世界の自動車卸売・流通市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

221.32 Billion

USD

339.66 Billion

2025

2033

USD

221.32 Billion

USD

339.66 Billion

2025

2033

| 2026 –2033 | |

| USD 221.32 Billion | |

| USD 339.66 Billion | |

| % | |

|

世界の自動車卸売・流通市場の区分、交換部品(タイヤ、バッテリー、ブレーキ部品、フィルター、ボディ部品、照明・電子部品、ホイール、排気部品など)、認証(純正部品、認証部品、非認証部品)、流通チャネル(小売業者、卸売業者、販売業者)、サービスチャネル(DIY、DIFM、OEM) - 2033年までの業界動向と予測

卸売・流通自動車市場規模

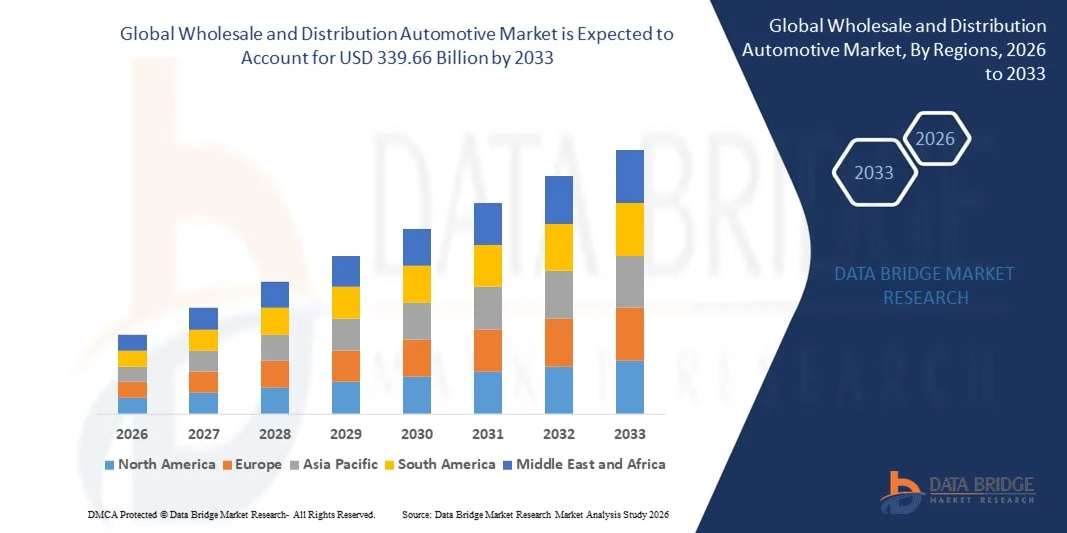

- 世界の自動車卸売・流通市場規模は2025年に2,213.2億米ドルと評価され、予測期間中に5.50%のCAGRで成長し、2033年までに3,396.6億米ドル に達すると予想されています。

- 市場の成長は、主に自動車アフターマーケット部品の需要増加、自動車流通のための電子商取引プラットフォームの拡大、新興国における自動車保有台数の増加によって推進されている。

- さらに、電気自動車の普及と特殊な部品やコンポーネントの需要の増加が市場の成長をさらに促進しています。

卸売・流通自動車市場分析

- デジタル流通チャネル、サプライチェーンの最適化、高度な在庫管理ソリューションの統合により、市場は変革を目の当たりにしています。

- メーカー、販売業者、小売業者間の連携が強化され、自動車部品の配送の可用性と効率性が向上し、市場全体の状況が強化されています。

- 北米は、確立された自動車産業、強力なアフターマーケットの需要、デジタル流通チャネルの採用率の高さにより、2025年には25.3%という最大の収益シェアで自動車卸売・流通市場を支配しました。

- アジア太平洋地域は、自動車保有台数の増加、可処分所得の増加、アフターマーケットサービスの採用拡大、新興国における効率的な物流・流通ネットワークの拡大により、世界の自動車卸売・流通市場において最も高い成長率を達成すると予想されています。

