Les implants orthopédiques, y compris les implants dentaires, sont des dispositifs médicaux essentiels. Ils redonnent mobilité et qualité de vie aux patients souffrant de problèmes articulaires, de fractures ou de perte de dents. Ces implants comportent des matériaux biocompatibles qui s'intègrent aux tissus du corps, garantissant stabilité et durabilité. Ils sont utilisés dans les chirurgies orthopédiques telles que les arthroplasties et la fixation des fractures. Les implants dentaires offrent une solution durable aux dents manquantes, améliorant ainsi la fonction buccale et l’esthétique. Dans l’ensemble, les implants orthopédiques améliorent grandement le bien-être des patients en rétablissant la mobilité physique et la santé dentaire.

Accéder au rapport complet @ https://www.databridgemarketresearch.com/reports/mena-and-gcc-orthopedic-implants-inclure-dental-implants-market

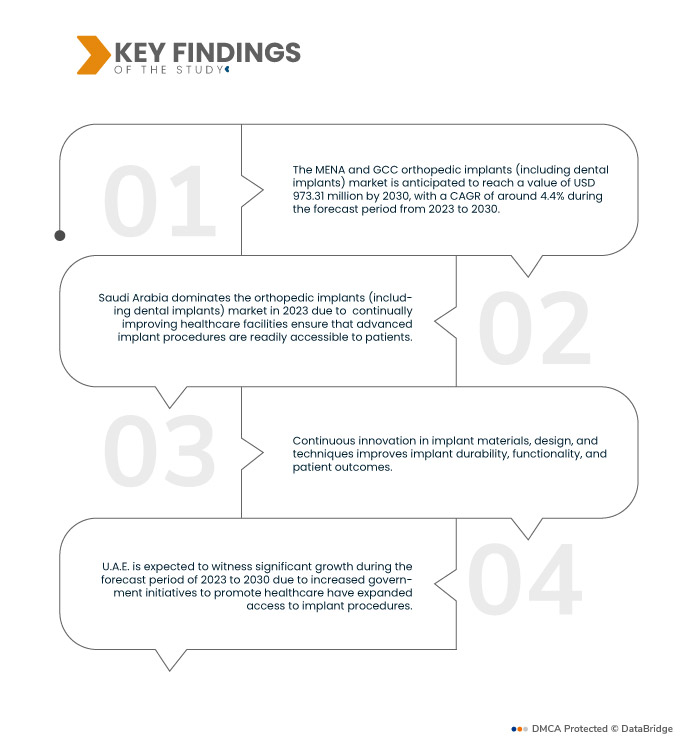

Data Bridge Market Research analyse que le Marché des implants orthopédiques MENA et GCC (y compris les implants dentaires) est évalué à 689,67 millions de dollars en 2022 et devrait atteindre 973,31 millions de dollars d'ici 2030, enregistrant un TCAC de 4,4 % au cours de la période de prévision de 2023 à 2030. La population vieillissante connaît davantage de problèmes orthopédiques et dentaires, tels que la dégénérescence des articulations et des dents. perte. Cette tendance démographique alimente la demande d’implants orthopédiques et dentaires en tant que solutions efficaces pour résoudre ces problèmes de santé liés à l’âge, stimulant ainsi la croissance du marché des implants.

Principales conclusions de l'étude

La sensibilisation à la santé dentaire devrait stimuler le taux de croissance du marché

La sensibilisation croissante à la santé dentaire et aux avantages des implants dentaires en tant qu’option de remplacement dentaire durable est un moteur important du marché. Les patients recherchent des solutions à long terme qui imitent les dents naturelles et améliorent leur santé bucco-dentaire globale. Cette prise de conscience encourage davantage de personnes à envisager les implants dentaires plutôt que les options traditionnelles, telles que les prothèses dentaires ou les ponts. En conséquence, la demande d’implants dentaires continue d’augmenter alors que les patients accordent la priorité à leur bien-être dentaire et à leur qualité de vie.

