Mercado de equipos de fabricación de semiconductores de América del Norte , por tipo de equipo (equipo front-end y equipo back-end), dimensiones (3D, 2.5D y 2D), tipo de producto (memoria, MEMS, fundición, analógico, MPU, lógica, discreto, otros), participante de la cadena de suministro (fundición, empresas de ensamblaje y prueba de semiconductores subcontratadas (OSAT) y empresas de fabricación de dispositivos integrados (IDM)) y equipo de instalaciones de fabricación (automatización de fábrica, equipo de control de gas, equipo de control químico) - Tendencias de la industria y pronóstico hasta 2030.

Análisis y perspectivas del mercado de equipos de fabricación de semiconductores de América del Norte

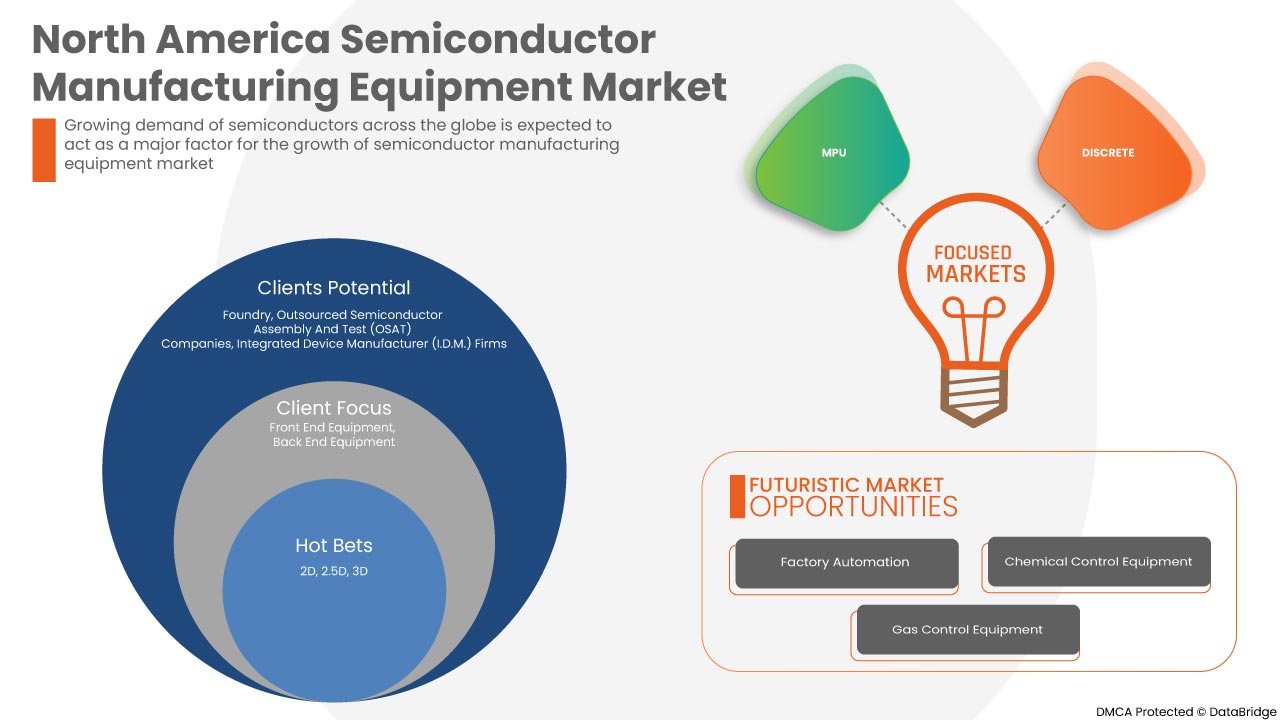

El mercado de equipos de fabricación de semiconductores está creciendo sustancialmente debido a la mayor adopción de equipos de semiconductores en dispositivos conectados y la industria automotriz. A medida que los diseños de circuitos integrados se vuelven más complejos, se incorporan más productos semiconductores en la creación de circuitos integrados. El semiconductor se ha convertido en parte integral del proceso de diseño electrónico, ya que ayuda a reducir el costo del desarrollo de circuitos integrados, aumenta el valor del producto final, acelera el tiempo de comercialización y reduce el tiempo de volumen. Ayuda a las empresas a llenar el vacío de diseño de circuitos integrados.