- タイヤセグメントは、高い交換頻度、車両普及率、そして耐久性と性能重視のタイヤに対する需要の高まりにより、2025年には最大の市場収益シェアを獲得しました。タイヤは車両の安全性と効率性に不可欠であり、販売業者や小売業者にとって重要な焦点となっています。

レポートの範囲と卸売・流通自動車市場のセグメンテーション

|

属性 |

卸売・流通 自動車の主要市場インサイト |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジ市場調査チームがまとめた市場レポートには、市場価値、成長率、市場セグメント、地理的範囲、市場プレーヤー、市場シナリオなどの市場洞察に加えて、専門家による詳細な分析、輸入/輸出分析、価格分析、生産消費分析、ペストル分析が含まれています。 |

卸売・流通自動車市場動向

電子商取引と効率的な流通チャネルの需要の高まり

- デジタル販売プラットフォームと合理化されたサプライチェーンへの注目が高まるにつれ、自動車卸売・流通市場は大きく変化しています。企業は、より迅速な配送、幅広い製品ラインナップ、そして信頼性の高い在庫管理を提供するチャネルをますます好むようになっています。オンラインおよびオムニチャネルの流通ソリューションは、運用コストの削減、サービス効率の向上、顧客満足度の向上といったメリットから注目を集めており、流通業者による革新的な物流およびデジタルツールの導入を促進しています。

- 車両メンテナンス、アフターマーケット部品の入手可能性、そして便利な注文オプションに関する意識の高まりにより、乗用車、商用車、そして特殊車両分野において、卸売・流通サービスの導入が加速しています。消費者やフリートオペレーターは、スペアパーツやアクセサリーをより迅速かつ容易に入手できるチャネルを積極的に求めており、企業は販売代理店やeコマースプラットフォームとの提携を強化しています。

- AIベースの在庫管理、予測分析、自動倉庫といった技術の進歩は購買決定に影響を与えており、販売業者は納期の短縮、透明性の高いサプライチェーン、リアルタイムの追跡を重視しています。これらの要素は、自動車メーカーが競争の激しい市場において差別化を図り、業務効率と顧客満足度を向上させるのに役立ちます。

- 例えば、2024年には、米国のオートゾーンとLKQコーポレーションがデジタル流通ネットワークを拡大し、スペアパーツとアクセサリーのeコマースプラットフォームを統合しました。これらの取り組みは、より迅速で便利な部品配送と幅広い製品供給に対する需要の高まりに対応して導入され、小売店、オンラインマーケットプレイス、フリートサービスチャネルを通じた流通を実現しています。

- 効率的な卸売・流通チャネルへの需要が高まる一方で、持続的な市場拡大は、物流インフラ、デジタルプラットフォーム、そしてサプライチェーンの信頼性への継続的な投資にかかっています。企業はまた、より広範な導入に向けて、コスト、スピード、そしてサービス品質のバランスをとるために、在庫管理、配送ネットワーク、そして受注処理の最適化にも注力しています。

卸売・流通自動車市場の動向

ドライバ

電子商取引とオムニチャネル流通の導入拡大

- より迅速で便利な発注・配送ソリューションへの需要の高まりは、自動車卸売・流通市場における大きな原動力となっています。流通業者は、消費者の期待に応え、製品の入手性を向上させ、市場リーチを拡大するために、オンラインプラットフォームと従来の小売ネットワークの統合を進めています。

- 自動車アフターマーケット、フリートマネジメント、交換部品セグメントの拡大が市場の成長に影響を与えています。効率的な流通チャネルは、タイムリーな納品、ダウンタイムの削減、車両性能の維持に役立ち、高品質な部品とサービスに対する高まる需要に対応します。

- 自動車メーカーと販売店は、パートナーシップ、テクノロジーの導入、物流の改善を通じて、デジタル販売とサプライチェーンの合理化を積極的に推進しています。これらの取り組みは、自動車保有台数の増加、都市化、そしてコネクテッドカーや電気自動車への移行によって支えられており、これらの車には専門的な流通ソリューションが求められています。

