북미 실험실 자동화 시장, 제품 유형별(장비, 소프트웨어 및 정보학 및 분석기), 자동화 유형(모듈식 자동화 및 전체 실험실 자동화), 응용 분야(신약 발견, 임상 진단, 유전체학 솔루션, 단백질체학 솔루션, 생물 분석, 단백질 공학, 동결 건조, 시스템 생물학, 분석 화학 및 기타), 최종 사용자(생명 공학 및 제약, 병원 및 실험실, 연구 및 학술 기관 및 기타) - 업계 동향 및 2029년까지의 예측.

북미 실험실 자동화 시장 분석 및 통찰력

전 세계적으로 기술이 발전함에 따라 실험실 자동화 시장에 대한 수요가 증가하고 있습니다. 의료 분야에서는 실험실 자동화 장비와 도구가 사용됩니다. 여러 요인으로 인해 의료 지출이 증가함에 따라 선도적인 제약 및 의료 회사는 더 짧은 시간 내에 문 앞에서 고급 의료 서비스를 제공하기 위해 실험실을 자동화해야 합니다.

시장에서 증가하는 의료 수요는 전 세계적으로 실험실 자동화 개선에 있어서 선도적인 의료 및 제약 회사 간의 경쟁의 주요 원인입니다. 실험실을 위한 장비, 분석기 및 소프트웨어 사용이 증가했습니다. 시장 참여자의 초점은 자동화된 실험실 인프라의 개발 및 제조를 지원하기 위한 다양한 도구, 장비, 기계 및 기술을 제공하는 것입니다. 시장 참여자는 첨단 기술과 방법을 구축하기 위해 더 많은 투자와 자금을 제공하고 있습니다.

의료비 지출은 인구 고령화, 만성 질환 유병률, 약물 가격 상승, 의료 서비스 비용 및 행정 비용 등 여러 요인으로 인해 증가했습니다. 게다가 병원, 사립 실험실, 임상 연구 및 진단 센터가 증가하면서 실험실 자동화 시장 수요가 증가하고 있습니다.

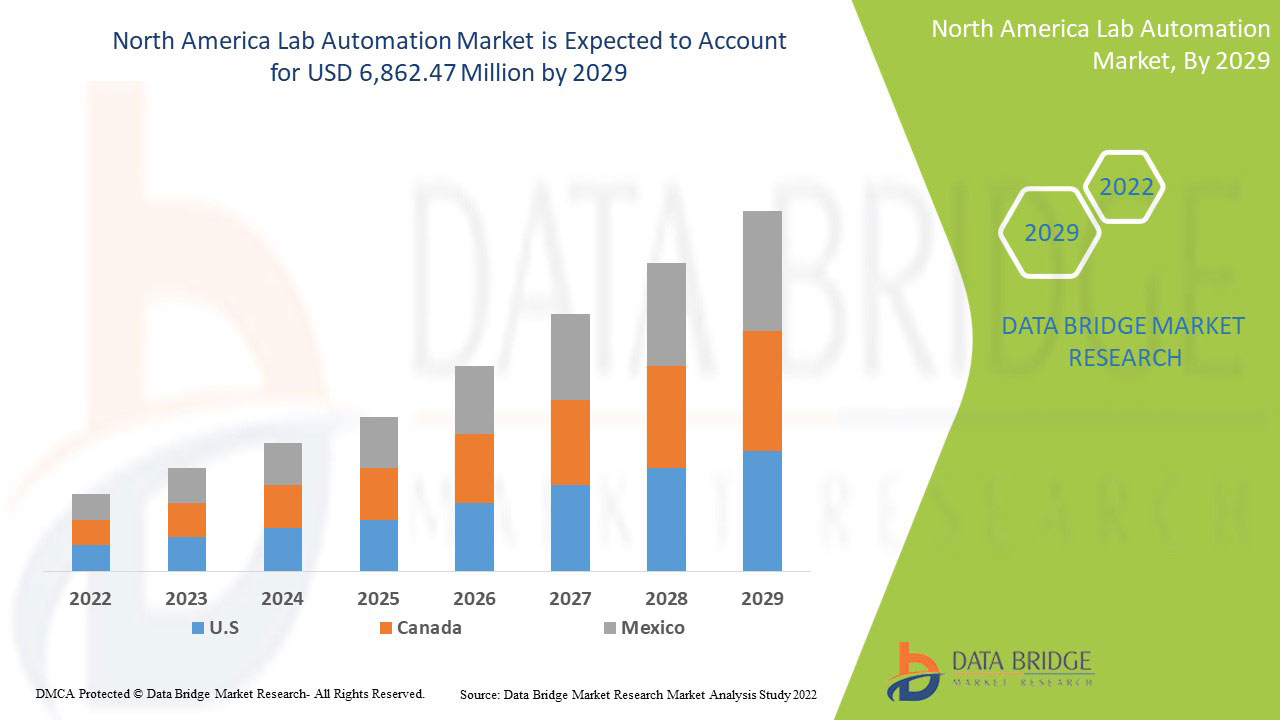

북미 랩 자동화 시장은 2022년부터 2029년까지의 예측 기간 동안 시장 성장을 이룰 것으로 예상됩니다. Data Bridge Market Research는 시장이 2022년부터 2029년까지의 예측 기간 동안 6.8%의 CAGR로 성장하고 있으며 2029년까지 6,862.47백만 달러에 도달할 것으로 분석합니다.

