Global Paper Based Containers Market

Market Size in USD Billion

USD

104.69 Billion

USD

155.73 Billion

2024

2032

USD

104.69 Billion

USD

155.73 Billion

2024

2032

| 2025 - 2032 | |

| USD 104.69 Billion | |

| USD 155.73 Billion | |

| % | |

|

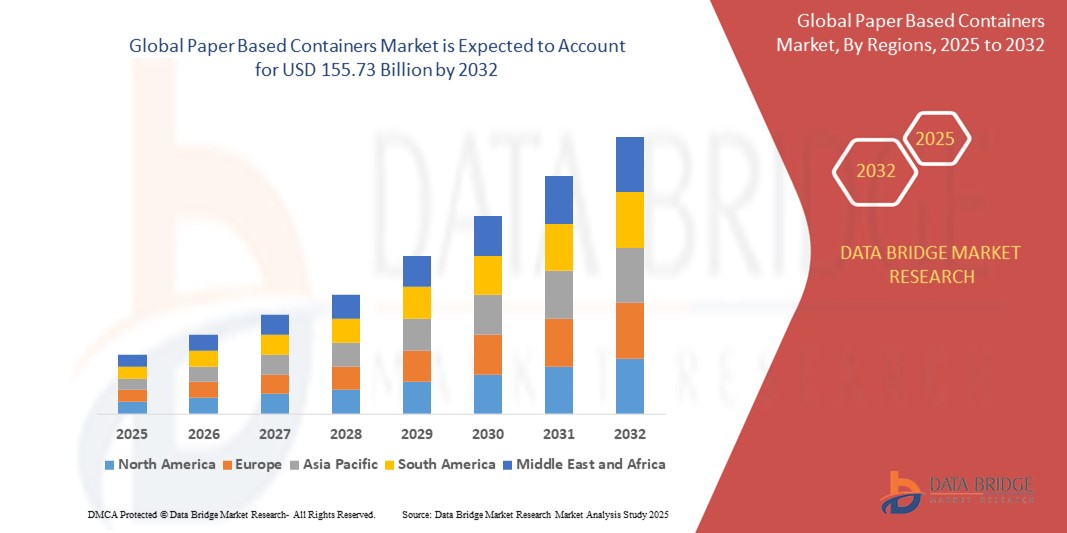

Paper Based Containers Market Size

- The global paper based containers market size was valued at USD 104.69 billion in 2024 and is expected to reach USD 155.73 billion by 2032, at a CAGR of 5.09% during the forecast period of 2025 to 2032

- The market growth is largely fueled by the increasing shift toward sustainable packaging solutions driven by regulatory bans on single-use plastics and rising consumer environmental awareness across industries such as food, beverages, and consumer goods

- Furthermore, growing demand from e-commerce and retail sectors for lightweight, recyclable, and cost-effective packaging, combined with advancements in paper strength, barrier coatings, and printing technologies, is accelerating the adoption of paper-based containers, thereby significantly boosting the industry's growth

Paper Based Containers Market Analysis

- Paper-based containers, serving as eco-friendly alternatives to plastic and other non-biodegradable packaging, are increasingly critical in modern packaging strategies across industries due to their recyclability, versatility, and alignment with global sustainability goals

- The escalating demand for paper-based containers is primarily fueled by regulatory pressure to reduce plastic usage, rising consumer preference for sustainable packaging, and the rapid expansion of e-commerce and food delivery services requiring durable, lightweight, and environmentally responsible packaging solutions

- Asia-Pacific dominated the paper based containers market with a share of 39.8% in 2024, due to booming e-commerce, increasing urban population, and heightened demand for sustainable packaging across consumer goods and food sectors

- North America is expected to be the fastest growing region in the paper based containers market during the forecast period due to growing awareness of environmental issues and increasing demand for renewable packaging across food, electronics, and retail sectors

- Boxes segment dominated the market with a market share of 49.1% in 2024, due to their widespread use across various industries including food & beverages, consumer goods, and e-commerce. Their structural integrity, ease of printing for branding, and recyclability make boxes the preferred packaging solution, particularly for shipping and retail. The growth of online retail has significantly boosted demand for corrugated and folding carton boxes due to their protective qualities and cost-efficiency

