世界の無眼球症および小眼球症市場の規模、シェア、傾向分析レポート

Market Size in USD Billion

CAGR :

%

USD

6.77 Billion

USD

11.99 Billion

2024

2032

USD

6.77 Billion

USD

11.99 Billion

2024

2032

| 2025 –2032 | |

| USD 6.77 Billion | |

| USD 11.99 Billion | |

| % | |

|

診断(CTスキャン、MRスキャン、染色体分析、超音波検査)、治療(手術など)、エンドユーザー(病院や診療所、研究センターなど)による世界の無眼球症および小眼球症市場のセグメンテーション - 2032年までの業界動向と予測

無眼球症および小眼球症の市場分析

無眼球症および小眼球症の市場は、遺伝子研究、医療技術、およびこれらの先天性眼疾患の治療オプションの改善の進歩により成長しています。無眼球症は出生時に片目または両目が欠損している状態であり、小眼球症は正常よりも小さい未発達の目を指します。これらの疾患は通常、乳児期に診断され、生活の質を向上させるには早期介入が不可欠です。市場は、遺伝子検査、画像診断、分子診断などの診断技術の革新の恩恵を受けており、これらの疾患を早期かつ正確に特定するのに役立ちます。さらに、義眼や再建手術などの外科技術の進歩により、罹患した個人の転帰が改善されています。市場は、意識の高まり、医療費の増加、および眼科医療における技術の進歩にも支えられています。北米などの地域は、医療インフラの整備、高度な医療研究、および遺伝性疾患の発生率の高さにより、市場を支配すると予想されています。一方、アジア太平洋地域は、医療技術の急速な発展と患者数の増加により、最も高い成長が見込まれています。遺伝子治療と幹細胞技術の研究が進行中であり、無眼球症と小眼球症の治療の将来は有望に見えます。

