ヨーロッパの膀胱疾患市場

Market Size in USD Billion

CAGR :

%

USD

2,332.69 Million

USD

5,226.00 Million

2021

2029

USD

2,332.69 Million

USD

5,226.00 Million

2021

2029

| 2022 –2029 | |

| USD 2,332.69 Million | |

| USD 5,226.00 Million | |

| % | |

ヨーロッパの膀胱障害市場、タイプ別(膀胱炎、尿失禁、過活動膀胱、間質性膀胱炎、膀胱がん)、治療タイプ別(手術、薬物療法、非手術)、エンドユーザー別(病院、診療所、外来手術センター、その他)、流通チャネル別(直接、小売) - 2029年までの業界動向と予測。

ヨーロッパの膀胱疾患市場の分析と洞察

膀胱障害は、人間の日常生活に影響を及ぼす可能性のある障害のグループです。最も一般的な膀胱障害には、膀胱炎(膀胱が感染して炎症を起こす)、尿失禁(膀胱をコントロールできなくなる)、間質性膀胱炎(膀胱の痛みと頻尿、切迫した排尿)、過活動膀胱(膀胱が尿を絞り出す状態)などがあります。膀胱障害は生活の質に影響を及ぼし、その他の健康上の問題を引き起こす可能性があります。神経系や生活習慣の要因を含む健康の変化や問題は、男性と女性の UI の原因または一因となる可能性があります。

最も一般的な膀胱障害は、過活動膀胱と UI です。これらの問題は神経系に関連しています。神経は脳から膀胱に筋肉の収縮または弛緩を指示するメッセージを伝えます。

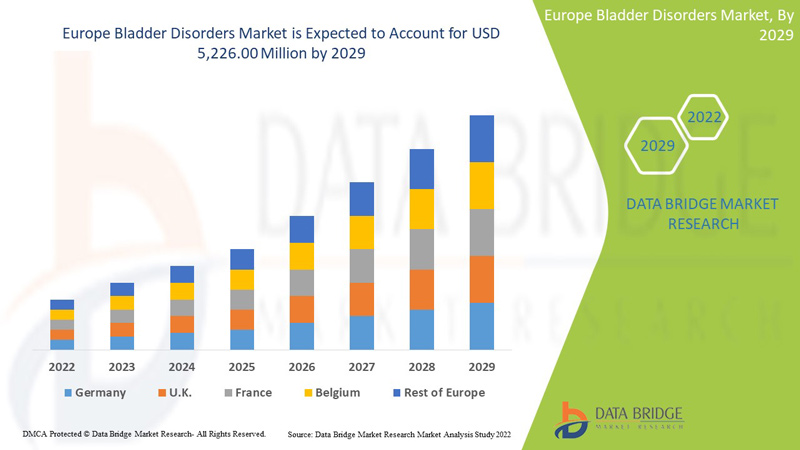

ヨーロッパの膀胱障害市場は、2022年から2029年の予測期間に成長すると予想されています。データブリッジマーケットリサーチは、市場は2022年から2029年の予測期間に10.7%のCAGRで成長し、2021年の23億3,269万米ドルから2029年には52億2,600万米ドルに達すると分析しています。

|

レポートメトリック |

詳細 |

|

予測期間 |

2022年から2029年 |

|

基準年 |

2021 |

|

歴史的な年 |

2020 (カスタマイズ可能 2019-2014) |

|

定量単位 |

収益(百万米ドル) |

|

対象セグメント |

タイプ別(膀胱炎、尿失禁、過活動膀胱、間質性膀胱炎、膀胱がん)、治療タイプ別(外科手術、薬物療法、非外科的治療)、エンドユーザー別(病院、診療所、外来手術センター、その他)、流通チャネル別(直接、小売) |

|

対象国 |

ドイツ、フランス、イギリス、イタリア、スペイン、オランダ、ロシア、スイス、トルコ、オーストリア、ノルウェー、ハンガリー、リトアニア、アイルランド、ポーランド、その他のヨーロッパ諸国 |

|

対象となる市場プレーヤー |

この市場で取引している主な企業としては、メドトロニック、ラボリー、ボストン・サイエンティフィック・コーポレーション、ファイザー社、アステラス製薬、杏林製薬株式会社(杏林製薬ホールディングス株式会社の子会社)、ブリストル・マイヤーズ スクイブ社、ジョンソン・エンド・ジョンソン・サービシズ社、アクソニクス社、メルク社、ビアトリス社、ブルー・ウィンド・メディカル、ゲイロード・ケミカル社、コロプラスト社、アッヴィ社、サン・ファーマシューティカル・インダストリーズ社、ザイダス・グループ、ウロバント・サイエンシズ社などがあります。 |

