North America Vegan Protein Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

3.77 Billion

USD

6.63 Billion

2024

2032

USD

3.77 Billion

USD

6.63 Billion

2024

2032

| 2025 –2032 | |

| USD 3.77 Billion | |

| USD 6.63 Billion | |

| % | |

|

Segmentación del mercado de proteínas veganas en Norteamérica por fuente (proteína de soja, proteína de guisante, proteína de arroz, proteína de cáñamo, espirulina, proteína de quinua, proteína de linaza, proteína de chía, proteína de canola, semilla de calabaza, entre otras), tipo de proteína (aislados, concentrados e hidrolizados), grado de hidrolización (intacto, ligeramente hidrolizado, fuertemente hidrolizado), forma (seca y líquida), naturaleza (convencional y orgánica), función (solubilidad, emulsificación, gelificación, fijación de agua, formación de espuma, entre otras), aplicación (alimentos, bebidas, nutracéuticos y suplementos dietéticos, cosméticos y cuidado personal, piensos, productos farmacéuticos, entre otros): tendencias y pronóstico de la industria hasta 2032.

Tamaño del mercado de proteínas veganas en América del Norte

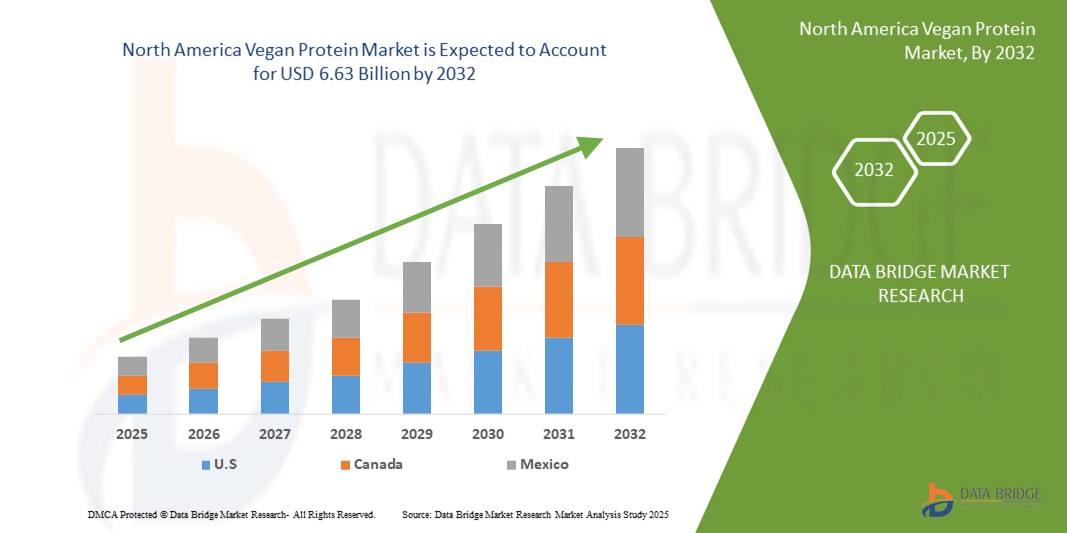

- El tamaño del mercado de proteína vegana de América del Norte se valoró en USD 3.77 mil millones en 2024 y se espera que alcance los USD 6.63 mil millones para 2032 , con una CAGR del 7,30% durante el período de pronóstico.

- El crecimiento del mercado está impulsado en gran medida por la creciente adopción de dietas basadas en plantas, el creciente enfoque del consumidor en la salud y el bienestar y la creciente conciencia ambiental y ética.

- El aumento de la demanda de alimentos funcionales, bebidas y suplementos dietéticos enriquecidos con proteínas está impulsando aún más la expansión del mercado.

Análisis del mercado de proteínas veganas en Norteamérica

- La creciente adopción de dietas basadas en plantas y la creciente concienciación sobre la salud entre los consumidores impulsan la demanda de productos proteicos veganos. La creciente concienciación sobre los beneficios ambientales y éticos de las proteínas vegetales impulsa aún más el crecimiento del mercado.

- El aumento de las tendencias de fitness y bienestar, junto con el uso cada vez mayor de proteínas veganas en alimentos funcionales, nutracéuticos y suplementos dietéticos, está contribuyendo a la expansión del mercado.

