北米の膀胱疾患市場

Market Size in USD Billion

CAGR :

%

USD

4,332.44 Million

USD

10,554.59 Million

2021

2029

USD

4,332.44 Million

USD

10,554.59 Million

2021

2029

| 2022 –2029 | |

| USD 4,332.44 Million | |

| USD 10,554.59 Million | |

| % | |

北米の膀胱障害市場、タイプ別(膀胱炎、尿失禁、過活動膀胱、間質性膀胱炎、膀胱がん)、治療タイプ別(手術、薬物療法、非手術)、エンドユーザー別(病院、診療所、外来手術センター、その他)、流通チャネル別(直接、小売) - 2029年までの業界動向と予測。

北米の膀胱疾患市場の分析と洞察

膀胱障害は、人間の日常生活に影響を及ぼす可能性のある障害のグループです。最も一般的な膀胱障害には、膀胱炎(膀胱が感染して炎症を起こす)、尿失禁(膀胱をコントロールできなくなる)、間質性膀胱炎(膀胱の痛みと頻尿、切迫した排尿)、過活動膀胱(膀胱が尿を絞り出す状態)などがあります。膀胱障害は生活の質に影響を及ぼし、その他の健康上の問題を引き起こす可能性があります。神経系や生活習慣の要因を含む健康の変化や問題は、男性と女性の UI の原因または一因となる可能性があります。

最も一般的な膀胱障害は、過活動膀胱と UI です。これらの問題は神経系に関連しています。神経は脳から膀胱に筋肉の収縮または弛緩を指示するメッセージを伝えます。

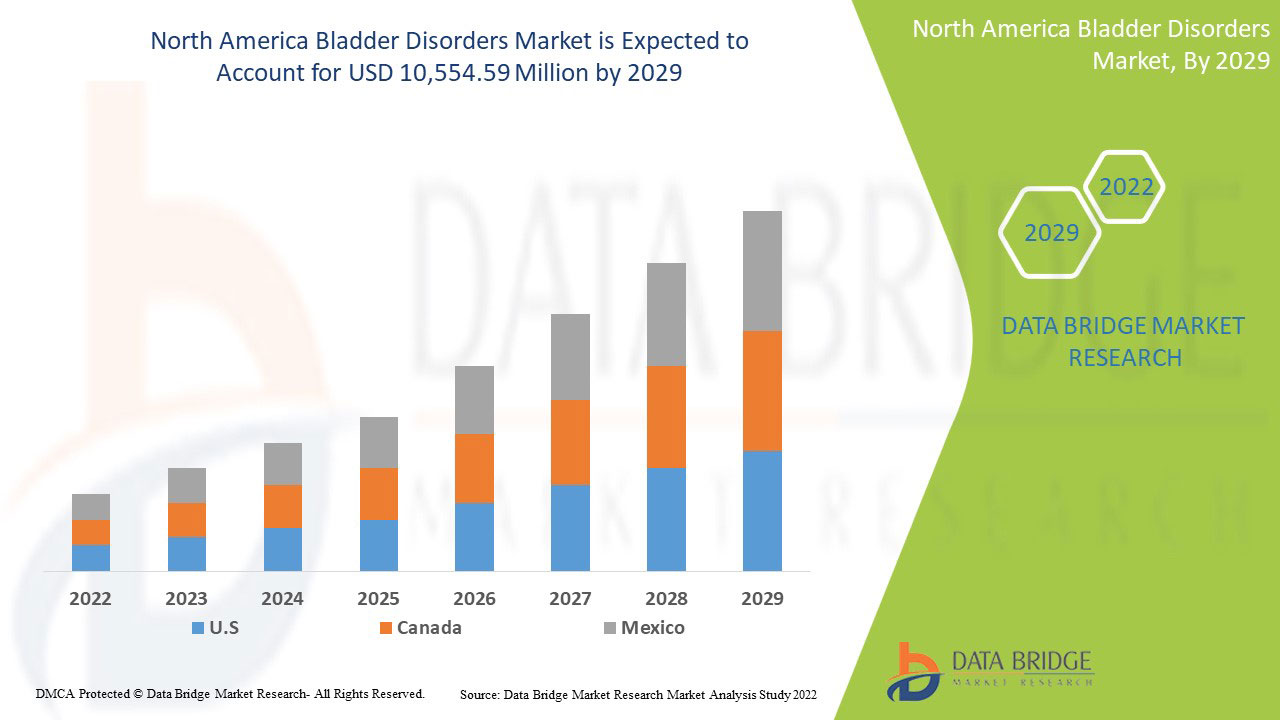

北米の膀胱障害市場は、2022年から2029年の予測期間に成長すると予想されています。データブリッジマーケットリサーチは、市場は2022年から2029年の予測期間に11.8%のCAGRで成長し、2021年の43億3,244万米ドルから2029年には105億5,459万米ドルに達すると分析しています。

