Global Ear Nasal Packing Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

257.26 Million

USD

410.03 Million

2024

2032

USD

257.26 Million

USD

410.03 Million

2024

2032

| 2025 –2032 | |

| USD 257.26 Million | |

| USD 410.03 Million | |

| % | |

|

Global Ear and Nasal Packing Market Segmentation, By Type (Nasal packingand Ear packing), Material (Bio Absorbable and Non-Absorbable), Distribution Channel (Direct Tender and OTC), End User (Hospitals, Clinics, Ambulatory Centres, and Others) - Industry Trends and Forecast to 2032

Ear and Nasal Packing Market Size

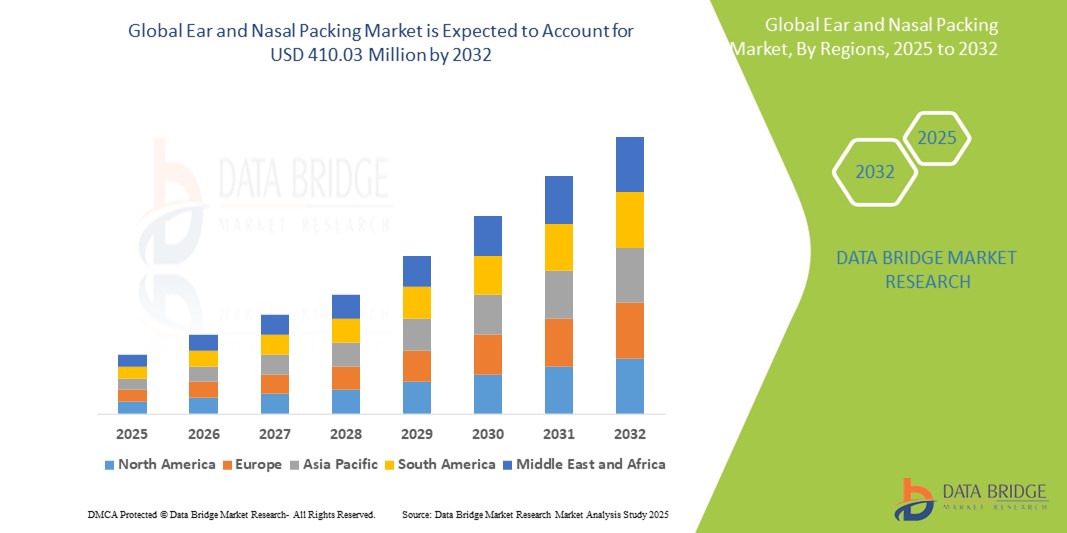

- The global ear and nasal packing market size was valued atUSD 257.26 million in 2024and is expected to reachUSD 410.03 million by 2032, at aCAGR of 6.00%during the forecast period

- This growth is driven by factors such as the rising prevalence of ENT disorders, increasing adoption of minimally invasive surgeries, and advancements in bioresorbable nasal and ear packing materials

Ear and Nasal Packing Market Analysis

- Ear and nasal packing products are used in medical procedures to control bleeding, support tissue healing, and stabilize nasal and ear structures during and after surgeries

- The demand for these packing materials is primarily driven by the rising incidence of ENT disorders, increased preference for minimally invasive surgeries, and technological advancements in packing materials

- North America is expected to dominate the ear and nasal packings market with a market share of 38.5%, due to high prevalence of ent disorders, increasing number of ENT surgeries, and widespread adoption of advanced packing materials such as bioresorbable and drug-eluting types

- Asia-Pacific is expected to be the fastest growing region in the ear and nasal packing market with a market share of 22.5%, during the forecast period due to rapid healthcare infrastructure development, increasing ENT surgical volumes, and growing awareness about modern treatment solutions

- Non-Absorbable segment is expected to dominate the market with a market share of 55.2% due to its durability and long-lasting performance. Non-absorbable packing materials are preferred in cases where long-term support and stability are required, particularly in more complex surgeries.