|

보고서 메트릭 |

세부 |

|

예측 기간 |

2022년부터 2029년까지 |

|

기준 연도 |

2021 |

|

역사적 연도 |

2020 (2019-2014로 사용자 정의 가능) |

|

양적 단위 |

수익 (단위: USD 백만) |

|

다루는 세그먼트 |

제품 유형(장비, 소프트웨어 및 정보학 및 분석기), 자동화 유형(모듈식 자동화 및 전체 실험실 자동화), 응용 프로그램(약물 발견, 임상 진단, 유전체학 솔루션, 프로테오믹스 솔루션, 생물 분석, 단백질 공학, 동결 건조, 시스템 생물학, 분석 화학 및 기타), 최종 사용자(생명 공학 및 제약, 병원 및 실험실, 연구 및 학술 기관 및 기타) |

|

적용 국가 |

미국, 캐나다, 멕시코 |

|

시장 참여자 포함 |

Danaher, PerkinElmer Inc., Thermo Fisher Scientific Inc., Agilent Technologies, Inc., QIAGEN, F. Hoffman-La Roche Ltd, Siemens Healthcare GmbH, Abbott, Aurora Biomed Inc., BD, BIOMÉRIEUX, Eppendorf SE, LabVantage Solutions Inc., LabWare, LabLynx LIMS, Azenta US Inc., Hamilton Company, Hudson Robotics 및 Tecan Trading AG 등 |

시장 정의

실험실 자동화는 실험실에서 자동화된 기술을 결합하여 새롭고 개선된 프로세스를 가능하게 하는 것입니다. 실험실에서 기술을 연구, 개발, 최적화하고 활용하는 전략으로 사용됩니다. 특히 최소한의 인적 투입이 필요한 실험실 프로세스를 자동화하고 인적 오류를 제거하는 데 사용됩니다. 실험실 자동화는 보다 효율적인 테스트 및 진단을 제공하는 것을 목표로 사용됩니다.

실험실 자동화는 연구자와 기술자가 더 짧은 시간 안에 효율적이고 효과적으로 산출물을 생산할 수 있게 해주며, 이는 실험실 자동화 시장을 주도할 것으로 예상됩니다. 또한, 질병의 급속한 확산과 의료 분야의 새로운 발견은 진단 및 치료에 대한 수요를 증가시키며, 이는 실험실 자동화 시장을 촉진할 것으로 예상됩니다. 연구 및 발견 연구에 대한 정부 및 민간 자금 지원이 많고 주요 시장 참여자가 있는 것도 시장 성장에 기여합니다.

북미 실험실 자동화 시장 역학

운전자

- 시장 참여자들의 투자 및 전략적 이니셔티브 증가

실험실 자동화 시장은 인적 오류를 제거하는 전문화된 고급 자동화 서비스에 대한 수요가 높기 때문에 증가하고 있습니다. 시장 참여자와 회사의 초점은 자동화된 실험실 인프라의 개발 및 제조를 지원하기 위해 다양한 도구, 장비, 기계 및 기술을 제공하는 것입니다. 실험실 자동화 시장은 인적 오류를 제거하는 전문화된 고급 자동화 서비스에 대한 수요가 높기 때문에 증가하고 있습니다. 북미 시장 점유율을 확보하기 위해 시장 참여자는 고급 기술과 방법을 구축하기 위해 더 많은 투자와 자금을 제공하고 있습니다. 이러한 참여자는 전통적으로 노동 집약적인 프로세스에 대한 수동 작업과 실무 시간을 줄이는 데 더 집중하고 있습니다. 이는 시장 성장을 촉진할 것으로 예상됩니다.

- 실험실 인프라 강화를 위한 정부 이니셔티브

의료 분야와 실험실 인프라를 더욱 강화하기 위해 정부 기관은 중요한 역할을 합니다. 실험실 자동화를 확대하기 위한 정부의 자금 지원과 이니셔티브는 시장 성장을 돕고 시장 참여자를 늘릴 것입니다. 시장의 주요 참여자와의 정부 협력 및 협정은 실험실 인프라를 더욱 강화할 것입니다.

- 실험실 자동화 도구 및 장비에 대한 지출 증가

실험실 자동화 도구 및 장비에 대한 지출이 증가하고 있습니다. 이는 주로 인구 고령화, 만성 질환 증가, 새롭고 더 효과적인 바이오마커 발견, 전반적인 건강 또는 진단 수요 증가 등 다양한 이유로 실험실 검사에 대한 수요가 빠르게 증가하고 있기 때문입니다.

- 인간의 노력을 줄이고 인간의 오류를 없애다

인적 오류를 줄이는 전통적인 방법은 여러 가지가 있지만, 인적 오류의 위험을 최소화하는 시스템을 개발하면 같은 실수를 다시 하지 않도록 하는 데 도움이 됩니다. 제조 시설은 인공 지능 기술을 활용하여 문제가 발생하기 전에 인식하고 수정하기 위해 고급 시스템을 구축하는 데 중점을 둡니다.

