Europe Bladder Disorders Market

Taille du marché en milliards USD

TCAC :

%

USD

2,332.69 Million

USD

5,226.00 Million

2021

2029

USD

2,332.69 Million

USD

5,226.00 Million

2021

2029

| 2022 –2029 | |

| USD 2,332.69 Million | |

| USD 5,226.00 Million | |

| % | |

Marché européen des troubles de la vessie, par type (cystite, incontinence urinaire, vessie hyperactive, cystite interstitielle , cancer de la vessie), type de traitement (chirurgie, médicament, non chirurgical), utilisateur final (hôpitaux, cliniques, centres de chirurgie ambulatoire, autres), canal de distribution (direct, vente au détail) - Tendances et prévisions de l'industrie jusqu'en 2029.

Analyse et perspectives du marché des troubles de la vessie en Europe

Les troubles de la vessie sont un groupe de troubles qui peuvent affecter les activités quotidiennes de la vie humaine. Certains des troubles de la vessie les plus courants sont la cystite, dans laquelle la vessie est infectée et provoque une inflammation. L'incontinence urinaire, dans laquelle la vessie est perdue, la cystite interstitielle, dans laquelle la vessie se met à uriner fréquemment et impérativement, et la vessie hyperactive , dans laquelle la vessie comprime l'urine. Les troubles de la vessie peuvent affecter la qualité de vie et causer d'autres problèmes de santé. Les changements et problèmes de santé, notamment les facteurs liés au système nerveux et au mode de vie, peuvent provoquer ou contribuer à l'IU chez les hommes et les femmes.

Les troubles de la vessie les plus courants sont l'hyperactivité vésicale et l'incontinence urinaire. Ces problèmes sont associés au système nerveux. Les nerfs transmettent des messages du cerveau à la vessie, indiquant que les muscles se contractent ou se relâchent.

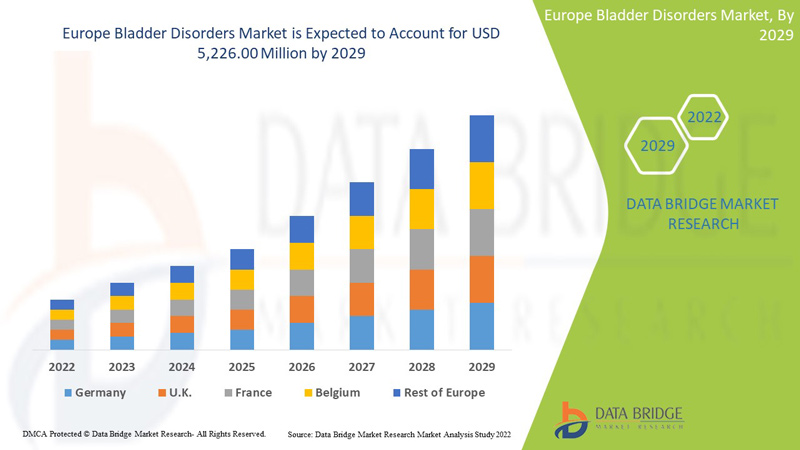

Le marché européen des troubles de la vessie devrait croître au cours de la période de prévision de 2022 à 2029. Data Bridge Market Research analyse que le marché croît avec un TCAC de 10,7 % au cours de la période de prévision de 2022 à 2029 et devrait atteindre 5 226,00 millions USD d'ici 2029 contre 2 332,69 millions USD en 2021.

|

Rapport métrique |

Détails |

|

Période de prévision |

2022 à 2029 |

|

Année de base |

2021 |

|

Années historiques |

2020 (Personnalisable 2019-2014) |

|

Unités quantitatives |

Chiffre d'affaires en millions USD |

|

Segments couverts |

Par type (cystite, incontinence urinaire, vessie hyperactive, cystite interstitielle, cancer de la vessie), type de traitement (chirurgie, médicament, non chirurgical), utilisateur final (hôpitaux, cliniques, centres de chirurgie ambulatoire, autres), canal de distribution (direct, vente au détail) |

|

Pays couverts |

Allemagne, France, Royaume-Uni, Italie, Espagne, Pays-Bas, Russie, Suisse, Turquie, Autriche, Norvège, Hongrie, Lituanie, Irlande, Pologne, Reste de l'Europe |

|

Acteurs du marché couverts |

Les principales entreprises présentes sur le marché sont Medtronic, Laborie, Boston Scientific Corporation, Pfizer Inc., Astellas Pharma Inc., KYORIN Pharmaceutical Co., Ltd. (Une filiale de KYORIN Holdings, Inc.), Bristol-Myers Squibb Company, Johnson & Johnson Services, Inc., Axonics, Inc., Merck & Co., Inc., Viatris Inc., Blue Wind Medical, Gaylord Chemical Company, LLC, Coloplast Corp, AbbVie Inc., Sun Pharmaceutical Industries Ltd., Zydus Group, Urovant Sciences entre autres. |

Définition du marché des troubles de la vessie en Europe

Les troubles liés à la vessie comprennent la cystite (inflammation de la vessie, souvent due à une infection), l'incontinence urinaire (perte de contrôle de la vessie), l'hyperactivité vésicale (une condition dans laquelle la vessie expulse l'urine au mauvais moment), la cystite interstitielle (un problème chronique qui provoque des douleurs à la vessie et des mictions fréquentes et urgentes) et le cancer de la vessie.