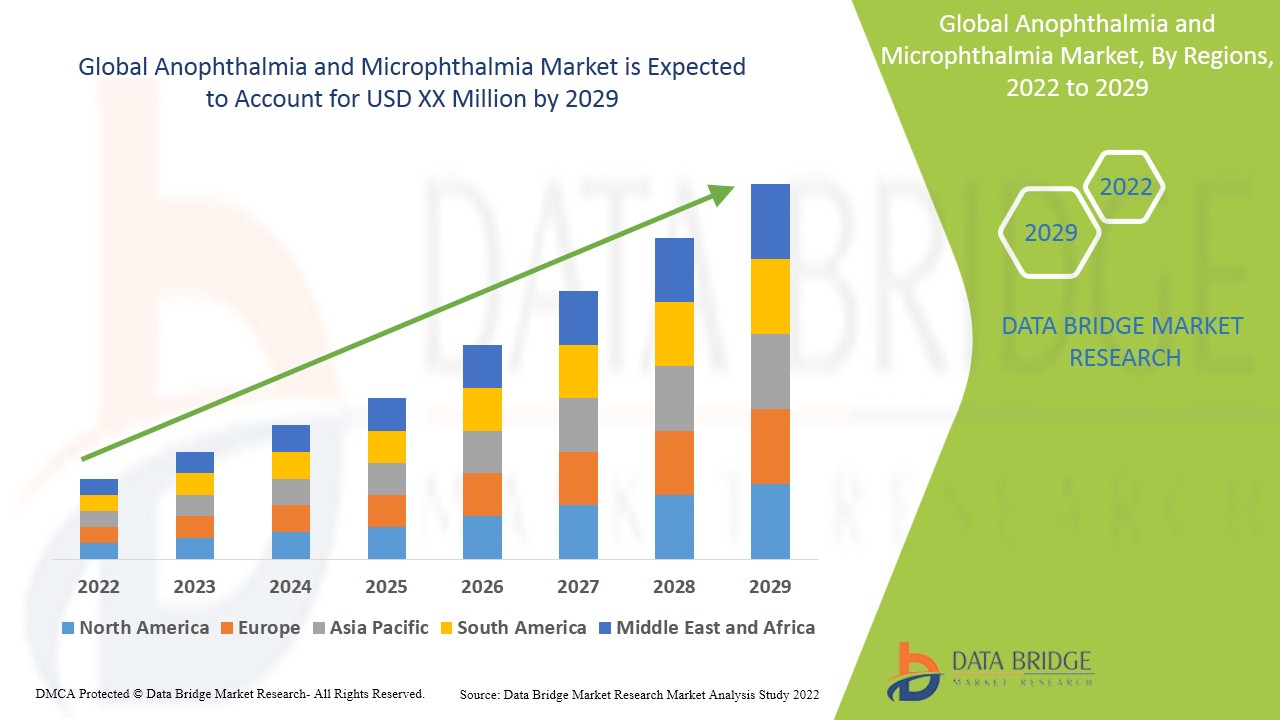

無眼球症および小眼球症の市場規模

世界の無眼球症および小眼球症の市場規模は、2024年に67億7,000万米ドルと評価され、2025年から2032年の予測期間中に7.40%のCAGRで成長し、2032年までに119億9,000万米ドルに達すると予測されています。市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがまとめた市場レポートには、詳細な専門家の分析、患者の疫学、パイプライン分析、価格分析、規制の枠組みも含まれています。

無眼球症および小眼球症の市場動向

「個別化治療と遺伝子治療への注目が高まる」

無眼球症および小眼球症市場における顕著な傾向の 1 つは、個別化治療および遺伝子ベースの治療への注目が高まっていることです。遺伝子検査および研究の進歩により、これらの先天性眼疾患の早期診断がより正確になり、罹患した個人に合わせた治療アプローチが可能になりました。たとえば、遺伝子検査により、無眼球症および小眼球症に関連する特定の変異を特定できるようになり、医療提供者は個別化された介入を提供できるようになりました。さらに、義眼や幹細胞療法などの革新的な外科技術の開発により、治療結果が向上しています。医療インフラが最先端の技術をサポートしている北米やヨーロッパなどの地域では、このような個別化された治療の需要が急速に高まっています。さらに、遺伝子治療の進歩により、これらの疾患を引き起こす遺伝子欠陥を修正できる可能性が示されており、将来のブレークスルーへの希望が生まれています。遺伝子ベースの治療が進化し続けると、無眼球症および小眼球症の管理を変革する上で重要な役割を果たし、市場を前進させるでしょう。

レポートの範囲と無眼球症および小眼球症の市場セグメンテーション

|

属性 |

無眼球症と小眼球症の主要市場洞察 |

|

対象セグメント |

|

|

対象国 |

北米では米国、カナダ、メキシコ、ヨーロッパではドイツ、フランス、英国、オランダ、スイス、ベルギー、ロシア、イタリア、スペイン、トルコ、その他のヨーロッパ、ヨーロッパでは中国、日本、インド、韓国、シンガポール、マレーシア、オーストラリア、タイ、インドネシア、フィリピン、アジア太平洋地域 (APAC) ではその他のアジア太平洋地域 (APAC)、中東およびアフリカ (MEA) の一部としてサウジアラビア、UAE、南アフリカ、エジプト、イスラエル、中東およびアフリカ (MEA) の一部としてその他の中東およびアフリカ (MEA)、南米の一部としてブラジル、アルゼンチン、その他の南米 |

|

主要な市場プレーヤー |

ブリストル・マイヤーズ スクイブ社(米国)、ヌサピュア・データ社(米国)、アラガン社(アイルランド)、アルコン社(スイス)、ファイザー社(米国)、バウシュ・ヘルス社(カナダ)、バイエル社(ドイツ)、ジェネンテック社(米国)、リジェネロン・ファーマシューティカルズ社(米国)、ノバルティス社(スイス)、武田薬品工業株式会社(日本)、参天製薬株式会社(日本) |

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Research がまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、患者の疫学、パイプライン分析、価格分析、規制の枠組みも含まれています。 |

無眼球症および小眼球症市場の定義

無眼症と小眼症は、片目または両目の発育不全または欠損を特徴とする先天性の眼疾患です。無眼症は、胎児の発育中に眼の形成がうまくいかなかったために、出生時に片目または両目が完全に欠損している状態を指します。一方、小眼症は、異常に小さく、発育不全の眼を伴い、ある程度の視力はあるものの、視力が大幅に低下していることが多いです。