|

レポートメトリック |

詳細 |

|

予測期間 |

2022年から2029年 |

|

基準年 |

2021 |

|

歴史的な年 |

2020 (カスタマイズ可能 2019-2014) |

|

定量単位 |

収益(百万米ドル) |

|

対象セグメント |

タイプ別(膀胱炎、尿失禁、過活動膀胱、間質性膀胱炎、膀胱がん)、治療タイプ別(外科手術、薬物療法、非外科的治療)、エンドユーザー別(病院、診療所、外来手術センター、その他)、流通チャネル別(直接、小売) |

|

対象国 |

米国、カナダ、メキシコ |

|

対象となる市場プレーヤー |

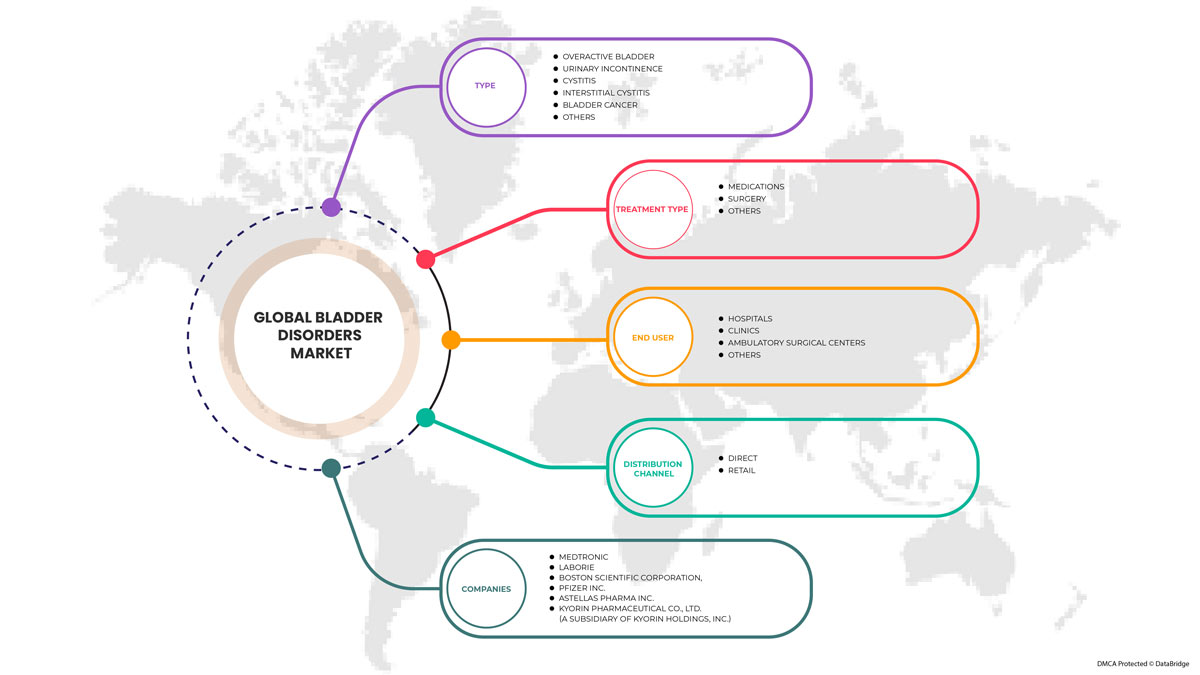

この市場で取引している主な企業としては、メドトロニック、ラボリー、ボストン・サイエンティフィック・コーポレーション、ファイザー株式会社、アステラス製薬株式会社、杏林製薬株式会社(杏林製薬ホールディングス株式会社の子会社)、ブリストル・マイヤーズ スクイブ社、ジョンソン・エンド・ジョンソン・サービスの子会社、アクソニクス社、メルク社、ビアトリス社、ブルー・ウィンド・メディカル、バレンシア・テクノロジーズ、ゲイロード・ケミカル・カンパニー、コロプラスト社、アッヴィ社、サン・ファーマシューティカル・インダストリーズ社、ザイダス・グループ、ウロバント・サイエンシズなどがあります。 |

