Global Robotic Flight Simulator Surgery Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

549.22 Million

USD

1,230.55 Million

2025

2033

USD

549.22 Million

USD

1,230.55 Million

2025

2033

| 2026 –2033 | |

| USD 549.22 Million | |

| USD 1,230.55 Million | |

| % | |

|

Global Robotic Flight Simulator Surgery Market Segmentation, By Application (General Surgery, Neurosurgery, Cardiology Surgery, and Gynecology), Method (Direct Telemanipulator and Computer Control), End-User (Hospitals and Ambulatory Surgical Centers) - Industry Trends and Forecast to 2033

Robotic Flight Simulator Surgery Market Size

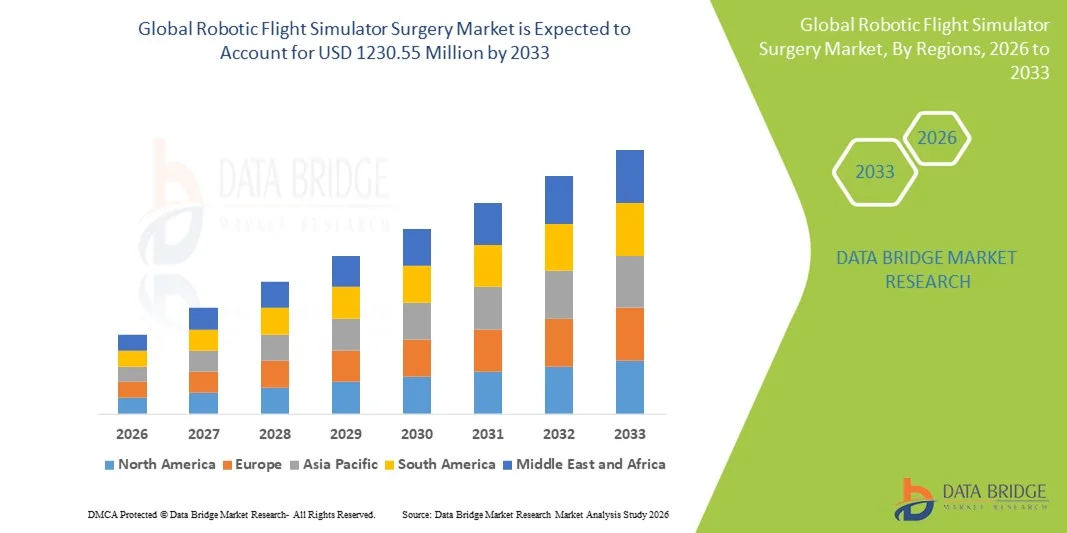

- The global robotic flight simulator surgery market size was valued at USD 549.22 Million in 2025 and is expected to reach USD 1230.55 Million by 2033, at a CAGR of 10.61% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced surgical training technologies and the rising demand for precision-based surgical simulations, enabling surgeons to practice complex procedures in a risk-free environment

- Furthermore, growing emphasis on medical education, coupled with technological advancements in robotic simulation platforms, is driving the demand for Robotic Flight Simulator Surgery solutions. These factors are accelerating the adoption of these simulators across hospitals, medical training institutes, and research centers, thereby significantly boosting the industry’s growth

Robotic Flight Simulator Surgery Market Analysis

- Surgical simulation platforms, particularly robotic flight simulator surgery systems, are increasingly vital components of modern surgical training and pre‑operative planning across both tertiary care centers and medical education institutions due to their enhanced realism, immersive 3D environments, and ability to replicate complex procedures without patient risk

- The escalating demand for robotic flight simulator surgery solutions is primarily fueled by the widespread adoption of robotic surgical systems, growing emphasis on improving surgical outcomes, and the rising need for standardized, competency‑based surgeon training. These converging factors are accelerating the uptake of simulator platforms, thereby significantly boosting the industry’s growth

- North America dominated the robotic flight simulator surgery market with the largest revenue share of 37.5% in 2025, characterized by advanced healthcare infrastructure, strong research and clinical training programs, high healthcare spending, and a strong presence of key industry players. The U.S. has experienced substantial growth in simulator installations in academic hospitals and surgical training centers, driven by collaborations between device manufacturers and medical schools