無眼球症および小眼球症の市場動向

ドライバー

- 遺伝性疾患の増加

遺伝性疾患の増加は、無眼球症および小眼球症市場における医療ソリューションの需要を大幅に押し上げています。世界保健機関(WHO)の調査によると、遺伝性疾患はすべての先天性奇形の約6〜8%を占めており、そのうちのかなりの割合が無眼球症や小眼球症などの眼の異常に関係しています。遺伝子検査の進歩により遺伝性疾患の診断がより一般的になるにつれて、これらの眼疾患に罹患する人の数は増加し続けており、それによって専門的な治療と介入の必要性が高まっています。たとえば、無眼球症の発生率は、世界中で10,000〜18,000人に1人の割合で発生すると推定されていますが、小眼球症は5,000人に1人の割合で発生しています。この罹患率の増加により、早期診断、個別化治療、高度な補綴技術などの医療ソリューションの需要が高まり、市場の成長をさらに促進しています。遺伝性疾患の増加は、無眼球症および小眼球症市場の大きな推進力となり、継続的なイノベーションとヘルスケアソリューションの必要性を強調しています。

- 先天性眼疾患に関する認識の高まり

Growing awareness about congenital eye disorders such as anophthalmia and microphthalmia has significantly contributed to earlier diagnoses and improved treatment outcomes, thereby driving the demand for specialized medical care and therapies. Public health initiatives, patient advocacy groups, and increasing media attention have played crucial roles in educating both healthcare professionals and the general public about these rare conditions. As a result, parents and caregivers are more likely to seek early medical attention, enabling earlier interventions such as the fitting of prosthetic eyes or the use of advanced surgical techniques to improve the quality of life for affected children. For instance, organizations such as the Anophthalmia and Microphthalmia Children’s Foundation have been instrumental in raising awareness and providing resources for affected families. This heightened awareness facilitates timely medical intervention and fosters demand for more advanced treatments, including genetic testing, stem cell therapy, and customized prosthetics. Consequently, as diagnoses become more frequent and treatment options more effective, the market for anophthalmia and microphthalmia solutions continues to expand.

Opportunities

- Increasing Advancements in Diagnostic Technology

Advancements in diagnostic technology, particularly in genetic testing, imaging, and molecular diagnostics, have opened up significant market opportunities for the anophthalmia and microphthalmia market by enabling early and accurate identification of these conditions. Technologies such as high-resolution imaging and genetic screening tools now allow healthcare providers to detect congenital eye disorders in the early stages of pregnancy or shortly after birth, leading to timely interventions. For instance, non-invasive prenatal testing (NIPT) is becoming a valuable tool for detecting genetic mutations linked to these eye conditions, which allows parents to make informed decisions and pursue early treatment options. Moreover, the integration of molecular diagnostics in clinical settings enables precise identification of underlying genetic causes, facilitating personalized therapies. The rise of next-generation sequencing (NGS) techniques, which can analyze multiple genetic factors simultaneously, is further improving diagnostic accuracy. This evolution in diagnostic capabilities presents a market opportunity for the development of specialized diagnostic tools, early intervention strategies, and more effective treatments, thereby driving growth in the anophthalmia and microphthalmia market.

- Rising Healthcare Expenditure

Rising healthcare expenditure, particularly in both developed and emerging regions, is creating a significant market opportunity for the anophthalmia and microphthalmia market by providing better access to advanced diagnostic tools, treatments, and surgical procedures for patients. For instance, countries such as the U.S. and Germany, with their well-established healthcare systems, are investing heavily in medical technologies and research, enabling more precise and timely diagnoses, as well as more advanced treatment options, such as reconstructive surgery, prosthetics, and gene therapy. In addition, emerging economies such as China and India are increasing their healthcare spending, leading to improvements in medical infrastructure, which allows for the adoption of cutting-edge diagnostic and treatment methods for congenital eye disorders. The rise in healthcare spending also fuels the availability of specialized medical professionals and better access to support services for patients, thus improving overall care. This trend of increased investment in healthcare enhances patient outcomes and creates a growing demand for advanced solutions, representing a key market opportunity in the anophthalmia and microphthalmia sector.

Restraints/Challenges

- High Treatment and Surgical Costs

High treatment and surgical costs are a major challenge in the anophthalmia and microphthalmia market, as individuals with these conditions require specialized care that can be both complex and expensive. For instance, surgeries to reconstruct the eye socket, fit ocular prostheses, or correct associated deformities can cost thousands of dollars, especially when ongoing adjustments and follow-up care are necessary. A child with anophthalmia may require multiple surgeries over the course of their life to accommodate growth or improve the fit of their prosthetic eye. In addition, the cost of prosthetics themselves ranging from a few hundred to several thousand dollars per prosthesis can be a significant financial burden, especially for families without insurance coverage or in low-income regions. Long-term care, including rehabilitation, psychological support, and visual therapy, adds to the overall expenses. This high cost of treatment limits access to necessary care for many patients, particularly in developing countries, and presents a significant market challenge. As a result, there is a need for cost-effective solutions, improved insurance coverage, and financial support programs to ensure that these patients receive adequate care without incurring crippling expenses.