- El mercado estadounidense de proteínas veganas captó la mayor participación en los ingresos de Norteamérica en 2024, impulsado por la alta concienciación de los consumidores sobre las dietas basadas en plantas, la salud y la sostenibilidad. Los consumidores priorizan cada vez más los alimentos, bebidas y suplementos dietéticos enriquecidos con proteínas, lo que impulsa la demanda de polvos, barras y productos funcionales veganos.

- Se espera que Canadá experimente la mayor tasa de crecimiento anual compuesta (TCAC) en el mercado norteamericano de proteínas veganas debido a la creciente demanda de alternativas alimentarias sostenibles, el aumento de la población vegana y el aumento de las inversiones en innovación alimentaria de origen vegetal. Las políticas gubernamentales de apoyo y la creciente adopción de proteínas veganas en los sectores minorista y de servicios de alimentación están acelerando el crecimiento del mercado.

- El segmento de proteína de soya obtuvo la mayor participación en los ingresos del mercado en 2024, impulsado por su amplio uso en alimentos, bebidas y suplementos dietéticos. La proteína de soya es apreciada por su alto valor nutricional, sus aplicaciones versátiles y su consolidada cadena de suministro en diferentes países.

Alcance del informe y segmentación del mercado de proteínas veganas en América del Norte

|

Atributos |

Perspectivas clave del mercado de proteínas veganas en América del Norte |

|

Segmentos cubiertos |

• Por origen: proteína de soya, proteína de guisante, proteína de arroz, proteína de cáñamo, espirulina, proteína de quinoa, proteína de semillas de lino, proteína de chía, proteína de canola, semilla de calabaza y otras |

|

Países cubiertos |

América del norte

|

|

Actores clave del mercado |

|

|

Oportunidades de mercado |

|

|

Conjuntos de información de datos de valor añadido |

Además de los conocimientos sobre escenarios de mercado, como valor de mercado, tasa de crecimiento, segmentación, cobertura geográfica y actores principales, los informes de mercado seleccionados por Data Bridge Market Research también incluyen análisis en profundidad de expertos, análisis de precios, análisis de participación de marca, encuesta de consumidores, análisis demográfico, análisis de la cadena de suministro, análisis de la cadena de valor, descripción general de materias primas/consumibles, criterios de selección de proveedores, análisis PESTLE, análisis de Porter y marco regulatorio. |

Tendencias del mercado de proteínas veganas en América del Norte

Creciente adopción de soluciones proteicas de origen vegetal

- La creciente tendencia hacia los productos proteicos veganos está transformando el panorama alimentario y nutracéutico al ofrecer alternativas proteicas sostenibles de origen vegetal. Estos productos permiten a los consumidores cubrir sus necesidades proteicas diarias, reduciendo al mismo tiempo la dependencia de fuentes de origen animal, lo que contribuye a objetivos de salud y ambientales. El creciente interés de los consumidores por opciones alimentarias éticas y ecológicas impulsa aún más su aceptación en el mercado.

- La creciente demanda de proteínas en polvo, barras y suplementos prácticos está impulsando la adopción de soluciones proteicas veganas. Estos productos son especialmente eficaces en los sectores del fitness y el bienestar, donde los consumidores buscan opciones rápidas y nutritivas. La disponibilidad de productos listos para usar y con sabor aumenta la comodidad del consumidor y fomenta su consumo frecuente.

- La asequibilidad, la variedad y la facilidad de incorporación de la proteína vegana a la dieta diaria hacen que estos productos sean atractivos para hogares, gimnasios y establecimientos de restauración. Su consumo frecuente mejora la diversidad dietética y favorece las tendencias generales de salud y bienestar. Además, la tendencia hacia las proteínas vegetales funcionales y fortificadas está ampliando sus aplicaciones en la nutrición diaria.

- Por ejemplo, en los últimos años, varias marcas de nutrición informaron un aumento en las ventas tras el lanzamiento de nuevos polvos de proteína de guisante, arroz y soja dirigidos a consumidores veganos y flexitarianos. Estos lanzamientos propiciaron una mayor adopción y una mayor interacción con el consumidor. Las iniciativas de marketing que destacan la sostenibilidad, la nutrición y la versatilidad ampliaron aún más el alcance del producto.

