и бобовые, газонные и декоративные растения, а также другие культуры. Сегмент фруктов и овощей обеспечил наибольшую долю выручки рынка в 2024 году, что обусловлено высокой восприимчивостью этих культур к вирусным инфекциям и растущим спросом на безопасную и высококачественную продукцию. Потребительское предпочтение решений без использования химикатов дополнительно стимулирует внедрение противовирусной обработки этих культур. Передовые методы применения и методы точного земледелия также повышают эффективность противовирусных препаратов в этом сегменте.

Прогнозируется, что сегмент зерновых культур будет демонстрировать самые высокие среднегодовые темпы роста в период с 2025 по 2032 год, что обусловлено ростом спроса на основные культуры и участившимися вспышками вирусных патогенов, влияющих на глобальную продовольственную безопасность. Противовирусные препараты для зерновых культур помогают предотвратить потери урожая, повысить устойчивость культур к внешним воздействиям и обеспечить стабильность поставок продовольствия, что способствует более широкому внедрению этих решений. Растущая осведомленность фермеров об экономическом влиянии вирусных инфекций в сочетании с интеграцией противовирусных препаратов в современные методы ведения сельского хозяйства дополнительно стимулирует внедрение этих решений.

- По каналу распространения

По каналам сбыта рынок противовирусных препаратов сегментируется на прямые и непрямые. Сегмент прямых сбыта обеспечил наибольшую долю выручки рынка в 2024 году благодаря более тесным связям между производителями и крупными конечными пользователями, такими как сельскохозяйственные кооперативы, коммерческие фермы и учреждения здравоохранения. Прямые каналы сбыта позволяют лучше контролировать ценообразование, обеспечивать своевременные поставки и разрабатывать индивидуальные решения, отвечающие потребностям конечных пользователей. Мощная поддержка со стороны производителей и послепродажное обслуживание дополнительно укрепляют его доминирующее положение.

Ожидается, что сегмент непрямой дистрибуции будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год благодаря расширяющейся сети дистрибьюторов, розничных продавцов и онлайн-платформ. Непрямые каналы сбыта повышают доступность продукции для мелких фермеров и региональных сельскохозяйственных операторов, способствуя проникновению на рынок и широкому внедрению. Росту также способствует развитие электронной коммерции и цифровых торговых площадок, которые позволяют производителям охватывать отдаленные и слаборазвитые регионы. Кроме того, партнерские отношения с местными дистрибьюторами и поставщиками агротехнологических услуг способствуют повышению осведомленности о преимуществах биогербицидов, ускоряя их внедрение в различных регионах.

Региональный анализ европейского рынка биогербицидов

- Германия заняла лидирующие позиции на рынке биогербицидов, получив наибольшую долю выручки в 2024 году благодаря развитому сельскохозяйственному сектору, акценту на устойчивое земледелие и растущему внедрению экологически чистых решений по защите растений.

- Лидерство страны подкреплено масштабными инвестициями в НИОКР, государственной поддержкой биологической борьбы с вредителями и сорняками, а также интеграцией технологий точного земледелия.

- Растущий спрос на зерновые, зерновые и садовые культуры, а также растущая осведомлённость о сорняках, устойчивых к гербицидам, ещё больше укрепляют позиции Германии. Сотрудничество между отечественными производителями биогербицидов и международными компаниями продолжает стимулировать инновации и расширение рынка, укрепляя доминирующее положение Германии в регионе.

Обзор рынка биогербицидов в Великобритании

Ожидается, что рынок Великобритании будет демонстрировать самые высокие среднегодовые темпы роста в Европе в период с 2025 по 2032 год, чему будет способствовать растущее внедрение устойчивых и органических методов ведения сельского хозяйства и повышение внимания к сокращению использования химикатов в растениеводстве. Росту способствуют правительственные инициативы, направленные на продвижение экологически безопасного сельского хозяйства, расширение выращивания высокотоварных культур и повышение осведомленности фермеров о преимуществах биогербицидов. Инвестиции в исследования, интеграцию технологий и сотрудничество с мировыми поставщиками биогербицидов повышают эффективность и доступность продукции. Акцент Великобритании на экологически ответственное земледелие и точное земледелие расширяет проникновение на рынок и ускоряет темпы внедрения.