기회

-

증가하는 의료비

의료비 지출은 인구 고령화, 만성 질환 유병률, 약물 가격 상승, 의료 서비스 비용 및 행정 비용 등 여러 요인으로 인해 증가했습니다. 그러나 2020년은 COVID-19 팬데믹으로 인해 지출이 가장 높은 순위를 차지한 전환점이었습니다. 2020년 의료비 지출은 팬데믹으로 인해 2002년 이후 가장 빠른 성장률로 증가한 것으로 나타났습니다 .

-

주요 참여자들의 전략적 이니셔티브

선도적인 제약 및 의료 회사는 짧은 시간 내에 고급 의료 서비스를 집 앞까지 제공하기 위해 실험실을 자동화하기 위한 다양한 이니셔티브를 취했습니다. 시장에서 증가하는 의료 수요는 전 세계적으로 실험실 자동화 개선을 위한 선도적인 의료 및 제약 회사 간의 경쟁의 주요 원인입니다. 따라서 시장 참여자의 전략적 이니셔티브는 실험실 자동화 시장 성장의 기회로 작용할 것으로 예상됩니다.

-

제약회사 수의 증가

제약 산업은 지난 20년 동안 상당한 성장을 경험했습니다. 가처분 소득 증가, 의료 시설 접근성 증가, 사람들 사이에서 의료에 대한 의식 증가, 의료 서비스 침투 증가로 인해 제약 회사가 수요를 충족하기 위해 수가 증가하고 있습니다.

COVID-19 팬데믹은 의료 서비스와 약물 공급에 대한 수요 증가로 인해 제약 산업에 큰 영향을 미쳤습니다. 제약 산업은 인류의 높은 수요를 충족하기 위해 전 세계적으로 빠르게 성장해 왔기 때문에 서비스는 최대한 빨리 제공되어야 합니다. 따라서 짧은 시간 내에 오류 없는 신속한 서비스를 제공하는 고급 의료 시설을 달성하려면 실험실 자동화가 필요합니다. 따라서 제약 회사의 수 증가는 실험실 자동화 시장 성장의 기회로 작용할 것으로 예상됩니다.

제약/도전

- 새로운 복합 제품의 한계 분석

자동화된 실험실에서 사용되는 새로운 제품의 복잡성에 기여하는 다양한 요소가 있습니다. 개발 프로세스 초기에 직원과 장치 제조업체 간의 지속적인 참여는 매우 필요하며 부품이나 전체 설정을 작동하기 위해 이해하는 것이 필수적입니다. 기계, 도구 및 장비와 같은 새로운 복잡한 제품의 탐지 및 분석에 대한 제한은 시장에서 자동화된 실험실의 설치 및 작업을 방해하고 있습니다.

- 설치 및 설정 비용이 많이 듭니다

실험실 자동화 설치 및 설정은 훨씬 더 노동 집약적이고 복잡한 절차입니다. 자동화된 실험실을 설정하려면 많은 시간, 노력, 계획, 구현 및 다양한 정부 부서의 승인이 필요합니다. 게다가 새로운 실험실을 설정하는 데 필수적인 것은 고급 기계, 도구 및 장비의 높은 비용으로 인해 인프라에 대한 중요한 투자가 필요합니다.

- 업그레이드, 유지관리 및 정기점검

설치 후 실험실을 효율적으로 운영하는 것이 가장 중요한 관심사입니다. 장비의 유지 관리, 업그레이드 및 정기적인 점검은 운영에 필요합니다. 이를 위해 필요한 비용은 시장 참여자에게 주요 제약 요소 중 하나입니다. 실험실 보유자는 원활하게 운영하고 상황을 피하기 위해 제조 회사와 관계없이 제품을 테스트하도록 규정 또는 품질 관리에 의해 의무화됩니다. 이는 시장 성장을 제한할 수 있습니다.

COVID-19 이후 실험실 자동화 시장에 미치는 영향

COVID-19는 자동화 시장에 긍정적인 영향을 미쳤습니다. 팬데믹으로 인해 사람들의 건강이 영향을 받았고, 이로 인해 진단 검사가 많이 이루어졌고 수요가 증가했습니다. 팬데믹으로 인해 개인 실험실, 병원 및 임상 연구가 증가했습니다. 따라서 COVID-19는 실험실 자동화 시장을 긍정적으로 증가시켰습니다.

최근 개발 사항

- 2022년 6월, BD는 비상장 회사인 Straub Medical AG의 인수를 완료했다고 발표했습니다. 이 인수를 통해 회사는 Straub Medical AG의 귀중한 전문 지식과 경험을 추가하고 제품 포트폴리오를 확장했습니다.

- 2022년 1월, QIAGEN은 비침습적 산전 검사 솔루션을 제공하기 위해 Atlia Biosystems와 새로운 협력을 체결했다고 발표했습니다.