Report Scope and Paper Based Containers Market Segmentation

|

Attributes |

Paper Based Containers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Paper Based Containers Market Trends

“Rising Expansion in Food Delivery Services”

- A significant and accelerating trend in the global paper-based containers market is the rising expansion of food delivery services, which is driving demand for sustainable, durable, and functional packaging solutions that align with both brand and environmental goals

- For instance, major players such as Graphic Packaging International, WestRock Company, and Smurfit Kappa Group have introduced innovative paper-based containers designed specifically for the foodservice and takeaway sectors, including grease-resistant boxes, heat-retentive trays, and recyclable clamshells that maintain food integrity during transit

- The surge in online food ordering, particularly through platforms such as Swiggy, DoorDash, and Uber Eats, has intensified the need for lightweight, stackable, and customizable packaging that ensures product protection while enhancing consumer experience. These packaging solutions also serve as brand carriers, often featuring high-quality printing and eco-labeling

- Technological advancements in barrier coatings and water-resistant paperboard materials are enabling food-grade paper containers to compete directly with plastic in terms of performance and shelf life. For example, Huhtamaki offers compostable paper containers that provide oil and moisture resistance without using polyethylene liners

- This trend towards sustainable packaging in the food delivery ecosystem is fundamentally reshaping brand packaging strategies and consumer expectations. As a result, packaging providers are scaling up production of recyclable and biodegradable formats tailored to evolving foodservice models

- The demand for paper-based containers in the expanding food delivery market is growing rapidly across both developed and emerging economies, as consumers and companies alike prioritize eco-friendly solutions without compromising on functionality and visual appeal

Paper Based Containers Market Dynamics

Driver

“Rising Demand for Sustainable Packaging”

- The rising demand for sustainable packaging across industries is a significant driver for the growth of the paper-based containers market, as businesses and consumers increasingly shift away from plastic due to environmental concerns and regulatory pressures

- For instance, in March 2024, Smurfit Kappa Group launched a new line of fully recyclable and compostable paper-based containers for the fresh produce sector, aiming to support customers in meeting sustainability goals and complying with plastic reduction mandates. Initiatives such as these by key companies are expected to drive market expansion over the forecast period

- As consumers become more conscious of climate impact and product lifecycle, brands are under increasing pressure to adopt eco-friendly packaging alternatives. Paper-based containers offer renewable, biodegradable, and recyclable solutions, aligning well with these evolving consumer preferences

- Furthermore, governments worldwide are introducing stringent regulations banning single-use plastics and promoting circular economy models, which are accelerating the transition to fiber-based packaging

- The growing emphasis on corporate sustainability, combined with innovations in paperboard strength, moisture resistance, and printability, is propelling the widespread adoption of paper-based containers across foodservice, retail, and industrial applications

Restraint/Challenge

“Limited Durability of Paper-Based Containers”

- Limited durability of paper-based containers poses a significant challenge to broader market penetration, particularly in applications requiring high resistance to moisture, grease, or mechanical stress. Unlike plastic or metal counterparts, traditional paper-based containers may lack the structural integrity needed for heavy or long-term use, which can hinder adoption in sectors such as frozen foods, industrial packaging, and liquids

- For instance, food delivery businesses have raised concerns over leakage and deformation of paper-based clamshells and trays during transit, prompting companies such as Huhtamaki and WestRock Company to invest in advanced coating technologies and multi-layered board compositions

- Addressing these durability limitations through material innovation—such as biodegradable barrier coatings, enhanced corrugated strength, and hybrid fiber compositions—is critical for expanding usage across high-demand categories. Companies including Graphic Packaging International have introduced moisture-resistant paperboard solutions aimed at replacing plastic in chilled and frozen food applications

- However, achieving this balance between durability and full recyclability remains complex, as certain coatings can compromise the biodegradability or recyclability of the final product. This has led to concerns among environmentally conscious consumers and regulators

- Overcoming these challenges will depend on continued R&D investments, collaborative innovation between packaging firms and end-users, and the development of universally recyclable, high-durability paper-based solutions that do not compromise environmental goals

Paper Based Containers Market Scope

The market is segmented on the basis of product type, board type, and end-use.