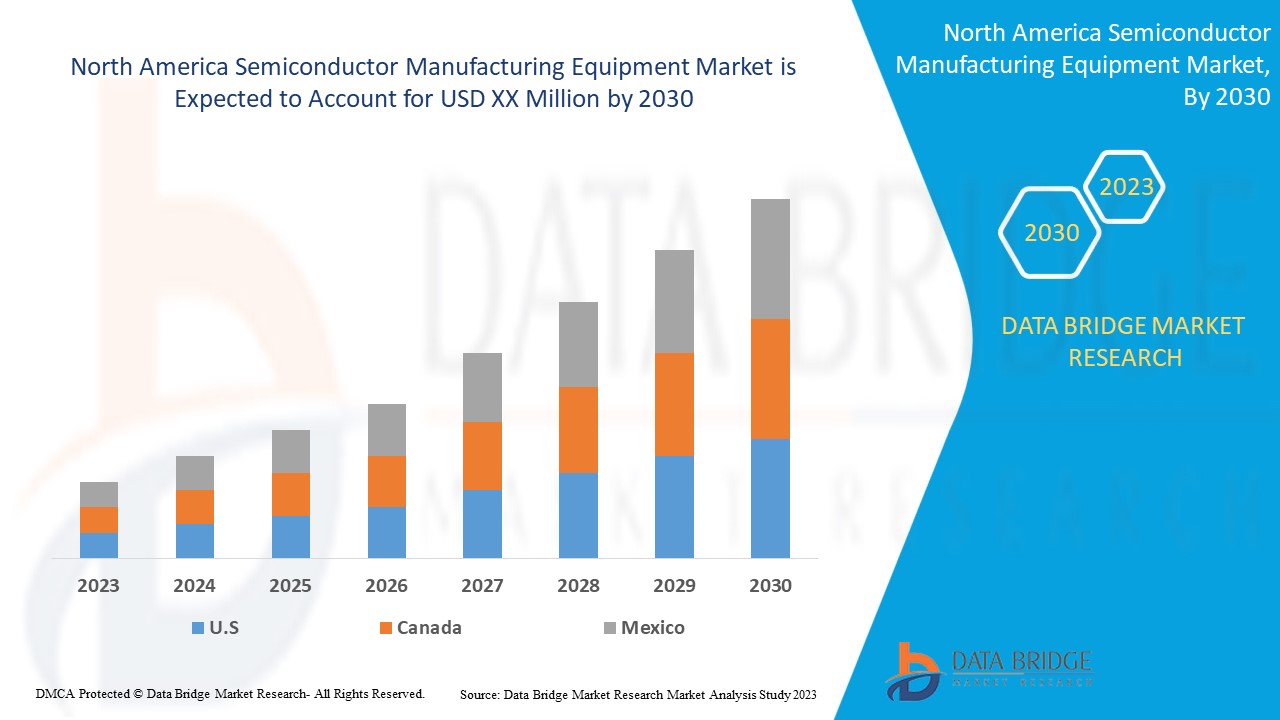

Data Bridge Market Research analiza que el mercado de equipos de fabricación de semiconductores de América del Norte crecerá a una CAGR del 9,1 % durante el período de pronóstico de 2023 a 2030.

