Global Meat Ingredients Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

44.30 Billion

USD

68.90 Billion

2024

2032

USD

44.30 Billion

USD

68.90 Billion

2024

2032

| 2025 –2032 | |

| USD 44.30 Billion | |

| USD 68.90 Billion | |

| % | |

|

글로벌 육류 원료 시장 세분화(성분별: 결합제, 증량제, 충전제, 착색제, 향미제, 방부제, 질감제, 소금, 기타), 육류 종류(양고기, 닭고기, 소고기, 돼지고기, 기타), 제품 종류(신선 가공육, 생고기 및 조리육, 반조리육, 기타) - 2032년까지의 산업 동향 및 전망

육류 재료 시장 규모

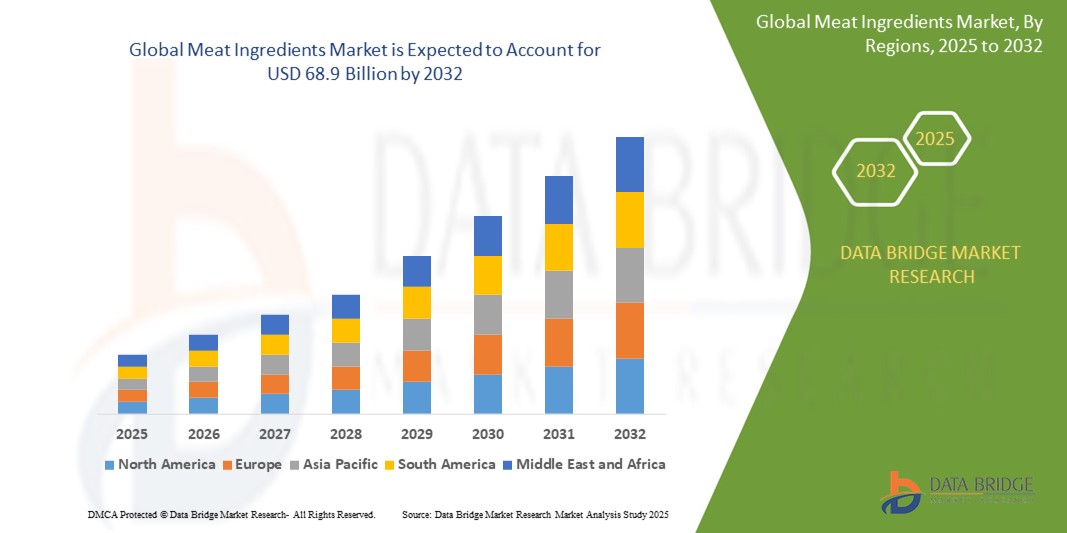

- 글로벌 육류 성분 시장 규모는 2024년에 443억 달러 로 평가되었으며 예측 기간 동안 5.31%의 CAGR 로 2032년까지 689억 달러에 도달할 것으로 예상됩니다 .

- 시장 성장은 주로 가공육 및 편의육 제품에 대한 글로벌 수요 증가와 고단백질 식단 및 기능성 육류 품목에 대한 소비자 선호도 증가에 의해 주도됩니다.

- 또한, 육류 가공 기술의 발전과 식품 안전 및 보존에 대한 투자 증가는 육류 재료의 기능성과 매력을 향상시키고 있습니다. 이러한 요소들이 결합되어 글로벌 육류 재료 산업의 탄탄한 성장을 견인하고 있습니다.

육류 재료 시장 분석

- 방부제, 결합제, 충전제, 향미제, 증량제, 질감제 등을 포함한 육류 성분은 소매 및 식품 서비스 부문 모두에서 가공육 제품의 유통기한, 질감, 풍미, 영양 프로필을 향상시키는 데 점점 더 중요해지고 있습니다.

- 육류 재료에 대한 수요가 급증한 주된 이유는 가공육류와 즉석섭취 육류 제품의 소비 증가, 단백질이 풍부한 식단을 장려하는 건강 의식 제고, 육류 가공 및 보존 기술의 발전 때문입니다.

- 북미는 2025년에 가장 큰 매출 점유율을 기록하며 글로벌 육류 성분 시장을 장악할 것으로 예상됩니다. 이는 1인당 육류 소비량이 높고, 주요 식품 가공 기업의 입지가 강하며, 기능성 및 강화 육류 제품에 대한 소비자 선호도가 높아지고 있기 때문입니다.

- 아시아 태평양 지역은 예측 기간 동안 글로벌 육류 성분 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다. 이는 도시화 증가, 중산층 인구 증가, 식습관 변화, 중국과 인도 등 국가에서 가공육 산업의 급속한 성장에 기인합니다.

