Global Afterburner Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

165.85 Million

USD

318.53 Million

2025

2033

USD

165.85 Million

USD

318.53 Million

2025

2033

| 2026 –2033 | |

| USD 165.85 Million | |

| USD 318.53 Million | |

| % | |

|

Global Afterburner Market Segmentation, By Type (Turbofans Engine and Turbojet Engine), Plane Type (Air Superiority Fighter, Interceptor Aircraft and Light Fighter)- Industry Trends and Forecast to 2033

Afterburner Market Size

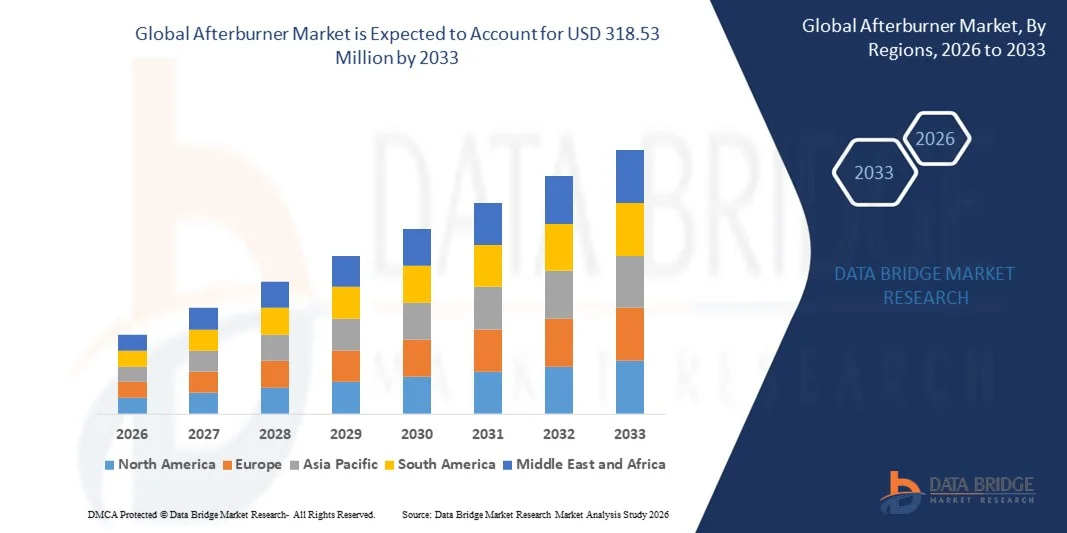

- The global afterburner market size was valued at USD 165.85 million in 2025 and is expected to reach USD 318.53 million by 2033, at a CAGR of 8.50% during the forecast period

- • The market growth is largely fuelled by increasingly stringent emission regulations across industrial sectors, rising adoption of thermal oxidation systems for air pollution control, and growing focus on reducing volatile organic compound and hazardous air pollutant emissions

- Expanding applications in chemical processing, pharmaceuticals, food processing, and automotive manufacturing are supporting sustained demand for advanced afterburner solutions

Afterburner Market Analysis

- The afterburner market is characterised by steady demand driven by regulatory compliance requirements and the need for effective emission control technologies across multiple end-use industries

- Manufacturers are focusing on innovation in design, integration with heat recovery systems, and optimisation of fuel consumption to enhance overall system performance and cost efficiency

- North America dominated the global afterburner market with the largest revenue share in 2025, driven by strict environmental regulations, strong enforcement of air quality standards, and the presence of advanced industrial infrastructure

- Asia-Pacific region is expected to witness the highest growth rate in the global afterburner market, driven by rising military modernization programs, increasing procurement of advanced combat aircraft, and growing investments in aerospace infrastructure across emerging economies

- The turbofan engine segment held the largest market revenue share in 2025 driven by its widespread use in modern military aircraft and its ability to deliver higher thrust efficiency with comparatively better fuel economy. Turbofan afterburners are widely adopted in advanced fighter jets as they support supersonic flight, enhanced combat performance, and improved mission flexibility, making them a preferred choice for air forces globally

Report Scope and Afterburner Market Segmentation

|

Attributes |

Afterburner Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Afterburner Market Trends

Rising Focus on Industrial Emission Control and Environmental Compliance

- The increasing emphasis on reducing harmful industrial emissions is significantly shaping the global afterburner market, as industries face stricter air pollution control regulations and environmental standards. Afterburner systems are gaining wider adoption due to their effectiveness in oxidizing volatile organic compounds, hazardous air pollutants, and odorous gases generated during industrial processes. This trend is strengthening demand across chemical processing, pharmaceuticals, food processing, and automotive manufacturing, encouraging manufacturers to develop high-efficiency and compliant solutions