북미 실험실 자동화 시장 범위

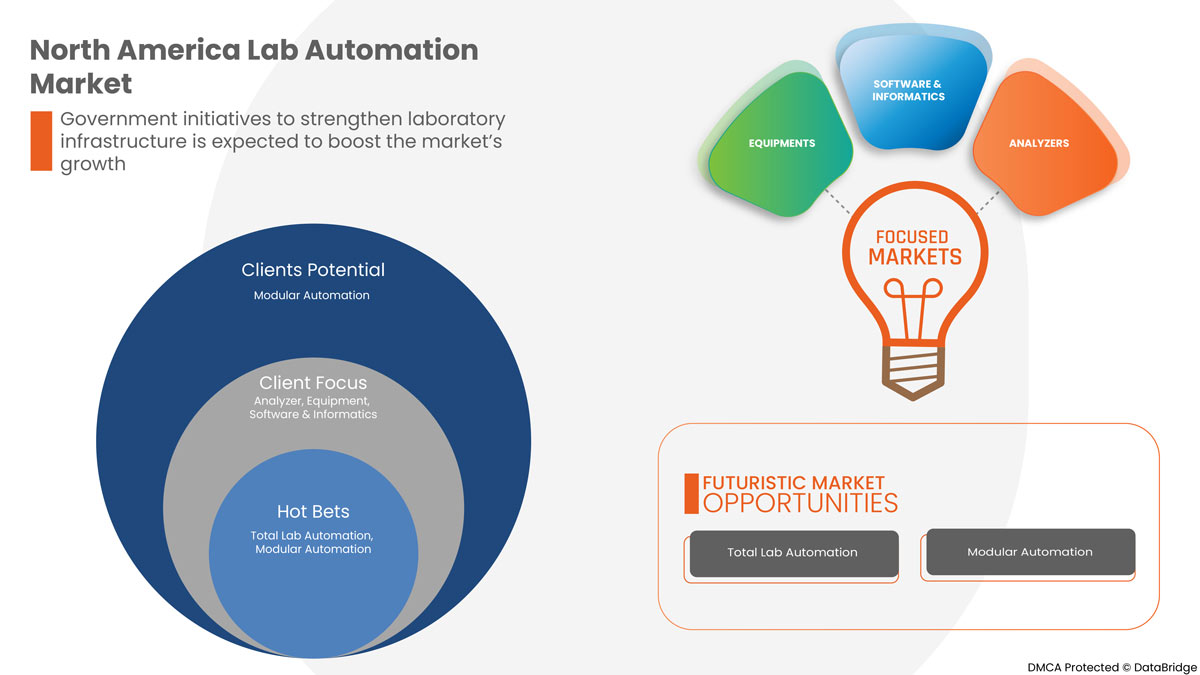

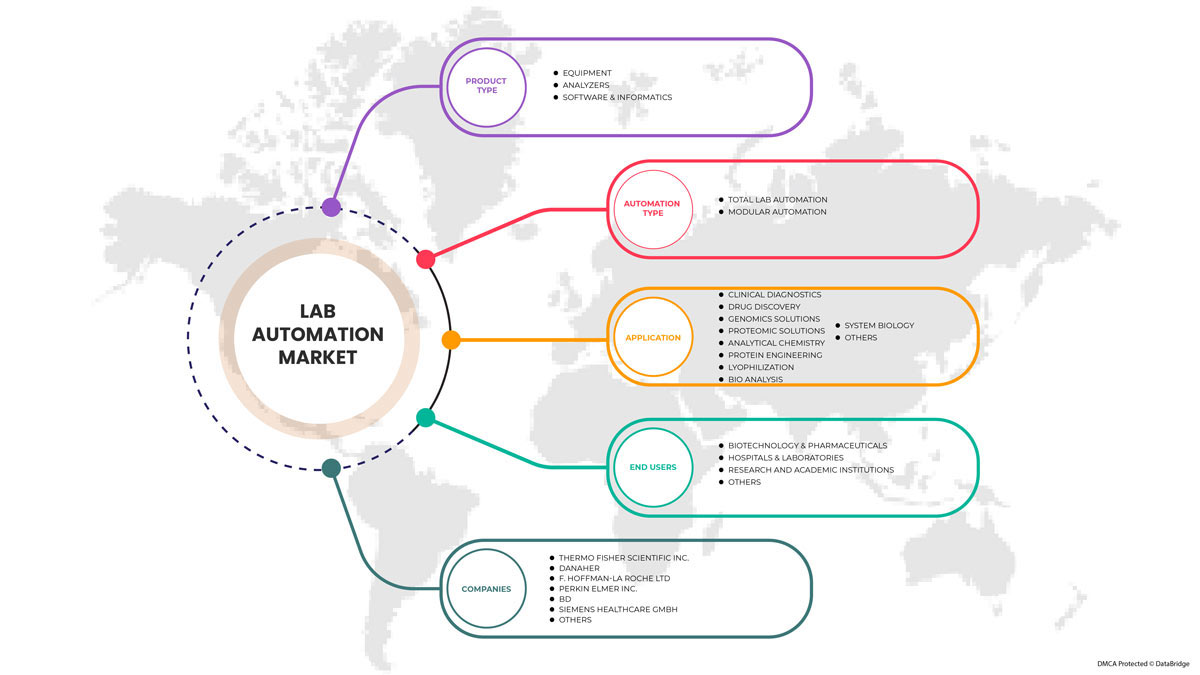

북미 실험실 자동화 시장은 제품 유형, 자동화 시스템, 애플리케이션 및 최종 사용자로 세분화됩니다. 이러한 세그먼트 간의 성장은 산업의 빈약한 성장 세그먼트를 분석하고 사용자에게 핵심 시장 애플리케이션을 식별하기 위한 전략적 결정을 내릴 수 있는 귀중한 시장 개요와 시장 통찰력을 제공하는 데 도움이 됩니다.

제품 유형

- 장비

- 분석기

- 소프트웨어 및 정보학

제품 유형을 기준으로 북미 실험실 자동화 시장은 장비, 분석기 및 소프트웨어, 정보학으로 구분됩니다.

자동화 시스템

- 전체 실험실 자동화

- 모듈식 랩 자동화

Based on automated systems, the North America lab automation market is segmented into total lab automation and modular lab automation.

Application

- Clinical Diagnostics

- Drug Discovery

- Genomics Solutions

- Proteomic Solutions

- Analytical Chemistry

- Protein Engineering

- Lyophilization

- Bio Analysis

- System Biology

- Others

Based on application, the North America lab automation market is segmented into drug discovery, clinical diagnostics, genomic solutions, proteomic solutions, bio analysis, protein engineering, lyophilization, system biology, analytical chemistry and others.

End User

- Biotechnology And Pharmaceuticals

- Hospitals & Laboratories

- Research And Academic Institutes

- Others

Based on end user, the North America lab automation market is segmented into biotechnology & pharmaceuticals, hospitals & laboratories, research and academic institutions and others.