北米膀胱疾患市場の市場定義

膀胱関連の疾患には、膀胱炎(多くの場合は感染症による膀胱の炎症)、尿失禁(膀胱のコントロールの喪失)、過活動膀胱(膀胱が不適切なタイミングで尿を排出する状態)、間質性膀胱炎(膀胱の痛み、頻尿、尿意切迫感、膀胱がんを引き起こす慢性の問題)などがあります。

膀胱障害を診断するために、医師はレントゲン、尿検査、膀胱鏡と呼ばれるスコープによる膀胱壁検査など、さまざまな検査を行います。障害の治療は問題の原因によって異なり、薬物療法、手術(重症の場合)、非外科的処置が含まれます。

抗コリン薬は、過活動膀胱(OAB)症候群の薬物療法の第一選択薬です。OAB は、我慢できないほどの尿意切迫感を特徴とする臨床症状で、一般的に 1 日 8 回以上の排尿頻度は OAB とみなされます。抗コリン薬は、膀胱の収縮力を低下させる排尿筋のムスカリン受容体を阻害します。副作用を軽減するために、膀胱選択性が向上した新しい薬や徐放性製剤が開発されています。最近の薬のほとんどは、過活動膀胱の症状を軽減するのに同等の効果があります。

北米の膀胱疾患市場の動向

ドライバー

-

市場参加者が採用した戦略的取り組み

膀胱障害は、日常の身体活動に影響を及ぼす可能性のあるさまざまな膀胱の問題です。最も一般的な膀胱障害は、膀胱炎、間質性膀胱炎、過活動膀胱、尿失禁、膀胱がんなどです。膀胱の問題のほとんどは、尿路に入り込んだ細菌感染によって引き起こされます。

市場プレーヤーによるコラボレーション、買収、パートナーシップなどのさまざまな戦略的取り組みにより、自社の製品ポートフォリオを拡大し、市場を拡大して顧客間の製品需要を高めることができ、最終的に市場プレーヤーは最大の収益を得ることができます。

-

高齢化人口の増加

加齢は、膀胱関連障害に関連する可能性のある強力なリスク要因です。加齢は、膀胱機能の神経学的、解剖学的、生化学的変化を促し、OAB の発症につながる可能性があります。過活動膀胱は、高齢者の間で最も一般的な問題です。高齢者は、膀胱に関連するさまざまな問題や障害に悩まされており、そのため、慢性的な健康管理サービスやソリューションの主なユーザーとなっています。

According to the noble study, the prevalence rate of overactive bladder is approximately 16.9 in women and men, around 16.0%, and the prevalence of OAB is growing with age. However, treatment guidelines specify the preferred first-, second-, and third-line OAB therapy strategies. Bladder disorders are associated with the Neurologic disorders such as dementia and in this age group OAB is very challenging for the senior population. Over the last few decades, the old age population has been drastically growing worldwide.

-

RISING R&D INVESTMENTS AND LAUNCH OF NOVEL THERAPIES IN UPCOMING YEARS

Various treatment options and innovative therapies are available for OAB and other bladder disorders. Many biopharmaceutical and pharmaceutical companies are investing in various unconventional therapies for bladder disorders, which are expected to launch during the forecast period.