- Asia‑Pacific is expected to be the fastest‑growing region in the robotic flight simulator surgery market during the forecast period due to increasing healthcare investments, expanding surgical robotics adoption, rising numbers of medical training institutes, and growing demand for high‑fidelity surgical education in countries such as China and India

- The Direct Telemanipulator segment held the largest market revenue share of 48.2% in 2025, supported by its ability to provide realistic tactile feedback and direct replication of surgeon movements

Report Scope and Robotic Flight Simulator Surgery Market Segmentation

|

Attributes |

Robotic Flight Simulator Surgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Robotic Flight Simulator Surgery Market Trends

Enhanced Realism and Immersive Surgical Training

- A significant and accelerating trend in the global robotic flight simulator surgery market is the increasing adoption of high-fidelity simulators with realistic haptic feedback, 3D visualization, and VR-based procedural environments. These systems allow surgeons to practice complex operations in a risk-free setting, improving skill acquisition and reducing the learning curve for robotic-assisted surgeries

- For instance, the Simulab Robotic Surgery Trainer provides full tactile feedback along with anatomically accurate models, enabling residents and practicing surgeons to rehearse minimally invasive procedures prior to operating on actual patients. Such advanced simulators are becoming a standard component in teaching hospitals and surgical training centers worldwide

- The integration of real-time performance analytics and scenario-based simulations enables trainees to receive quantitative feedback on efficiency, precision, and instrument handling. This allows for objective assessment of surgical competencies and helps institutions standardize skill evaluation

- The seamless incorporation of robotic simulators into academic curricula ensures trainees can practice a wide variety of procedures without patient risk, fostering improved procedural accuracy and confidence

- This trend towards more realistic, immersive, and data-driven surgical training is reshaping expectations for medical education, making simulation-based competency a core requirement for modern robotic-assisted surgery program

- Demand for advanced surgical simulators is growing rapidly in both academic and hospital settings, as institutions seek to improve patient outcomes while minimizing procedural errors

Robotic Flight Simulator Surgery Market Dynamics

Driver

Rising Demand for Skilled Robotic Surgeons and Training Programs

- The increasing number of robotic-assisted procedures in general surgery, urology, gynecology, and cardiothoracic disciplines is driving the need for comprehensive simulator-based training programs. Surgeons require extensive practice on simulators before performing operations on patients to reduce errors and improve outcomes

- For instance, in March 2024, Medtronic expanded its robotic surgery training program in collaboration with leading U.S. academic hospitals, introducing new simulator modules for minimally invasive cardiac procedures. Such initiatives by key players are expected to drive adoption of robotic flight simulator systems in the forecast period

- As hospitals invest in robotic surgical systems, simulator adoption becomes critical for credentialing, skills assessment, and ongoing professional development

- The demand is further boosted by the growing focus on patient safety, clinical efficiency, and hospital accreditation standards, which increasingly require proficiency-based assessments

- Increased government and institutional support for medical simulation centers, along with partnerships between device manufacturers and training hospitals, enhances market penetration

- The ability of simulators to replicate rare or complex surgical scenarios also supports continuous skill development for experienced surgeons, reinforcing the growth trajectory of the market

Restraint/Challenge

High Capital Costs and Limited Accessibility

- The relatively high cost of advanced robotic flight simulators, which includes hardware, software, maintenance, and scenario updates, poses a barrier for smaller hospitals, developing countries, and budget-conscious training centers

- For instance, reports in July 2023 highlighted that several regional hospitals in Southeast Asia delayed simulator acquisition due to upfront costs exceeding USD 250,000 per unit, limiting widespread adoption despite growing demand

- In additional challenges include space requirements, technical support needs, and the learning curve associated with simulator integration into existing training programs

- While simulators offer long-term benefits in training efficiency and patient safety, the high initial investment can discourage adoption in resource-constrained settings

- To overcome these barriers, manufacturers are exploring modular, scalable simulator systems, cloud-based virtual simulations, and partnerships with academic institutions to improve accessibility and cost-efficiency

- Addressing these financial and logistical constraints will be crucial for sustained growth and broader penetration of robotic flight simulator surgery technologies globally

Robotic Flight Simulator Surgery Market Scope

The market is segmented on the basis of application, method, and end-user.