ヨーロッパの膀胱疾患市場の市場定義

膀胱関連の障害には、膀胱炎(感染症が原因となることが多い膀胱の炎症)、尿失禁(膀胱をコントロールできなくなる)、過活動膀胱(膀胱が不適切なタイミングで尿を排出する状態)、間質性膀胱炎(膀胱の痛みや頻尿、尿意切迫感、膀胱がんを引き起こす慢性的な問題)などがあります。

膀胱障害を診断するために、医師はレントゲン、尿検査、膀胱鏡と呼ばれるスコープによる膀胱壁検査など、さまざまな検査を行います。障害の治療は問題の原因によって異なり、薬物療法、手術(重症の場合)、非外科的処置が含まれます。

抗コリン薬は、過活動膀胱(OAB)症候群の薬物療法の第一選択薬です。OAB は、我慢できないほどの尿意切迫感を特徴とする臨床症状で、一般的に 1 日 8 回以上の排尿頻度は OAB とみなされます。抗コリン薬は、膀胱の収縮力を低下させる排尿筋のムスカリン受容体を阻害します。副作用を軽減するために、膀胱選択性が向上した徐放性製剤の新しい薬が開発されています。最近の薬のほとんどは、過活動膀胱の症状を軽減するのに同等の効果があります。

ヨーロッパの膀胱疾患市場の動向

ドライバー

-

市場参加者が採用した戦略的取り組み

膀胱障害は、日常の身体活動に影響を及ぼす可能性のあるさまざまな膀胱の問題です。最も一般的な膀胱障害は、膀胱炎、間質性膀胱炎、過活動膀胱、尿失禁、膀胱がんなどです。膀胱の問題のほとんどは、尿路に入り込んだ細菌感染によって引き起こされます。

市場プレーヤーによるコラボレーション、買収、パートナーシップなどのさまざまな戦略的取り組みにより、自社の製品ポートフォリオを拡大し、市場を拡大して顧客間の製品需要を高めることができ、最終的に市場プレーヤーは最大の収益を得ることができます。

-

高齢化人口の増加

加齢は、膀胱関連障害に関連する可能性のある強力なリスク要因です。加齢は、膀胱機能の神経学的、解剖学的、生化学的変化を促し、OAB の発症につながる可能性があります。過活動膀胱は、高齢者の間で最も一般的な問題です。高齢者は、膀胱に関連するさまざまな問題や障害に悩まされており、そのため、慢性的な健康管理サービスやソリューションの主なユーザーとなっています。

ノーベル研究によると、過活動膀胱の有病率は女性で約 16.9%、男性で約 16.0% で、OAB の有病率は加齢とともに増加しています。ただし、治療ガイドラインでは、第一、第二、第三の OAB 治療戦略として推奨されるものが規定されています。膀胱障害は認知症などの神経疾患と関連しており、この年齢層では、OAB は高齢者にとって非常に困難な問題です。過去数十年間、高齢者人口は世界中で急激に増加しています。

-

今後数年間の研究開発投資の増加と新しい治療法の導入

OAB やその他の膀胱疾患には、さまざまな治療オプションと革新的な治療法があります。多くのバイオ医薬品企業や製薬企業は、予測期間中に発売されると予想される膀胱疾患のさまざまな非従来型治療法に投資しています。