Différents tests sont effectués par les médecins pour diagnostiquer le trouble de la vessie, notamment des radiographies, des analyses d'urine et un examen de la paroi de la vessie à l'aide d'un appareil appelé cystoscope. Le traitement du trouble dépend de la cause du problème et comprend des médicaments, des interventions chirurgicales (dans les cas graves) et des procédures non chirurgicales.

Les médicaments anticholinergiques constituent la première ligne de traitement pharmacologique du syndrome de la vessie hyperactive (VHA). La VHA est un symptôme clinique caractérisé par une envie impérieuse d'uriner, qui est difficile à différer. En général, une fréquence d'uriner supérieure à huit fois par jour est considérée comme une VHA. Les médicaments anticholinergiques inhibent les récepteurs muscariniques du muscle détrusor qui réduisent la contractilité de la vessie. Pour réduire les effets secondaires, de nouveaux médicaments avec une sélectivité vésicale améliorée et des formulations à libération prolongée sont en cours de développement. La majorité des médicaments les plus récents sont tout aussi efficaces pour réduire les symptômes d'une vessie hyperactive.

Dynamique du marché des troubles de la vessie en Europe

Conducteurs

-

INITIATIVES STRATÉGIQUES ADOPTÉES PAR LES ACTEURS DU MARCHÉ

Les troubles de la vessie sont un ensemble de problèmes de vessie qui peuvent affecter les activités physiques quotidiennes. Les troubles de la vessie les plus courants sont la cystite, la cystite interstitielle, l'hyperactivité vésicale, l'incontinence urinaire et le cancer de la vessie. La plupart des problèmes de vessie sont causés par une infection bactérienne qui pénètre dans les voies urinaires.

Diverses initiatives stratégiques des acteurs du marché en termes de collaboration, d'acquisition, de partenariat et autres, leur permettent d'augmenter le portefeuille de produits de leur entreprise, conduisant à l'expansion du marché et donc à l'amélioration de la demande de produits parmi les clients, ce qui permet finalement aux acteurs du marché de gagner un maximum de revenus.

-

POPULATION GÉRIATRIQUE CROISSANTE

Le vieillissement est un facteur de risque important qui peut être associé aux troubles liés à la vessie. Le vieillissement entraîne des changements neurologiques, anatomiques et biochimiques dans la fonction de la vessie, qui peuvent favoriser le développement de l'HVV. L'hyperactivité vésicale est le problème le plus courant chez la population gériatrique. La population vieillissante souffre de divers problèmes et troubles associés à la vessie, en raison desquels elle est la principale utilisatrice de services et de solutions de gestion de la santé chronique.

Selon l'étude Noble, le taux de prévalence de la vessie hyperactive est d'environ 16,9 chez les femmes et les hommes, soit environ 16,0 %, et la prévalence de l'HVV augmente avec l'âge. Cependant, les directives de traitement précisent les stratégies thérapeutiques préférées de première, deuxième et troisième intention pour l'HVV. Les troubles de la vessie sont associés à des troubles neurologiques tels que la démence, et dans ce groupe d'âge, l'HVV est un véritable défi pour la population âgée. Au cours des dernières décennies, la population âgée a connu une croissance spectaculaire dans le monde entier.

-

AUGMENTATION DES INVESTISSEMENTS EN R&D ET LANCEMENT DE NOUVELLES THÉRAPIES DANS LES ANNÉES À VENIR

Il existe plusieurs options de traitement et thérapies innovantes pour l'HVV et d'autres troubles de la vessie. De nombreuses sociétés biopharmaceutiques et pharmaceutiques investissent dans diverses thérapies non conventionnelles pour les troubles de la vessie, qui devraient être lancées au cours de la période de prévision.