- Growing awareness around environmental sustainability and corporate responsibility has accelerated the adoption of afterburners in industrial facilities aiming to minimize environmental impact. Industries are increasingly investing in advanced emission control technologies to meet compliance requirements while maintaining operational efficiency. This has led to higher demand for afterburners integrated with thermal oxidizers and air pollution control systems, supporting long-term market growth

- Regulatory compliance and sustainability goals are influencing capital investment decisions, with manufacturers prioritizing systems that ensure consistent emission reduction and regulatory adherence. Companies are emphasizing system reliability, low maintenance requirements, and energy efficiency to enhance overall value propositions. These factors are also driving the adoption of modern afterburner technologies with improved combustion efficiency and reduced fuel consumption

- For instance, in 2024, industrial facilities in Germany and the U.S. across chemical and automotive manufacturing sectors upgraded emission control systems by installing advanced afterburners to comply with updated emission norms. These installations supported improved regulatory compliance and operational safety while reinforcing environmental commitments. The systems were widely adopted across large-scale production units and specialized manufacturing plants

- While demand for afterburners is increasing, sustained market growth depends on technological innovation, cost-effective system integration, and energy optimization. Manufacturers are focusing on developing solutions that balance performance, operational costs, and environmental benefits to support wider adoption across diverse industrial applications

Afterburner Market Dynamics

Driver

Stringent Environmental Regulations and Industrial Emission Standards

- Increasingly strict environmental regulations aimed at controlling industrial air pollution are a major driver for the global afterburner market. Regulatory bodies are enforcing limits on volatile organic compounds and hazardous air pollutants, prompting industries to adopt efficient emission control systems. Afterburners play a critical role in meeting these requirements by ensuring effective thermal oxidation of harmful gases

- Expanding industrial activities in sectors such as chemicals, pharmaceuticals, automotive manufacturing, and food processing are contributing to higher emission levels, thereby increasing demand for afterburner systems. These systems help maintain compliance while supporting uninterrupted production, making them essential components of industrial pollution control infrastructure

- Industrial operators are actively investing in afterburner-based solutions to avoid regulatory penalties and improve environmental performance. These investments are supported by government initiatives promoting cleaner production practices and the adoption of advanced emission reduction technologies. Partnerships between system manufacturers and industrial operators are also increasing to deliver customized and compliant solutions

- For instance, in 2023, manufacturing plants operated by BASF in Germany and Dow in the U.S. expanded their use of afterburner systems within chemical processing units to comply with tightening emission standards. These installations supported continuous operations while improving air quality compliance and strengthening sustainability commitments

- Although regulatory pressure continues to drive market growth, long-term expansion depends on improving system efficiency, reducing fuel consumption, and integrating afterburners with heat recovery technologies. Ongoing investment in innovation and system optimization will remain essential for maintaining compliance and cost efficiency

Restraint/Challenge

High Installation Costs and Energy Consumption Requirements

- The relatively high capital investment required for installing afterburner systems remains a key challenge, particularly for small and medium-sized industrial facilities. Equipment costs, integration with existing systems, and installation complexity contribute to higher upfront expenditure, limiting adoption among cost-sensitive operators

- Energy consumption associated with afterburner operation is another challenge, as maintaining high combustion temperatures can increase operational costs. Industries with tight energy budgets may hesitate to adopt or upgrade afterburner systems, especially when alternative emission control technologies appear more cost-effective in the short term

- Maintenance requirements and system downtime can also affect adoption, as afterburners require regular inspection and servicing to ensure optimal performance and compliance. Unplanned shutdowns or inefficiencies can disrupt industrial operations and increase total cost of ownership

- For instance, in 2024, small-scale manufacturers in Southeast Asia reported slower adoption of afterburner systems due to high installation costs and increased fuel consumption compared to alternative emission control solutions. Energy price volatility and limited access to technical expertise further constrained adoption across cost-sensitive industries

- Addressing these challenges will require the development of energy-efficient afterburner designs, integration with waste heat recovery systems, and flexible financing options. Improving system efficiency and reducing operational costs will be critical for expanding adoption and supporting sustainable growth in the global afterburner market

Afterburner Market Scope

The market is segmented on the basis of type and plane type.

- By Type

On the basis of type, the global afterburner market is segmented into turbofan engine and turbojet engine. The turbofan engine segment held the largest market revenue share in 2025 driven by its widespread use in modern military aircraft and its ability to deliver higher thrust efficiency with comparatively better fuel economy. Turbofan afterburners are widely adopted in advanced fighter jets as they support supersonic flight, enhanced combat performance, and improved mission flexibility, making them a preferred choice for air forces globally.

The turbojet engine segment is expected to witness steady growth from 2026 to 2033, driven by its continued application in legacy aircraft, interceptor platforms, and specialized military programs. Turbojet afterburners are valued for their high thrust-to-weight ratio and simple design, which makes them suitable for short-duration high-speed missions. Ongoing modernization and maintenance of existing fleets are supporting the sustained demand for turbojet engine afterburners.