- By Product Type

On the basis of product type, the paper-based containers market is segmented into boxes, tubes, trays, liquid cartons, clamshells, and others. The boxes segment dominated the market with the largest market revenue share of 49.1% in 2024, owing to their widespread use across various industries including food & beverages, consumer goods, and e-commerce. Their structural integrity, ease of printing for branding, and recyclability make boxes the preferred packaging solution, particularly for shipping and retail. The growth of online retail has significantly boosted demand for corrugated and folding carton boxes due to their protective qualities and cost-efficiency.

The liquid cartons segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing demand for sustainable packaging in the dairy, juice, and ready-to-drink beverage segments. Liquid cartons are lightweight, easy to stack, and help preserve freshness, which is crucial for perishable liquids. Rising environmental concerns and regulatory pressure on plastic usage are accelerating the shift toward fiber-based alternatives such as aseptic and gable-top liquid cartons.

- By Board Type

On the basis of board type, the paper-based containers market is segmented into paperboard, containerboard, and others. The containerboard segment accounted for the largest market share in 2024, supported by its extensive use in the manufacture of corrugated boxes for packaging and shipping purposes. Containerboard’s durability, recyclability, and high resistance to compression make it ideal for transit packaging. Surging demand from e-commerce and industrial logistics further fuels its dominance.

The paperboard segment is projected to record the fastest growth rate from 2025 to 2032, owing to its increasing adoption in consumer goods and premium packaging applications. Paperboard offers a smooth surface for high-quality graphics, making it highly attractive for branding in personal care, pharmaceuticals, and food packaging. The demand for compact, visually appealing, and eco-friendly packaging is propelling the uptake of paperboard across various retail sectors.

- By End-Use

On the basis of end-use, the paper-based containers market is segmented into food & beverages, chemicals & fertilizers, pharmaceuticals, automotive & allied industries, electrical & electronics, consumer goods, and others. The food & beverages segment dominated the market in 2024 with the largest revenue share, due to the growing consumer preference for sustainable, biodegradable packaging and increasing regulatory bans on single-use plastics. Paper-based containers such as trays, boxes, and cartons are extensively used for packaging fast food, bakery items, frozen foods, and beverages. Their compatibility with printing for branding, ease of handling, and recyclability contribute to their widespread use.

The pharmaceuticals segment is anticipated to witness the fastest CAGR from 2025 to 2032, driven by rising demand for secure, tamper-evident, and eco-friendly packaging formats. As pharmaceutical companies aim to reduce plastic use and meet green compliance targets, paper-based alternatives for blister packs, pill boxes, and secondary packaging are gaining traction. Stringent safety and sustainability standards further support the growth of paper-based packaging in this sector.

Paper Based Containers Market Regional Analysis

- Asia-Pacific dominated the paper based containers market with the largest revenue share of 39.8% in 2024, driven by booming e-commerce, increasing urban population, and heightened demand for sustainable packaging across consumer goods and food sectors

- Growth is fueled by rapid industrialization, rising disposable incomes, and government initiatives promoting plastic alternatives and waste reduction

- The region benefits from large-scale local production, expanding retail infrastructure, and rising investments in automated paper packaging machinery across emerging economies

Japan Paper-Based Containers Market Insight

The Japan market is expanding steadily due to rising demand for high-quality, compact, and eco-friendly packaging in food, cosmetics, and electronics. Consumers prefer minimalistic yet functional packaging, and paper-based solutions meet sustainability and hygiene standards. Domestic producers focus on innovation in lightweight, premium packaging with high recyclability to align with consumer values and government regulations.

China Paper-Based Containers Market Insight

The China paper-based containers market accounted for the largest share in Asia-Pacific in 2024, fueled by the country’s large manufacturing base, rapid growth in online retail, and food delivery services. Government crackdowns on plastic usage and supportive policies for green packaging have accelerated the transition toward paper-based alternatives. Major domestic players are scaling up production and investing in biodegradable and recyclable materials to meet both domestic and international demand.

Europe Paper-Based Containers Market Insight

The Europe market is projected to grow at a strong CAGR over the forecast period, driven by stringent environmental regulations and high consumer awareness of sustainable consumption. Countries across the region are actively implementing circular economy principles, boosting demand for recyclable and biodegradable paper packaging. Food and beverage manufacturers are shifting from plastic to paper cartons, trays, and clamshells to align with EU Green Deal objectives.