-

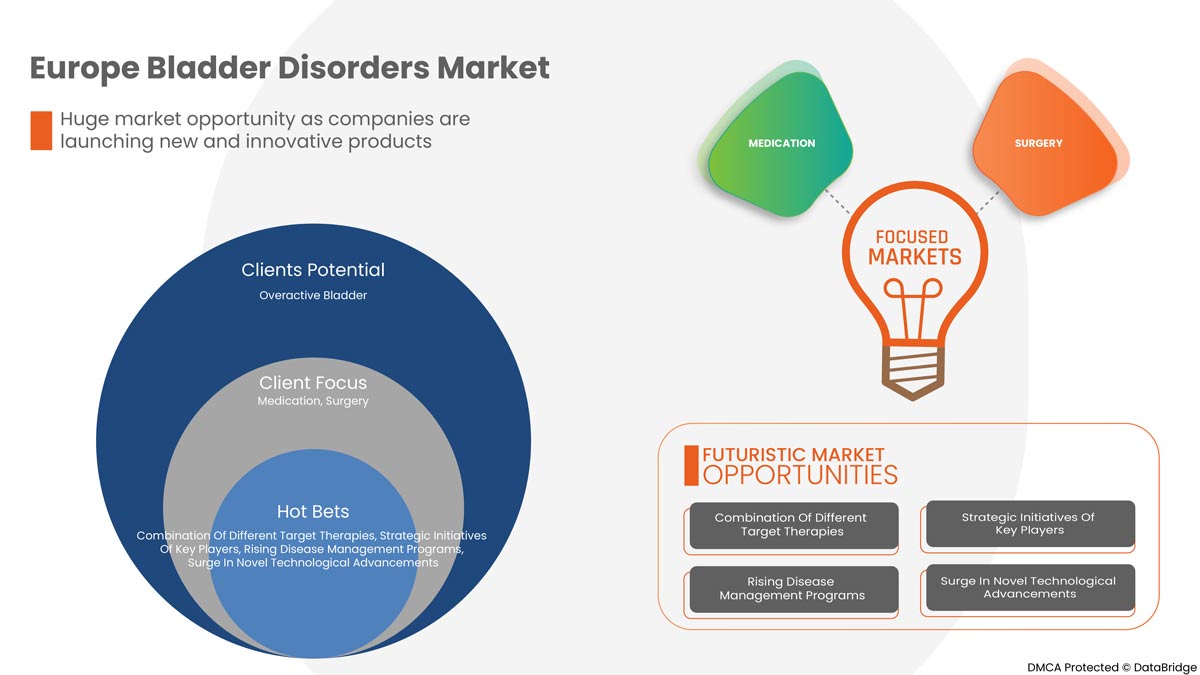

COMBINAISON DE DIFFÉRENTES THÉRAPIES CIBLÉES

Les thérapies combinées sont beaucoup plus efficaces que la monothérapie, sans effets secondaires supplémentaires. Les thérapies combinées sont une alternative sûre et efficace pour les personnes souffrant de troubles réfractaires de la vessie. La combinaison de différentes stratégies de thérapie ciblée est la meilleure approche pour soulager les patients atteints de troubles de la vessie. Des médicaments oraux et une thérapie comportementale doivent être envisagés pour le traitement réfractaire des patients. Diverses thérapies ciblées avancées sont disponibles, telles que la neuromodulation sacrée, l'injection intradétrusorienne de toxine botulique A et la stimulation percutanée du nerf tibial. Il s'agit de traitements avancés et plus efficaces que les agents oraux.

Opportunités

-

HAUSSE DES NOUVELLES AVANCÉES TECHNOLOGIQUES

Les maladies chroniques sont considérées comme l’une des principales causes de décès dans les pays en développement. Par conséquent, l’importance de la gestion des maladies chroniques dans les soins de santé est de plus en plus importante parmi les praticiens de la santé publique.

La prise en charge des troubles de la vessie met désormais l’accent sur l’aide aux patients en leur proposant diverses alternatives de soins personnels et une gamme de services de consultation pour les informer sur leur état de santé et leur permettre d’avancer. Ces thérapies aident également les patients à surmonter les traumatismes émotionnels et l’anxiété, ce qui peut agir comme un mécanisme de contre-protection.

Les avancées technologiques croissantes permettent aux organisations de soins de santé d'explorer des services et des solutions innovants pour la gestion des troubles chroniques de la vessie. Comme ils ne sont pas obligés de rester à l'hôpital pendant une période prolongée, ils ont également réduit les coûts et le volume de patients. De plus, la réduction des visites et des séjours à l'hôpital rend ce développement pratique pour les personnes âgées. Compte tenu des aspects favorables, de nombreuses organisations et entreprises développent et mettent en œuvre les technologies les plus récentes dans la gestion des maladies chroniques pour améliorer les résultats des patients.

-

PROGRAMMES DE GESTION DES MALADIES EN HAUSSE

Les personnes souffrant de problèmes de vessie ont généralement besoin de plus de services médicaux, comme des séjours à l’hôpital, des visites chez le médecin et des médicaments sur ordonnance. L’augmentation du nombre de personnes vivant plus longtemps avec de nombreux problèmes chroniques, associée à l’augmentation des dépenses de santé, a encouragé la mise en place de meilleurs plans de soins de santé.

