Europe Clinical Laboratory Services Market, By Specialty (Clinical Chemistry Testing, Hematology Testing, Microbiology Testing, Immunology Testing, Drugs Of Abuse Testing, Anatomic Pathology Services, Cytology Testing, Genetic Testing, and Other Esoteric Testing), Technology (Chemiluminescence Immunoassay, Enzyme-Linked Immunosorbent Assay, Mass Spectrometry, Real-Time PCR, DNA Sequencing, Flow Cytometry, and Other Technologies), Provider (Independent & Reference Laboratories, Hospital-Based Laboratories, Clinical Based Laboratories, and Nursing and Physician Office-Based Laboratories), Application (Drug Discovery Related Services and Development Related Services, Bioanalytical & Lab Chemistry Services, Toxicology Testing Services, Cell & Gene Therapy Related Services, Preclinical & Clinical Trial Related Services, and Other Clinical Laboratory Services) - Industry Trends And Forecast to 2030.

Europe Clinical Laboratory Services Market Analysis and Size

The market is expected to gain market. Growing application of high-throughput assays and advancement in clinical diagnostic methods act as a driver for the market growth.

Clinical labs provide testing products to public and private health service agencies, including health centers, clinics, medical centers, and nursing homes. Laboratory research areas protected by accreditation include medicinal chemistry, clinical microbiology, hematology, anatomy, clinical physics, psychology, nuclear medicine, and clinical neurophysiology.

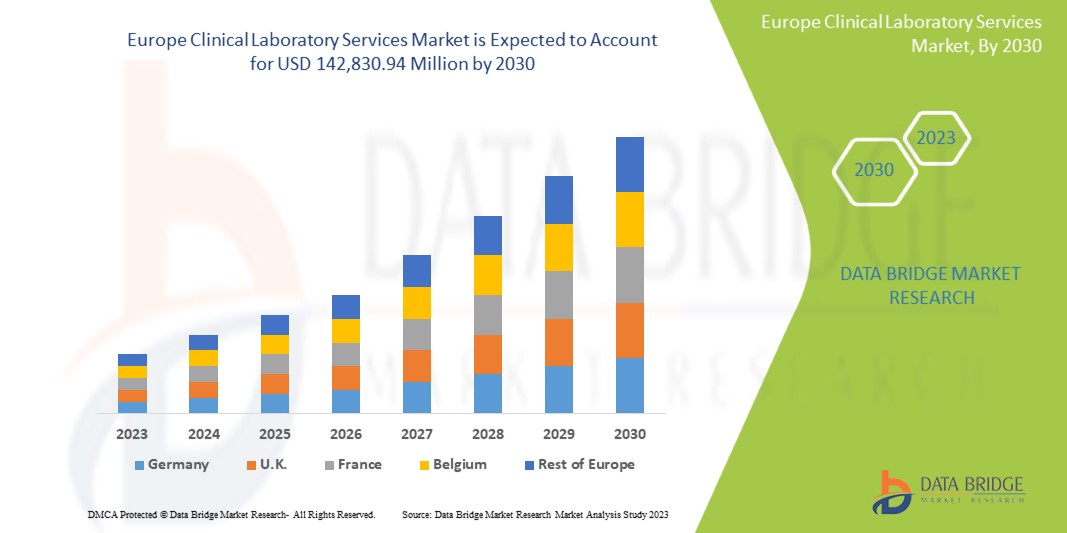

Data Bridge Market Research analyses that the Europe clinical laboratory services market is expected to reach the value of USD 142,830.94 million by 2030, at a CAGR of 6.6% during the forecast period.

|

Report Metric |

Details |

|

Forecast Period |

2023 to 2030 |

|

Base Year |

2022 |

|

Historic Year |

2021 (Customizable to 2015-2020) |

|

Quantitative Units |

Revenue in USD Million |

|

Segments Covered |

Specialty (Clinical Chemistry Testing, Hematology Testing, Microbiology Testing, Immunology Testing, Drugs Of Abuse Testing, Anatomic Pathology Services, Cytology Testing, Genetic Testing, and Other Esoteric Testing), Technology (Chemiluminescence Immunoassay, Enzyme-Linked Immunosorbent Assay, Mass Spectrometry, Real-Time PCR, DNA Sequencing, Flow Cytometry, and Other Technologies), Provider (Independent & Reference Laboratories, Hospital-Based Laboratories, Clinical Based Laboratories, and Nursing and Physician Office-Based Laboratories), Application (Drug Discovery Related Services and Development Related Services, Bioanalytical & Lab Chemistry Services, Toxicology Testing Services, Cell & Gene Therapy Related Services, Preclinical & Clinical Trial Related Services, and Other Clinical Laboratory Services) |

