Circumvent the Tariff challenges with an agile supply chain Consulting

Supply Chain Ecosystem Analysis now part of DBMR Reports

Global Micro Mobile Data Center Market

Market Size in USD Billion

CAGR :

%

USD

5.29 Billion

USD

14.16 Billion

2024

2032

Forecast Period

2025 –2032

Market Size(Base Year)

USD

5.29 Billion

Market Size (Forecast Year)

USD

14.16 Billion

CAGR

%

Major Markets Players

Corgan

Currie &

Brown Holdings Limited

DPR Construction

Holder Construction Group LLC

Global Micro Mobile Data Center Market Segmentation, By Component (Function Module Solutions and Services), Application (Instant DC and Retrofit, High Density Networks, Remote Office Support, Mobile Computing, and Others), Rack Unit (Up To 25 Ru, 25-40 Ru, and Above 40 Ru), Organization Size (Small and Medium-Sized Enterprises and Large Enterprises), Industry (Banking, Financial Services and Insurance, IT and Telecom, Government and Defense, Healthcare, Education, Retail, Energy, Manufacturing, and Others) - Industry Trends and Forecast to 2032

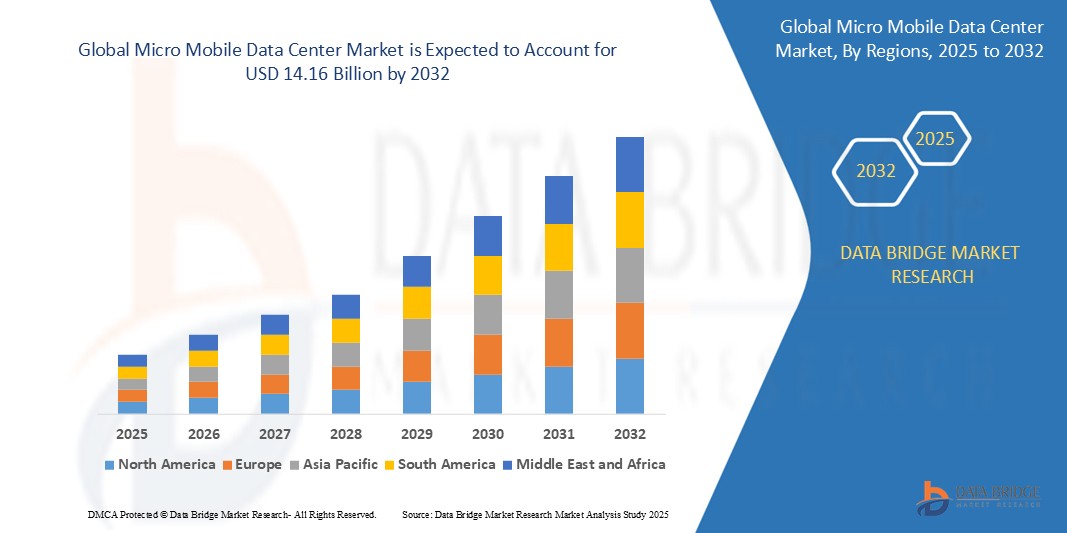

The global micro mobile data center market size was valued at USD 5.29 billion in 2024 and is expected to reach USD 14.16 billion by 2032,at a CAGR of 13.10% during the forecast period

The market growth is largely fueled by the increasing global demand for edge computing capabilities across various industries, driven by the proliferation of Internet of Things (IoT) devices and the necessity for low-latency processing for applications such as autonomous vehicles, industrial automation, and augmented/virtual reality

Technological advancements in micro mobile data center design, cooling systems, power management, and remote monitoring software are enhancing the efficiency, reliability, and ease of management of these deployments. The growing preference among enterprises for deploying IT infrastructure closer to the data source and end-users is also a significant driver due to benefits such as reduced latency, improved security, and enhanced control over data

Micro Mobile Data Center Market Analysis

Micro mobile data centers involve utilizing compact, self-contained data center units, often rack-mounted or containerized, to deliver localized computing and storage capabilities. This approach has become increasingly crucial in modern IT infrastructure due to its ability to address the growing demands for edge computing, rapid deployment, and enhanced data security and resilience