-

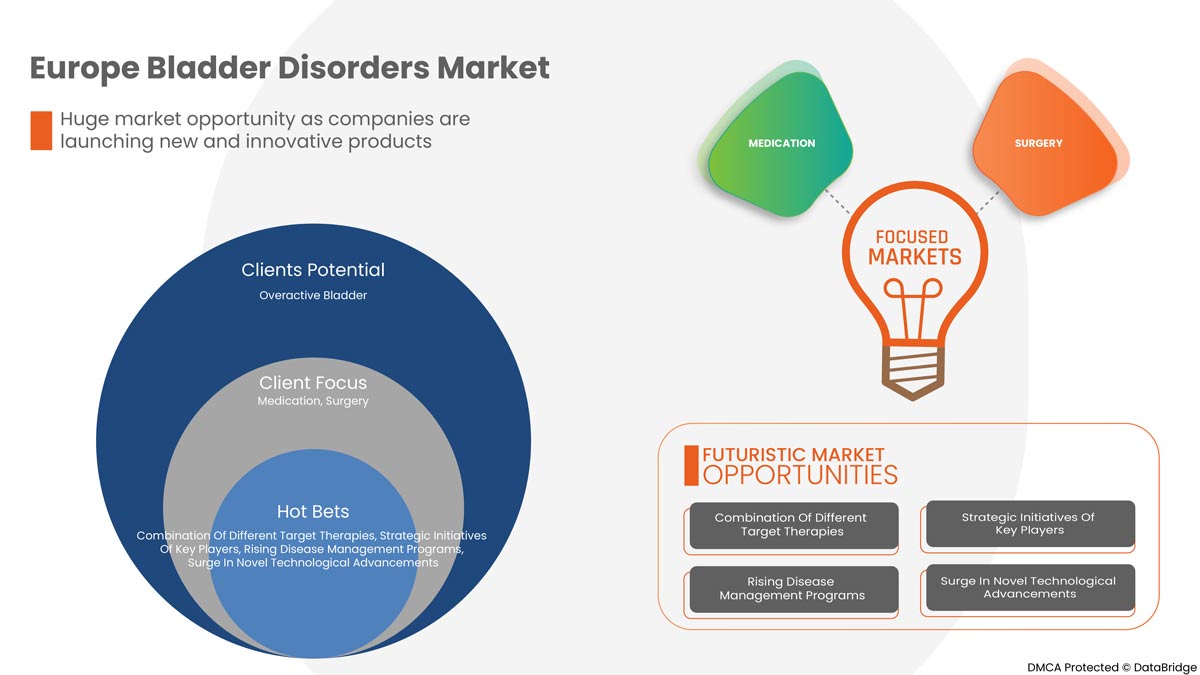

異なる標的療法の組み合わせ

併用療法は単独療法よりはるかに効果的で、副作用もありません。併用療法は、難治性膀胱疾患の患者にとって安全で効果的な代替療法です。さまざまな標的療法戦略を組み合わせることが、膀胱疾患の患者を緩和する最善の方法です。患者の難治性治療には、経口薬と行動療法を考慮する必要があります。仙骨神経調節、ボツリヌス毒素 A の排尿筋内注射、経皮的脛骨神経刺激など、さまざまな高度な標的療法が利用可能です。これらは高度な治療法であり、経口薬に比べて効果的です。

機会

-

新たな技術進歩の急増

慢性疾患は、世界中の発展途上国における主要な死亡原因の 1 つと考えられています。そのため、公衆衛生従事者の間では、慢性疾患の管理に関するヘルスケア管理の重要性が高まっています。

膀胱障害の管理では、現在、さまざまなセルフケアの選択肢と、病状について患者に説明し、前進するためのさまざまな相談サービスで患者を支援することに重点が置かれています。これらの療法は、患者が感情的なトラウマや不安を克服するのを助け、反防御メカニズムとして機能する可能性があります。

技術革新の進展により、医療機関は慢性膀胱疾患の管理に革新的なサービスやソリューションを模索できるようになりました。長期間入院する必要がないため、コストと患者数も削減されました。さらに、通院や入院回数が減るため、高齢者にとってこの開発は便利です。こうした好ましい側面を考慮して、多くの組織や企業が慢性疾患の管理における最新の技術を開発し、実装して患者の転帰を改善しています。

-

疾病管理プログラムの増加

膀胱関連の問題を抱える人は、通常、入院、医師の診察、処方薬など、より多くの医療サービスを必要とします。多くの慢性的な問題を抱えながら長生きする人の数が増え、医療費も増加しているため、より優れた医療計画が求められています。

疾病管理は、慢性疾患患者の治療費を削減しながらケアを改善しようとする戦略の 1 つです。疾病管理プログラムは、膀胱疾患などの特定の慢性疾患を持つ人々の健康を増進すると同時に、医療サービスの需要と、入院や緊急訪問などの回避可能な結果に伴う関連費用を削減することを目的としています。これらのプログラムには、慢性疾患管理サービスとソリューションに関する情報も含まれます。これらは、世界中で慢性疾患の有病率が上昇しているため、非常に人気が高まっています。政府とヘルスケア組織は、膀胱がん、間質性膀胱炎、過活動膀胱管理プログラムなど、複数の疾病管理プログラムを使用してこれらの慢性疾患を組織し、実施しています。疾病管理プログラムは、セルフケアの実践を大幅に改善し、病院への通院と入院期間を大幅に短縮できるため、人々の間でより多くの注目を集めています。