-

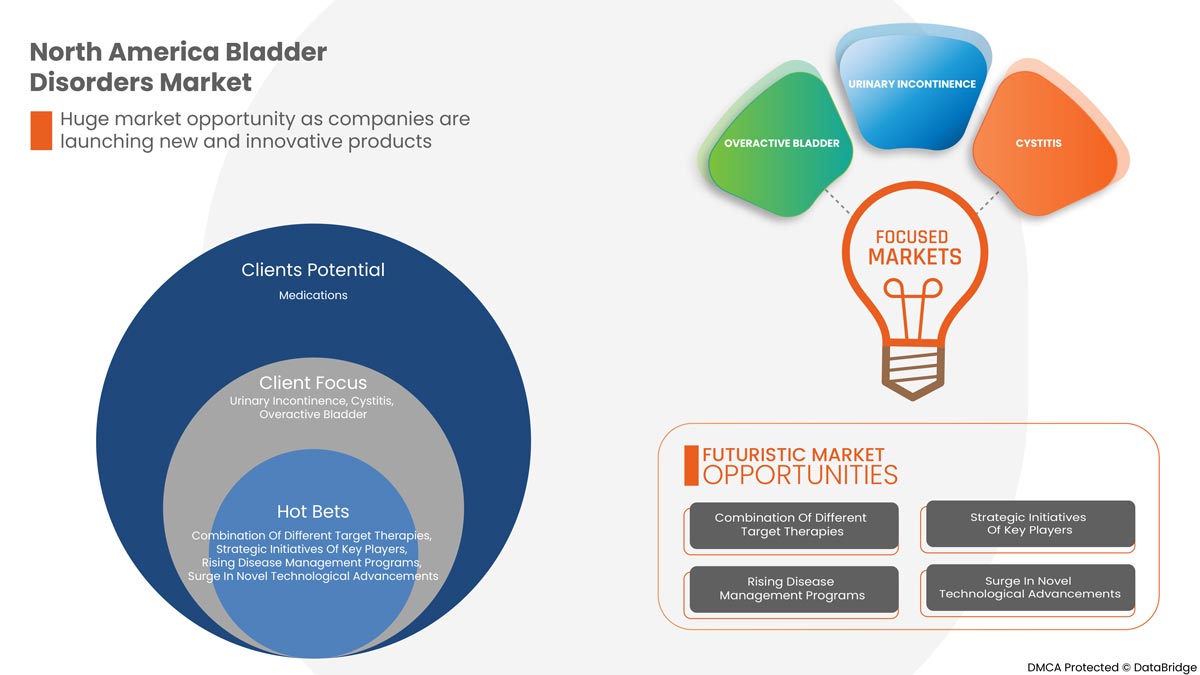

COMBINATION OF DIFFERENT TARGET THERAPIES

Combination Therapies are much more effective than monotherapy, without additional side effects. Combination Therapies are a safe and effective alternative for individuals with refractory bladder conditions. Combining different target therapy strategies is the best approach to relieve patients of bladder disorders. Oral medication and behavioral therapy should be considered for the patients' refractory treatment. Various advanced target therapies are available such as sacral neuromodulation, intradetrusor injection of a botulinum toxin A and percutaneous tibial nerve stimulation. These are advanced treatments and more effective as compared to oral agents.

Opportunities

-

SURGE IN NOVEL TECHNOLOGICAL ADVANCEMENTS

Chronic diseases are considered one of the major leading causes of death in developing countries worldwide. Therefore, the importance of healthcare management of chronic management is increased among public health practitioners.

Bladder disorder management now emphasizes assisting patients with various alternatives for self-care and a range of consultation services to educate patients about their illness state and move forward. These therapies also assist patients in getting over emotional trauma and anxiety, which may act as a counter-protective mechanism.

Rising technical breakthroughs allow healthcare organizations to explore innovative services and solutions for managing chronic bladder disorders. Since they are not required to stay in the hospital for an extended period of time, they have also decreased costs and patient volume. Furthermore, lowering hospital visits and remains makes this development convenient for older adults. Considering the favorable aspects, many organizations and businesses are developing and implementing the most recent technologies in managing chronic diseases to enhance patient outcomes.

-

RISING DISEASE MANAGEMENT PROGRAMS

People with bladder-related problems typically need more medical services, such as hospital stays, doctor visits, and prescription medications. Rise in the number of people living longer with many chronic problems coupled with increasing healthcare expenditures has encouraged better healthcare plans.

Disease management is one strategy that tries to improve care while lowering the expense of caring for the chronically ill. Programs for managing diseases aim to enhance the health of people with certain chronic disorders such as bladder disorders while lowering the demand for medical services and associated expenses for consequences that can be avoided, such as hospital stays and emergency visits. These programs also include information regarding chronic disease management services and solutions. These are becoming very popular owing to the rising prevalence of chronic diseases worldwide. Government and healthcare organizations have organized and implemented these chronic diseases with multiple disease management programs such as bladder cancer, interstitial cystitis, and overactive bladder management programs. Since disease management programs can significantly improve self-care practices and reduce hospital visits and staying periods to a more excellent extent, they receive more attention among people.