Report Scope and Ear and Nasal Packing Market Segmentation

|

Attributes |

Ear and Nasal Packing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ear and Nasal Packing Market Trends

“Advancements in Bioresorbable Materials & Minimally Invasive Technique”

- A prominent trend in the ear and nasal packing market is the increasing adoption of bioresorbable materials, which eliminate the need for removal after use, enhancing patient comfort and reducing recovery time

- These materials are designed to gradually dissolve in the body, offering both effective support and reduced complications associated with traditional non-absorbable packing

- For instance, bioresorbable nasal packs are gaining popularity in surgeries such as septoplasty and rhinoplasty due to their ability to minimize the risk of infection and promote faster healing

- This trend is driving the demand for advanced packing solutions that align with the shift towards minimally invasive ENT procedures, improving surgical outcomes and reducing post-operative care requirements

Ear and Nasal Packing Market Dynamics

Driver

“Increasing Incidence of ENT Disorders and Surgical Interventions”

- The rising prevalence of ENT (ear, nose, and throat) disorders such as chronicsinusitis, epistaxis(nosebleeds),nasal polyps, and otitis media is significantly driving the demand for ear and nasal packing products

- With growing environmental pollution, allergen exposure, and lifestyle changes, more individuals are developing ENT conditions that often require surgical treatment and post-operative care involving packing materials

- The demand is further boosted by the increasing number of ENT procedures, both in hospitals andambulatory surgical centers, requiring effective bleeding control and structural support

For instance,

- According to the World Health Organization (WHO), an estimated 430 million people worldwide require treatment for disabling hearing loss, while millions undergo sinus and nasal surgeries annually, creating a sustained need for high-performance packing solutions

- As the burden of ENT diseases continues to rise globally, the market for effective, patient-friendly ear and nasal packing solutions is expected to grow steadily

Opportunity

“Innovation in Bioresorbable and Drug-Eluting Packing Materials”

- Technological advancements in the development of bioresorbable and drug-eluting ear and nasal packing materials are creating significant growth opportunities in the market. These materials not only provide structural support but also dissolve naturally, reducing the need for painful removal and improving patient comfort

- Drug-eluting packs can deliver localized therapies—such as antibiotics or anti-inflammatory agents—directly to surgical sites, which helps reduce post-operative infections, inflammation, and healing time

- The combination of controlled drug release and patient-friendly material design is gaining traction among healthcare providers seeking safer and more effective post-operative solutions

For instance,

- In 2024 study published in the International Journal of Otolaryngology highlighted that drug-eluting nasal packs significantly reduced post-operative pain and infection rates in sinus surgery patients, improving overall clinical outcomes and satisfaction

- These innovations are transforming post-surgical care in ENT procedures, presenting an opportunity for manufacturers to develop differentiated, value-added products that cater to the growing demand for advanced and minimally invasive ENT treatments

Restraint/Challenge

“Limited Accessibility and High Cost of Advanced Packing Materials”

- The high cost of advanced ear and nasal packing materials, especially bioresorbable and drug-eluting types, presents a significant challenge to widespread adoption, particularly in low- and middle-income countries

- These premium products are often priced significantly higher than conventional non-absorbable options, making them less accessible to smaller healthcare facilities and clinics with constrained budgets

- The cost factor not only limits market penetration but also leads to continued reliance on older, less effective packing materials, which may cause discomfort or require manual removal

For instance,

- According to a 2023 report by Allied Market Research, healthcare providers in cost-sensitive markets often prefer traditional, affordable packing products, citing financial constraints and limited insurance coverage for newer technologies as major barriers to adoption

- Consequently, despite their clinical benefits, the use of innovative packing solutions remains restricted, which may hinder the overall advancement of ENT post-surgical care and restrain market growth

Ear and Nasal Packing Market Scope

The market is segmented on the basis of type, material, distribution channel, and end user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material |

|

|

By Distribution Channel |

|

|

By End User

|

|

In 2025, the non-absorbable is projected to dominate the market with a largest share in material segment

The non-absorbable segment is expected to dominate the ear and nasal packing market with the largest share of 55.2% in 2024 due to its durability and long-lasting performance. Non-absorbable packing materials are preferred in cases where long-term support and stability are required, particularly in more complex surgeries. In addition, these materials are highly effective in controlling bleeding and maintaining structural integrity during the healing process, making them a favored choice for many surgical procedures

The nasal packing is expected to account for the largest share during the forecast period in type market

In 2025, the nasal packing segment is expected to dominate the market with the largest market share of 65.5% due to its critical role in managing post-operative bleeding and stabilizing nasal structures after surgeries such as septoplasty and rhinoplasty. The growing preference for advanced, bioresorbable nasal packing materials, which minimize discomfort and reduce the need for removal, is also driving this segment’s growth. In addition, the increasing number of nasal surgeries globally contributes to the segment's dominant position.