- By Application

On the basis of application, the Robotic Flight Simulator Surgery market is segmented into General Surgery, Neurosurgery, Cardiology Surgery, and Gynecology. The General Surgery segment dominated the market with the largest revenue share of 41.5% in 2025, driven by the high volume of general surgical procedures performed worldwide and the adoption of simulation-based training in medical schools and teaching hospitals. General surgery simulators provide trainees with repetitive practice opportunities, allowing them to refine techniques for procedures such as appendectomies, hernia repairs, and laparoscopic interventions, enhancing patient safety and reducing intraoperative errors. The widespread inclusion of general surgery modules in residency programs, combined with government and institutional funding for surgical education, further supports market dominance. In addition, collaborations between simulator manufacturers and hospitals have facilitated the development of highly realistic general surgery scenarios that mimic real-life complications, making the segment a preferred choice for training. High adoption in emerging economies, where surgical training resources are limited, also contributes to this segment’s leading market position. The increasing focus on competency-based education and accreditation requirements reinforces its continued dominance.

The Neurosurgery segment is expected to witness the fastest CAGR of 22.4% from 2026 to 2033, driven by the increasing complexity of neurological procedures and the need for precision-based training. Neurosurgery simulators allow surgeons to practice delicate procedures such as tumor resections, aneurysm clipping, and spinal interventions without risk to patients. Technological advancements, including enhanced 3D imaging, haptic feedback, and augmented reality integration, are improving the realism of neurosurgical simulations. Rising incidences of neurological disorders and expanding neurosurgery training programs worldwide contribute to this rapid growth. The increasing investment by hospitals, academic centers, and government bodies in neurosurgical training infrastructure further propels adoption. Emerging markets in Asia-Pacific and Latin America are also witnessing strong uptake due to increased awareness and accessibility of simulation-based surgical training solutions.

- By Method

On the basis of method, the Robotic Flight Simulator Surgery market is segmented into Direct Telemanipulator and Computer Control. The Direct Telemanipulator segment held the largest market revenue share of 48.2% in 2025, supported by its ability to provide realistic tactile feedback and direct replication of surgeon movements. This method allows for precise control of robotic instruments, making it highly effective for training across multiple surgical disciplines. Direct Telemanipulator systems are widely adopted in teaching hospitals and surgical centers due to their robustness, reliability, and ease of integration with existing training protocols. Strong collaborations between device manufacturers and medical institutions have further reinforced the market leadership of this segment.

The Computer Control segment is expected to witness the fastest CAGR of 21.1% from 2026 to 2033, driven by the increasing incorporation of artificial intelligence, motion tracking, and predictive analytics in surgical simulators. Computer Control systems allow for automated scenario customization, performance analytics, and real-time feedback, which significantly enhances the quality of surgical training. These systems are particularly preferred for complex procedures like cardiothoracic or neurosurgery. The growing emphasis on standardized skill assessment and outcome-based evaluation across hospitals and academic institutions is accelerating the adoption of computer-controlled simulators globally.

- By End-User

On the basis of end-user, the Robotic Flight Simulator Surgery market is segmented into Hospitals and Ambulatory Surgical Centers. The Hospitals segment accounted for the largest revenue share of 52.7% in 2025, driven by the high number of surgical procedures conducted in hospitals and the growing investments in advanced training infrastructure. Hospitals prefer simulators that can support multiple departments, offer extensive scenario libraries, and provide detailed performance tracking for residents and attending surgeons. The increasing focus on patient safety, regulatory requirements for surgical training, and the expansion of residency programs in developed countries further strengthen this segment’s market dominance.