Restraints/Challenges

However, the difficulty in diagnosing the disease and the cost of the treatments and diagnostics are high due to the procedure of various checkpoints along with the high-tech technologies and modalities to perform the procedures. The cost of the procedure generally gets elevated because of the high price of the advanced technological devices used in the treatment, which is expected to restrain the market growth.

This North America bladder disorders market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, the impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on the North America bladder disorders market, contact Data Bridge Market Research for an Analyst Brief. Our team will help you make an informed market decision to achieve market growth.

Post COVID-19 Impact on North America Bladder Disorders Market

COVID-19 has positively affected the market. Lockdowns and isolation during pandemics complicate disease management and medication adherence. Hence the use of various treatment drugs has widely increased in the world's population. Hence, the pandemic has effected positively on this market

Recent Development

- In June 2022, Valencia Technologies Corporation announced the implantable neuromodulation technology product eCoin®, which is reshaping the delivery of long-term therapy for bladder control, is a tibial implant for Urge Urinary Incontinence (UUI). eCoin® received premarket approval (PMA) from the U.S. Food and Drug Administration (FDA) in March 2022, making it the first and only FDA-approved implantable tibial neurostimulator indicated for the treatment of urge urinary incontinence (UUI). This new product has helped the company to increase its portfolio.

North America Bladder Disorders Market Scope

North America bladder disorders market is segmented into type, treatment type, end user, and distribution channel. The growth amongst these segments will help you analyze meager growth segments in the industries and provide the users with a valuable market overview and market insights to make strategic decisions to identify core market applications.

Type

- Cystitis

- Urinary Incontinence

- Overactive Bladder

- Interstitial Cystitis

- Bladder Cancer

On the basis of type, the North America bladder disorders market is segmented into cystitis, urinary incontinence, overactive bladder, interstitial cystitis, bladder cancer.

Treatment type

- Surgery

- Medications

- Others

On the basis of product, the North America bladder disorders market is segmented into surgery, medication, and others.

End User

- Hospital

- Clinics

- Ambulatory Surgery centers

- Others

On the basis of end users, the North America bladder disorders market is segmented into hospitals, clinics, ambulatory surgery centers, and others.

Distribution Channel

- Direct

- Retail

On the basis of distribution channel, the North America bladder disorders market is segmented into direct and retail.

North America Bladder Disorders Market Regional Analysis/Insights

North America bladder disorders market is analyzed, and market size insights and trends are provided by country, type, treatment type, end user, and distribution channel as referenced above.

Countries covered in this market are U.S., Canada, Mexico. U.S. dominates the North America bladder disorders market in terms of market share and revenue and will continue to flourish its dominance during the forecast period. This is due to the high prevalence of overactive bladder disorder in the region, and growing R&D investments and the launch of novel therapies are boosting the market

レポートの国別セクションでは、市場の現在および将来の傾向に影響を与える個々の市場影響要因と市場規制の変更も提供しています。新規および交換販売、国の人口統計、疾病疫学、輸出入関税などのデータポイントは、個々の国の市場シナリオを予測するために使用される主要な指標の一部です。さらに、国別データの予測分析を提供する際には、北米ブランドの存在と入手可能性、地元および国内ブランドとの激しい競争により直面する課題、販売チャネルの影響が考慮されています。

競争環境と北米の膀胱疾患市場シェア分析

北米の膀胱障害市場の競争状況は、競合他社に関する詳細を提供します。詳細には、会社概要、会社の財務状況、収益、市場の可能性、研究開発への投資、新しい市場への取り組み、北米でのプレゼンス、生産拠点と施設、生産能力、会社の強みと弱み、製品の発売、製品の幅と広さ、アプリケーションの優位性が含まれます。上記のデータ ポイントは、北米の膀胱障害市場への会社の重点にのみ関連しています。

北米の膀胱疾患市場で活動している主要企業としては、メドトロニック、ラボリー、ボストン・サイエンティフィック・コーポレーション、ファイザー社、アステラス製薬、杏林製薬株式会社(杏林製薬ホールディングス株式会社の子会社)、ブリストル・マイヤーズ スクイブ社、ジョンソン・エンド・ジョンソン・サービシズ社、アクソニクス社、メルク社、ビアトリス社、ブルー・ウィンド・メディカル、バレンシア・テクノロジーズ、ゲイロード・ケミカル・カンパニー、コロプラスト社、アッヴィ社、サン・ファーマシューティカル・インダストリーズ社、ザイダス・グループ、スワティ・スペントース、ウロバント・サイエンシズなどが挙げられます。