Обзор рынка биогербицидов во Франции

Ожидается, что Франция будет демонстрировать устойчивый рост в период с 2025 по 2032 год, чему будет способствовать развитый сельскохозяйственный сектор, увеличение производства зерновых, фруктов и овощей, а также растущий интерес к органическим и устойчивым решениям для защиты растений. Расширение рынка обусловлено растущим внедрением микробных и биохимических биогербицидов в сочетании с государственной политикой, направленной на сокращение использования химических веществ. Сотрудничество между отечественными производителями и международными разработчиками биогербицидов повышает их доступность, эффективность и осведомленность фермеров. Акцент страны на устойчивые методы ведения сельского хозяйства, соблюдение экологических норм и технологическую интеграцию продолжает укреплять рыночные перспективы Франции.

Доля европейского рынка биогербицидов

Лидерами отрасли биогербицидов являются, в первую очередь, хорошо зарекомендовавшие себя компании, в том числе:

- БАСФ (Германия)

- Корпорация FMC (США)

- Coromandel International Limited (Индия)

- Certis USA LLC (США)

- Emery Oleochemicals (Малайзия)

- BioHerbicides Australia (Австралия)

- Herbanatur (Испания)

- Andermatt Biocontrol Suisse (Швейцария)

- Syngenta AG (Швейцария)

- Bayer CropScience AG (Германия)

- Novozymes A/S (Дания)

- Marrone Bio Innovations Inc. (США)

- Verdesian Life Sciences (США)

- Deer Creek Holdings (США)

- EcoPesticides International, Inc. (США)

Последние события на европейском рынке биогербицидов

- В июле 2025 года испанская компания Seipasa, специализирующаяся на биопестицидах, объявила о своих усилиях по регистрации нового биогербицида с новым механизмом действия. Цель этой разработки – предложить альтернативу существующим синтетическим гербицидам, отвечая растущему спросу на экологически безопасные решения для защиты растений. Ожидается, что внедрение этого инновационного продукта расширит портфель Seipasa и будет способствовать развитию экологически чистых методов ведения сельского хозяйства.

- В декабре 2022 года компания Seipasa открыла новую производственную базу площадью 4000 м² для поддержки разработки и регистрации своих биогербицидных продуктов. Этот объект призван способствовать росту компании и расширить её возможности по удовлетворению растущего спроса на биопестицидные решения.

- В мае 2023 года компания BASF представила два новых гербицида, Facet и Duvelon, которые помогут индийским фермерам, выращивающим рис и чай, бороться с проблемными сорняками. Facet борется с травянистой сорняковой травой Echinochloa spp на рисовых плантациях, а Duvelon, в сочетании с Kixor Active, борется с широколиственными сорняками на чайных плантациях. Этот запуск расширяет ассортимент BASF, решая ключевые проблемы, с которыми сталкиваются производители риса и чая в Индии, и ещё раз подчёркивает приверженность компании принципам устойчивого ведения сельского хозяйства.

- В октябре 2024 года компания FMC Corporation объявила о запуске гербицида Ambriva в Чандигархе, Индия, призванного помочь фермерам, выращивающим пшеницу, бороться с устойчивым сорняком Phalaris minor. Благодаря Isoflex active, новому гербициду группы 13, Ambriva обеспечивает эффективный контроль на раннем послевсходовом этапе и длительную остаточную защиту. Гербицид прошел тщательные испытания и представляет собой новое эффективное решение для фермеров в Пенджабе, Харьяне, Уттар-Прадеше и Раджастане, решая серьёзные проблемы, связанные с этим вредоносным сорняком.

- В декабре 2022 года FMC Corporation и Micropep Technologies объявили о сотрудничестве в разработке биологических решений для борьбы с сорняками, устойчивыми к гербицидам. Это партнерство объединяет сельскохозяйственный опыт FMC и микропептидную технологию Micropep для ускорения разработки инновационных биогербицидных решений, направленных на повышение урожайности и внедрение устойчивых методов ведения сельского хозяйства.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.