- 결합제 및 증량제 부문은 2025년에 43.2%의 시장 점유율로 육류 성분 시장을 장악할 것으로 예상됩니다. 이는 특히 빠르게 성장하고 있는 가공식품 및 편의식품 부문에서 육류 제품의 질감, 수율 및 비용 효율성을 개선하는 데 중요한 역할을 하기 때문입니다.

보고서 범위 및 육류 성분 시장 세분화

|

속성 |

육류 재료 주요 시장 통찰력 |

|

다루는 세그먼트 |

|

|

포함 국가 |

북아메리카

유럽

아시아 태평양

중동 및 아프리카

남아메리카

|

|

주요 시장 참여자 |

|

|

시장 기회 |

|

|

부가가치 데이터 정보 세트 |

Data Bridge Market Research에서 큐레이팅한 시장 보고서에는 시장 가치, 성장률, 세분화, 지리적 적용 범위, 주요 기업 등 시장 시나리오에 대한 통찰력 외에도 심층적인 전문가 분석, 가격 분석, 브랜드 점유율 분석, 소비자 설문 조사, 인구 통계 분석, 공급망 분석, 가치 사슬 분석, 원자재/소모품 개요, 공급업체 선택 기준, PESTLE 분석, Porter 분석 및 규제 프레임워크가 포함되어 있습니다. |

육류 재료 시장 동향

" 클린 라벨과 기능성 성분이 혁신을 이끈다 "

- 글로벌 육류 성분 시장에서 중요하고 가속화되는 추세는 식품 생산에서 건강, 투명성 및 지속 가능성에 대한 소비자 인식이 높아짐에 따라 클린 라벨 및 기능성 육류 성분에 대한 수요가 증가하고 있다는 것입니다.

- 소비자들은 천연 방부제, 식물성 결합제 및 최소한의 인공 첨가물로 제조된 육류 제품을 점점 더 많이 찾고 있으며, 이로 인해 제조업체는 식초 추출물, 감귤 섬유 및 로즈마리와 녹차 추출물과 같은 천연 항산화제와 같은 성분을 사용하여 제품을 재구성하고 있습니다.

- 섬유질이 풍부한 충전제, 단백질 강화제, 저염 풍미 강화제와 같은 영양 프로필을 향상시키는 기능성 육류 성분이 건강을 중시하고 부가가치가 있는 육류 제품을 찾는 노령층 사이에서 특히 인기를 얻고 있습니다.

- 식물성 및 알레르기 없는 성분의 채택도 증가하고 있어 더 넓은 시장 호소력과 클린 라벨 추세 준수가 가능해지고 식이 제한 및 윤리적 소비자 선호도에 부응할 수 있습니다.

- This trend is supported by innovations in ingredient processing technologies—such as microencapsulation and controlled-release delivery systems—that improve functionality, flavor retention, and shelf stability without compromising the clean-label appeal

Meat Ingredients Market Dynamics

Driver

“Rising Demand for Processed Meat and Protein-Enriched Diets”

- The growing global demand for processed and convenience meat products, along with an increasing emphasis on high-protein diets, is a major driver for the Global Meat Ingredients Market

- Urbanization, evolving lifestyles, and rising incomes have led to greater consumption of ready-to-cook and ready-to-eat meat products, which heavily rely on a range of meat ingredients such as binders, fillers, preservatives, and flavor enhancers to improve shelf life, taste, and texture

- For instance, leading players like Kerry Group and IFF are expanding their portfolios to meet the functional and sensory demands of modern meat formulations, supporting clean-label and health-oriented trends

- Additionally, the growing health consciousness among consumers is spurring demand for fortified and functional meat products, which incorporate meat ingredients that enhance nutritional value, such as protein isolates, dietary fibers, and natural antioxidants

- This growing awareness and demand for functional, high-protein foods—especially in regions like North America and Asia-Pacific—is expected to significantly boost the adoption of meat ingredients in the coming years

Restraint/Challenge

“Stringent Regulations and Growing Clean Label Demands”

- One of the key challenges for the Meat Ingredients Market is the increasing regulatory scrutiny on the use of artificial additives, preservatives, and flavor enhancers, particularly in regions such as the European Union and North America

- Regulatory bodies are imposing stricter food safety standards and labeling requirements, which can limit the use of certain synthetic ingredients, requiring manufacturers to invest in clean label alternatives that meet both regulatory and consumer expectations

- For example, the demand for natural preservatives over traditional nitrites and phosphates is increasing, but formulating with natural alternatives often presents technical challenges in terms of product stability and shelf life

- Additionally, the rising consumer awareness about ingredient transparency and clean labels is compelling meat processors to reformulate products, sometimes at a higher production cost, which can restrain profitability and scalability, particularly for small to mid-sized players

- Successfully navigating these challenges will require continuous innovation in ingredient development, strategic collaborations, and transparent marketing strategies to align with consumer and regulatory demands

Meat Ingredients Market Scope

The market is segmented on the basis of ingredient, meat type and product type.