|

Countries Covered |

독일, 프랑스, 영국, 이탈리아, 스페인, 러시아, 터키, 벨기에, 네덜란드, 스위스 및 유럽의 나머지 지역 |

|

시장 참여자 포함 |

Mayo Foundation for Medical Education and Research, Quest Diagnostics Incorporated, Eurofins Scientific, UNILABS, SYNLAB International GmbH, HU Groups Holdings, Inc., Sonic Healthcare Limited, ACM Global Laboratories, Amedes Medical Services GmbH, Abbott, Charles River Laboratories, Cerba Healthcare, Q2 Solutions(IQVIA Inc의 자회사) 등 |

시장 정의

임상 실험실은 의료 분야의 중요한 부분입니다. 혈액 검사에서 유전자 분석에 이르기까지 대부분의 진단 검사는 이러한 임상 실험실에서 다양한 질병을 탐지하기 위해 수행됩니다. 임상 실험실은 진단 및 검사 결과와 같이 의료 시스템에서 필요한 분배를 최적화하는 데이터와 리소스를 제공합니다. 이를 통해 의사가 다양한 수준의 의료 서비스에서 적절한 임상 및 진단 결정을 내릴 수 있도록 하는 신뢰할 수 있고 정확한 검사 결과를 유지하고 제공합니다. 이를 통해 임상의는 의료 실험실 시설이 없다면 방해받을 수 있는 치료를 적응, 시작 및 중단할 수 있습니다. 임상 실험실 서비스에는 약물 발견, 약물 개발, 생물 분석 및 실험실 화학, 독성학 검사, 세포 및 유전자 치료 , 임상 전 및 임상 시험 관련 서비스가 포함됩니다. 독립 및 참조 실험실, 병원 기반 실험실, 간호 및 의사 사무실 기반 실험실은 임상 실험실 서비스의 주요 제공자 중 일부입니다.

시장 동향

이 섹션에서는 시장 동인, 이점, 기회, 제약 및 과제를 이해하는 것을 다룹니다. 이 모든 내용은 아래에서 자세히 설명합니다.

운전사

- 감염병 사례 증가

최근 바이러스성 유행병과 항생제 내성 병원균과 같은 감염성 질환 의 발생률이 증가하면서 진단 검사와 임상 검사 서비스에 대한 수요가 증가했습니다. 바이러스, 기생충, 진균, 박테리아와 같은 유기체에 의해 영향을 받는 감염성 질환은 한 사람에서 다른 사람으로 직접 또는 간접적으로 전파됩니다. 임상 검사실은 이러한 질병을 효과적으로 식별하고 관리하기 위해 분자 진단 및 혈청학 검사를 포함한 고급 진단 기술에 상당한 투자를 하고 있습니다. 감염성 질환의 증가는 환자의 감염성 질환에 대한 실험실 진단으로 임상 검사실에 대한 수요를 증가시킵니다. 임상 검사실은 혈액 검사, 면역학 및 알레르기 검사, 요분석 등을 포함하여 감염성 질환으로 인한 환자의 진단 및 치료를 위한 다양한 유형의 서비스를 제공합니다.

기회

- 디지털 병리학 플랫폼의 인기 상승

디지털 병리학 플랫폼은 유리 현미경 고해상도 슬라이드 스캐닝에서 얻은 디지털 전체 슬라이드 이미지를 보는 데 사용되는 컴퓨터 워크스테이션입니다. 디지털 병리학 플랫폼은 분석 및 진단 보고 알고리즘을 사용하여 연구의 재현성, 더 높은 정확성 및 표준화를 보장합니다. 디지털 병리학 플랫폼의 응용 프로그램은 다양한 임상 실험실에서 실험실에서 본격적인 작업을 성공적으로 구현하기 위해 증가하고 있습니다. 또한 전체 슬라이드 이미징이 스캐너 용량, 스캔 시간, 이미지 해상도, 이미지 관리 소프트웨어, 실험실 정보 시스템 통합 및 간단한 이미지 보기 및 평가에서 다양한 개선을 보임에 따라 디지털 병리학 플랫폼의 채택이 증가했습니다.