The growing adoption of this data center model is primarily due to the widespread increase in data generation from IoT devices and edge applications, a rising recognition of the limitations and challenges associated with relying solely on centralized or cloud-based infrastructure for all workloads, and an escalating demand from businesses for more agile, scalable, and geographically distributed IT resources to better serve their operations and end-users

North America is expected to dominate the micro mobile data center marketwith a share of 41.1% due to a robust existing IT infrastructure and an increasing demand for edge computing capabilities across various industries

Asia-Pacific is expected to be the fastest growing region in the micro mobile data center market with a share of during the forecast period due to rapid digitalization, increasing internet penetration, and the expansion of cloud computing and edge computing initiatives in countries such as China, India, and Japan

Large enterprises segment is expected to dominate the market with a market share of 65.4% due to their early adoption of micro mobile data centers to address challenges related to latency, data sovereignty, and the need for dedicated infrastructure for specific business units or applications

Report Scope and Micro Mobile Data Center Market Segmentation

Attributes

Micro Mobile Data Center Key Market Insights

Segments Covered

By Component: Function Module Solutions and Services

By Application: Instant DC and Retrofit, High Density Networks, Remote Office Support, Mobile Computing, and Others

By Rack Unit: Up To 25 Ru, 25-40 Ru, and Above 40 Ru

By Organization Size: Small and Medium-Sized Enterprises and Large Enterprises

By Industry: Banking, Financial Services and Insurance, IT and Telecom, Government and Defense, Healthcare, Education, Retail, Energy, Manufacturing, and Others

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis.

Micro Mobile Data Center Market Trends

“Growing Demand for Data Center Modernization”

A significant and accelerating trend in the global micro mobile data center market is the increasing need for organizations to modernize their existing data center infrastructure and deploy new, agile solutions closer to the data source and end-users. This shift is driven by the growing demands of latency-sensitive applications and the exponential growth of data generated at the edge

For instance, major players in the IT infrastructure and data center solutions industries, such as Vertiv, with its SmartCabinet and SmartRow solutions, Schneider Electric, offering Micro Data Centers, and Dell Technologies, with its Micro Data Center portfolio, are heavily invested in providing innovative micro mobile data center solutions to meet this evolving demand

This heightened need for modernization enables the development of infrastructure strategies capable of deploying computing and storage resources precisely where they are needed, based on factors such as application performance requirements, data locality regulations, and the need for rapid scalability. This approach significantly enhances operational efficiency and responsiveness compared to relying solely on traditional, centralized data center models

The growing preference among businesses for distributed IT architectures that can support digital transformation initiatives, along with the increasing complexity and geographical spread of operations, further fuels the importance of micro mobile data centers as a key component of modern IT strategy

Organizations are increasingly recognizing the potential of these compact and efficient solutions to effectively address their evolving infrastructure needs, reduce latency, improve resilience, and support new technologies such as 5G and IoT. This trend towards greater edge computing and infrastructure modernization is driving significant growth in the micro mobile data center market

The demand for micro mobile data centers is growing rapidly as the increasing need for data center modernization and edge computing encourages businesses to develop and adopt innovative infrastructure strategies tailored for these distributed environments. This direct and localized approach to deploying IT resources is vital for effective digital transformation and significantly boosts the micro mobile data center market

Micro Mobile Data Center Market Dynamics

Driver

“Growing Need for Disaster Recovery Solutions”

The increasing recognition of the critical need for robust disaster recovery and business continuity solutions among organizations is a significant driver for the heightened demand for micro mobile data centers

For instance, major providers in the micro mobile data center space, such as Dell Technologies, with their ruggedized and rapidly deployable micro data center options and IBM, offering solutions for business continuity and disaster recovery with micro data centers, highlight the effectiveness of their solutions in ensuring minimal downtime and quick recovery of critical IT infrastructure