North America Lab Automation Market Regional Analysis/Insights

The lab automation market is analyzed and country, product type, automated systems, application and end user provide market size insights and trends.

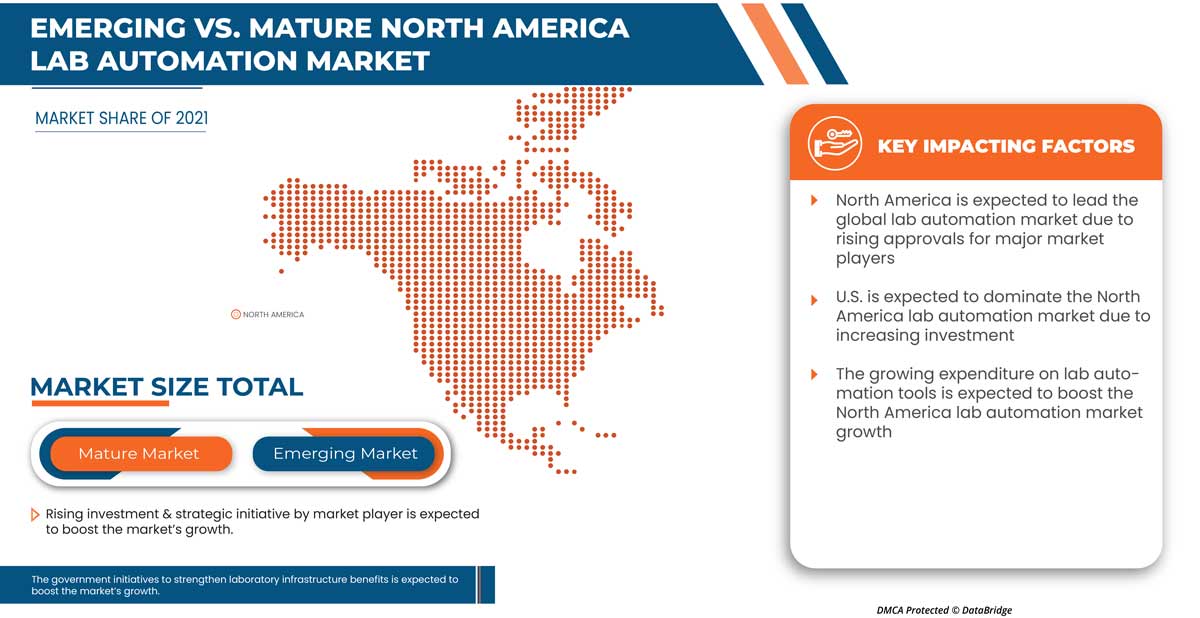

Countries covered in market are U.S., Canada, Mexico. The U.S. is expected to dominate the North America lab automation market due to a growing number of research activities and an increase in demand for drug discovery and clinical diagnostics.

The region section of the report also provides individual market impacting factors and changes in regulations in the market that impact the current and future trends of the market. Data points, such as new and replacement sales, country demographics, disease epidemiology and import-export tariffs, are some of the major pointers used to forecast the market scenario for individual countries. In addition, the presence and availability of Central America brands and their challenges faced due to high competition from local and domestic brands and the impact of sales channels are considered while providing forecast analysis of the country data.