디지털 병리학 플랫폼은 팀 커뮤니케이션, 사례 관리, 워크플로우 가속화 및 이미지 분석, 슬라이드 이미징, 종양 보드, 원격 컨설팅에서 유용성을 입증했습니다. 이를 통해 연구자와 임상의에게 보다 협력적이고 효율적이며 보람 있는 환경이 조성되어 전 세계적으로 디지털 병리학 플랫폼 채택이 증가하고 있습니다.

디지털 병리학 플랫폼의 채택은 임상 실험실의 다양한 부서에서 훈련, 교육, 팀 커뮤니케이션, 연구 활동 및 1차 진단 보고를 포함한 기능적 능력이 향상됨에 따라 선진국과 개발도상국에서 증가하고 있습니다. 디지털 병리학 플랫폼은 임상 실험실에서 효능을 보여주었으며 임상 실험실 운영에 많은 이점이 있습니다.

- 예방 건강 검진에 대한 인구의 인식 증가

예방 건강 검진은 질병을 초기에 발견하고 미래에 발생할 수 있는 질병에 대한 노출을 방지하기 위해 수행하는 예방 조치입니다. 검진은 질병을 식별하고 위험 요소를 검사하여 조기에 손실을 제한하는 것으로 구성됩니다. 예방 건강 검진은 혈액 화학, 헤모글로빈, 요분석, 전립선암 검진, 난소암 검진, ECG, 지질 패널 등 다양한 실험실 검사를 통해 수행됩니다.

예방적 건강 검진은 다양한 연구와 조사에서 질병 예방과 경제에 효과가 입증됨에 따라 전 세계적으로 증가하고 있습니다. 또한 예방적 건강 검진에 대한 수요는 다양한 국가의 건강 보험 회사에서 예방적 건강 검진을 보장하고 현재 COVID-19 상황이 개인의 안전을 위해 필요한 것으로 추가됨에 따라 증가했습니다. 전염병이 발병하면 이상적인 대응책은 공중 보건 당국이 조기에 검사를 시작하는 것입니다. 그러면 사례를 신속하게 식별하고 해당 사람들을 신속하게 치료하고 확산을 방지하기 위해 즉시 격리할 수 있습니다. 조기 검사는 감염된 사람과 접촉한 사람을 식별하여 신속하게 치료할 수 있도록 도와줍니다.

제약 /도전

- 숙련되고 인증된 전문가의 부족

숙련되고 인증된 전문가에 대한 요구는 임상 실험실에 큰 제약입니다. 임상 실험실 서비스는 건강을 위해 정기적인 진단 검사가 필요한 65세 이상의 사람들의 수가 크게 증가함에 따라 증가했지만 실험실 센터에 있는 숙련된 전문가의 수는 시장 성장을 제한할 것으로 예상됩니다. 방법과 실험실 절차에는 장점이 있지만 표준화, 평등화 및 지식에 일정한 격차가 있습니다. 기술자는 절차를 효율적으로 수행하기 위해 고급 방법을 안전하게 채택하는 데 있어서 문제와 관련된 기술 교육 격차에 직면해 있습니다. 방법 개발, 검증, 운영 및 문제 해결 활동을 위해 임상 실험실에서 고도로 숙련된 전문가가 필요합니다.

- 부정확한 테스트 결과로 인한 정밀도와 신뢰성 저하

진단 검사 결과의 부정확성은 환자 안전에 부정적인 영향을 미쳐 잠재적으로 환자의 건강을 해치는 잘못된 진단이나 지연된 진단으로 이어질 수 있습니다. 많은 부정확한 결과와 진단 검사 오류는 실험실 관행과 관련이 있습니다. 실험실 관행은 사전 분석, 분석 및 사후 분석의 세 부분으로 나눌 수 있습니다.

분석 오류: 성능 사양에 따라 시험 방법을 수립하고 검증하는 과정에서 정밀도, 정확도, 특이성, 민감도, 선형성을 시험하는 것은 임상 실험실 시험에서 오류가 많은 영역입니다.

사전 분석 오류: 사전 분석 오류 단계는 최대 실험실 오류가 발생하는 프로세스입니다. 사전 분석 오류는 환자 평가, 환자 식별, 요청 완료, 검사 주문 입력, 검체 운송, 검체 수집 및 실험실에서의 검체 수령 중에 발생할 수 있습니다.

분석 후 오류: 분석 후 단계는 진단 및 치료 결정 단계입니다. 분석 후 오류는 실험실 검사 결과의 부적절한 사용, 올바른 결과의 전달 및 중요한 결과 보고로 인해 발생할 수 있으며, 이는 전체 실험실 검사 프로세스의 분석 후 단계에서 잠재적인 오류 영역입니다.