- 例えば、2023年には、米国のアドバンス・オート・パーツとイタリアのブレンボが、デジタル注文追跡と倉庫自動化を統合することで物流効率が向上したと報告しました。この拡大は、自動車部品やアクセサリーのタイムリーな配送に対する需要の高まりを受けて実施され、顧客満足度とロイヤルティの強化につながりました。

- 電子商取引とオムニチャネルの普及拡大は成長を支えているものの、市場への浸透拡大には物流の最適化、コスト管理、そして技術投資が不可欠です。倉庫の自動化、AIを活用した在庫追跡、そして堅牢な配送ネットワークへの投資は、世界的な需要に対応し、競争優位性を維持するために不可欠です。

抑制/挑戦

High Operational Costs And Complex Supply Chain Management

- The relatively high operational cost of maintaining extensive distribution networks, warehousing, and last-mile delivery remains a key challenge, limiting profitability for some distributors. Rising fuel costs, labor expenses, and technology investments contribute to elevated operating costs

- Market awareness and digital adoption remain uneven, particularly in emerging economies where online and omnichannel distribution is still developing. Limited understanding of e-commerce and logistics efficiency restricts market growth in certain regions

- Supply chain complexities also impact market expansion, as automotive parts distribution requires coordination among manufacturers, wholesalers, retailers, and service providers. Delays, inventory mismanagement, and logistical inefficiencies can affect service quality and customer satisfaction

- For instance, in 2024, distributors in India and Southeast Asia supplying aftermarket parts to automotive service providers reported slower growth due to high operational costs and limited digital adoption. Infrastructure limitations and fragmented supply networks were additional barriers, affecting timely delivery and market reach

- Overcoming these challenges will require investment in cost-efficient logistics, digital supply chain platforms, and education for distributors and retailers. Collaboration with manufacturers, e-commerce platforms, and fleet operators can help unlock the long-term growth potential of the global wholesale and distribution automotive market. Furthermore, optimizing delivery networks and inventory management will be essential for widespread adoption

Wholesale and Distribution Automotive Market Scope

The market is segmented on the basis of replacement part, certification, distribution channel, and service channel.

- By Replacement Part

On the basis of replacement part, the wholesale and distribution automotive market is segmented into tire, battery, brake parts, filters, body parts, lighting and electronic components, wheels, exhaust components, and others. The tire segment held the largest market revenue share in 2025, driven by high replacement frequency, widespread vehicle usage, and increasing demand for durable and performance-oriented tires. Tires are essential for vehicle safety and efficiency, making them a key focus for distributors and retailers.

The battery segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising adoption of electric vehicles and hybrid vehicles, which require frequent replacement and advanced battery technologies. Battery replacement demand is further fueled by consumer preference for longer-lasting, high-capacity batteries and the increasing use of battery management systems in modern vehicles.

- By Certification

On the basis of certification, the market is segmented into genuine parts, certified parts, and uncertified parts. The genuine parts segment held the largest market revenue share in 2025, fueled by consumer preference for original equipment manufacturer (OEM) quality, reliability, and warranty assurance. Genuine parts are widely sought after by vehicle owners and service centers to maintain vehicle performance and safety standards.

The certified parts segment is expected to witness the fastest growth rate from 2026 to 2033, driven by regulatory compliance requirements, rising awareness of safety standards, and the increasing availability of certified aftermarket components. Certified parts offer verified quality and performance while often being more cost-effective than OEM parts.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into retailers, wholesalers, and distributors. The retailers segment held the largest revenue share in 2025, driven by the accessibility of automotive parts to end consumers, the expansion of retail networks, and growing online sales channels. Retailers often combine physical stores and e-commerce platforms to provide convenient purchasing options.