- Si bien los productos proteicos veganos promueven un consumo responsable y una dieta sostenible, su crecimiento en el mercado depende de la innovación continua, la optimización del sabor y la asequibilidad. Los fabricantes deben centrarse en formulaciones innovadoras, un abastecimiento de calidad y un marketing estratégico para aprovechar al máximo esta creciente demanda. El envasado mejorado, los formatos estables y las mezclas de proteínas multifuncionales también contribuyen al impulso del mercado.

Dinámica del mercado de proteínas veganas en América del Norte

Conductor

Aumentar la conciencia sobre la salud y la transición hacia dietas basadas en plantas

- El creciente interés por la salud está impulsando tanto a fabricantes como a minoristas a priorizar los productos proteicos de origen vegetal. Los consumidores buscan cada vez más alternativas a las proteínas animales tradicionales para la salud cardiovascular, el control de peso y el bienestar digestivo. Este cambio se ve reforzado por la creciente popularidad de los productos alimenticios naturales y de etiqueta limpia.

- La creciente conciencia sobre el impacto ambiental de la ganadería está impulsando a los consumidores hacia las opciones de proteína vegana. Esta tendencia impulsa a las marcas a ofrecer formulaciones vegetales más diversas e invertir en prácticas de abastecimiento sostenible. El énfasis en la reducción de la huella de carbono y los envases ecológicos también está fortaleciendo la preferencia de los consumidores por las proteínas vegetales.

- Gobiernos, organizaciones de nutrición y programas de bienestar promueven dietas basadas en plantas como parte de campañas de salud pública. Las iniciativas educativas y el apoyo de influencers del fitness y la salud impulsan aún más su adopción por parte de los consumidores. Las iniciativas que destacan los beneficios de la nutrición preventiva y los alimentos funcionales contribuyen al crecimiento constante del mercado.

- Por ejemplo, varias marcas implementaron recientemente campañas de concientización que enfatizan los beneficios nutricionales y ambientales de las proteínas veganas, lo que generó mayor visibilidad del producto y mayor interés del consumidor. Las campañas de promoción cruzada con plataformas de fitness, estilo de vida y bienestar han ayudado a expandir su alcance en el mercado.

- Si bien la concienciación sobre la salud y la sostenibilidad impulsan el crecimiento, la innovación de productos, la optimización del sabor y la expansión de la distribución siguen siendo cruciales para la expansión continua del mercado. Además, el desarrollo de proteínas híbridas y mezclas fortificadas está mejorando el atractivo funcional de los productos proteicos veganos.

Restricción/Desafío

Alto costo de las formulaciones de proteínas premium y preferencias de sabor

- Las proteínas vegetales en polvo, aisladas y mezclas premium suelen tener un precio más elevado que las fuentes de proteínas tradicionales, lo que limita su adopción entre los consumidores sensibles al precio. Esto restringe su uso generalizado en mercados emergentes y entre consumidores ocasionales. La producción rentable y el abastecimiento de ingredientes siguen siendo retos clave para los fabricantes.

- En muchas regiones, los consumidores pueden percibir las proteínas vegetales como menos apetecibles o menos efectivas que las proteínas animales. Los desafíos de sabor, textura y digestibilidad siguen afectando el comportamiento de compra recurrente. Las marcas están invirtiendo en enmascaramiento del sabor, mejora de la textura y combinaciones de proteínas para superar estas barreras.

- Las limitaciones de la cadena de suministro, como el abastecimiento de soja, guisantes, arroz u otros ingredientes ricos en proteínas de alta calidad, pueden generar cuellos de botella en la producción y precios minoristas más altos, lo que afecta la accesibilidad. Los retrasos en la disponibilidad de materias primas y las fluctuaciones en el suministro global también pueden perturbar la estabilidad del mercado.

- Por ejemplo, varias marcas de proteínas veganas revisaron recientemente sus envases, etiquetado y declaraciones nutricionales para garantizar la precisión y la transparencia, aumentando así la confianza del consumidor y fomentando la repetición de compras. Estas iniciativas también incluyeron campañas educativas para aclarar la calidad y los beneficios de las proteínas.