|

Métrica del informe |

Detalles |

|

Período de pronóstico |

2023 a 2030 |

|

Año base |

2022 |

|

Años históricos |

2021 (Personalizable para 2020 - 2015) |

|

Unidades cuantitativas |

Ingresos en millones de USD, volúmenes en unidades, precios en USD |

|

Segmentos cubiertos |

Por tipo de equipo (equipo front-end y equipo back-end), dimensiones (3D, 2.5D y 2D), tipo de producto (memoria, MEMS, fundición, analógico, MPU, lógico, discreto, otros), participante de la cadena de suministro (fundición, empresas de ensamblaje y prueba de semiconductores subcontratadas (OSAT) y empresas de fabricación de dispositivos integrados (IDM)) y equipo de la instalación de fabricación ( automatización de fábrica , equipo de control de gas, equipo de control químico). |

|

Países cubiertos |

Estados Unidos, Canadá y México en América del Norte. |

|

Actores del mercado cubiertos |

Español ASML, KLA Corporation, Plasma-Therm, LAM RESEARCH CORPORATION, Veeco Instruments Inc., EV Group, Tokyo Electron Limited, Canon Machinery Inc., Nordson Corporation, Hitachi High-Tech Corporation, Advanced Dicing Technologies, Evatec AG, NOIVION, Modutek.com, QP Technologies, Applied Materials, Inc., SCREEN Holdings Co., Ltd., Teradyne Inc., Onto Innovation, ADVANTEST CORPORATION, TOKYO SEIMITSU CO., LTD., SÜSS MicroTec SE, ASMPT, FormFactor, UNITES Systems as, Gigaphoton Inc. y Palomar Technologies, entre otros. |

Definición de equipo de fabricación de semiconductores

El término "equipo para semiconductores" hace referencia, en general, al equipo de producción necesario para producir diversos productos semiconductores y pertenece al eslabón de apoyo clave de la cadena de la industria de semiconductores. El equipo para semiconductores es el líder tecnológico en la industria de semiconductores. El diseño de chips, la fabricación de obleas y el empaquetado y las pruebas deben diseñarse y fabricarse dentro del alcance de la tecnología de equipos. El avance de la tecnología de equipos también promueve el desarrollo de la industria de semiconductores.

Dinámica del mercado de equipos de fabricación de semiconductores

En esta sección se aborda la comprensión de los factores impulsores del mercado, las ventajas, las oportunidades, las limitaciones y los desafíos. Todo esto se analiza en detalle a continuación:

Conductores

-

AUMENTO DEL CONSUMO DE PRODUCTOS ELECTRÓNICOS DE CONSUMO

El aumento de los ingresos disponibles de los consumidores y la necesidad de productos electrónicos avanzados impulsan el mercado de la electrónica de consumo . Los consumidores se están volviendo expertos en tecnología y están adoptando nuevas tecnologías en el trabajo, en las rutinas diarias, en el entretenimiento personal y en otros ámbitos. Los dispositivos inteligentes están acaparando la mayor parte del mercado debido a la mejora del control, las características y otras funciones. Los consumidores están dispuestos a gastar dinero extra en aparatos avanzados para mejorar sus experiencias y su nivel de vida. Los productos electrónicos flexibles equipados con sensores flexibles están disponibles en el mercado en la categoría de productos premium; por lo tanto, la aceptación de los productos premium está impulsando el crecimiento del mercado.

-

CRECIENTE DEMANDA DE SEMICONDUCTORES EN TODO EL MUNDO

Una sustancia con propiedades eléctricas especializadas llamada semiconductor puede utilizarse como base para ordenadores y otros dispositivos electrónicos. Normalmente, se trata de un elemento o compuesto químico sólido que, en algunas circunstancias, transmite electricidad, pero en otras no. Por ello, es el medio perfecto para controlar la corriente eléctrica y los aparatos eléctricos comunes.

Los semiconductores son dispositivos eléctricos microscópicos compuestos de silicio, germanio o arseniuro de galio. La industria de los semiconductores desarrolla y produce semiconductores. Casi todos los dispositivos electrónicos incluyen semiconductores, incluidos televisores, computadoras, herramientas de diagnóstico médico, teléfonos celulares y videojuegos. La tecnología de tubos de vacío grandes y engorrosos del pasado ha sido reemplazada por los semiconductores modernos, cada vez más pequeños, gracias a los avances realizados en la industria de los semiconductores desde 1960, lo que permitió la creación de dispositivos electrónicos más pequeños, más rápidos y aún más confiables. Las empresas y fabricantes de productos electrónicos en los Estados Unidos, Japón, China, Corea del Sur, Francia e Italia actualmente conforman el sector de semiconductores de USD 300 mil millones.