- Complexity of Treatment Protocols

The complexity of treatment protocols is a significant challenge in the anophthalmia and microphthalmia market, as each case requires highly individualized care tailored to the specific needs of the patient. These conditions often involve not just the eye and the surrounding tissues, requiring multidisciplinary treatment from pediatric ophthalmologists, plastic surgeons, prosthetists, and sometimes genetic counselors. For instance, a child with microphthalmia may need eye socket expansion surgery, followed by fitting a prosthetic eye, along with regular adjustments as they grow. In addition to addressing the physical aspects, these patients often require psychological support to deal with the emotional and social challenges associated with their condition, such as low self-esteem or bullying. Furthermore, some patients may experience associated health conditions such as hearing loss or developmental delays, necessitating a broader healthcare approach. Coordinating such complex care, often over many years, adds logistical and financial strain on healthcare systems, making it harder to deliver comprehensive, effective treatment. The fragmented nature of care and the need for specialized expertise increases the burden on healthcare providers and patients alike, presenting a key challenge to the growth and accessibility of treatments in this market.

This market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, Technological innovations in the market. To gain more info on the market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

Anophthalmia and Microphthalmia Market Scope

The market is segmented on the basis of diagnosis, treatment, and end users. The growth amongst these segments will help you analyse meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Diagnosis

- CT Scan

- MR Scan

- Chromosome Analysis

- Ultrasonography

Treatment

- Surgery

- Others

End Users

- Hospitals and Clinics

- Research Centers

- Others

Anophthalmia and Microphthalmia Market Regional Analysis

The market is analysed and market size insights and trends are provided by country, diagnosis, treatment, and end users as referenced above.

The countries covered in the market report are U.S., Canada and Mexico in North America, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Rest of Europe in Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), Saudi Arabia, U.A.E., South Africa, Egypt, Israel, Rest of Middle East and Africa (MEA) as a part of Middle East and Africa (MEA), Brazil, Argentina and Rest of South America as part of South America.

North America dominates the anophthalmia and microphthalmia market and is expected to maintain its dominant position throughout the forecast period. This growth is driven by the region's advanced healthcare technology and infrastructure, which enables better diagnosis and treatment options for these conditions. In addition, the rising prevalence of genetic disorders, along with an expanding patient pool, further fuels market demand. Furthermore, increased healthcare spending and strong government support for research and development (R&D) initiatives in North America contribute significantly to the ongoing growth and innovation in this market.

Asia-Pacific is expected to witness the highest growth rate in the anophthalmia and microphthalmia market during the forecast period. This is due to the rapid advancements in healthcare technology, which are enhancing the quality and accessibility of diagnostic and treatment options across the region. The vast patient population base, coupled with an increasing prevalence of genetic disorders, is further driving market growth. In addition, rising healthcare expenditure and improved government initiatives to support medical research and infrastructure are contributing to the region's expanding market potential.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points such as down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

Anophthalmia and Microphthalmia Market Share

市場競争環境では、競合他社ごとの詳細が提供されます。詳細には、会社概要、会社の財務状況、収益、市場の可能性、研究開発への投資、新しい市場への取り組み、世界的なプレゼンス、生産拠点と施設、生産能力、会社の強みと弱み、製品の発売、製品の幅と広さ、アプリケーションの優位性などが含まれます。提供される上記のデータ ポイントは、市場に関連する会社の焦点にのみ関連しています。

無眼球症および小眼球症の市場で活躍するリーダー企業は次のとおりです。

- ブリストル・マイヤーズ スクイブ社(米国)

- Nusapure Data(米国)

- アラガン(アイルランド)

- アルコン社(スイス)

- ファイザー社(米国)

- バウシュ・ヘルス・カンパニーズ(カナダ)

- バイエルAG(ドイツ)

- ジェネンテック社(米国)

- リジェネロン・ファーマシューティカルズ社(米国)

- ノバルティスAG(スイス)

- 武田薬品工業株式会社(日本)

- 参天製薬株式会社(日本)

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。