Competitive Landscape and North America Lab Automation Market Share Analysis

North America lab automation market competitive landscape provides details by the competitors. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, North America presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth and application dominance. The above data points provided are only related to the companies focus on the North America lab automation market

Some of the major players operating in the North America lab automation market are Danaher, PerkinElmer Inc., Thermo Fisher Scientific Inc., Agilent Technologies, Inc., QIAGEN, F. Hoffman-La Roche Ltd, Siemens Healthcare GmbH, Abbott, Aurora Biomed Inc., BD, BIOMÉRIEUX, Eppendorf SE, LabVantage Solutions Inc., LabWare, LabLynx LIMS, Azenta US Inc., Hamilton Company, Hudson Robotics and Tecan Trading AG among others.

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석 및 추정됩니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 기본(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 이 외에도 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 회사 시장 점유율 분석, 측정 표준, 북미 대 지역 및 공급업체 점유율 분석이 포함됩니다. 추가 문의 사항이 있는 경우 분석가에게 전화를 요청하십시오.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE NORTH AMERICA LAB AUTOMATION MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRODUCT TYPE LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.2 PORTER’S FIVE FORCES

5 REGULATION

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 INCREASING INVESTMENT & STRATEGIC INITIATIVES BY MARKET PLAYERS

6.1.2 GOVERNMENT INITIATIVES TO STRENGTHEN LABORATORY INFRASTRUCTURES

6.1.3 GROWING EXPENDITURE ON LAB AUTOMATION TOOLS AND EQUIPMENT

6.1.4 REDUCING HUMAN EFFORTS AND ELIMINATING HUMAN ERROR

6.2 RESTRAINTS

6.2.1 LIMITATION ANALYZING NOVEL COMPLEX PRODUCT

6.2.2 HIGH COST FOR INSTALLATION AND SETUP

6.2.3 UPGRADATION, MAINTENANCE, AND PERIODICAL CHECKUPS

6.3 OPPORTUNITIES

6.3.1 RISING HEALTHCARE EXPENDITURE

6.3.2 STRATEGIC INITIATIVES BY KEY PLAYERS

6.3.3 RISE IN THE NUMBER OF PHARMA COMPANIES

6.4 CHALLENGES

6.4.1 SLOW ADOPTION OF AUTOMATION AMONG SMALL AND MEDIUM SIZED LABORATORIES

6.4.2 LIMITED FEASIBILITY WITH TECHNOLOGY INTEGRATION IN ANALYTICAL LABS

7 NORTH AMERICA LAB AUTOMATION MARKET, BY PRODUCT TYPE

7.1 OVERVIEW

7.2 EQUIPMENT

7.2.1 AUTOMATED WORKSTATIONS

7.2.1.1 AUTOMATED LIQUID HANDLING SYSTEMS

7.2.1.2 AUTOMATED INTEGRATED WORKSTATIONS

7.2.1.3 PIPETTING SYSTEMS

7.2.1.4 MICROPLATE WASHERS

7.2.1.5 REAGENT DISPENSERS

7.2.2 MICROPLATE READERS

7.2.2.1 MULTI-MODE MICROPLATE READERS

7.2.2.2 SINGLE-MODE MICROPLATE READERS

7.2.2.3 AUTOMATED NUCLEIC ACID PURIFICATION SYSTEMS

7.2.2.4 AUTOMATED ELISA SYSTEMS

7.2.3 OFF-THE-SHELF AUTOMATED WORKCELLS

7.2.4 ROBOTIC SYSTEMS

7.2.4.1 ROBOTIC ARMS

7.2.4.2 TRACK ROBOTS

7.2.5 AUTOMATE STORAGE & RETRIEVALS (ASRS)

7.2.6 OTHERS

7.3 ANALYZER

7.3.1 BIO CHEMISTRY ANALYZERS

7.3.2 HAEMATOLOGY ANALYZERS

7.3.3 IMMUNO-BASED ANALYZERS

7.4 SOFTWARE & INFORMATICS

7.4.1 LABORATORY INFORMATION MANAGEMENT SYSTEM (LIMS)

7.4.2 ELECTRONIC LABORATORY NOTEBOOK (ELN)

7.4.3 LABORATORY EXECUTION SYSTEMS (LES)

7.4.4 SCIENTIFIC DATA MANAGEMENT SYSTEMS (SDMS)

8 NORTH AMERICA LAB AUTOMATION MARKET, BY AUTOMATION TYPE

8.1 OVERVIEW

8.2 TOTAL LAB AUTOMATION

8.3 MODULAR AUTOMATION

9 NORTH AMERICA LAB AUTOMATION MARKET, BY APPLICATION

9.1 OVERVIEW

9.2 CLINICAL DIAGNOSTICS

9.3 DRUG DISCOVERY

9.4 GENOMICS SOLUTIONS

9.5 PROTEOMIC SOLUTIONS

9.6 ANALYTICAL CHEMISTRY

9.7 PROTEIN ENGINEERING

9.8 BIO ANALYSIS

9.9 SYSTEM BIOLOGY

9.1 OTHERS

10 NORTH AMERICA LAB AUTOMATION MARKET, BY END USER

10.1 OVERVIEW

10.2 BIOTECHNOLOGY & PHARMACEUTICALS

10.3 HOSPITALS & LABORATORIES

10.4 RESEARCH & ACADEMIC INSTITUTES

10.5 OTHERS

11 NORTH AMERICA LAB AUTOMATION MARKET, BY REGION

11.1 NORTH AMERICA

11.1.1 U.S.

11.1.2 CANADA

11.1.3 MEXICO

12 NORTH AMERICA LAB AUTOMATION MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 THERMO FISHER SCIENTIFIC INC.

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENTS

14.2 DANAHER

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENTS

14.3 F. HOFFMANN- LA ROCHE LTD

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENTS

14.4 PERKINELMER INC

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENTS

14.5 BD

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT PORTFOLIO

14.5.5 RECENT DEVELOPMENTS

14.6 ABBOTT

14.6.1 COMPANY SNAPSHOT

14.6.2 REVENUE ANALYSIS

14.6.3 PRODUCT PORTFOLIO

14.6.3 RECENT DEVELOPMENTS

14.7 AGILENT TECHNOLOGIES

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCT PORTFOLIO

14.7.4 RECENT DEVELOPMENTS