As the understanding of the potential impact of downtime expands, micro mobile data centers offer a potentially superior approach compared to relying solely on centralized facilities for disaster recovery, by promising rapid deployment of infrastructure in affected areas and maintaining essential services

Furthermore, the growing recognition of the limitations of traditional disaster recovery methods, such as relying on distant recovery sites with potential latency issues, and the potential of micro mobile data centers to provide localized and immediately available resources is prompting more investment and innovation in this area

The increasing availability of compact, ruggedized, and easily transportable micro mobile data center units, coupled with the growing awareness among businesses of the importance of minimizing downtime, makes it an attractive area for innovation and investment. The trend towards enhanced business resilience and the desire for infrastructure that can quickly adapt to unforeseen events are also key factors propelling the adoption and development of Micro mobile data centers for disaster recovery

Restraint/Challenge

“Supply Chain Disruptions”

Global supply chain disruptions present a significant challenge to the timely and cost-effective deployment of micro mobile data centers in the Micro Mobile Data Centers market. The specialized nature of some components and the reliance on international logistics can lead to delays and increased costs

For instance, disruptions in the availability of critical components such as specialized cooling units or specific types of electronic hardware, as experienced by major players such as Vertiv, Schneider Electric, and Dell Technologies during recent global events, can significantly impact project timelines and overall deployment schedules

Addressing these supply chain challenges requires the development of resilient procurement strategies, diversification of supplier bases, and potentially increased inventory holding to mitigate the risk of delays and ensure consistent availability of necessary materials for manufacturing and assembly

While the potential long-term benefits of overcoming these limitations, such as more predictable deployment schedules, stable project costs, and the ability to meet the growing demand for edge computing infrastructure, are substantial, the current vulnerabilities in the global supply chain can hinder the rapid expansion and widespread adoption of micro mobile data centers.

Overcoming these challenges through proactive supply chain management, strategic partnerships with component manufacturers, and exploration of regional sourcing options will be vital for ensuring the consistent growth and reliability of the micro mobile data center sector

Micro Mobile Data Center Market Scope

The market is segmented on the basis of component, application, rack unit, organization size, and industry.

By Component

On the basis of component, the market is segmented into function module solutions and services. The services segment dominates the largest market revenue share of in 2025, driven by the immediate requirement for specialized expertise in the installation, configuration, and ongoing support of micro mobile data center deployments. Organizations often initially rely on external service providers for these complex integrations.

The function module solutions segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing demand for pre-fabricated, standardized, and easily scalable micro data center units that offer plug-and-play capabilities and reduced deployment timelines as the market matures and adoption broadens.

By Application

On the basis of application, the market is segmented into instant DC and retrofit, high-density networks, remote office support, mobile computing, and others. The mobile computing segment dominates the largest market revenue share in 2025, driven by the critical need for localized data processing and storage at the edge to support a growing number of mobile applications, IoT devices, and real-time data analytics closer to the source.

The remote office support segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing prevalence of hybrid work models and the demand for reliable, secure, and easily manageable IT infrastructure to support remote employees and branch offices with consistent performance.

By Rack Unit

On the basis of rack unit, the market is segmented into up to 25 RU, 25–40 RU, and above 40 RU. The above 40 RU segment dominates the largest market revenue share of 43.1% in 2025, driven by the initial adoption by larger enterprises and data centers needing to quickly expand capacity for specific high-performance computing or localized processing needs that require more significant rack space.

The 25–40 RU segment is expected to witness the fastest CAGR of 19.1% from 2025 to 2032, driven by its optimal balance of capacity, footprint, and cost-effectiveness, making it a versatile solution for a wide array of edge computing deployments, smaller enterprise expansions, and specific industry applications.

By Organization Size

On the basis of organization size, the market is divided into small and medium-sized enterprises and large enterprises. The large enterprises segment dominates the largest market revenue share of 65.4% in 2025, driven by their early adoption of micro mobile data centers to address challenges related to latency, data sovereignty, and the need for dedicated infrastructure for specific business units or applications.

The small and medium-sized enterprises segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing availability of cost-effective and user-friendly micro data center solutions that enable them to enhance their IT infrastructure, support digital transformation initiatives, and improve operational efficiency without substantial upfront investments.