U.K. Paper-Based Containers Market Insight

The U.K. market is experiencing notable growth as businesses adapt to packaging waste reduction targets and growing consumer preference for recyclable materials. With bans on single-use plastics and a surge in organic product lines, brands are rapidly adopting paper-based packaging across food, cosmetics, and retail. Local innovations in molded fiber packaging and print-friendly paperboard solutions are further supporting market expansion.

Germany Paper-Based Containers Market Insight

Germany's market is expanding significantly, driven by its strong commitment to environmental sustainability and innovation. With one of the highest recycling rates globally, Germany is a key hub for paper-based container development. Rising demand from foodservice, personal care, and industrial sectors is supported by widespread consumer preference for low-impact, FSC-certified packaging.

North America Paper-Based Containers Market Insight

North America is expected to register the fastest CAGR from 2025 to 2032, supported by growing awareness of environmental issues and increasing demand for renewable packaging across food, electronics, and retail sectors. The rise of direct-to-consumer brands and e-commerce is accelerating the shift to durable yet sustainable packaging formats. Companies are also responding to state-level bans on plastic and extended producer responsibility policies.

U.S. Paper-Based Containers Market Insight

The U.S. held the largest revenue share in the North American market in 2024, backed by rising demand in food delivery, retail, and healthcare. The country’s robust infrastructure and consumer demand for biodegradable, tamper-proof, and customizable packaging drive continuous innovation. Investments in recycled containerboard and digital printing technologies are expanding the use of paper-based containers across both large corporations and small businesses.

Paper Based Containers Market Share

The paper based containers industry is primarily led by well-established companies, including:

- Huhtamaki (Finland)

- International Paper (U.S.)

- Detmold Group (Australia)

- Georgia-Pacific (U.S.)

- Mondi (U.K.)

- Tetra Pak International S.A. (Switzerland)

- Smurfit Kappa (Ireland)

- DS Smith (U.K.)

- NIPPON PAPER INDUSTRIES CO., LTD (Japan)

- Oji Holdings Corporation (Japan)

- Packaging Corporation of America (U.S.)

- Pratt Industries, Inc. (U.S.)

- Sonoco Products Company (U.S.)

- Visy (Australia)

What are the Recent Developments in Global Paper Based Containers Market?

- In June 2024, Saica Group, a leading company in packaging solutions, partnered with Mondelez, a prominent fast-moving consumer goods manufacturer, to introduce a new paper-based product aimed at multipack items in the confectionery, biscuit, and chocolate markets. This innovative packaging is designed to be recyclable within the paper waste stream and is suitable for heat-sealable packing processes

- In June 2024, Keystone Folding Box, a paperboard packaging specialist, introduced Push-Pak, a paperboard blister wallet designed for medicine tablets. This innovative packaging features a straightforward push-through opening system, eliminating the need for complex instructions. In addition, it boasts a more compact blister arrangement, which reduces the overall size of the package

- In September 2023, Mondi, in collaboration with Veetee, introduced the U.K.’s first paper-based packaging for dry rice using recyclable FunctionalBarrier Paper. This innovation replaces plastic and also enhances shelf appeal and product protection, marking a significant milestone in driving sustainable packaging adoption within the food industry. The initiative strengthens Veetee’s sustainability commitments and sets a precedent for broader adoption of paper-based formats in staple food packaging

- In February 2023, ProAmpac launched ProActive Recyclable Paper-1000, a curbside recyclable, heat-sealable paper-based packaging solution with strong moisture barrier and directional tear properties. This advancement expands the company’s sustainable product portfolio and accelerates the shift from plastic to paper across a wide range of dry goods and consumer products, reinforcing ProAmpac’s position as a leader in eco-friendly flexible packaging

- In January 2022, Amcor unveiled AmFiberTM, a new platform of paper-based packaging products designed to offer enhanced functionality compared to conventional paper. This strategic launch supports Amcor’s vision to meet evolving consumer and regulatory demands for sustainable packaging and enhances its competitive edge by delivering paper solutions with advanced protection and versatility for applications in snacks, confections, and other fast-moving consumer goods

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Paper Based Containers Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Paper Based Containers Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Paper Based Containers Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.