Ear and Nasal Packing Market Regional Analysis

“North America Holds the Largest Share in the Ear and Nasal Packing Market”

- North America dominates the ear and nasal packing market with a market share of estimated 38.5%, driven, by a high prevalence of ENT disorders, increasing number of ENT surgeries, and widespread adoption of advanced packing materials such as bioresorbable and drug-eluting types

- U.S. holds a market share of 43.6%, due to robust healthcare infrastructure, strong presence of leading medical device manufacturers, and well-established reimbursement systems

- In addition, a growing geriatric population prone to ENT conditions and strong government initiatives aimed at improving healthcare delivery continue to bolster market growth in the region

- High awareness among healthcare professionals and patients about minimally invasive procedures and post-operative care further accelerates the adoption of premium packing solutions

“Asia-Pacific is Projected to Register the Highest CAGR in the Ear and Nasal Packing Market”

- Asia-Pacific is expected to witness the highest growth rate in the Ear and Nasal Packing market with a market share of 22.5%, driven by rapid healthcare infrastructure development, increasing ENT surgical volumes, and growing awareness about modern treatment solutions

- Countries such as China, India, and South Korea are emerging as major contributors due to rising pollution levels, increasing allergic rhinitis and sinusitis cases, and expanding access to healthcare facilities

- As healthcare spending rises and more ENT procedures are performed in both urban and rural settings, the demand for effective and patient-friendly packing materials is expected to grow significantly across the region

- India is expected to register the highest CAGR, supported by a large patient base, increasing ENT surgeon availability, and growing investments in medical device innovation and accessibility

Ear and Nasal Packing Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- BD(U.S.)

- Medtronic(Ireland)

- Stryker(U.S.)

- Smith+Nephew(U.K.)

- Olympus Corporation(Japan)

- Richard Wolf GmbH (Germany)

- MED-EL Medical Electronics (Austria)

- Sonova (Switzerland)

- FUJIFILM Corporation (Japan)

- ZHEJIANG NUROTRON BIOTECHNOLOGY CO., LTD. (China)

- DCC plc (Ireland)

- Danaher (U.S.)

- Summit Health (U.S.)

- Network Medical Products Ltd. (U.S.)

- Boston Scientific Corporation (U.S.)

- AptarGroup, Inc. (U.S.)

- L&R Group (Germany)

- Aegis Lifesciences (India)

- Meril Life Sciences Pvt Ltd. (India)

Latest Developments in Global Ear and Nasal Packing Market

- In October 2024, Aptar Pharma acquired SipNose Nasal Delivery Systems' device technology assets, strengthening its position in the intranasal drug delivery market. SipNose’s devices, designed for targeted delivery within the nasal cavity, will enhance Aptar Pharma's patent portfolio and aid in developing new drug delivery products

- In September 2024, Phillips Medisize, a Molex subsidiary, announced its agreement to acquire Vectura Group, a UK-based CDMO specializing in inhalation drug delivery devices. Vectura's expertise includes the development of dry powder inhalers and metered dose inhalers, enhancing Phillips Medisize’s capabilities in inhalation drug delivery

- In April 2024, Aptar Pharma announced plans to expand its manufacturing facility in Congers, New York, with completion expected by the end of 2024. The expansion will enhance the production of Unidose nasal spray systems by adding moulds and assembly lines in cleanroom environments. The facility is set to be operational by 2025

- In March 2024, Enzymatica’s mouth spray ColdZyme secured CE-certification of Class III from Eurofins, a European-approved notified body for medical devices. The new EU medical device regulation (MDR) aims to improve patient safety by introducing more stringent methods of assessment and market surveillance. However, it has been questioned if the extensive technical documentation requirements of the MDR are suppressing opportunities for early device development

- In June 2024- CHAMPS Group Purchasing (GPO) will distribute the exclusive nosebleed devices developed by CoagCo LLC. CHAMPS GPO will incorporate the Coag it NP7 device within its member contracts

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.