制約/課題

しかし、さまざまなチェックポイントの手順と、手順を実行するためのハイテク技術とモダリティのため、病気の診断の難しさと治療と診断のコストは高くなります。治療に使用される高度な技術デバイスのコストが高いため、手順のコストは一般的に高くなり、市場の成長を抑制すると予想されます。

この膀胱障害市場レポートは、最近の新しい開発、貿易規制、輸出入分析、生産分析、バリュー チェーンの最適化、市場シェア、国内および現地の市場プレーヤーの影響、新たな収益源の観点から見た機会の分析、市場規制の変更、戦略的市場成長分析、市場規模、カテゴリ市場の成長、アプリケーションのニッチと優位性、製品の承認、製品の発売、地理的拡大、市場における技術革新の詳細を提供します。ヨーロッパの膀胱障害市場に関する詳細情報を取得するには、アナリストの概要について Data Bridge Market Research にお問い合わせください。当社のチームは、市場の成長を達成するための情報に基づいた市場決定を行うお手伝いをします。

COVID-19後の欧州膀胱疾患市場への影響

COVID-19は市場にプラスの影響を与えています。パンデミック中のロックダウンと隔離は、病気の管理と服薬遵守を複雑にします。そのため、さまざまな治療薬の使用が世界中の人々の間で大幅に増加しています。したがって、パンデミックはこの市場にプラスの影響を与えています。

最近の開発

- 2月に、アッヴィは、5歳の小児患者の神経疾患に伴う排尿筋(膀胱筋)の過活動の治療薬として、米国FDAがボトックス®を承認したことを発表した。「ボトックス®は、抗コリン剤療法では治療がうまくいかない小児の神経性排尿筋過活動の治療薬として認可された初の神経毒です。」この承認により、同社の収益は増加するだろう。

欧州の膀胱疾患市場の範囲

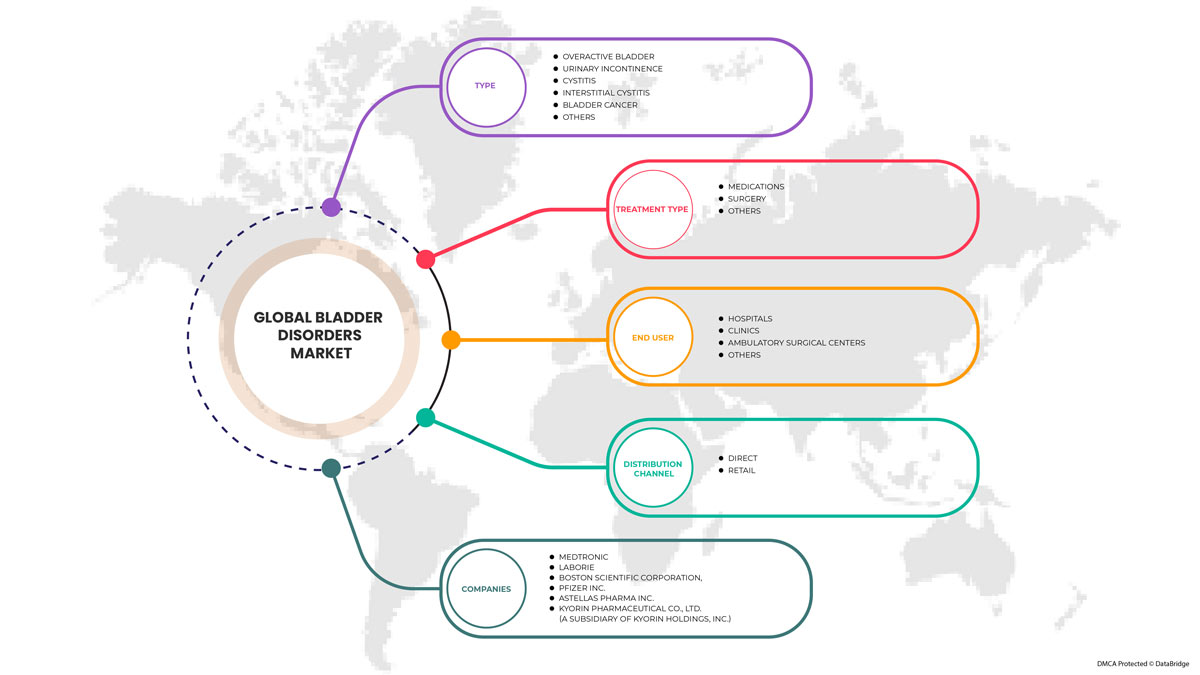

ヨーロッパの膀胱障害市場は、タイプ、治療タイプ、エンドユーザー、流通チャネルに細分化されています。これらのセグメントの成長は、業界のわずかな成長セグメントを分析し、コア市場アプリケーションを特定するための戦略的な決定を下すための貴重な市場概要と市場洞察をユーザーに提供するのに役立ちます。