The distributors segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the increasing demand for bulk supply, fleet management services, and partnerships with automotive manufacturers. Distributors provide efficient supply chain solutions and enable wider market penetration for replacement parts.

- By Service Channel

On the basis of service channel, the market is segmented into DIY, DIFM (Do It For Me), and OEM. The DIFM segment held the largest market revenue share in 2025, driven by vehicle owners’ preference for professional installation, convenience, and assurance of proper fitment and performance. DIFM services are commonly offered by service centers, workshops, and dealerships.

The DIY segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing trend of vehicle owners performing minor repairs and replacements themselves, supported by online tutorials, instructional content, and availability of easy-to-install parts.

Wholesale and Distribution Automotive Market Regional Analysis

- North America dominated the wholesale and distribution automotive market with the largest revenue share of 25.3% in 2025, driven by a well-established automotive industry, strong aftermarket demand, and high adoption of digital distribution channels

- Businesses in the region highly value efficient supply chain management, reliable inventory availability, and fast delivery services offered by wholesalers and distributors, ensuring timely access to replacement parts and automotive components

- This widespread adoption is further supported by robust infrastructure, advanced logistics networks, and a strong focus on fleet management and service quality, establishing wholesale and distribution channels as a preferred solution for automotive parts in both commercial and retail segments

U.S. Wholesale and Distribution Automotive Market Insight

The U.S. wholesale and distribution automotive market captured the largest revenue share in 2025 within North America, fueled by increasing vehicle parc, rising demand for aftermarket parts, and the growing trend of online automotive sales. Businesses are prioritizing faster, reliable access to replacement components through integrated distribution networks. The expansion of e-commerce platforms, coupled with advanced inventory management systems and fleet servicing solutions, further propels the market. Moreover, partnerships between distributors, retailers, and manufacturers enhance availability and operational efficiency, significantly contributing to market growth.

Europe Wholesale and Distribution Automotive Market Insight

The Europe wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by regulatory requirements for quality and safety, increasing vehicle ownership, and demand for timely delivery of replacement parts. Urbanization, coupled with the growth of connected vehicle technologies, is fostering the adoption of advanced distribution solutions. European businesses are also investing in digital supply chain platforms to ensure seamless procurement and distribution across retail and commercial segments.

U.K. Wholesale and Distribution Automotive Market Insight

The U.K. wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for aftermarket parts, fleet management services, and e-commerce-based distribution. Concerns over vehicle downtime and the need for prompt maintenance are encouraging businesses and individual consumers to rely on professional distributors and wholesalers. The country’s well-developed logistics and retail infrastructure, alongside increasing online sales penetration, is expected to continue supporting market growth.

Germany Wholesale and Distribution Automotive Market Insight

The Germany wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s large automotive manufacturing base, high-quality standards, and advanced logistics networks. Businesses in Germany are increasingly adopting integrated inventory management, automated warehousing, and digital ordering solutions to enhance distribution efficiency. The emphasis on timely delivery, sustainability in logistics, and operational optimization supports market adoption across commercial and retail segments.

Asia-Pacific Wholesale and Distribution Automotive Market Insight

The Asia-Pacific wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, rising vehicle sales, and expansion of automotive aftermarket infrastructure in countries such as China, Japan, and India. Growing urbanization, increasing disposable incomes, and technological advancements in logistics and e-commerce platforms are driving the adoption of efficient distribution solutions. Furthermore, APAC’s emergence as a manufacturing hub for automotive components enhances affordability and accessibility of replacement parts across the region.

Japan Wholesale and Distribution Automotive Market Insight

The Japan wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s high vehicle ownership, demand for efficient fleet management, and adoption of digital supply chain solutions. Japanese businesses increasingly rely on distributors and wholesalers for timely access to replacement parts, ensuring minimal downtime and operational efficiency. Integration of automated inventory management, predictive ordering, and e-commerce channels is fueling growth, while aging population trends also boost demand for easy-to-access automotive services.