By Industry

On the basis of industry, the market is segmented into banking, financial services and insurance (BFSI), IT and telecom, government and defense, healthcare, education, retail, energy, manufacturing, and others. The IT and telecom segment dominates the largest market revenue share 34.4% in 2025, driven by the industry's fundamental need for robust, scalable, and rapidly deployable infrastructure to support their core services, expanding networks, and the increasing demand for edge computing capabilities.

The government and defense segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing investments in secure, self-contained, and rapidly deployable data processing and storage solutions for sensitive information, tactical operations, and localized computing needs in various defense and government applications.

Micro Mobile Data Center Market Regional Analysis

North America dominates the micro mobile data center market with the largest revenue share of 41.1% in 2024, driven by a robust existing IT infrastructure and an increasing demand for edge computing capabilities across various industries

Enterprises in the region are rapidly adopting micro mobile data centers to support IoT deployments, reduce latency for critical applications, and improve data processing closer to the source

This widespread adoption is further supported by the presence of major technology providers, high internet penetration, and the growing focus on data security and compliance, establishing micro mobile data centers as a key component of modern IT strategies for both large corporations and distributed operations

U.S. Micro Mobile Data Center Market Insight

U.S. micro mobile data center market captured the largest revenue share within North America in 2025, fueled by the swift growth of cloud computing, the proliferation of data-intensive applications, and the escalating need for localized infrastructure to support digital transformation initiatives. Businesses are increasingly prioritizing the deployment of micro data centers to enhance network performance, ensure business continuity, and manage the exponential growth of data generated at the edge. The strong demand for edge computing solutions in sectors such as retail, healthcare, and manufacturing further propels the micro mobile data center industry. Moreover, the increasing integration of IoT devices and the expansion of 5G networks are significantly contributing to the market's expansion.

Europe Micro Mobile Data Center Market Insight

European micro mobile data center market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent data privacy regulations such as GDPR and the escalating need for localized and secure data processing in various industries. The increase in the adoption of cloud services, coupled with the demand for low-latency applications, is fostering the adoption of micro data centers. European enterprises are also drawn to the energy efficiency and scalability these solutions offer. The region is experiencing significant growth across manufacturing, telecommunications, and research sectors, with micro mobile data centers being incorporated into both new infrastructure deployments and upgrades of existing facilities.

U.K. Micro Mobile Data Center Market Insight

U.K. micro mobile data center market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating trend of edge computing and a desire for enhanced network performance and data security. In addition, the growing deployment of 5G infrastructure and the increasing demand for real-time data processing are encouraging both enterprises and service providers to choose micro mobile data center solutions. The UK’s embrace of digital transformation across various sectors, alongside its strong presence in finance and technology, is expected to continue to stimulate market growth.

Germany Micro Mobile Data Center Market Insight

German micro mobile data center market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing demand for localized data processing in the manufacturing sector and the need for secure infrastructure in highly regulated industries. Germany’s well-developed industrial base, combined with its emphasis on automation and Industry 4.0 initiatives, promotes the adoption of micro data centers, particularly in factory settings and remote industrial locations. The integration of micro data centers with industrial IoT (IIoT) solutions is also becoming increasingly prevalent, with a strong focus on data security and operational efficiency aligning with local business needs.

Asia-Pacific Micro Mobile Data Center Market Insight

Asia-Pacific micro mobile data center market is poised to grow at the fastest CAGR of 19.5% in the forecast period, driven by rapid digitalization, increasing internet penetration, and the expansion of cloud computing and edge computing initiatives in countries such as China, India, and Japan. The region's growing inclination towards smart cities, supported by government investments in digital infrastructure, is driving the adoption of micro data centers to support various applications such as smart grids, transportation, and public safety. Furthermore, as APAC emerges as a major hub for data generation and consumption, the need for efficient and localized data processing capabilities is expanding significantly.