研究方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。市場データは、市場統計モデルとコヒーレント モデルを使用して分析および推定されます。さらに、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数の市場への影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、企業市場シェア分析、測定基準、NA 対地域、ベンダー シェア分析が含まれます。さらに質問がある場合は、アナリストへの電話をリクエストしてください。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

目次

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF NORTH AMERICA BLADDER DISORDERS MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 TYPE LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.2 PORTER'S FIVE FORCES

4.3 NORTH AMERICA BLADDER DISORDERS MARKET, PIPELINE ANALYSIS

5 NORTH AMERICA BLADDER DISORDER MARKET: REGULATIONS

5.1 THE U.S. REGULATORY FRAMEWORK FOR BLADDER DISOREDER MEDICATION

5.2 EUROPE REGULATORY FRAMEWORK FOR BLADDER DISORDER DRUGS

5.3 JAPAN REGULATORY GUIDANCE ON BLADDER DISORDER DRUGS

6 NORTH AMERICA BLADDER DISORDERS MARKET OVERVIEW

6.1 DRIVERS

6.1.1 STRATEGIC INITIATIVES ADOPTED BY MARKET PLAYERS

6.1.2 GROWING GERIATRIC POPULATION

6.1.3 RISING R&D INVESTMENTS AND LAUNCH OF NOVEL THERAPIES IN UPCOMING YEARS

6.1.4 COMBINATION OF DIFFERENT TARGET THERAPIES

6.2 RESTRAINTS

6.2.1 HIGH COST ASSOCIATED WITH BLADDER DISORDER DIAGNOSTIC TREATMENT

6.2.2 PRODUCTS RECALLS FROM MARKET

6.3 OPPORTUNITIES

6.3.1 SURGE IN NOVEL TECHNOLOGICAL ADVANCEMENTS

6.3.2 RISING DISEASE MANAGEMENT PROGRAMS

6.4 CHALLENGES

6.4.1 LACK OF AWARENESS ABOUT BLADDER DISORDERS RELATED PROBLEMS

6.4.2 PATENT EXPIRY OF DRUGS

7 NORTH AMERICA BLADDER DISORDERS MARKET, BY TYPE

7.1 OVERVIEW

7.2 OVERACTIVE BLADDER

7.3 URINARY INCONTINENCE

7.4 CYSTITIS

7.5 INTERSTITIAL CYSTITIS

7.6 BLADDER CANCER

7.7 OTHERS

8 NORTH AMERICA BLADDER DISORDERS MARKET, BY TREATMENT TYPE

8.1 OVERVIEW

8.2 MEDICATION

8.2.1 TOLTERODINE

8.2.2 MIRABEGRON

8.2.3 FESOTERODINE

8.2.4 OXYBUTYNIN

8.2.5 SOLIFENACIN

8.2.6 DARIFENACIN

8.2.7 TROSPIUM

8.2.8 OTHERS

8.3 SURGERY

8.3.1 SURGERY TO INCREASE BLADDER CAPACITY

8.3.2 BLADDER REMOVAL

8.3.3 OTHERS

8.4 OTHERS

9 NORTH AMERICA BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL

9.1 OVERVIEW

9.2 DIRECT

9.3 RETAIL

10 NORTH AMERICA BLADDER DISORDERS MARKET, BY END USER

10.1 OVERVIEW

10.2 HOSPITALS

10.3 CLINICS

10.4 AMBULATORY SURGICAL CENTERS

10.5 OTHERS

11 NORTH AMERICA BLADDER DISORDERS MARKET, BY GEOGRAPHY

11.1 NORTH AMERICA

11.1.1 U.S.

11.1.2 CANADA

11.1.3 MEXICO

12 NORTH AMERICA BLADDER DISORDERS MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 MERCK AND CO. INC. (2021)

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENT

14.2 ASTELLAS PHARMA INC. (2021)

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENTS

14.3 BRISTOL-MYERS SQUIBB COMPANY (2021)

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENT

14.4 BOSTON SCIENTIFIC CORPORATION (2021)

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENT

14.5 VIATRIS INC. (2021)

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT PORTFOLIO

14.5.5 RECENT DEVELOPMENT

14.6 ABBVIE (2021)

14.6.1 COMPANY SNAPSHOT

14.6.2 REVENUE ANALYSIS

14.6.3 PRODUCT PORTFOLIO

14.6.4 RECENT DEVELOPMENT

14.7 AXONICS, INC. (2021)

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCT PORTFOLIO

14.7.4 RECENT DEVELOPMENT

14.8 BLUE WIND MEDICAL (2021)

14.8.1 COMPANY SNAPSHOT

14.8.2 PRODUCT PORTFOLIO

14.8.3 RECENT DEVELOPMENT

14.9 COLOPLAST CORP. (2021)

14.9.1 COMPANY SNAPSHOT

14.9.2 REVENUE ANALYSIS

14.9.3 PRODUCT PORTFOLIO

14.1 GAYLORD CHEMICAL COMPANY, LLC (2021)

14.10.1 COMPANY SNAPSHOT

14.10.2 PRODUCT PORTFOLIO

14.10.3 RECENT DEVELOPMENT

14.11 JOHNSON & JOHNSON SERVICES, INC. (2021)

14.11.1 COMPANY SNAPSHOT

14.11.2 REVENUE ANALYSIS

14.11.3 PRODUCT PORTFOLIO

14.11.4 RECENT DEVELOPMENT

14.12 KYORIN PHARMACEUTICAL CO., LTD. (A SUBSIDIARY OF KYORIN HOLDINGS, INC.) (2021)

14.12.1 COMPANY SNAPSHOT

14.12.2 PRODUCT PORTFOLIO

14.12.3 RECENT DEVELOPMENTS

14.13 LABORIE (2021)

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCT PORTFOLIO

14.13.3 RECENT DEVELOPMENT

14.14 MEDTRONIC (2021)

14.14.1 COMPANY SNAPSHOT

14.14.2 REVENUE ANALYSIS

14.14.3 PRODUCT PORTFOLIO