La gestion des maladies est une stratégie qui vise à améliorer les soins tout en réduisant les dépenses liées aux soins des malades chroniques. Les programmes de gestion des maladies visent à améliorer la santé des personnes atteintes de certains troubles chroniques tels que les troubles de la vessie tout en réduisant la demande de services médicaux et les dépenses associées aux conséquences qui peuvent être évitées, telles que les séjours à l'hôpital et les visites aux urgences. Ces programmes comprennent également des informations sur les services et les solutions de gestion des maladies chroniques. Ceux-ci deviennent très populaires en raison de la prévalence croissante des maladies chroniques dans le monde. Les gouvernements et les organismes de santé ont organisé et mis en œuvre ces maladies chroniques avec de multiples programmes de gestion des maladies tels que le cancer de la vessie, la cystite interstitielle et les programmes de gestion de la vessie hyperactive. Étant donné que les programmes de gestion des maladies peuvent améliorer considérablement les pratiques d'auto-soins et réduire les visites à l'hôpital et les durées de séjour dans une plus grande mesure, ils reçoivent plus d'attention de la part des gens.

Contraintes/Défis

Cependant, la difficulté de diagnostic de la maladie et le coût des traitements et des diagnostics sont élevés en raison de la procédure de divers points de contrôle ainsi que des technologies et modalités de haute technologie pour effectuer les procédures. Le coût de la procédure est généralement élevé en raison du coût élevé des appareils technologiques avancés utilisés dans le traitement, ce qui devrait freiner la croissance du marché.

Ce rapport sur le marché des troubles de la vessie fournit des détails sur les nouveaux développements récents, les réglementations commerciales, l’analyse des importations et des exportations, l’analyse de la production, l’optimisation de la chaîne de valeur, la part de marché, l’impact des acteurs du marché national et localisé, les opportunités d’analyse en termes de poches de revenus émergentes, les changements dans les réglementations du marché, l’analyse stratégique de la croissance du marché, la taille du marché, la croissance du marché des catégories, les niches d’application et la domination, les approbations de produits, les lancements de produits, les expansions géographiques, les innovations technologiques sur le marché. Pour obtenir plus d’informations sur le marché européen des troubles de la vessie, contactez Data Bridge Market Research pour un briefing d’analyste. Notre équipe vous aidera à prendre une décision de marché éclairée pour atteindre la croissance du marché.

Impact post-COVID-19 sur le marché européen des troubles de la vessie

La COVID-19 a eu un impact positif sur le marché. Les confinements et l'isolement pendant les pandémies compliquent la gestion des maladies et l'observance des traitements. Par conséquent, l'utilisation de divers médicaments de traitement a considérablement augmenté dans la population mondiale. Par conséquent, la pandémie a eu un effet positif sur ce marché

Développement récent

- En février, AbbVie a annoncé l'approbation par la FDA américaine du BOTOX® pour le traitement de l'hyperactivité du détrusor (muscle de la vessie) associée à une affection neurologique chez les patients pédiatriques âgés de 5 ans. « Le BOTOX® est la première neurotoxine autorisée pour traiter l'hyperactivité neurogène du détrusor chez les enfants dont l'affection ne peut être traitée avec succès par un traitement anticholinergique. » Cette approbation augmentera le chiffre d'affaires de l'entreprise