Japan Micro Mobile Data Center Market Insight

Japan micro mobile data center market is gaining momentum due to the country’s focus on technological innovation, rapid urbanization, and demand for efficient and space-saving data center solutions. The Japanese market places a significant emphasis on energy efficiency and reliability, and the adoption of micro data centers is driven by the increasing need for localized infrastructure to support IoT deployments, disaster recovery, and specific industry applications. The integration of micro mobile data centers with advanced networking technologies and the need for low-latency processing for applications such as autonomous vehicles and robotics are fueling growth. Moreover, Japan's aging population and the need for remote healthcare solutions are likely to spur demand for distributed data center infrastructure.

China Micro Mobile Data Center Market Insight

China micro mobile data center market accounted for the largest market revenue share in Asia Pacific, attributed to the country's massive data generation, rapid expansion of cloud and edge computing infrastructure, and strong government support for digital transformation. China stands as one of the largest and fastest-growing markets for digital services, and micro mobile data centers are becoming increasingly popular in various sectors, including e-commerce, telecommunications, and manufacturing, to support edge computing workloads, improve network performance, and comply with data localization regulations. The push towards smart cities, the development of 5G networks, and the availability of cost-competitive micro data center solutions from domestic manufacturers are key factors propelling the market in China.

Micro Mobile Data Center Market Share

The micro mobile data center industry is primarily led by well-established companies, including:

Latest Developments in Global Micro Mobile Data Center Market

In October 2024, Zella DC introduced the Zella Outback. This outdoor micro data center was specifically designed for edge computing and optimized to perform reliably in challenging environments. This new enterprise size offered several environmental advantages, including enhanced insulation and modular panels for easier maintenance and quick replacements during extreme weather. Furthermore, it included improved security features such as upgraded access control with remote pin management and multi-factor authentication, along with optional fireproofing and a reinforced condenser cage

In November 2023, Schneider Electric, a leading company in digital transformation for energy management and automation, revealed a USD 3 billion multi-year agreement with Compass Datacenters. This agreement, which extends their existing partnership, focuses on integrating their supply chains to manufacture and deliver prefabricated modular data center solution

In June 2023, Secure I.T. Environments, known for providing secure IT environments, delivered a micro data center to Barnet Hospital's intensive care unit (ICU) in London, United Kingdom. The 42U Micro Data Center, housed in a containerized facility, supports up to a 12kW load and will provide essential network and communications services for the ICU’s operational needs

In November 2022, Schneider Electric launched the EcoStruxure Micro Data Center R-Series 42U Medium Density. This initiative expanded Schneider Electric's range of ruggedized micro data center offerings. The new enterprise size aimed to simplify the ordering and deployment process by providing IT professionals and enterprise size providers with a complete, pre-integrated solution, ultimately improving operational efficiency

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

Interactive Data Analysis Dashboard

Company Analysis Dashboard for high growth potential opportunities

Research Analyst Access for customization & queries

Competitor Analysis with Interactive dashboard

Latest News, Updates & Trend analysis

Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.

Frequently Asked Questions

Who are major players in micro mobile data center market?

Companies such as Corgan (U.S.), Currie & Brown Holdings Limited (U.K.), DPR Construction (U.S.), Holder Construction Group LLC (U.S.), and AECOM (U.S.) are the major companies in the micro mobile data center market.

What are the recent product launches by major companies in the micro mobile data center market?

In October 2024, Zella DC introduced the Zella Outback. This outdoor micro data center was specifically designed for edge computing and optimized to perform reliably in challenging environments.

Which countries data is covered in the micro mobile data center market?

The countries covered in the micro mobile data center market are U.S., Canada, Mexico, Germany, France, U.K., Italy, Spain, Russia, Turkey, Netherlands, Switzerland, Austria, Poland, Norway, Ireland, Hungary, Lithuania, rest of Europe, China, Japan, India, South Korea, Australia, Taiwan, Philippines, Thailand, Malaysia, Vietnam, Indonesia, Singapore, rest of Asia-Pacific, Brazil, Argentina, Chili, Colombia, Peru, Venezuela, Ecuador, Uruguay, Paraguay ,Bolivia, Trinidad And Tobago, Curaçao, rest Of South America, South Africa, Saudi Arabia, U.A.E, Egypt, Israel, Kuwait, rest of Middle East and Africa, Guatemala, Costa Rica, Honduras, EL Salvador, Nicaragua, and rest of Central America.