The Ambulatory Surgical Centers segment is expected to witness the fastest CAGR of 19.6% from 2026 to 2033, fueled by the rising number of outpatient surgeries, cost-effective training needs, and increasing adoption of minimally invasive procedures. Ambulatory centers are increasingly investing in compact, modular simulators to enhance surgeon proficiency and reduce procedural errors. The segment is also supported by favorable government initiatives and accreditation programs promoting surgical skill enhancement in outpatient settings.

Robotic Flight Simulator Surgery Market Regional Analysis

- North America dominated the robotic flight simulator surgery market with the largest revenue share of 37.5% in 2025, supported by advanced healthcare infrastructure, strong research and clinical training programs, high healthcare spending, and the presence of key industry players. The U.S. has been the largest contributor within the region, driven by the increasing installation of simulators in academic hospitals and surgical training centers

- Collaborations between device manufacturers and medical schools have enabled extensive adoption of high-fidelity simulators, helping train surgeons in robotic-assisted procedures across specialties such as urology, gynecology, cardiothoracic, and general surgery

- The region’s focus on improving patient safety, standardizing surgical training, and integrating performance analytics into curricula further bolsters market growth

U.S. Robotic Flight Simulator Surgery Market Insight

The U.S. robotic flight simulator surgery market captured the largest revenue share within North America in 2025, driven by the increasing installation of robotic simulators in academic hospitals and surgical training centers. Collaborations between simulator manufacturers and medical schools have expanded access to high-fidelity training programs across specialties such as urology, gynecology, cardiothoracic, and general surgery. The growing emphasis on improving surgical outcomes, reducing procedural errors, and integrating performance analytics into training curricula is further propelling the U.S. market. Additionally, government initiatives and private investments in surgical education are enabling the rapid adoption of advanced simulators across hospitals and training institutes.

Europe Robotic Flight Simulator Surgery Market Insight

The Europe robotic flight simulator surgery market is expected to witness substantial growth during the forecast period, driven by stringent medical training regulations, rising adoption of robotic surgery, and increasing investments in clinical education centers. Countries like Germany, France, and Switzerland are emphasizing competency-based surgical training programs, requiring trainees to practice extensively on simulators before performing live procedures. Urbanization, rising healthcare budgets, and the focus on reducing surgical errors contribute to the increasing incorporation of robotic simulators in both teaching hospitals and private clinics. The region is also seeing growth in multi-disciplinary simulation centers that allow for standardized training across surgical specialties, boosting market expansion.

U.K. Robotic Flight Simulator Surgery Market Insight

The U.K. robotic flight simulator surgery market is projected to grow at a notable CAGR during the forecast period, driven by expanding investments in surgical robotics and increasing adoption of simulation-based training in medical curricula. The growing focus on enhancing patient safety and minimizing procedural errors is encouraging hospitals and teaching institutions to integrate advanced robotic simulators. Furthermore, government initiatives promoting medical education and skill standardization, alongside strong collaborations with simulator manufacturers, are supporting the growth of this market in the U.K.

Germany Robotic Flight Simulator Surgery Market Insight

Germany robotic flight simulator surgery market is expected to see significant growth in the Robotic Flight Simulator Surgery market due to its emphasis on technological advancement, healthcare innovation, and medical training excellence. The country’s robust healthcare infrastructure, coupled with government support for simulation-based training programs, promotes the adoption of high-fidelity robotic simulators in both academic hospitals and private training centers. Increasing awareness regarding procedural safety, precision in robotic-assisted surgeries, and the need for standardized surgeon credentialing are key factors driving market adoption.

Asia-Pacific Robotic Flight Simulator Surgery Market Insight

The Asia-Pacific robotic flight simulator surgery market is poised to be the fastest-growing region, with a CAGR of approximately 24% during 2026–2033, fueled by rising healthcare investments, increasing adoption of robotic surgical systems, and the growing number of medical training institutes. Countries such as China, India, and Japan are seeing rapid expansion in surgical education programs emphasizing high-fidelity simulation, which is essential for training surgeons in minimally invasive and robotic-assisted procedures. Government initiatives promoting advanced medical technologies, coupled with the rising number of hospitals adopting robotic systems, are driving demand for simulators. The increasing focus on reducing surgical complications, improving procedural efficiency, and expanding the skilled surgeon workforce further supports market growth.