최근 개발 사항

- 2023년 8월, Abbott은 Alinity h-series 혈액학 시스템에 대한 FDA 승인을 받아 완전 혈구 수치(CBC) 검사를 위한 진단 서비스 라인업을 확장했습니다. 이 시스템은 정기 검진에 필수적이며 감염, 빈혈, 면역 체계 질환, 혈액암 과 같은 다양한 질환의 스크리닝을 돕습니다 . Alinity h-series는 자동 혈액학 분석기인 Alinity hq와 통합 슬라이드 메이커 및 염색기인 Alinity hs로 구성되어 있습니다. 특히 Alinity HQ는 광산란을 사용하여 고급 세포 식별을 위한 MAPSSTM 기술을 사용합니다.

- 2022년 11월, Microba Life Sciences는 의료 진단 분야의 글로벌 리더인 Sonic Healthcare Limited와 전략적 파트너십을 발표했습니다. Sonic은 Microba의 지분 19.99%를 인수할 예정이며, 주주 승인이 있을 경우 추가 5%에 대한 옵션이 제공됩니다.

시장 범위

유럽 임상 검사실 서비스 시장은 전문성, 기술, 공급자 및 응용 프로그램을 기준으로 4개의 주요 세그먼트로 분류됩니다. 이러한 세그먼트 간의 성장은 산업의 주요 성장 세그먼트를 분석하고 사용자에게 핵심 시장 응용 프로그램을 식별하기 위한 전략적 결정을 내리는 데 도움이 되는 귀중한 시장 개요와 시장 통찰력을 제공하는 데 도움이 됩니다.

전문

- 임상화학 테스트

- 혈액학 검사

- 미생물학 테스트

- 면역학 테스트

- 약물 남용 테스트

- 세포학 검사

- 유전자 검사

- 해부병리학 서비스

- 기타 Estoric 테스트

전문성을 기준으로 시장은 임상화학 검사, 혈액학 검사, 미생물학 검사, 면역학 검사, 약물남용 검사, 세포학 검사, 유전자 검사, 해부병리 서비스 및 기타 난해한 검사로 구분됩니다.

기술

기술을 기준으로 보면 시장은 효소 결합 면역 흡착 검사법, 실시간 PCR, 화학 발광 면역 검사법, 질량 분석법, 유세포 분석법, DNA 시퀀싱 및 기타 기술로 구분됩니다.

공급자

- 병원 기반 실험실

- 독립 및 참조 실험실

- 간호 및 의사 사무실 기반 실험실

- 임상 기반 실험실

공급자를 기준으로 시장은 병원 기반 실험실, 독립 및 참조 실험실, 간호 및 의사 사무실 기반 실험실, 진료소 기반 실험실로 구분됩니다.

애플리케이션

- 생물분석 및 실험실 화학 서비스

- 약물 발견 및 개발 관련 서비스

- 독성학 테스트 서비스

- 세포 및 유전자 치료 관련 서비스

- 전임상 및 임상 시험 관련 서비스

- 기타 임상 검사 서비스

응용 분야를 기준으로 시장은 약물 발견 및 개발 관련 서비스, 생물분석 및 실험실 화학 서비스, 독성학 검사 서비스, 세포 및 유전자 치료 관련 서비스, 전임상 및 임상 시험 관련 서비스, 기타 임상 실험실 서비스로 구분됩니다.

지역 분석/통찰력

유럽 임상 검사 서비스 시장은 전문성, 기술, 공급업체, 응용 프로그램을 기준으로 4개의 주요 부문으로 분류됩니다.

유럽 임상 검사 서비스 시장 보고서에서 다루는 국가는 독일, 프랑스, 영국, 이탈리아, 스페인, 러시아, 터키, 벨기에, 네덜란드, 스위스 및 기타 유럽 국가입니다.

독일은 선진 의료 인프라와 광범위한 고품질 임상 실험실 네트워크를 갖추고 있어 시장을 주도할 것으로 예상됩니다.