Portée du rapport et segmentation du marché

|

Mesure du rapport

|

Détails

|

|

Période de prévision

|

2023 à 2030

|

|

Année de référence

|

2022

|

|

Années historiques

|

2021 (personnalisable jusqu'en 2015-2020)

|

|

Unités quantitatives

|

Chiffre d'affaires en millions USD, volumes en unités, prix en USD

|

|

Segments couverts

|

Produits (arthroplasties reconstructives, Implants rachidiens, Traumatisme et craniomaxillo-facial, implants dentaires, orthobiologiques), type de dispositif (dispositifs de fixation interne et dispositifs de fixation externe), biomatériau (Biomatériaux métalliques, Biomatériaux polymères, biomatériaux céramiques, biomatériaux naturels et autres), procédures (chirurgie ouverte et chirurgie mini-invasive (Mis)), utilisateur final (hôpitaux, centre de soins ambulatoires, cliniques spécialisées, centres orthopédiques et autres), propriété (gouvernementale et privée)

|

|

Pays couverts

|

Arabie saoudite, Koweït, Émirats arabes unis, Qatar, Bahreïn et Oman

|

|

Acteurs du marché couverts

|

3M (États-Unis), B. Braun Melsungen AG (Allemagne), Integra LifeSciences (États-Unis), Depuy Synthes (filiale de JnJ) Inc. (États-Unis), Zimmer Biomet (États-Unis), Smith & Nephew plc (Royaume-Uni), Medtronic ( Irlande), Stryker (États-Unis), Changzhou Waston Medical Appliance Co., Ltd. (États-Unis), Narang Medical Limited (Inde), WL Gore & Associates, Inc. (États-Unis), Arthrex, Inc. (États-Unis), GE HEALTHCARE ( États-Unis), DJO, LLC (filiale de Colfax Corporation) (Chine), curex (États-Unis), Samay Surgical (Inde), Dongguan Traumed Technology Co., Ltd. (Chine), Abou Hamela Group (Égypte)

|

|

Points de données couverts dans le rapport

|

En plus des informations sur les scénarios de marché tels que la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux acteurs, les rapports de marché organisés par Data Bridge Market Research comprennent également une analyse approfondie d'experts, l'épidémiologie des patients, une analyse du pipeline, une analyse des prix, et cadre réglementaire

|

Analyse sectorielle :

Le marché des implants orthopédiques MENA et GCC (y compris les implants dentaires) est segmenté en fonction des produits, du type d’appareil, du biomatériau, des procédures, de l’utilisateur final et de la propriété.

- Sur la base des produits, le marché des implants orthopédiques (y compris les implants dentaires) est segmenté en arthroplasties reconstructives, implants rachidiens, implants traumatologiques et craniomaxillo-faciaux, implants dentaires et orthobiologiques. En 2023, le segment des arthroplasties reconstructives domine le marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 5,1 % au cours de la période de prévision 2023 à 2030, à mesure que le vieillissement de la population augmente, tout comme la prévalence des affections articulaires telles que l'arthrose.

En 2023, le segment des arthroplasties reconstructives domine le marché. Marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 5,1 % au cours de la période de prévision 2023 à 2030

En 2023, le segment des arthroplasties reconstructives domine le marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 5,1 % au cours de la période de prévision 2023 à 2030, car les arthroplasties reconstructives, telles que les arthroplasties de la hanche et du genou, offrent des solutions efficaces pour restaurer la mobilité et soulager la douleur. Les progrès technologiques ont conduit à des conceptions d’implants durables et innovantes, améliorant ainsi les résultats pour les patients. De plus, ces procédures sont devenues plus accessibles, grâce à des techniques chirurgicales améliorées et des temps de récupération réduits.

- Sur la base du type de dispositif, le marché des implants orthopédiques (y compris les implants dentaires) est segmenté en dispositifs de fixation interne et dispositifs de fixation externe. En 2023, le segment des dispositifs de fixation interne domine le marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 4,5 % au cours de la période de prévision 2023 à 2030, car ces dispositifs, notamment les vis, les plaques et les clous, sont essentiels à la stabilisation des fractures et à la facilitation des os. guérison.