- Si bien la formulación y el sabor de los productos proteicos veganos siguen evolucionando, abordar los costos, las preferencias sensoriales y los desafíos de la cadena de suministro sigue siendo vital. Las partes interesadas deben centrarse en soluciones asequibles, de alta calidad y agradables al paladar para mantener el potencial de crecimiento a largo plazo. La inversión en investigación, producción escalable y fuentes alternativas de proteínas puede mejorar la accesibilidad y la rentabilidad.

Análisis del mercado de proteínas veganas en América del Norte

El mercado está segmentado según la fuente, el tipo de proteína, el nivel de hidrólisis, la forma, la naturaleza, la función y la aplicación.

- Por fuente

Según su origen, el mercado norteamericano de proteínas veganas se segmenta en proteína de soya, proteína de guisante, proteína de arroz, proteína de cáñamo, espirulina, proteína de quinoa, proteína de linaza, proteína de chía, proteína de canola, semilla de calabaza, entre otras. El segmento de proteína de soya registró la mayor participación en los ingresos del mercado en 2024, impulsado por su amplio uso en alimentos, bebidas y suplementos dietéticos. La proteína de soya es apreciada por su alto valor nutricional, sus aplicaciones versátiles y su consolidada cadena de suministro en diferentes países.

Se prevé que el segmento de proteína de guisante experimente el mayor crecimiento entre 2025 y 2032, impulsado por la creciente preferencia de los consumidores por fuentes de proteína vegetal sin alérgenos. La proteína de guisante es especialmente popular en proteínas en polvo, snacks y alimentos funcionales debido a su sabor neutro, alta digestibilidad y su idoneidad para formulaciones de etiqueta limpia.

- Por tipo de proteína

Según el tipo de proteína, el mercado norteamericano de proteínas veganas se segmenta en aislados, concentrados e hidrolizados. El segmento de aislados obtuvo la mayor participación en los ingresos en 2024 gracias a su alto contenido proteico, pureza y propiedades funcionales, ideales para bebidas y suplementos nutricionales.

Se prevé que el segmento de hidrolizados experimente el mayor crecimiento entre 2025 y 2032, impulsado por una mayor digestibilidad, una rápida absorción y su idoneidad para la nutrición deportiva y las aplicaciones clínicas. Los hidrolizados son populares entre los consumidores que buscan una utilización rápida y eficiente de las proteínas.

- Por nivel de hidrólisis

Según el nivel de hidrólisis, el mercado norteamericano de proteínas veganas se segmenta en proteínas intactas, ligeramente hidrolizadas y fuertemente hidrolizadas. El segmento intacto dominó en 2024 gracias a su perfil nutricional equilibrado y su relación calidad-precio para el consumo diario.

Se espera que el segmento ligeramente hidrolizado experimente la tasa de crecimiento más rápida entre 2025 y 2032, impulsado por una mejor solubilidad, rendimiento funcional y digestibilidad, lo que lo hace ideal para bebidas fortificadas y formulaciones de proteínas especializadas.

- Por formulario

En cuanto a su forma, el mercado norteamericano de proteínas veganas se segmenta en proteínas secas y líquidas. El segmento seco obtuvo la mayor participación en los ingresos del mercado en 2024 gracias a su fácil almacenamiento, larga vida útil y su aplicabilidad en proteínas en polvo, barras y productos de panadería.

Se espera que el segmento de líquidos experimente la tasa de crecimiento más rápida entre 2025 y 2032, impulsada por la creciente demanda de bebidas listas para beber, batidos y bebidas funcionales enriquecidas con proteínas entre los consumidores preocupados por la salud.

- Por naturaleza

Basándose en la naturaleza, el mercado norteamericano de proteínas veganas se segmenta en proteínas convencionales y orgánicas. El segmento convencional lideró el mercado en 2024, gracias a una sólida infraestructura de fabricación y a su asequibilidad.

Se espera que el segmento orgánico sea testigo de la tasa de crecimiento más rápida entre 2025 y 2032, impulsado por la creciente preferencia de los consumidores por proteínas de origen vegetal, no transgénicas, de etiqueta limpia y de origen sostenible en América del Norte.

- Por función

En función de su función, el mercado norteamericano de proteínas veganas se segmenta en solubilidad, emulsificación, gelificación, retención de agua, formación de espuma, entre otros. El segmento de solubilidad tuvo la mayor participación de mercado en 2024 debido a su importancia en bebidas, batidos y alimentos funcionales.