보고서의 국가 섹션은 또한 현재 및 미래 시장 추세에 영향을 미치는 개별 시장 영향 요인과 시장 규제의 변화를 제공합니다. 다운스트림 및 업스트림 가치 사슬 분석, 기술 추세 및 포터의 5가지 힘 분석, 사례 연구와 같은 데이터 포인트는 개별 국가의 시장 시나리오를 예측하는 데 사용되는 몇 가지 포인터입니다. 또한 지역 브랜드의 존재 및 가용성과 지역 및 국내 브랜드와의 대규모 또는 희소한 경쟁으로 인해 직면한 과제, 국내 관세 및 무역 경로의 영향은 국가 데이터 의 예측 분석을 제공하는 동안 고려됩니다 .

경쟁 환경 및 점유율 분석

유럽 임상 검사실 서비스 시장 경쟁 구도는 경쟁자별 세부 정보를 제공합니다. 포함된 세부 정보는 회사 개요, 회사 재무, 창출된 수익, 시장 잠재력, 연구 개발 투자, 새로운 시장 이니셔티브, 지역적 입지, 생산 현장 및 시설, 생산 용량, 회사의 강점과 약점, 제품 출시, 제품 폭과 범위, 응용 프로그램 우세입니다. 위에 제공된 데이터 포인트는 유럽 임상 검사실 서비스 시장에 대한 회사의 초점과만 관련이 있습니다.

유럽 임상 검사 서비스 시장의 주요 기업으로는 Mayo Foundation for Medical Education and Research, Quest Diagnostics Incorporated, Eurofins Scientific, UNILABS, SYNLAB International GmbH, HU Groups Holdings, Inc., Sonic Healthcare Limited, ACM Global Laboratories, Amedes Medical Services GmbH, Abbott, Charles River Laboratories, Cerba Healthcare, Q2 Solutions(IQVIA Inc의 자회사) 등이 있습니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE EUROPE CLINICAL LABORATORY SERVICES MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 MARKET APPLICATION COVERAGE GRID

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTLE ANALYSIS

4.1.1 POLITICAL FACTORS

4.1.2 ECONOMIC FACTORS

4.1.3 SOCIAL FACTORS

4.1.4 TECHNOLOGICAL FACTORS

4.1.5 LEGAL FACTORS

4.1.6 ENVIRONMENTAL FACTORS

4.2 PORTER’S FIVE FORCES

4.2.1 THREAT OF NEW ENTRANTS

4.2.2 THREAT OF SUBSTITUTES

4.2.3 CUSTOMER BARGAINING POWER

4.2.4 SUPPLIER BARGAINING POWER

4.2.5 INTERNAL COMPETITION (RIVALRY)

5 REGULATORY FRAMEWORK

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 RISE IN THE CASES OF INFECTIOUS DISEASES