China Wholesale and Distribution Automotive Market Insight

The China wholesale and distribution automotive market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding automotive industry, rapidly growing vehicle parc, and rising demand for aftermarket services. China is one of the largest markets for replacement parts and automotive components, with wholesalers and distributors playing a critical role in ensuring availability across retail, commercial, and fleet segments. Government initiatives promoting digitalization, expansion of e-commerce channels, and local manufacturing capabilities are key factors propelling market growth.

Wholesale and Distribution Automotive Market Share

The Wholesale and Distribution Automotive industry is primarily led by well-established companies, including:

- 3M (U.S.)

- Continental AG (Germany)

- BorgWarner Inc. (U.S.)

- DENSO CORPORATION (Japan)

- Tenneco Inc. (U.S.)

- Marelli Holdings Co., Ltd. (Japan)

- Robert Bosch GmbH (Germany)

- The Goodyear Tire and Rubber Company (U.S.)

- ZF Friedrichshafen AG (Germany)

- Cooper Tire and Rubber Company (U.S.)

- LEMANS CORPORATION (U.S.)

- Motorsport Aftermarket Group (U.S.)

- Textron Inc. (U.S.)

- Western Power Sports, Inc. (U.S.)

- Polaris Inc. (U.S.)

- AISIN SEIKI Co., Ltd. (Japan)

- Deere and Company (U.S.)

- BRP (Canada)

Latest Developments in Global Wholesale and Distribution Automotive Market

- 2023年7月、ゼネラルモーターズ(GM)はイスラエルに拠点を置くバッテリーソフトウェアのスタートアップ企業ALGOLiON Ltd.の買収を完了しました。GMのテクノロジー・アクセラレーション・アンド・コマーシャルライゼーション(TAC)チームが主導するこの戦略的買収は、高度なソフトウェアソリューションを通じてGMのバッテリー開発能力を強化することを目的としています。この買収は、GMの電気自動車技術における地位を強化し、バッテリーの性能、効率、エネルギー管理におけるイノベーションを加速させ、EV市場にプラスの影響を与えるでしょう。

- 2023年6月、コンチネンタルAGは、同社史上最も環境に優しいタイヤ「UltraContact NXT」を発表しました。最大65%のリサイクル材、再生可能材、そしてマスバランス認証取得済みの素材を使用したこのタイヤは、環境への影響を低減しながら、最高レベルの安全性と性能を提供します。この発売は、コンチネンタルのサステナビリティ戦略を強化し、環境意識の高い消費者のニーズに応えることで、グリーンモビリティソリューションにおける市場競争力を高めるものです。

- 2023年5月、ステランティスNVはサウジアラビアのペトロミンと提携し、自動車部品およびメンテナンス用品のEuroreparラインを立ち上げました。この提携により、車両メンテナンスのアクセシビリティが向上し、道路安全への取り組みが促進されます。信頼性の高い部品を提供することで、ステランティスはアフターマーケットにおけるプレゼンスを強化し、中東地域における市場リーチを拡大します。

- コンチネンタルAGは2023年2月、舗装路と未舗装路の両方で多用途に使用できるよう設計されたサマータイヤ「CrossContact H/T」を発売しました。従来型車両と電気自動車の両方に適しており、優れた耐久性と快適性、そして軽度のオフロード走行に対応するM+Sグレードを含む安全性を兼ね備えています。この発売により、コンチネンタルの製品ポートフォリオが拡充され、多目的・高性能タイヤに対する消費者の需要に応えます。

- ボルグワーナー社は2023年3月、従来の鋳鉄製ディスクよりも軽量で静粛性が高く、燃費効率に優れたバイメタルブレーキディスクを発表しました。この2層構造の合金設計により、重量が15%軽減され、燃費と排出ガス量が向上するとともに、振動と騒音を最小限に抑え、よりスムーズな乗り心地を実現します。このイノベーションは、車両の性能と持続可能性を向上させ、ブレーキ部品市場におけるボルグワーナーの競争力を強化します。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。