- Sur la base des biomatériaux, le marché des implants orthopédiques (y compris les implants dentaires) est segmenté en biomatériaux métalliques, biomatériaux polymères, biomatériaux céramiques, biomatériaux naturels, et d'autres. En 2023, le segment des biomatériaux métalliques dominera le marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 4,7 % au cours de la période de prévision 2023 à 2030, car les biomatériaux métalliques, tels que le titane et l'acier inoxydable, sont appréciés pour leur résistance, leur durabilité, et biocompatibilité, ce qui les rend idéaux pour les implants orthopédiques tels que les arthroplasties et les dispositifs rachidiens.

- Sur la base des procédures, le marché des implants orthopédiques (y compris les implants dentaires) est segmenté en chirurgie ouverte et la chirurgie minimalement invasive (MIS). En 2023, le segment de la chirurgie ouverte domine le marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 4,5 % au cours de la période de prévision 2023 à 2030, car les procédures de chirurgie ouverte traditionnelles offrent une visibilité directe et un retour tactile aux chirurgiens orthopédistes, permettant une pose précise des implants. surtout dans les cas complexes.

- Sur la base de l’utilisateur final, le marché des implants orthopédiques (y compris les implants dentaires) est segmenté en hôpitaux, centres de soins ambulatoires, cliniques spécialisées, centres orthopédiques et autres. En 2023, le segment des hôpitaux domine le marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 4,8 % au cours de la période de prévision 2023 à 2030, les hôpitaux servant de centres principaux pour les interventions chirurgicales, y compris les chirurgies orthopédiques.

En 2023, le segment des hôpitaux domine le marché Marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 4,8 % au cours de la période de prévision 2023 à 2030

En 2023, le segment des hôpitaux domine le marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 4,8 % au cours de la période de prévision 2023 à 2030, car ils ont accès à des équipements de pointe, à des chirurgiens expérimentés et à des installations complètes de soins aux patients, ce qui en fait le segment préféré. choix pour les procédures d’implantation orthopédiques complexes. De plus, les hôpitaux reçoivent souvent des références pour des cas orthopédiques spécialisés, renforçant ainsi leur domination sur ce marché. À mesure que la population mondiale vieillit et que les problèmes orthopédiques deviennent plus répandus, la demande de procédures d'implants orthopédiques en milieu hospitalier continue d'augmenter, consolidant ainsi la position de leader du segment hospitalier dans la croissance du marché.

- Sur la base de la propriété, le marché des implants orthopédiques (y compris les implants dentaires) est segmenté en public et privé. En 2023, le segment gouvernemental domine le marché des implants orthopédiques (y compris les implants dentaires) avec un TCAC de 4,7 % au cours de la période de prévision 2023 à 2030 en raison de son rôle important dans la régulation et le financement des systèmes de santé.

Acteurs majeurs

Data Bridge Market Research reconnaît les sociétés suivantes comme les principaux acteurs du marché des implants orthopédiques (y compris les implants dentaires) de la région MENA et GCC (y compris les implants dentaires) sur le marché des implants orthopédiques (y compris les implants dentaires) de la région MENA et GCC : 3M (États-Unis), B. Braun Melsungen AG (Allemagne), Integra LifeSciences (États-Unis), Depuy Synthes (filiale de JnJ) Inc. (États-Unis), Zimmer Biomet (États-Unis), Smith & Nephew plc (Royaume-Uni), Medtronic (Irlande), Stryker (États-Unis), Changzhou Waston Medical Appliance Co. , Ltd. (États-Unis)