Claudio Rondena

Group Business Development & Strategic Marketing Director, C.O.C Farmaceutici SRL

"This morning we were involved in the first part, the data presentation of MKT analysis, selected abstract from your work. The board team was really impressed and very appreciated, as well."

David Manning - Thermo Fisher Scientific

Director, Global Strategic Accounts,

Dear Ricky, I want to thank you for the excellent market analysis (LIMS INSTALLED BASE DATA) that you and your team delivered, especially end of year on short notice.

Sachin and Shraddha captured the requirements, determined their path forward and executed quickly.

You, Sachin and Shraddha have been a pleasure to work with – very responsive, professional and thorough.

Your work is much appreciated.

Manager - Market Analytics,

Uriah D. Avila - Zeus Polymer Solutions

Thank you for all the assistance and the level of detail in the market report. We are very pleased with the results and the customization. We would like to continue to do business.

Business Development Manager,

(Pharmaceuticals Partner for Nasal Sprays) | Renaissance Lakewood LLC

DBMR was attentive and engaged while discussing the Global Nasal Spray Market. They understood what we were looking for and was able to provide some examples from the report as requested. DBMR Service team has been responsive as needed. Depending on what my colleagues were looking for, I will recommend your services and would be happy to stay connected in case we can utilize your research in the future.

Business Intelligence and Analytics,

Ipsen Biopharm Limited

We are impressed by the CENTRAL PRECOCIOUS PUBERTY (CPP) TREATMENT report - so a BIG thanks to you colleagues.

Competition Analyst,

Basler Web

I just wanted to share a quick note and let you know that you guys did a really good job. I’m glad I decided to work with you. I shall continue being associated with your company as long as we have market intelligence needs.

Marketing Director,

Buhler Group

It was indeed a good experience, would definitely recommend and come back for future prospects.

COO,

A global leader providing Drug Delivery Services

DBMR did an outstanding job on the Global Drug Delivery project, We were extremely impressed by the simple but comprehensive presentation of the study and the quality of work done. This report really helped us to access untapped opportunities across the globe.

Marketing Director,

Philips Healthcare

The study was customized to our targets and needs with well-defined milestones. We were impressed by the in-depth customization and inclusion of not only major but also minor players across the globe. The DBMR Market position grid helped us to analyze the market in different dimension which was very helpful for the team to get into the minute details.

Product manager,

Fujifilms

Thankful to the team for the amazing coordination, and helping me at the last moment with my presentation. It was indeed a comprehensive report that gave us revenue impacting solution enabling us to plan the right move.

Investor relations,

GE Healthcare

Thank you for the report, and addressing our needs in such short time. DBMR has outdone themselves in this project with such short timeframe.

Market Analyst,

Medincell

We found the results of this study compelling and will help our organization validate a market we are considering to enter. Thank you for a job well done.

Andrew - Senior Global Marketing Manager,

Medtronic (US)

I want to thank you for your help with this report – It’s been very helpful in our business planning and it well organized.

Amarildo - Manager, Global Strategic Alignment

MasterCard

We believe the work done by Data Bridge Team for our requirements in the North America Loyalty Management Market was fantastic and would love to continue working with your team moving forward.

Tor Hammer

Green Nexus LLc

Thank you for your quick response to this unfortunate circumstance. Please extend my thanks to your reach team. I will be contacting you in the future with further projects

I acknowledge the difficulty given by the very short warning for this report, and I think that its quality and your delivering time have been very satisfying.

Obviously, as a provider Data Bridge Market Research will be considered as a plus for future needs of Nippon Gases.

Yuki Kopyl (Asian Business Development Department)

UENO FOOD TECHNO INDUSTRY, LTD. (JAPAN)

Xylose report was very useful for our team. Thank you very much & hope to work with you again in the future