タイプ

- 膀胱炎

- 尿失禁

- 過活動膀胱

- 間質性膀胱炎

- 膀胱がん

タイプ別に見ると、ヨーロッパの膀胱疾患市場は、膀胱炎、尿失禁、過活動膀胱、間質性膀胱炎、膀胱がんに分類されます。

治療の種類

- 手術

- 医薬品

- その他

製品に基づいて、ヨーロッパの膀胱障害市場は手術、薬物療法、その他に分類されます。

エンドユーザー

- 病院

- クリニック

- 外来手術センター

- その他

エンドユーザーに基づいて、ヨーロッパの膀胱障害市場は、病院、診療所、外来手術センター、その他に分類されます。

流通チャネル

- 直接

- 小売り

流通チャネルに基づいて、ヨーロッパの膀胱疾患市場は直接販売と小売販売に区分されます。

ヨーロッパの膀胱疾患市場の地域分析/洞察

ヨーロッパの膀胱疾患市場が分析され、上記のように国、タイプ、治療タイプ、エンドユーザー、流通チャネル別に市場規模の洞察と傾向が提供されます。

この市場に含まれる国は、ドイツ、英国、フランス、イタリア、スペイン、トルコ、ロシア、オランダ、スイス、ベルギー、その他のヨーロッパ諸国です。

ドイツは、市場シェアと収益の面でヨーロッパの膀胱疾患市場を支配しており、予測期間中もその優位性を維持し続けるでしょう。これは、この地域での過活動膀胱疾患の有病率の高さによるもので、研究開発投資の増加と新しい治療法の発売が市場を押し上げています。

レポートの国別セクションでは、市場の現在および将来の傾向に影響を与える個別の市場影響要因と市場規制の変更も提供しています。新規および交換販売、国の人口統計、疾病疫学、輸出入関税などのデータ ポイントは、個々の国の市場シナリオを予測するために使用される主要な指標の一部です。さらに、国別データの予測分析を提供する際には、ヨーロッパ ブランドの存在と可用性、地元および国内ブランドとの激しい競争により直面する課題、販売チャネルの影響が考慮されています。

競争環境と欧州の膀胱疾患市場シェア分析

ヨーロッパの膀胱障害市場の競争状況は、競合他社に関する詳細を提供します。詳細には、会社概要、会社の財務状況、収益、市場の可能性、研究開発への投資、新しい市場への取り組み、アジア太平洋地域でのプレゼンス、生産拠点と施設、生産能力、会社の強みと弱み、製品の発売、製品の幅と広さ、アプリケーションの優位性などが含まれます。上記のデータ ポイントは、ヨーロッパの膀胱障害市場への会社の重点にのみ関連しています。

ヨーロッパの膀胱疾患市場で活動している主要企業には、メドトロニック、ラボリー、ボストン・サイエンティフィック・コーポレーション、ファイザー社、アステラス製薬、杏林製薬株式会社(杏林製薬ホールディングス株式会社の子会社)、ブリストル・マイヤーズ スクイブ社、ジョンソン・エンド・ジョンソン・サービシズ社、アクソニクス社、メルク社、ビアトリス社、ブルー・ウィンド・メディカル、ゲイロード・ケミカル社、コロプラスト社、アッヴィ社、サン・ファーマシューティカル・インダストリーズ社、ザイダス・グループ、ウロバント・サイエンシズなどがある。

研究方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。市場データは、市場統計モデルとコヒーレント モデルを使用して分析および推定されます。さらに、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数の市場への影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、企業市場シェア分析、測定基準、ヨーロッパと地域、ベンダー シェア分析が含まれます。さらに質問がある場合は、アナリストへの電話をリクエストしてください。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

目次

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF EUROPE BLADDER DISORDERS MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 TYPE LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.2 PORTER'S FIVE FORCES