Développements du marché

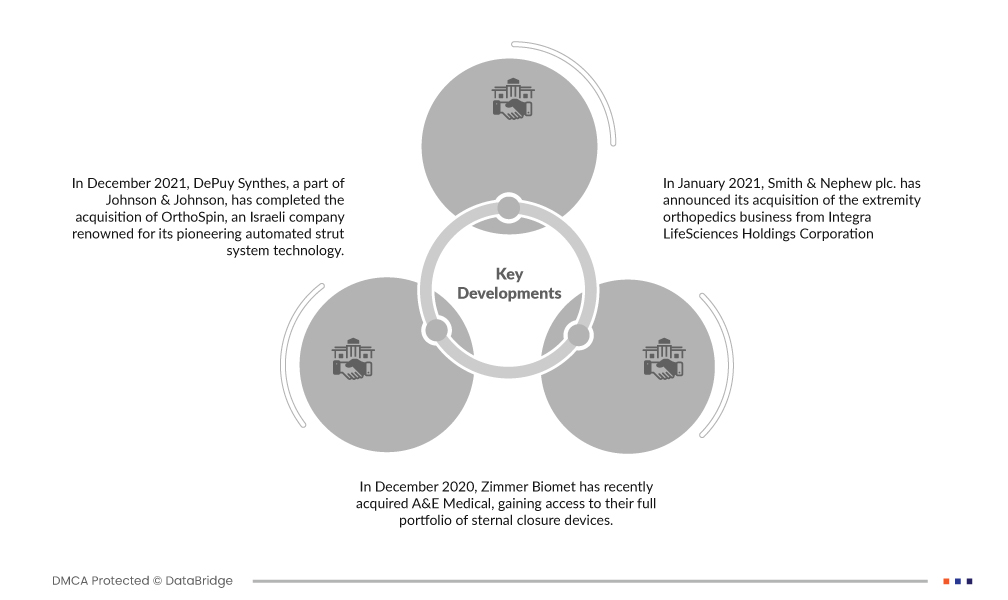

- En décembre 2021, DePuy Synthes, qui fait partie de Johnson & Johnson, a finalisé l'acquisition d'OrthoSpin, une société israélienne réputée pour sa technologie pionnière de système de jambe de force automatisée. Ce système innovant complète le système de correction multi-axiale MAXFRAME de DePuy Synthes, un système de fixation par anneau externe, améliorant les capacités de l'entreprise dans le domaine de l'innovation médicale.

- En décembre 2020, Zimmer Biomet a récemment acquis A&E Medical, accédant ainsi à sa gamme complète de dispositifs de fermeture sternale. Cette acquisition stratégique élargit considérablement le portefeuille d'implants orthopédiques de Zimmer Biomet, positionnant ainsi l'entreprise pour une augmentation des ventes et une demande accrue sur le marché. Cette décision devrait stimuler la croissance future des revenus de Zimmer Biomet.

- En janvier 2021, Smith & Nephew plc. a annoncé son acquisition de l'activité d'orthopédie des extrémités auprès d'Integra LifeSciences Holdings Corporation. Cette décision stratégique a effectivement élargi le portefeuille de produits de l'entreprise.

Analyse régionale

Géographiquement, les pays couverts par le rapport sur le marché des implants orthopédiques (y compris les implants dentaires) de la région MENA et CCG sont l’Arabie saoudite, le Koweït, les Émirats arabes unis, le Qatar, Bahreïn et Oman.

Selon l’analyse de l’étude de marché Data Bridge :

L’Arabie Saoudite domine la région MENA et le CCG Marché des implants orthopédiques (y compris les implants dentaires) pendant la période de prévision 2023 - 2030

En 2023, l'Arabie Saoudite domine le marché des implants orthopédiques (y compris les implants dentaires) de la région MENA et GCC en raison de la forte présence d'acteurs majeurs de l'industrie qui stimule l'innovation et la concurrence, améliorant la qualité et la variété des implants disponibles. De plus, les infrastructures de santé exceptionnelles dans les régions développées soutiennent l’intégration transparente de ces implants. Enfin, une population importante confrontée à des blessures et à des interventions chirurgicales, en particulier dans une population vieillissante, contribue à une croissance soutenue du marché, les implants devenant des solutions essentielles pour restaurer la mobilité et la qualité de vie.

Les Émirats arabes unis devraient connaître une croissance significative au cours de la période de prévision de 2023 à 2030.

En 2023, les Émirats arabes unis devrait connaître une croissance significative en raison de la sensibilisation croissante du public aux avantages des implants et des options chirurgicales avancées qui ont stimulé la demande des patients. Troisièmement, un bassin de population important et croissant, combiné à un besoin croissant de soins de santé de qualité, a créé un marché important pour ces technologies médicales avancées. En résumé, ces facteurs convergent pour alimenter l’expansion du marché des implants orthopédiques en réponse à une sensibilisation et à une demande accrues en matière de soins de santé.

Pour des informations plus détaillées sur le marché des implants orthopédiques (y compris les implants dentaires) rapport, cliquez ici – https://www.databridgemarketresearch.com/reports/mena-and-gcc-orthopedic-implants-inclure-dental-implants-market