- By Ingredient

On the basis of ingredient, the meat ingredients market is segmented into binders, extenders, fillers, colouring agents, flavouring agents, preservatives, texturing agents, salts and others. The binders segment dominates the largest market revenue share of 43.2% in 2025, driven by its vital role in improving meat texture, water retention, and product consistency. Binders such as soy protein, starches, and gums are widely used in processed meats to maintain structure and enhance yield, making them highly valuable to manufacturers.

The flavouring agents segment is anticipated to witness the fastest growth rate of 21.7% from 2025 to 2032, fueled by increasing consumer demand for enhanced taste and sensory experiences in meat products. The growing popularity of ethnic and regional flavor profiles is also pushing innovation in this category, particularly in convenience and ready-to-eat meat segments.

- By Meat Type

On the basis of communication protocol, the meat ingredients market is segmented into mutton, chicken, beef, pork and others. The chicken segment held the largest market revenue share in 2025, driven by its widespread global consumption, cost-effectiveness, and suitability for diverse meat products like sausages, nuggets, and deli meats. The adaptability of chicken to various meat ingredient formulations also supports its dominant position.

The beef segment is expected to witness the fastest CAGR from 2025 to 2032, supported by increasing demand for high-protein diets, particularly in North America and Asia-Pacific. The rising popularity of gourmet and premium beef products is encouraging the use of specialized meat ingredients that enhance flavor, juiciness, and shelf life.

- By Product Type

Based on the product type, the meat ingredients market is segmented into fresh processed meat, raw & cooked meat, pre-cooked meat and others. The fresh processed meat segment held the largest market revenue share in 2025, owing to the high consumption of sausages, patties, and meatballs globally. This category relies heavily on meat ingredients for preservation, binding, and flavoring to ensure product quality and extended shelf life.

The pre-cooked meat segment is expected to witness the fastest CAGR from 2025 to 2032, driven by rising demand for convenient, ready-to-eat meals among urban consumers. Meat ingredients used in this category play a critical role in maintaining product integrity during reheating and storage, thereby enhancing consumer satisfaction and repeat purchases.

Meat Ingredients Market Regional Analysis

- North America dominates the Meat Ingredients market with the largest revenue share of 40.01% in 2024, driven by a high demand for processed and convenience meat products and increasing consumer preference for clean-label and functional ingredients

- The region's well-established meat processing industry, particularly in the United States, is fostering innovation in ingredient formulations, including natural preservatives, binders, and flavor enhancers that align with health-conscious trends

- Additionally, strong regulatory frameworks, high disposable incomes, and a growing focus on protein-enriched diets contribute to the expansion of the meat ingredients market across retail and foodservice channels

- The presence of major industry players such as Kerry Group, IFF, and ADM in North America further accelerates product innovation and market penetration, making the region a critical hub for meat ingredient advancements

U.S. Meat Ingredients Market Insight

The U.S. Meat Ingredients market captured the largest revenue share of 81% within North America in 2025, fueled by the robust meat processing industry, high consumer demand for value-added meat products, and growing interest in clean-label and functional ingredients. Increasing health consciousness among consumers is driving the adoption of natural binders, flavor enhancers, and preservative alternatives. Additionally, innovation in meat analogs and plant-based meat products is further propelling demand for specialized ingredients that replicate traditional meat textures and flavors.

Europe Meat Ingredients Market Insight

The European Meat Ingredients market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent food safety regulations and the rising demand for high-quality processed meat products. Clean-label trends and increasing consumer preference for natural and organic ingredients are fostering innovations in ingredient formulations. The region's well-developed food processing industry and shifting dietary habits, especially in Germany, France, and Italy, are contributing to steady market growth across both traditional meat and alternative protein sectors.

U.K. Meat Ingredients Market Insight

The U.K. Meat Ingredients market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising demand for ready-to-eat and on-the-go meat snacks and increased awareness around ingredient transparency. The trend toward plant-based and flexitarian diets is encouraging meat processors to enhance formulations with texturizing and flavoring ingredients that appeal to changing consumer palates. Moreover, the emphasis on sustainability and traceability in food production supports the adoption of functional and natural meat ingredients.