4.3 EUROPE BLADDER DISORDERS MARKET, PIPELINE ANALYSIS

5 EUROPE BLADDER DISORDER MARKET: REGULATIONS

5.1 THE U.S. REGULATORY FRAMEWORK FOR BLADDER DISOREDER MEDICATION

5.2 EUROPE REGULATORY FRAMEWORK FOR BLADDER DISORDER DRUGS

5.3 JAPAN REGULATORY GUIDANCE ON BLADDER DISORDER DRUGS

6 EUROPE BLADDER DISORDERS MARKET OVERVIEW

6.1 DRIVERS

6.1.1 STRATEGIC INITIATIVES ADOPTED BY MARKET PLAYERS

6.1.2 GROWING GERIATRIC POPULATION

6.1.3 RISING R&D INVESTMENTS AND LAUNCH OF NOVEL THERAPIES IN UPCOMING YEARS

6.1.4 COMBINATION OF DIFFERENT TARGET THERAPIES

6.2 RESTRAINTS

6.2.1 HIGH COST ASSOCIATED WITH BLADDER DISORDER DIAGNOSTIC TREATMENT

6.2.2 PRODUCTS RECALLS FROM MARKET

6.3 OPPORTUNITIES

6.3.1 SURGE IN NOVEL TECHNOLOGICAL ADVANCEMENTS

6.3.2 RISING DISEASE MANAGEMENT PROGRAMS

6.4 CHALLENGES

6.4.1 LACK OF AWARENESS ABOUT BLADDER DISORDERS RELATED PROBLEMS

6.4.2 PATENT EXPIRY OF DRUGS

7 EUROPE BLADDER DISORDERS MARKET, BY TYPE

7.1 OVERVIEW

7.2 OVERACTIVE BLADDER

7.3 URINARY INCONTINENCE

7.4 CYSTITIS

7.5 INTERSTITIAL CYSTITIS

7.6 BLADDER CANCER

7.7 OTHERS

8 EUROPE BLADDER DISORDERS MARKET, BY TREATMENT TYPE

8.1 OVERVIEW

8.2 MEDICATION

8.2.1 TOLTERODINE

8.2.2 MIRABEGRON

8.2.3 FESOTERODINE

8.2.4 OXYBUTYNIN

8.2.5 SOLIFENACIN

8.2.6 DARIFENACIN

8.2.7 TROSPIUM

8.2.8 OTHERS

8.3 SURGERY

8.3.1 SURGERY TO INCREASE BLADDER CAPACITY

8.3.2 BLADDER REMOVAL

8.3.3 OTHERS

8.4 OTHERS

9 EUROPE BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL

9.1 OVERVIEW

9.2 DIRECT

9.3 RETAIL

10 EUROPE BLADDER DISORDERS MARKET, BY END USER

10.1 OVERVIEW

10.2 HOSPITALS

10.3 CLINICS

10.4 AMBULATORY SURGICAL CENTERS

10.5 OTHERS

11 EUROPE BLADDER DISORDERS MARKET, BY GEOGRAPHY

11.1 EUROPE

11.1.1 GERMANY

11.1.2 U.K.

11.1.3 FRANCE

11.1.4 ITALY

11.1.5 SPAIN

11.1.6 TURKEY

11.1.7 RUSSIA

11.1.8 NETHERLANDS

11.1.9 SWITZERLAND

11.1.10 BELGIUM

11.1.11 REST OF EUROPE

12 EUROPE BLADDER DISORDERS MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: EUROPE

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 MERCK AND CO. INC. (2021)