- By Plane Type

On the basis of plane type, the global afterburner market is segmented into air superiority fighter, interceptor aircraft, and light fighter. The air superiority fighter segment accounted for the largest market share in 2025 due to the high reliance on afterburners for achieving superior speed, maneuverability, and combat dominance during aerial missions. These aircraft require advanced propulsion systems with afterburners to maintain tactical advantages in modern warfare.

The interceptor aircraft and light fighter segments is expected to witness steady growth from 2026 to 2033, supported by increasing investments in air defense capabilities and the development of cost-effective combat aircraft. Interceptor aircraft rely on afterburners for rapid acceleration and quick response to aerial threats, while light fighters utilize afterburners to enhance performance without significantly increasing operational complexity, contributing to their adoption among emerging and mid-sized air forces.

Afterburner Market Regional Analysis

- North America dominated the global afterburner market with the largest revenue share in 2025, driven by strict environmental regulations, strong enforcement of air quality standards, and the presence of advanced industrial infrastructure

- Industries in the region place high importance on emission control compliance, operational safety, and sustainable manufacturing practices, leading to increased adoption of afterburner systems across chemical, pharmaceutical, automotive, and food processing sectors

- This widespread adoption is further supported by high industrial investments, continuous upgrades of emission control equipment, and growing awareness of environmental responsibility, establishing afterburners as a critical solution for industrial air pollution control

U.S. Afterburner Market Insight

The U.S. afterburner market captured the largest revenue share in 2025 within North America, fueled by stringent emission norms set by environmental regulatory agencies and the strong presence of large-scale manufacturing industries. Industrial operators are increasingly investing in afterburner systems to ensure compliance with volatile organic compound and hazardous air pollutant regulations. The focus on upgrading aging industrial infrastructure, coupled with rising adoption of advanced thermal oxidation systems, continues to support market growth in the country.

Europe Afterburner Market Insight

The Europe afterburner market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by tightening environmental regulations and aggressive climate targets across the region. Increasing industrial emphasis on reducing carbon footprint and improving emission efficiency is fostering the adoption of afterburner systems. Growth is supported by widespread implementation across chemical processing, pharmaceuticals, and specialty manufacturing industries, as well as strong investments in sustainable industrial technologies.

U.K. Afterburner Market Insight

The U.K. afterburner market is expected to witness steady growth from 2026 to 2033, driven by increasing regulatory scrutiny on industrial emissions and rising investments in cleaner production technologies. Manufacturing facilities are adopting afterburner systems to meet emission compliance requirements while improving operational efficiency. The country’s focus on sustainability initiatives and industrial modernization is further encouraging the deployment of advanced emission control solutions.

Germany Afterburner Market Insight

The Germany afterburner market is expected to witness strong growth from 2026 to 2033, fueled by the country’s robust industrial base and strong emphasis on environmental protection and energy efficiency. Germany’s advanced manufacturing sector, particularly in chemicals and automotive production, is driving demand for high-performance afterburner systems. The integration of afterburners with energy-efficient and heat recovery technologies aligns well with Germany’s sustainability and innovation-driven industrial approach.

Asia-Pacific Afterburner Market Insight

The Asia-Pacific afterburner market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, expanding manufacturing activities, and tightening emission regulations across emerging economies. Rising awareness of air pollution control and increasing investments in industrial infrastructure are accelerating afterburner adoption. The region’s growth is further supported by the expansion of chemical, pharmaceutical, and food processing industries.

Japan Afterburner Market Insight

The Japan afterburner market is expected to witness steady growth from 2026 to 2033 due to the country’s advanced manufacturing capabilities and strong regulatory framework for environmental protection. Japanese industries emphasize high-efficiency and reliable emission control systems, driving the adoption of technologically advanced afterburners. Integration with precision-controlled industrial processes and a strong focus on operational safety are key factors supporting market expansion.

China Afterburner Market Insight

The China afterburner market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid industrial expansion, rising environmental concerns, and stricter enforcement of emission control policies. China’s large-scale chemical and manufacturing sectors are increasingly adopting afterburner systems to comply with national air quality standards. Government initiatives targeting pollution reduction, along with growing investments in industrial emission control infrastructure, continue to propel the market in China.

Afterburner Market Share

The Afterburner industry is primarily led by well-established companies, including:

- Rolls-Royce plc (U.K.)

- GE Aviation (U.S.)

- Raytheon Technologies Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- SE Ivchenko-Progress (Ukraine)

- Aviadvigatel (Russia)

- Safran (France)

- EuroJet Turbo GmbH (Germany)

- JSC “Klimov” — United Engine Corporation (Russia)

- MTU Aero Engines AG (Germany)

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。