Portée du marché européen des troubles de la vessie

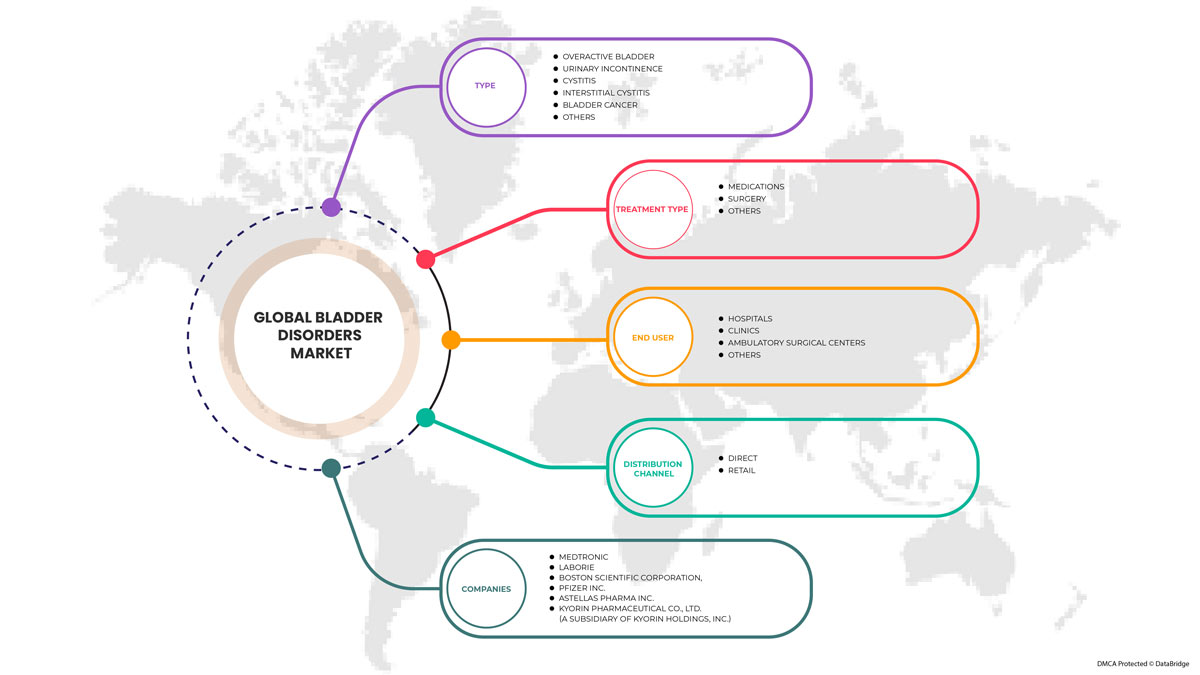

Le marché européen des troubles de la vessie est segmenté en type, type de traitement, utilisateur final et canal de distribution. La croissance parmi ces segments vous aidera à analyser les segments de croissance limités dans les industries et à fournir aux utilisateurs un aperçu précieux du marché et des informations sur le marché pour prendre des décisions stratégiques afin d'identifier les principales applications du marché.

Taper

- Cystite

- Incontinence urinaire

- Vessie hyperactive

- Cystite interstitielle

- Cancer de la vessie

Sur la base du type, le marché européen des troubles de la vessie est segmenté en cystite, incontinence urinaire, vessie hyperactive, cystite interstitielle et cancer de la vessie.

Type de traitement

- Chirurgie

- Médicaments

- Autres

Sur la base du produit, le marché européen des troubles de la vessie est segmenté en chirurgie, médicaments et autres

Utilisateur final

- Hôpital

- Cliniques

- Centres de chirurgie ambulatoire

- Autres

Sur la base des utilisateurs finaux, le marché européen des troubles de la vessie est segmenté en hôpitaux, cliniques, centres de chirurgie ambulatoire et autres

Canal de distribution

- Direct

- Vente au détail

Sur la base du canal de distribution, le marché européen des troubles de la vessie est segmenté en vente directe et au détail.

Analyse/perspectives régionales du marché des troubles de la vessie en Europe

Le marché européen des troubles de la vessie est analysé et des informations et tendances sur la taille du marché sont fournies par pays, type, type de traitement, utilisateur final et canal de distribution, comme référencé ci-dessus.

Les pays couverts par ce marché sont l'Allemagne, le Royaume-Uni, la France, l'Italie, l'Espagne, la Turquie, la Russie, les Pays-Bas, la Suisse, la Belgique et le reste de l'Europe.

L'Allemagne domine le marché européen des troubles de la vessie en termes de part de marché et de chiffre d'affaires et continuera de renforcer sa domination au cours de la période de prévision. Cela est dû à la forte prévalence des troubles de la vessie hyperactive dans la région, et aux investissements croissants en R&D et au lancement de nouvelles thérapies qui stimulent le marché

La section pays du rapport fournit également des facteurs d'impact sur les marchés individuels et des changements de réglementation sur le marché qui ont un impact sur les tendances actuelles et futures du marché. Des points de données, tels que les ventes de produits neufs et de remplacement, la démographie des pays, l'épidémiologie des maladies et les tarifs d'importation et d'exportation, sont quelques-uns des principaux indicateurs utilisés pour prévoir le scénario de marché pour les différents pays. En outre, la présence et la disponibilité des marques européennes et les défis auxquels elles sont confrontées en raison de la forte concurrence des marques locales et nationales et de l'impact des canaux de vente sont pris en compte tout en fournissant une analyse prévisionnelle des données nationales.

Analyse du paysage concurrentiel et des parts de marché des troubles de la vessie en Europe

Le paysage concurrentiel du marché des troubles de la vessie en Europe fournit des détails sur les concurrents. Les détails inclus sont la présentation de l'entreprise, les finances de l'entreprise, les revenus générés, le potentiel du marché, les investissements dans la recherche et le développement, les nouvelles initiatives du marché, la présence en Asie-Pacifique, les sites et installations de production, les capacités de production, les forces et les faiblesses de l'entreprise, le lancement du produit, la largeur et l'étendue du produit et la domination des applications. Les points de données ci-dessus ne concernent que l'orientation de l'entreprise vers le marché européen des troubles de la vessie.

Français Certains des principaux acteurs opérant sur le marché européen des troubles de la vessie sont Medtronic, Laborie, Boston Scientific Corporation, Pfizer Inc., Astellas Pharma Inc., KYORIN Pharmaceutical Co., Ltd. (Une filiale de KYORIN Holdings, Inc.), Bristol-Myers Squibb Company, Johnson & Johnson Services, Inc., Axonics, Inc., Merck & Co., Inc., Viatris Inc., Blue Wind Medical, Gaylord Chemical Company, LLC, Coloplast Corp, AbbVie Inc., Sun Pharmaceutical Industries Ltd., Zydus Group, Urovant Sciences entre autres.