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENT

14.2 ASTELLAS PHARMA INC. (2021)

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENTS

14.3 BRISTOL-MYERS SQUIBB COMPANY (2021)

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENT

14.4 BOSTON SCIENTIFIC CORPORATION (2021)

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENT

14.5 VIATRIS INC. (2021)

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT PORTFOLIO

14.5.5 RECENT DEVELOPMENT

14.6 ABBVIE (2021)

14.6.1 COMPANY SNAPSHOT

14.6.2 REVENUE ANALYSIS

14.6.3 PRODUCT PORTFOLIO

14.6.4 RECENT DEVELOPMENT

14.7 AXONICS, INC. (2021)

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCT PORTFOLIO

14.7.4 RECENT DEVELOPMENT

14.8 BLUE WIND MEDICAL (2021)

14.8.1 COMPANY SNAPSHOT

14.8.2 PRODUCT PORTFOLIO

14.8.3 RECENT DEVELOPMENT

14.9 COLOPLAST CORP. (2021)

14.9.1 COMPANY SNAPSHOT

14.9.2 REVENUE ANALYSIS

14.9.3 PRODUCT PORTFOLIO

14.1 GAYLORD CHEMICAL COMPANY, LLC (2021)

14.10.1 COMPANY SNAPSHOT

14.10.2 PRODUCT PORTFOLIO

14.10.3 RECENT DEVELOPMENT

14.11 JOHNSON & JOHNSON SERVICES, INC. (2021)

14.11.1 COMPANY SNAPSHOT

14.11.2 REVENUE ANALYSIS

14.11.3 PRODUCT PORTFOLIO

14.11.4 RECENT DEVELOPMENT

14.12 KYORIN PHARMACEUTICAL CO., LTD. (A SUBSIDIARY OF KYORIN HOLDINGS, INC.) (2021)

14.12.1 COMPANY SNAPSHOT

14.12.2 PRODUCT PORTFOLIO

14.12.3 RECENT DEVELOPMENTS

14.13 LABORIE (2021)

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCT PORTFOLIO

14.13.3 RECENT DEVELOPMENT

14.14 MEDTRONIC (2021)

14.14.1 COMPANY SNAPSHOT

14.14.2 REVENUE ANALYSIS

14.14.3 PRODUCT PORTFOLIO

14.14.4 RECENT DEVELOPMENTS

14.15 PFIZER INC. (2021)

14.15.1 COMPANY SNAPSHOT

14.15.2 REVENUE ANALYSIS

14.15.3 PRODUCT PORTFOLIO

14.15.4 RECENT DEVELOPMENTS

14.16 VALENCIA TECHNOLOGIES (2021)

14.16.1 COMPANY SNAPSHOT

14.16.2 PRODUCT PORTFOLIO

14.16.3 RECENT DEVELOPMENT

14.17 SUN PHAMACEUTICAL INDUSTRIES LTD. (2021)

14.17.1 COMPANY SNAPSHOT

14.17.2 REVENUE ANALYSIS

14.17.3 PRODUCT PORTFOLIO

14.17.4 RECENT DEVELOPMENT

14.18 SWATI SPENTOSE (2021)

14.18.1 COMPANY SNAPSHOT

14.18.2 PRODUCT PORTFOLIO

14.18.3 RECENT DEVELOPMENT

14.19 UROVANT SCIENCES (2021)

14.19.1 COMPANY SNAPSHOT

14.19.2 PRODUCT PORTFOLIO

14.19.3 RECENT DEVELOPMENT

14.2 ZYDUS GROUP (2021)

14.20.1 COMPANY SNAPSHOT

14.20.2 PRODUCT PORTFOLIO

14.20.3 RECENT DEVELOPMENT

15 QUESTIONNAIRE

16 RELATED REPORTS

表のリスト

TABLE 1 EUROPE BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 2 EUROPE OVERACTIVE BLADDER IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 3 EUROPE URINARY INCONTINENCE IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 4 EUROPE CYSTITIS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 5 EUROPE INTERSTITIAL CYSTITIS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 6 EUROPE BLADDER CANCER IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 7 EUROPE OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 8 EUROPE BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 9 EUROPE MEDICATION IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 10 EUROPE MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 11 EUROPE SURGERY IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 12 EUROPE SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 13 EUROPE OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 14 EUROPE BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 15 EUROPE DIRECT IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 16 EUROPE RETAIL IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 17 EUROPE BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 18 EUROPE HOSPITALS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 19 EUROPE CLINICS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 20 EUROPE AMBULATORY SURGICAL CENTERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 21 EUROPE OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 22 EUROPE BLADDER DISORDERS MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 23 EUROPE BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 24 EUROPE BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 25 EUROPE MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 26 EUROPE SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 27 EUROPE BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 28 EUROPE BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 29 GERMANY BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 30 GERMANY BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 31 GERMANY MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 32 GERMANY SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 33 GERMANY BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 34 GERMANY BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 35 U.K. BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 36 U.K. BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 37 U.K. MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 38 U.K. SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 39 U.K. BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 40 U.K. BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 41 FRANCE BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 42 FRANCE BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 43 FRANCE MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 44 FRANCE SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 45 FRANCE BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 46 FRANCE BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 47 ITALY BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 48 ITALY BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 49 ITALY MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 50 ITALY SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 51 ITALY BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 52 ITALY BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 53 SPAIN BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 54 SPAIN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 55 SPAIN MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 56 SPAIN. SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 57 SPAIN BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 58 SPAIN BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 59 TURKEY BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 60 TURKEY BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 61 TURKEY MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 62 TURKEY SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 63 TURKEY BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 64 TURKEY BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 65 RUSSIA BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 66 RUSSIA BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 67 RUSSIA MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 68 RUSSIA SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 69 RUSSIA BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 70 RUSSIA BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 71 NETHERLANDS BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 72 NETHERLANDS BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 73 NETHERLANDS MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 74 NETHERLANDS SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 75 NETHERLANDS BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 76 NETHERLANDS BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 77 SWITZERLAND BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 78 SWITZERLAND BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 79 SWITZERLAND MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 80 SWITZERLAND SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 81 SWITZERLAND BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 82 SWITZERLAND BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 83 BELGIUM BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 84 BELGIUM BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 85 BELGIUM MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 86 BELGIUM SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 87 BELGIUM BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 88 BELGIUM BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 89 REST OF EUROPE BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