14.14.4 RECENT DEVELOPMENTS

14.15 PFIZER INC. (2021)

14.15.1 COMPANY SNAPSHOT

14.15.2 REVENUE ANALYSIS

14.15.3 PRODUCT PORTFOLIO

14.15.4 RECENT DEVELOPMENTS

14.16 VALENCIA TECHNOLOGIES (2021)

14.16.1 COMPANY SNAPSHOT

14.16.2 PRODUCT PORTFOLIO

14.16.3 RECENT DEVELOPMENT

14.17 SUN PHAMACEUTICAL INDUSTRIES LTD. (2021)

14.17.1 COMPANY SNAPSHOT

14.17.2 REVENUE ANALYSIS

14.17.3 PRODUCT PORTFOLIO

14.17.4 RECENT DEVELOPMENT

14.18 SWATI SPENTOSE (2021)

14.18.1 COMPANY SNAPSHOT

14.18.2 PRODUCT PORTFOLIO

14.18.3 RECENT DEVELOPMENT

14.19 UROVANT SCIENCES (2021)

14.19.1 COMPANY SNAPSHOT

14.19.2 PRODUCT PORTFOLIO

14.19.3 RECENT DEVELOPMENT

14.2 ZYDUS GROUP (2021)

14.20.1 COMPANY SNAPSHOT

14.20.2 PRODUCT PORTFOLIO

14.20.3 RECENT DEVELOPMENT

15 QUESTIONNAIRE

16 RELATED REPORTS

表のリスト

TABLE 1 NORTH AMERICA BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 2 NORTH AMERICA OVERACTIVE BLADDER IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 3 NORTH AMERICA URINARY INCONTINENCE IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 4 NORTH AMERICA CYSTITIS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 5 NORTH AMERICA INTERSTITIAL CYSTITIS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 6 NORTH AMERICA BLADDER CANCER IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 7 NORTH AMERICA OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 8 NORTH AMERICA BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 9 NORTH AMERICA MEDICATION IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 10 NORTH AMERICA MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 11 NORTH AMERICA SURGERY IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 12 NORTH AMERICA SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 13 NORTH AMERICA OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 14 NORTH AMERICA BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 15 NORTH AMERICA DIRECT IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 16 NORTH AMERICA RETAIL IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 17 NORTH AMERICA BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 18 NORTH AMERICA HOSPITALS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 19 NORTH AMERICA CLINICS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 20 NORTH AMERICA AMBULATORY SURGICAL CENTERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 21 NORTH AMERICA OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 22 NORTH AMERICA BLADDER DISORDERS MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 23 NORTH AMERICA BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 24 NORTH AMERICA BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 25 NORTH AMERICA MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 26 NORTH AMERICA SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 27 NORTH AMERICA BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 28 NORTH AMERICA BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 29 U.S. BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 30 U.S. BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 31 U.S. MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 32 U.S. SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 33 U.S. BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 34 U.S. BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 35 CANADA BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 36 CANADA BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 37 CANADA MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 38 CANADA SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 39 CANADA BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 40 CANADA BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 41 MEXICO BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 42 MEXICO BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 43 MEXICO MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 44 MEXICO SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 45 MEXICO BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 46 MEXICO BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