Se espera que los segmentos de emulsificación y gelificación experimenten la tasa de crecimiento más rápida entre 2025 y 2032, impulsados por el aumento del uso de proteínas veganas en panadería, alternativas lácteas y aplicaciones de alimentos procesados para mejorar la textura y la estabilidad.

- Por aplicación

En cuanto a su aplicación, el mercado norteamericano de proteínas veganas se segmenta en productos alimenticios, bebidas, nutracéuticos y suplementos dietéticos, cosméticos y cuidado personal, piensos, productos farmacéuticos, entre otros. El segmento de productos alimenticios dominó en 2024 debido a la alta incorporación de proteínas vegetales en productos de panadería, snacks y repostería.

Se espera que el segmento de nutracéuticos y suplementos dietéticos experimente la tasa de crecimiento más rápida entre 2025 y 2032, impulsado por la creciente adopción de alimentos funcionales enriquecidos con proteínas, suplementos de bienestar y bebidas fortificadas.

Análisis regional del mercado de proteínas veganas en América del Norte

- El mercado estadounidense de proteínas veganas captó la mayor participación en los ingresos de Norteamérica en 2024, impulsado por la alta concienciación de los consumidores sobre las dietas basadas en plantas, la salud y la sostenibilidad. Los consumidores priorizan cada vez más los alimentos, bebidas y suplementos dietéticos enriquecidos con proteínas, lo que impulsa la demanda de polvos, barras y productos funcionales veganos.

- La creciente presencia de marcas consolidadas de proteína vegana, combinada con redes de distribución avanzadas, impulsa un crecimiento constante del mercado. El creciente interés en productos de etiqueta limpia, sin alérgenos y fortificados acelera aún más su adopción.

- Las iniciativas de marketing que enfatizan los beneficios nutricionales y el impacto ambiental también contribuyen a la preferencia del consumidor y a la expansión de las ventas.

Análisis del mercado de proteínas veganas en Canadá

Se prevé que el mercado canadiense de proteínas veganas experimente su mayor crecimiento entre 2025 y 2032, impulsado por una mayor concienciación sobre la salud, el aumento de las tendencias de fitness y la creciente concienciación sobre las dietas sostenibles. Los consumidores buscan productos proteicos de origen vegetal prácticos, como polvos, barritas y bebidas listas para beber, para su nutrición diaria. La expansión del comercio minorista, las plataformas en línea y las tiendas especializadas están facilitando una mejor accesibilidad y penetración en el mercado. La adopción de fórmulas sin alérgenos y de etiqueta limpia contribuye a este rápido crecimiento. Además, los lanzamientos de productos innovadores y las campañas de marketing centradas en los beneficios funcionales impulsan la continua expansión del mercado.

Cuota de mercado de proteínas veganas en América del Norte

La industria de proteínas veganas de América del Norte está liderada principalmente por empresas bien establecidas, entre las que se incluyen:

- Beyond Meat (EE. UU.)

- Impossible Foods (EE. UU.)

- SunOpta (Canadá)

- Vega (Canadá)

- Naked Nutrition (EE. UU.)

- Jardín de la Vida (EE. UU.)

- Bob's Red Mill (EE. UU.)

- Orgain (EE. UU.)

- NOW Foods (EE. UU.)

- Cosecha de Manitoba (Canadá)

Últimos avances en el mercado de proteínas veganas en América del Norte

- En marzo de 2023, la Biblioteca Nacional de Medicina publicó un artículo de investigación como parte de su iniciativa de desarrollo del conocimiento, centrado en el papel de las dietas basadas en plantas en la mejora de la salud y la reducción del impacto ambiental. El estudio destacó la creciente demanda de proteínas veganas por parte de los consumidores, impulsada por sus beneficios nutricionales y ventajas de sostenibilidad. Se espera que este avance fomente una mayor adopción de proteínas vegetales, creando nuevas oportunidades de crecimiento para los fabricantes. Es probable que el énfasis en la salud y el consumo ecológico tenga un impacto positivo en el mercado de las proteínas veganas, fomentando la concienciación y fortaleciendo la confianza de los consumidores en las soluciones basadas en plantas.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.