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. Les données du marché sont analysées et estimées à l'aide de modèles statistiques et cohérents du marché. En outre, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. La principale méthodologie de recherche utilisée par l'équipe de recherche DBMR est la triangulation des données, qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données comprennent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des parts de marché des entreprises, les normes de mesure, l'Europe par rapport aux régions et l'analyse des parts des fournisseurs. Veuillez demander un appel d'analyste en cas de demande de renseignements supplémentaires.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Table des matières

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF EUROPE BLADDER DISORDERS MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 TYPE LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.2 PORTER'S FIVE FORCES

4.3 EUROPE BLADDER DISORDERS MARKET, PIPELINE ANALYSIS

5 EUROPE BLADDER DISORDER MARKET: REGULATIONS

5.1 THE U.S. REGULATORY FRAMEWORK FOR BLADDER DISOREDER MEDICATION

5.2 EUROPE REGULATORY FRAMEWORK FOR BLADDER DISORDER DRUGS

5.3 JAPAN REGULATORY GUIDANCE ON BLADDER DISORDER DRUGS

6 EUROPE BLADDER DISORDERS MARKET OVERVIEW

6.1 DRIVERS

6.1.1 STRATEGIC INITIATIVES ADOPTED BY MARKET PLAYERS

6.1.2 GROWING GERIATRIC POPULATION

6.1.3 RISING R&D INVESTMENTS AND LAUNCH OF NOVEL THERAPIES IN UPCOMING YEARS

6.1.4 COMBINATION OF DIFFERENT TARGET THERAPIES

6.2 RESTRAINTS

6.2.1 HIGH COST ASSOCIATED WITH BLADDER DISORDER DIAGNOSTIC TREATMENT

6.2.2 PRODUCTS RECALLS FROM MARKET

6.3 OPPORTUNITIES

6.3.1 SURGE IN NOVEL TECHNOLOGICAL ADVANCEMENTS

6.3.2 RISING DISEASE MANAGEMENT PROGRAMS

6.4 CHALLENGES

6.4.1 LACK OF AWARENESS ABOUT BLADDER DISORDERS RELATED PROBLEMS

6.4.2 PATENT EXPIRY OF DRUGS

7 EUROPE BLADDER DISORDERS MARKET, BY TYPE

7.1 OVERVIEW

7.2 OVERACTIVE BLADDER

7.3 URINARY INCONTINENCE

7.4 CYSTITIS

7.5 INTERSTITIAL CYSTITIS

7.6 BLADDER CANCER

7.7 OTHERS

8 EUROPE BLADDER DISORDERS MARKET, BY TREATMENT TYPE

8.1 OVERVIEW

8.2 MEDICATION

8.2.1 TOLTERODINE

8.2.2 MIRABEGRON

8.2.3 FESOTERODINE

8.2.4 OXYBUTYNIN

8.2.5 SOLIFENACIN

8.2.6 DARIFENACIN

8.2.7 TROSPIUM

8.2.8 OTHERS

8.3 SURGERY

8.3.1 SURGERY TO INCREASE BLADDER CAPACITY

8.3.2 BLADDER REMOVAL

8.3.3 OTHERS

8.4 OTHERS

9 EUROPE BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL

9.1 OVERVIEW

9.2 DIRECT

9.3 RETAIL

10 EUROPE BLADDER DISORDERS MARKET, BY END USER

10.1 OVERVIEW

10.2 HOSPITALS

10.3 CLINICS

10.4 AMBULATORY SURGICAL CENTERS

10.5 OTHERS

11 EUROPE BLADDER DISORDERS MARKET, BY GEOGRAPHY

11.1 EUROPE

11.1.1 GERMANY

11.1.2 U.K.

11.1.3 FRANCE

11.1.4 ITALY

11.1.5 SPAIN

11.1.6 TURKEY

11.1.7 RUSSIA

11.1.8 NETHERLANDS

11.1.9 SWITZERLAND

11.1.10 BELGIUM

11.1.11 REST OF EUROPE

12 EUROPE BLADDER DISORDERS MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: EUROPE

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 MERCK AND CO. INC. (2021)