14.8 AURORA BIOMED INC.

14.8.1 COMPANY SNAPSHOT

14.8.2 PRODUCT PORTFOLIO

14.8.3 RECENT DEVELOPMENTS

14.9 AZENTA US INC

14.9.1 COMPANY SNAPSHOT

14.9.2 REVENUE ANALYSIS

14.9.3 PRODUCT PORTFOLIO

14.9.4 RECENT DEVELOPMENTS

14.1 BIOMERIEUX

14.10.1 COMPANY SNAPSHOT

14.10.2 REVENUE ANALYSIS

14.10.3 PRODUCT PORTFOLIO

14.10.4 RECENT DEVELOPMENTS

14.11 EPPENDORF SE

14.11.1 COMPANY SNAPSHOT

14.11.2 PRODUCT PORTFOLIO

14.11.3 RECENT DEVELOPMENTS

14.12 HAMILTON COMPANY

14.12.1 COMPANY SNAPSHOT

14.12.2 PRODUCT PORTFOLIO

14.12.3 RECENT DEVELOPMENTS

14.13 HUDSON ROBOTICS

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCT PORTFOLIO

14.13.3 RECENT DEVELOPMENTS

14.14 LABLYNX LIMS

14.14.1 COMPANY SNAPSHOT

14.14.2 PRODUCT PORTFOLIO

14.14.3 RECENT DEVELOPMENTS

14.15 LABVANTAGE SOLUTIONS INC.

14.15.1 COMPANY SNAPSHOT

14.15.2 PRODUCT PORTFOLIO

14.15.3 RECENT DEVELOPMENTS

14.16 LABWARE

14.16.1 COMPANY SNAPSHOT

14.16.2 PRODUCT PORTFOLIO

14.16.3 RECENT DEVELOPMENTS

14.17 QIAGEN

14.17.1 COMPANY SNAPSHOT

14.17.2 REVENUE ANALYSIS

14.17.3 PRODUCT PORTFOLIO

14.17.4 RECENT DEVELOPMENTS

14.18 SIEMENS HEALTHCARE GMBH

14.18.1 COMPANY SNAPSHOT

14.18.2 REVENUE ANALYSIS

14.18.3 PRODUCT PORTFOLIO

14.18.4 RECENT DEVELOPMENTS

14.19 TECAN TRADING AG

14.19.1 COMPANY SNAPSHOT

14.19.2 REVENUE ANALYSIS

14.19.3 PRODUCT PORTFOLIO

14.19.4 RECENT DEVELOPMENTS

15 QUESTIONNAIRE

16 RELATED REPORTS

표 목록

TABLE 1 NORTH AMERICA LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 2 NORTH AMERICA EQUIPMENT IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 3 NORTH AMERICA AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 4 NORTH AMERICA MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 5 NORTH AMERICA ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 6 NORTH AMERICA ANALYZER IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 7 NORTH AMERICA ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 8 NORTH AMERICA SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 9 NORTH AMERICA SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 10 NORTH AMERICA LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 11 NORTH AMERICA TOTAL LAB AUTOMATION IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 12 NORTH AMERICA MODULAR AUTOMATION IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 13 NORTH AMERICA LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 14 NORTH AMERICA CLINICAL DIAGNOSTICS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 15 NORTH AMERICA DRUG DISCOVERY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 16 NORTH AMERICA GENOMICS SOLUTIONS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 17 NORTH AMERICA PROTEOMIC SOLUTIONS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 18 NORTH AMERICA ANALYTICAL CHEMISTRY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 19 NORTH AMERICA PROTEIN ENGINEERING IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 20 NORTH AMERICA BIO ANALYSIS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 21 NORTH AMERICA SYSTEM BIOLOGY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 22 NORTH AMERICA OTHERS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 23 NORTH AMERICA LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 24 NORTH AMERICA BIOTECHNOLOGY & PHARMACEUTICALS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 25 NORTH AMERICA HOSPITALS & LABORATORIES IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 26 NORTH AMERICA RESEARCH & ACADEMIC INSTITUTES IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 27 NORTH AMERICA OTHERS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 28 NORTH AMERICA LAB AUTOMATION MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 29 NORTH AMERICA LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 30 NORTH AMERICA EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 31 NORTH AMERICA AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 32 NORTH AMERICA MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 33 NORTH AMERICA ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 34 NORTH AMERICA ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 35 NORTH AMERICA SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 36 NORTH AMERICA LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 37 NORTH AMERICA LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 38 NORTH AMERICA LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 39 U.S. LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 40 U.S. EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 41 U.S. AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 42 U.S. MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 43 U.S. ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 44 U.S. ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 45 U.S. SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 46 U.S. LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 47 U.S. LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 48 U.S. LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 49 CANADA LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 50 CANADA EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 51 CANADA AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 52 CANADA MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 53 CANADA ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 54 CANADA ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 55 CANADA SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 56 CANADA LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 57 CANADA LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 58 CANADA LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 59 MEXICO LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 60 MEXICO EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 61 MEXICO AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 62 MEXICO MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 63 MEXICO ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 64 MEXICO ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 65 MEXICO SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 66 MEXICO LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 67 MEXICO LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 68 MEXICO LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

그림 목록

FIGURE 1 NORTH AMERICA LAB AUTOMATION MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA LAB AUTOMATION MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA LAB AUTOMATION MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA LAB AUTOMATION MARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA LAB AUTOMATION MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA LAB AUTOMATION MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA LAB AUTOMATION MARKET: DBMR MARKET POSITION GRID

FIGURE 8 NORTH AMERICA LAB AUTOMATION MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 NORTH AMERICA LAB AUTOMATION MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 NORTH AMERICA LAB AUTOMATION MARKET: SEGMENTATION

FIGURE 11 GROWING EXPENDITURE ON LAB AUTOMATION TOOLS AND EQUIPMENT IS EXPECTED TO DRIVE THE NORTH AMERICA LAB AUTOMATION MARKET GROWTH IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 12 EQUIPMENT SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA LAB AUTOMATION MARKET IN 2022 & 2029

FIGURE 13 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE NORTH AMERICA LAB AUTOMATION MARKET

FIGURE 14 NORTH AMERICA LAB AUTOMATION MARKET: BY PRODUCT TYPE, 2021

FIGURE 15 NORTH AMERICA LAB AUTOMATION MARKET: BY PRODUCT TYPE, 2022-2029 (USD MILLION)

FIGURE 16 NORTH AMERICA LAB AUTOMATION MARKET: BY PRODUCT TYPE, CAGR (2022-2029)

FIGURE 17 NORTH AMERICA LAB AUTOMATION MARKET: BY PRODUCT TYPE, LIFELINE CURVE

FIGURE 18 NORTH AMERICA LAB AUTOMATION MARKET: BY AUTOMATION TYPE, 2021

FIGURE 19 NORTH AMERICA LAB AUTOMATION MARKET: BY AUTOMATION TYPE, 2022-2029 (USD MILLION)

FIGURE 20 NORTH AMERICA LAB AUTOMATION MARKET: BY AUTOMATION TYPE, CAGR (2022-2029)

FIGURE 21 NORTH AMERICA LAB AUTOMATION MARKET: BY AUTOMATION TYPE, LIFELINE CURVE

FIGURE 22 NORTH AMERICA LAB AUTOMATION MARKET: BY APPLICATION, 2021

FIGURE 23 NORTH AMERICA LAB AUTOMATION MARKET: BY APPLICATION, 2022-2029 (USD MILLION)

FIGURE 24 NORTH AMERICA LAB AUTOMATION MARKET: BY APPLICATION, CAGR (2022-2029)

FIGURE 25 NORTH AMERICA LAB AUTOMATION MARKET: BY APPLICATION, LIFELINE CURVE

FIGURE 26 NORTH AMERICA LAB AUTOMATION MARKET: BY END USER, 2021

FIGURE 27 NORTH AMERICA LAB AUTOMATION MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 28 NORTH AMERICA LAB AUTOMATION MARKET: BY END USER, CAGR (2022-2029)

FIGURE 29 NORTH AMERICA LAB AUTOMATION MARKET: BY END USER, LIFELINE CURVE

FIGURE 30 NORTH AMERICA LAB AUTOMATION MARKET: SNAPSHOT (2021)

FIGURE 31 NORTH AMERICA LAB AUTOMATION MARKET: BY COUNTRY (2021)

FIGURE 32 NORTH AMERICA LAB AUTOMATION MARKET: BY COUNTRY (2022 & 2029)

FIGURE 33 NORTH AMERICA LAB AUTOMATION MARKET: BY COUNTRY (2021 & 2029)

FIGURE 34 NORTH AMERICA LAB AUTOMATION MARKET: PRODUCT TYPE (2022-2029)

FIGURE 35 NORTH AMERICA LAB AUTOMATION MARKET: COMPANY SHARE 2021 (%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.