Japan Robotic Flight Simulator Surgery Market Insight

The Japan robotic flight simulator surgery market is witnessing notable growth due to the country’s high-tech healthcare ecosystem, strong emphasis on clinical training, and increasing adoption of robotic surgical systems. Academic hospitals and specialized training centers are incorporating simulators to enhance procedural accuracy and improve surgeon confidence before real operations. Japan’s aging population and the growing need for minimally invasive surgical solutions are also contributing to increased demand for simulator-based training. The integration of robotic simulators into surgical curricula ensures comprehensive training, helping hospitals maintain high standards of patient care.

China Robotic Flight Simulator Surgery Market Insight

China robotic flight simulator surgery market accounted for the largest revenue share in the Asia-Pacific region in 2025, driven by rapid expansion in medical training programs, increasing hospital investments in robotic surgery, and a growing middle-class patient population. High demand for surgical skill standardization, combined with government-backed initiatives to modernize healthcare and promote clinical education, is accelerating simulator adoption. Moreover, as China emerges as a manufacturing hub for robotic surgical systems and simulators, affordability and accessibility are improving, enabling wider adoption across urban and semi-urban teaching hospitals and training centers.

Robotic Flight Simulator Surgery Market Share

The Robotic Flight Simulator Surgery industry is primarily led by well-established companies, including:

• Medtronic (Ireland)

• Stryker Corporation (U.S.)

• Zimmer Biomet Holdings, Inc. (U.S.)

• Smith & Nephew plc (U.K.)

• CMR Surgical Ltd. (U.K.)

• Renishaw plc (U.K.)

• Johnson & Johnson (U.S.)

• Asensus Surgical, Inc. (U.S.)

• Titan Medical Inc. (Canada)

• Think Surgical, Inc. (U.S.)

• Accuray Incorporated (U.S.)

• Auris Health, Inc. (U.S.)

• Hansen Medical, Inc. (U.S.)

• Mazor Robotics Ltd. (Israel)

• Medrobotics Corporation (U.S.)

• Corindus Vascular Robotics, Inc. (U.S.)

• Robocath (France)

Latest Developments in Global Robotic Flight Simulator Surgery Market

- In October 2025, Surgical Science announced the launch of RobotiX Express, a new portable robotic surgery training platform designed to bring professional‑grade robotic surgery simulation outside the traditional operating room into classrooms, training centers, and remote environments. The system features customized controls, foot pedals, and an integrated 3D stereoscopic display—offering high‑fidelity simulator experiences in a compact form factor, lowering barriers to surgical training worldwide

- In January 2025, Surgical Science completed the acquisition of Mimic Technologies, expanding its product portfolio and global footprint in medical and robotic surgical simulators. This strategic acquisition strengthened its position in procedural simulation and broadened access to advanced robotic surgery training solutions across major international markets

- In March 2025, Osso VR announced a partnership with Proximie to integrate its virtual reality training modules with Proximie’s remote proctoring platform, enabling expert guidance in real time during simulated procedures — a meaningful step forward in remote competency‑based robotic surgery training

- In April 2024, Haag‑Streit launched the Eyesi Indirect Ophthalmoscope ROP Simulator (Eyesi Indirect ROP) for retinal and ophthalmic training, reflecting the ongoing trend of expanding surgical and procedural simulation offerings to include specialized modules that support robotic and AI‑assisted surgical planning and education

- In March 2024, Surgical Science expanded its simulation portfolio by introducing additional modules for its URO Mentor simulator, enhancing robotic training capabilities specifically for urology procedures such as TURP for benign prostatic hyperplasia—illustrating continual enhancement of simulation content aligned with clinical practice needs

- In February 2024, Madison Industries acquired CAE Healthcare, a leader in medical simulation and surgical training systems, bolstering its ability to deliver comprehensive robotic surgical simulators and training solutions as part of an expanding integrated healthcare technology offering

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。