図表一覧

FIGURE 1 EUROPE BLADDER DISORDERS MARKET: SEGMENTATION

FIGURE 2 EUROPE BLADDER DISORDERS MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE BLADDER DISORDERS MARKET: DROC ANALYSIS

FIGURE 4 EUROPE BLADDER DISORDERS MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE BLADDER DISORDERS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE BLADDER DISORDERS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE BLADDER DISORDERS MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE BLADDER DISORDERS MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 EUROPE BLADDER DISORDERS MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 EUROPE BLADDER DISORDERS MARKET: SEGMENTATION

FIGURE 11 RISING EPIDEMIC AND PANDEMIC OUTBREAK AND INCREASING PREVALENCE OF BLADDER DISORDERS EXPECTED TO DRIVE THE EUROPE BLADDER DISORDERS MARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 12 OVERACTIVE BLADDER SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE BLADDER DISORDERS MARKET IN 2022 & 2029

FIGURE 13 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE EUROPE BLADDER DISORDER MARKET

FIGURE 14 EUROPE BLADDER DISORDERS MARKET: BY TYPE, 2021

FIGURE 15 EUROPE BLADDER DISORDERS MARKET: BY TYPE, 2022-2029 (USD MILLION)

FIGURE 16 EUROPE BLADDER DISORDERS MARKET: BY TYPE, CAGR (2022-2029)

FIGURE 17 EUROPE BLADDER DISORDERS MARKET: BY TYPE, LIFELINE CURVE

FIGURE 18 EUROPE BLADDER DISORDERS MARKET: BY TREATMENT TYPE, 2021

FIGURE 19 EUROPE BLADDER DISORDERS MARKET: BY TREATMENT TYPE, 2022-2029 (USD MILLION)

FIGURE 20 EUROPE BLADDER DISORDERS MARKET: BY TREATMENT TYPE, CAGR (2022-2029)

FIGURE 21 EUROPE BLADDER DISORDERS MARKET: BY TREATMENT TYPE, LIFELINE CURVE

FIGURE 22 EUROPE BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, 2021

FIGURE 23 EUROPE BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, 2022-2029 (USD MILLION)

FIGURE 24 EUROPE BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, CAGR (2022-2029)

FIGURE 25 EUROPE BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, LIFELINE CURVE

FIGURE 26 EUROPE BLADDER DISORDERS MARKET: BY END USER, 2021

FIGURE 27 EUROPE BLADDER DISORDERS MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 28 EUROPE BLADDER DISORDERS MARKET: BY END USER, CAGR (2022-2029)

FIGURE 29 EUROPE BLADDER DISORDERS MARKET: BY END USER, LIFELINE CURVE

FIGURE 30 EUROPE BLADDER DISORDERS MARKET: SNAPSHOT (2021)

FIGURE 31 EUROPE BLADDER DISORDERS MARKET: BY COUNTRY (2021)

FIGURE 32 EUROPE BLADDER DISORDERS MARKET: BY COUNTRY (2022 & 2029)

FIGURE 33 EUROPE BLADDER DISORDERS MARKET: BY COUNTRY (2021 & 2029)

FIGURE 34 EUROPE BLADDER DISORDERS MARKET: BY TYPE (2022-2029)

FIGURE 35 EUROPE BLADDER DISORDERS MARKET: COMPANY SHARE 2021 (%)

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。