図表一覧

FIGURE 1 NORTH AMERICA BLADDER DISORDERS MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA BLADDER DISORDERS MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA BLADDER DISORDERS MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA BLADDER DISORDERS MARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA BLADDER DISORDERS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA BLADDER DISORDERS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA BLADDER DISORDERS MARKET: DBMR MARKET POSITION GRID

FIGURE 8 NORTH AMERICA BLADDER DISORDERS MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 NORTH AMERICA BLADDER DISORDERS MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 NORTH AMERICA BLADDER DISORDERS MARKET: SEGMENTATION

FIGURE 11 RISING EPIDEMIC AND PANDEMIC OUTBREAK AND INCREASING PREVALENCE OF BLADDER DISORDERS EXPECTED TO DRIVE THE NORTH AMERICA BLADDER DISORDERS MARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 12 OVERACTIVE BLADDER SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA BLADDER DISORDERS MARKET IN 2022 & 2029

FIGURE 13 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE NORTH AMERICA BLADDER DISORDER MARKET

FIGURE 14 NORTH AMERICA BLADDER DISORDERS MARKET: BY TYPE, 2021

FIGURE 15 NORTH AMERICA BLADDER DISORDERS MARKET: BY TYPE, 2022-2029 (USD MILLION)

FIGURE 16 NORTH AMERICA BLADDER DISORDERS MARKET: BY TYPE, CAGR (2022-2029)

FIGURE 17 NORTH AMERICA BLADDER DISORDERS MARKET: BY TYPE, LIFELINE CURVE

FIGURE 18 NORTH AMERICA BLADDER DISORDERS MARKET: BY TREATMENT TYPE, 2021

FIGURE 19 NORTH AMERICA BLADDER DISORDERS MARKET: BY TREATMENT TYPE, 2022-2029 (USD MILLION)

FIGURE 20 NORTH AMERICA BLADDER DISORDERS MARKET: BY TREATMENT TYPE, CAGR (2022-2029)

FIGURE 21 NORTH AMERICA BLADDER DISORDERS MARKET: BY TREATMENT TYPE, LIFELINE CURVE

FIGURE 22 NORTH AMERICA BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, 2021

FIGURE 23 NORTH AMERICA BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, 2022-2029 (USD MILLION)

FIGURE 24 NORTH AMERICA BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, CAGR (2022-2029)

FIGURE 25 NORTH AMERICA BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, LIFELINE CURVE

FIGURE 26 NORTH AMERICA BLADDER DISORDERS MARKET: BY END USER, 2021

FIGURE 27 NORTH AMERICA BLADDER DISORDERS MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 28 NORTH AMERICA BLADDER DISORDERS MARKET: BY END USER, CAGR (2022-2029)

FIGURE 29 NORTH AMERICA BLADDER DISORDERS MARKET: BY END USER, LIFELINE CURVE

FIGURE 30 NORTH AMERICA BLADDER DISORDERS MARKET: SNAPSHOT (2021)

FIGURE 31 NORTH AMERICA BLADDER DISORDERS MARKET: BY COUNTRY (2021)

FIGURE 32 NORTH AMERICA BLADDER DISORDERS MARKET: BY COUNTRY (2022 & 2029)

FIGURE 33 NORTH AMERICA BLADDER DISORDERS MARKET: BY COUNTRY (2021 & 2029)

FIGURE 34 NORTH AMERICA BLADDER DISORDERS MARKET: BY TYPE (2022-2029)

FIGURE 35 NORTH AMERICA BLADDER DISORDERS MARKET: COMPANY SHARE 2021 (%)

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。