6.1.2 TECHNOLOGICAL ADVANCEMENTS IN THE CLINICAL DIAGNOSTIC METHODS

6.1.3 DEVELOPMENT IN DATABASE MANAGEMENT TOOLS AND WIDE ACCEPTANCE OF POINT-OF-CARE (POC) TESTING SOLUTIONS

6.1.4 RISE IN DEMAND FOR EARLY AND ACCURATE DISEASE DIAGNOSIS

6.2 RESTRAINTS

6.2.1 LACK OF SKILLED AND CERTIFIED PROFESSIONALS

6.2.2 STRICT REGULATORY POLICIES

6.3 OPPORTUNITIES

6.3.1 RISING POPULARITY OF DIGITAL PATHOLOGY PLATFORMS

6.3.2 GROWTH IN AWARENESS AMONG POPULATION FOR PREVENTIVE HEALTH CHECK-UPS

6.4 CHALLENGE

6.4.1 INACCURATE TEST OUTCOMES UNDERMINING PRECISION AND RELIABILITY

7 EUROPE

8 EUROPE CLINICAL LABORATORY SERVICES MARKET: COMPANY LANDSCAPE

8.1 COMPANY SHARE ANALYSIS: EUROPE

9 SWOT ANALYSIS

10 COMPANY PROFILES

10.1 ABBOTT

10.1.1 COMPANY SNAPSHOT

10.1.2 REVENUE ANALYSIS

10.1.3 SERVICE PORTFOLIO

10.1.4 RECENT DEVELOPMENTS

10.2 SONIC HEALTHCARE LIMITED

10.2.1 COMPANY SNAPSHOT

10.2.2 REVENUE ANALYSIS

10.2.3 SERVICE PORTFOLIO

10.2.4 RECENT DEVELOPMENT

10.3 SYNLAB INTERNATIONAL GMBH

10.3.1 COMPANY SNAPSHOT

10.3.2 REVENUE ANALYSIS

10.3.3 SERVICE PORTFOLIO

10.3.4 RECENT DEVELOPMENTS

10.4 QUEST DIAGNOSTICS INCORPORATED

10.4.1 COMPANY SNAPSHOT

10.4.2 REVENUE ANALYSIS

10.4.3 SERVICE PORTFOLIO

10.4.4 RECENT DEVELOPMENT

10.5 SIEMENS HEALTHINEERS AG

10.5.1 COMPANY SNAPSHOT

10.5.2 REVENUE ANALYSIS

10.5.3 SERVICE PORTFOLIO

10.5.4 RECENT DEVELOPMENTS

10.6 ACM GLOBAL LABORATORIES

10.6.1 COMPANY SNAPSHOT

10.6.2 SERVICE PORTFOLIO

10.6.3 RECENT DEVELOPMENT

10.7 AMEDES MEDICAL SERVICES GMBH

10.7.1 COMPANY SNAPSHOT

10.7.2 SERVICE PORTFOLIO

10.7.3 RECENT DEVELOPMENT

10.8 CERBA HEALTHCARE

10.8.1 COMPANY SNAPSHOT

10.8.2 SERVICE PORTFOLIO

10.8.3 RECENT DEVELOPMENT

10.9 CHARLES RIVER LABORATORIES

10.9.1 COMPANY SNAPSHOT

10.9.2 REVENUE ANALYSIS

10.9.3 SERVICE PORTFOLIO

10.9.4 RECENT DEVELOPMENT

10.1 EUROFINS SCIENTIFIC

10.10.1 COMPANY SNAPSHOT

10.10.2 REVENUE ANALYSIS

10.10.3 SERVICE PORTFOLIO

10.10.4 RECENT DEVELOPMENT

10.11 EXACT SCIENCES CORPORATION

10.11.1 COMPANY SNAPSHOT

10.11.2 REVENUE ANALYSIS

10.11.3 SERVICE PORTFOLIO

10.11.4 RECENT DEVELOPMENT

10.12 H.U. GROUP HOLDINGS, INC.

10.12.1 COMPANY SNAPSHOT

10.12.2 REVENUE ANALYSIS

10.12.3 SERVICE PORTFOLIO

10.12.4 RECENT DEVELOPMENT

10.13 MAYO FOUNDATION FOR MEDICAL EDUCATION AND RESEARCH

10.13.1 COMPANY SNAPSHOT

10.13.2 SERVICE PORTFOLIO

10.13.3 RECENT DEVELOPMENT

10.15 Q2 SOLUTIONS (A SUBSIDIARY OF IQVIA INC)

10.15.1 COMPANY SNAPSHOT

10.15.2 SERVICE PORTFOLIO

10.15.3 RECENT DEVELOPMENTS

10.16 UNILABS

10.16.1 COMPANY SNAPSHOT

10.16.2 SERVICE PORTFOLIO

10.16.3 RECENT DEVELOPMENTS

11 QUESTIONNAIRE

12 RELATED REPORTS

그림 목록

FIGURE 1 EUROPE CLINICAL LABORATORY SERVICES MARKET: SEGMENTATION

FIGURE 2 EUROPE CLINICAL LABORATORY SERVICES MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE CLINICAL LABORATORY SERVICES MARKET: DROC ANALYSIS

FIGURE 4 EUROPE CLINICAL LABORATORY SERVICES MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE CLINICAL LABORATORY SERVICES MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE CLINICAL LABORATORY SERVICES MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE CLINICAL LABORATORY SERVICES MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE CLINICAL LABORATORY SERVICES MARKET APPLICATION COVERAGE GRID

FIGURE 9 EUROPE CLINICAL LABORATORY SERVICES MARKET: SEGMENTATION

FIGURE 10 RISING INFECTIOUS DISEASES WORLDWIDE AND RISING DEMAND FOR EARLY AND ACCURATE DISEASE DIAGNOSIS ARE EXPECTED TO DRIVE THE EUROPE CLINICAL LABORATORY SERVICES MARKET IN THE FORECAST PERIOD OF 2023 TO 2030

FIGURE 11 THE ROUTINE TESTING SERVICES SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE CLINICAL LABORATORY SERVICES MARKET IN 2023 & 2030

FIGURE 12 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE EUROPE CLINICAL LABORATORY SERVICES MARKET

FIGURE 13 EUROPE CLINICAL LABORATORY SERVICES MARKET: SNAPSHOT (2022)

FIGURE 14 EUROPE CLINICAL LABORATORY SERVICES MARKET: COMPANY SHARE 2022 (%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.