Germany Meat Ingredients Market Insight

독일 육류 원료 시장은 프리미엄 고단백 육류 제품에 대한 소비자 수요와 가공육 제품의 혁신에 힘입어 예측 기간 동안 상당한 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 독일의 탄탄한 육류 수출 부문과 유럽 식품 가공 시장에서의 선도적인 입지는 유화제, 안정제, 향미제 사용량 증가에 기여하고 있습니다. 또한, 무첨가 및 유기농 육류 제품 추세는 독일 제조업체 전반의 제품 개량 전략을 촉진하고 있습니다.

아시아 태평양 육류 원료 시장 통찰력

아시아 태평양 육류 원료 시장은 도시화 증가, 식생활 변화, 그리고 가처분소득 증가에 힘입어 2025년까지 24% 이상의 가장 빠른 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 중국, 인도, 동남아시아 등지의 육류 소비가 급증함에 따라 제품 안전성, 맛, 그리고 유통기한을 향상시키는 육류 가공 원료에 대한 수요가 급증하고 있습니다. 또한, 현대식 소매 채널과 포장 식품의 성장은 이 지역 시장에서 방부제, 결합제, 그리고 풍미 증진제의 도입을 촉진하고 있습니다.

일본 육류 재료 시장 통찰력

일본 육류 원료 시장은 특히 고령화 사회에서 편리하고 고품질의 육류 제품에 대한 수요가 증가함에 따라 성장세가 가속화되고 있습니다. 가공육과 즉석식품 소비 증가는 맛, 식감, 그리고 영양을 향상시키는 기능성 원료에 대한 수요를 견인하고 있습니다. 일본 식품 제조업체들은 변화하는 소비자 선호도에 맞춰 클린 라벨, 저염, 건강 중심의 육류 원료 솔루션에 점점 더 집중하고 있습니다.

중국 육류 재료 시장 통찰력

중국 육류 원료 시장은 2025년 아시아 태평양 지역에서 가장 큰 시장 점유율을 차지할 것으로 예상되는데, 이는 높은 육류 소비량, 육류 가공 용량의 빠른 성장, 그리고 가공 및 부가가치 육류 제품에 대한 수요 증가에 기인합니다. 중국이 포장 및 브랜드 육류로 전환함에 따라 방부제, 색소, 향료 사용이 급증하고 있습니다. 국내 혁신, 식품 안전에 대한 정부 지원, 그리고 건강에 대한 인식 제고는 중국 육류 가공 산업 전반의 원료 사용량을 좌우하고 있습니다.

육류 재료 시장 점유율

육류 성분 산업은 주로 다음을 포함한 잘 확립된 회사들이 주도하고 있습니다.

- 케리 그룹 plc(아일랜드)

- 케민 인더스트리즈(Kemin Industries, Inc.)(미국)

- 인그리디언 주식회사(미국)

- EI du Pont de Nemours and Company(미국)

- Associated British Foods plc(영국)

- 에센시아 단백질 솔루션(미국)

- 프루타롬(이스라엘)

- 웬다 재료(미국)

- 어드밴스드 푸드 시스템즈(Advanced Food Systems, Inc.) (미국)

- 코르비온 NV(네덜란드)

- NEXIRA(프랑스)

- ADM(Archer Daniels Midland Company)(미국)

- BASF SE(독일)

- DSM-Firmenich(네덜란드)

- Ohly GmbH(독일)

- Proliant 고기 성분(미국)

- IFF(미국)

- 지보당(스위스)

글로벌 육류 재료 시장의 최신 동향

- 2023년 3월, Kemin Industries는 가공육 제품의 수확량, 질감 및 유통기한을 향상시키도록 설계된 새로운 클린 라벨 기능성 성분 라인을 출시하여 천연 및 지속 가능한 육류 솔루션에 대한 소비자 수요 증가를 타겟으로 했습니다.

- 2023년 1월, Ingredion Incorporated는 Kalsec Inc.와 협력하여 육류 및 가금류 응용 분야에 특별히 맞춤화된 천연 향미료 및 색상 솔루션을 공동 개발하여 제품 매력도와 클린 라벨 포지셔닝을 강화했습니다.

- 2022년 10월, Essentia Protein Solutions는 성능 중심의 동물성 재료를 원하는 제조업체를 대상으로 조리 및 사전 조리된 육류 제품의 육즙과 결합력을 향상시키는 것을 목표로 하는 새로운 돼지고기 기반 단백질 성분 제품군을 출시했습니다.

- 2022년 6월, Corbion NV는 합성 첨가물 감소에 대한 규제 및 소비자의 압력이 높아지는 상황에서도 자연스러운 유통기한 연장을 제공하는 가공육용 최신 식초 기반 보존 시스템을 출시했습니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.