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENT

14.2 ASTELLAS PHARMA INC. (2021)

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENTS

14.3 BRISTOL-MYERS SQUIBB COMPANY (2021)

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENT

14.4 BOSTON SCIENTIFIC CORPORATION (2021)

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENT

14.5 VIATRIS INC. (2021)

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT PORTFOLIO

14.5.5 RECENT DEVELOPMENT

14.6 ABBVIE (2021)

14.6.1 COMPANY SNAPSHOT

14.6.2 REVENUE ANALYSIS

14.6.3 PRODUCT PORTFOLIO

14.6.4 RECENT DEVELOPMENT

14.7 AXONICS, INC. (2021)

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCT PORTFOLIO

14.7.4 RECENT DEVELOPMENT

14.8 BLUE WIND MEDICAL (2021)

14.8.1 COMPANY SNAPSHOT

14.8.2 PRODUCT PORTFOLIO

14.8.3 RECENT DEVELOPMENT

14.9 COLOPLAST CORP. (2021)

14.9.1 COMPANY SNAPSHOT

14.9.2 REVENUE ANALYSIS

14.9.3 PRODUCT PORTFOLIO

14.1 GAYLORD CHEMICAL COMPANY, LLC (2021)

14.10.1 COMPANY SNAPSHOT

14.10.2 PRODUCT PORTFOLIO

14.10.3 RECENT DEVELOPMENT

14.11 JOHNSON & JOHNSON SERVICES, INC. (2021)

14.11.1 COMPANY SNAPSHOT

14.11.2 REVENUE ANALYSIS

14.11.3 PRODUCT PORTFOLIO

14.11.4 RECENT DEVELOPMENT

14.12 KYORIN PHARMACEUTICAL CO., LTD. (A SUBSIDIARY OF KYORIN HOLDINGS, INC.) (2021)

14.12.1 COMPANY SNAPSHOT

14.12.2 PRODUCT PORTFOLIO

14.12.3 RECENT DEVELOPMENTS

14.13 LABORIE (2021)

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCT PORTFOLIO

14.13.3 RECENT DEVELOPMENT

14.14 MEDTRONIC (2021)

14.14.1 COMPANY SNAPSHOT

14.14.2 REVENUE ANALYSIS

14.14.3 PRODUCT PORTFOLIO

14.14.4 RECENT DEVELOPMENTS

14.15 PFIZER INC. (2021)

14.15.1 COMPANY SNAPSHOT

14.15.2 REVENUE ANALYSIS

14.15.3 PRODUCT PORTFOLIO

14.15.4 RECENT DEVELOPMENTS

14.16 VALENCIA TECHNOLOGIES (2021)

14.16.1 COMPANY SNAPSHOT

14.16.2 PRODUCT PORTFOLIO

14.16.3 RECENT DEVELOPMENT

14.17 SUN PHAMACEUTICAL INDUSTRIES LTD. (2021)

14.17.1 COMPANY SNAPSHOT

14.17.2 REVENUE ANALYSIS

14.17.3 PRODUCT PORTFOLIO

14.17.4 RECENT DEVELOPMENT

14.18 SWATI SPENTOSE (2021)

14.18.1 COMPANY SNAPSHOT

14.18.2 PRODUCT PORTFOLIO

14.18.3 RECENT DEVELOPMENT

14.19 UROVANT SCIENCES (2021)

14.19.1 COMPANY SNAPSHOT

14.19.2 PRODUCT PORTFOLIO

14.19.3 RECENT DEVELOPMENT

14.2 ZYDUS GROUP (2021)

14.20.1 COMPANY SNAPSHOT

14.20.2 PRODUCT PORTFOLIO

14.20.3 RECENT DEVELOPMENT

15 QUESTIONNAIRE

16 RELATED REPORTS

Liste des tableaux

TABLE 1 EUROPE BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 2 EUROPE OVERACTIVE BLADDER IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 3 EUROPE URINARY INCONTINENCE IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 4 EUROPE CYSTITIS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 5 EUROPE INTERSTITIAL CYSTITIS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 6 EUROPE BLADDER CANCER IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 7 EUROPE OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 8 EUROPE BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 9 EUROPE MEDICATION IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 10 EUROPE MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 11 EUROPE SURGERY IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 12 EUROPE SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 13 EUROPE OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 14 EUROPE BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 15 EUROPE DIRECT IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 16 EUROPE RETAIL IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 17 EUROPE BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 18 EUROPE HOSPITALS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 19 EUROPE CLINICS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 20 EUROPE AMBULATORY SURGICAL CENTERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 21 EUROPE OTHERS IN BLADDER DISORDERS MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 22 EUROPE BLADDER DISORDERS MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 23 EUROPE BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 24 EUROPE BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 25 EUROPE MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 26 EUROPE SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 27 EUROPE BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 28 EUROPE BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 29 GERMANY BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 30 GERMANY BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 31 GERMANY MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 32 GERMANY SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 33 GERMANY BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 34 GERMANY BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 35 U.K. BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 36 U.K. BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 37 U.K. MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 38 U.K. SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 39 U.K. BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 40 U.K. BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 41 FRANCE BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 42 FRANCE BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 43 FRANCE MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 44 FRANCE SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 45 FRANCE BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 46 FRANCE BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 47 ITALY BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 48 ITALY BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 49 ITALY MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 50 ITALY SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 51 ITALY BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 52 ITALY BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 53 SPAIN BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 54 SPAIN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 55 SPAIN MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 56 SPAIN. SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 57 SPAIN BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 58 SPAIN BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 59 TURKEY BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 60 TURKEY BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 61 TURKEY MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 62 TURKEY SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 63 TURKEY BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 64 TURKEY BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 65 RUSSIA BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 66 RUSSIA BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 67 RUSSIA MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 68 RUSSIA SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 69 RUSSIA BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 70 RUSSIA BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 71 NETHERLANDS BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 72 NETHERLANDS BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 73 NETHERLANDS MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 74 NETHERLANDS SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 75 NETHERLANDS BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 76 NETHERLANDS BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 77 SWITZERLAND BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 78 SWITZERLAND BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 79 SWITZERLAND MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 80 SWITZERLAND SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 81 SWITZERLAND BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 82 SWITZERLAND BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 83 BELGIUM BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 84 BELGIUM BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 85 BELGIUM MEDICATIONS IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 86 BELGIUM SURGERY IN BLADDER DISORDERS MARKET, BY TREATMENT TYPE, 2020-2029 (USD MILLION)

TABLE 87 BELGIUM BLADDER DISORDERS MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 88 BELGIUM BLADDER DISORDERS MARKET, BY DISTRIBUTION CHANNEL, 2020-2029 (USD MILLION)

TABLE 89 REST OF EUROPE BLADDER DISORDERS MARKET, BY TYPE, 2020-2029 (USD MILLION)

Liste des figures

FIGURE 1 EUROPE BLADDER DISORDERS MARKET: SEGMENTATION

FIGURE 2 EUROPE BLADDER DISORDERS MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE BLADDER DISORDERS MARKET: DROC ANALYSIS

FIGURE 4 EUROPE BLADDER DISORDERS MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE BLADDER DISORDERS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE BLADDER DISORDERS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE BLADDER DISORDERS MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE BLADDER DISORDERS MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 EUROPE BLADDER DISORDERS MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 EUROPE BLADDER DISORDERS MARKET: SEGMENTATION

FIGURE 11 RISING EPIDEMIC AND PANDEMIC OUTBREAK AND INCREASING PREVALENCE OF BLADDER DISORDERS EXPECTED TO DRIVE THE EUROPE BLADDER DISORDERS MARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 12 OVERACTIVE BLADDER SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE BLADDER DISORDERS MARKET IN 2022 & 2029

FIGURE 13 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE EUROPE BLADDER DISORDER MARKET

FIGURE 14 EUROPE BLADDER DISORDERS MARKET: BY TYPE, 2021

FIGURE 15 EUROPE BLADDER DISORDERS MARKET: BY TYPE, 2022-2029 (USD MILLION)

FIGURE 16 EUROPE BLADDER DISORDERS MARKET: BY TYPE, CAGR (2022-2029)

FIGURE 17 EUROPE BLADDER DISORDERS MARKET: BY TYPE, LIFELINE CURVE

FIGURE 18 EUROPE BLADDER DISORDERS MARKET: BY TREATMENT TYPE, 2021

FIGURE 19 EUROPE BLADDER DISORDERS MARKET: BY TREATMENT TYPE, 2022-2029 (USD MILLION)

FIGURE 20 EUROPE BLADDER DISORDERS MARKET: BY TREATMENT TYPE, CAGR (2022-2029)

FIGURE 21 EUROPE BLADDER DISORDERS MARKET: BY TREATMENT TYPE, LIFELINE CURVE

FIGURE 22 EUROPE BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, 2021

FIGURE 23 EUROPE BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, 2022-2029 (USD MILLION)

FIGURE 24 EUROPE BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, CAGR (2022-2029)

FIGURE 25 EUROPE BLADDER DISORDERS MARKET: BY DISTRIBUTION CHANNEL, LIFELINE CURVE

FIGURE 26 EUROPE BLADDER DISORDERS MARKET: BY END USER, 2021

FIGURE 27 EUROPE BLADDER DISORDERS MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 28 EUROPE BLADDER DISORDERS MARKET: BY END USER, CAGR (2022-2029)

FIGURE 29 EUROPE BLADDER DISORDERS MARKET: BY END USER, LIFELINE CURVE

FIGURE 30 EUROPE BLADDER DISORDERS MARKET: SNAPSHOT (2021)

FIGURE 31 EUROPE BLADDER DISORDERS MARKET: BY COUNTRY (2021)

FIGURE 32 EUROPE BLADDER DISORDERS MARKET: BY COUNTRY (2022 & 2029)

FIGURE 33 EUROPE BLADDER DISORDERS MARKET: BY COUNTRY (2021 & 2029)

FIGURE 34 EUROPE BLADDER DISORDERS MARKET: BY TYPE (2022-2029)

FIGURE 35 EUROPE BLADDER DISORDERS MARKET: COMPANY SHARE 2021 (%)

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.