Oportunidad

-

EL AUMENTO DE LA CADENA DE SUMINISTRO DIGITAL EN TODO EL MUNDO

Una cadena de suministro que utiliza análisis de datos y tecnologías digitales para tomar decisiones, mejorar el rendimiento y reaccionar rápidamente a circunstancias cambiantes se conoce como "cadena de suministro digital". Las redes de suministro digitales se basan fundamentalmente en datos generados por las cadenas de suministro actuales, que se almacenan en almacenes de datos y se evalúan para obtener información útil.

Como paso inicial necesario, las tecnologías de gestión de la cadena de suministro históricas, como la planificación de la demanda, la gestión de activos, el sistema de gestión de almacenes , la gestión del transporte y la logística, las compras y el cumplimiento de pedidos, deben estar totalmente integradas. Sin embargo, para digitalizar una cadena de suministro, también es necesario extraer datos de esas operaciones y equipar el equipo que les permita proporcionar los datos necesarios.

La aparición de la nube, la implementación de la tecnología 5G, los vehículos conectados y la digitalización han contribuido a una demanda nunca antes vista de computación de alto rendimiento. El mercado de semiconductores, el más codiciado, también está compitiendo para subirse al tren de la digitalización. Un elemento clave para mejorar la resiliencia de la cadena de suministro es el conocimiento de los datos. Las empresas de semiconductores pueden tomar decisiones más rápidas basadas en datos si utilizan tecnología y aplicaciones para capturar datos y análisis precisos en todos los puntos de la cadena de suministro.

Restricciones/Desafíos

- ALTERACIÓN EN LA CADENA DE SUMINISTRO DE LA INDUSTRIA

La guerra por los semiconductores, disputada específicamente por las industrias automotriz y de consumo de alta tecnología, es uno de los mayores problemas de América del Norte que afectan a las cadenas de suministro en industrias especializadas.

La pandemia de Covid-19, que paralizó la fabricación de automóviles y disparó el consumo de productos electrónicos domésticos en América del Norte, fue la principal causa del conflicto. Sin embargo, el origen del problema es anterior al confinamiento en América del Norte.

La fabricación disminuyó repentinamente en 2020 debido a la cancelación apresurada de pedidos y a los procedimientos justo a tiempo cuando comenzó el confinamiento por la pandemia. Sin embargo, a medida que los clientes utilizaban más computadoras portátiles, teléfonos 5G, consolas de juegos y otros dispositivos .TIT, la demanda de chips de silicio se disparó debido a las circunstancias laborales de la epidemia. Una recuperación en forma de V para las computadoras personales, los dispositivos móviles, los automóviles y las comunicaciones inalámbricas fue el resultado de una caída en la demanda de semiconductores a fines de 2020.

Desarrollo reciente

- En septiembre de 2022, Onto Innovation anunció su primer lote para entregar el sistema Dragonfly G3 de la empresa con el nuevo módulo EB40 a uno de los tres principales fabricantes de semiconductores. Esto ayuda a la empresa a ampliar su cartera de productos y su oferta en el mercado.

Alcance del mercado de equipos de fabricación de semiconductores

El mercado de equipos de fabricación de semiconductores está segmentado en función del tipo de equipo, las dimensiones, el tipo de producto, el participante de la cadena de suministro y el equipo de la planta de fabricación. El crecimiento entre estos segmentos le ayudará a analizar los segmentos de crecimiento reducido en las industrias y brindará a los usuarios una valiosa descripción general del mercado y conocimientos del mercado para ayudarlos a tomar decisiones estratégicas para identificar las principales aplicaciones del mercado.

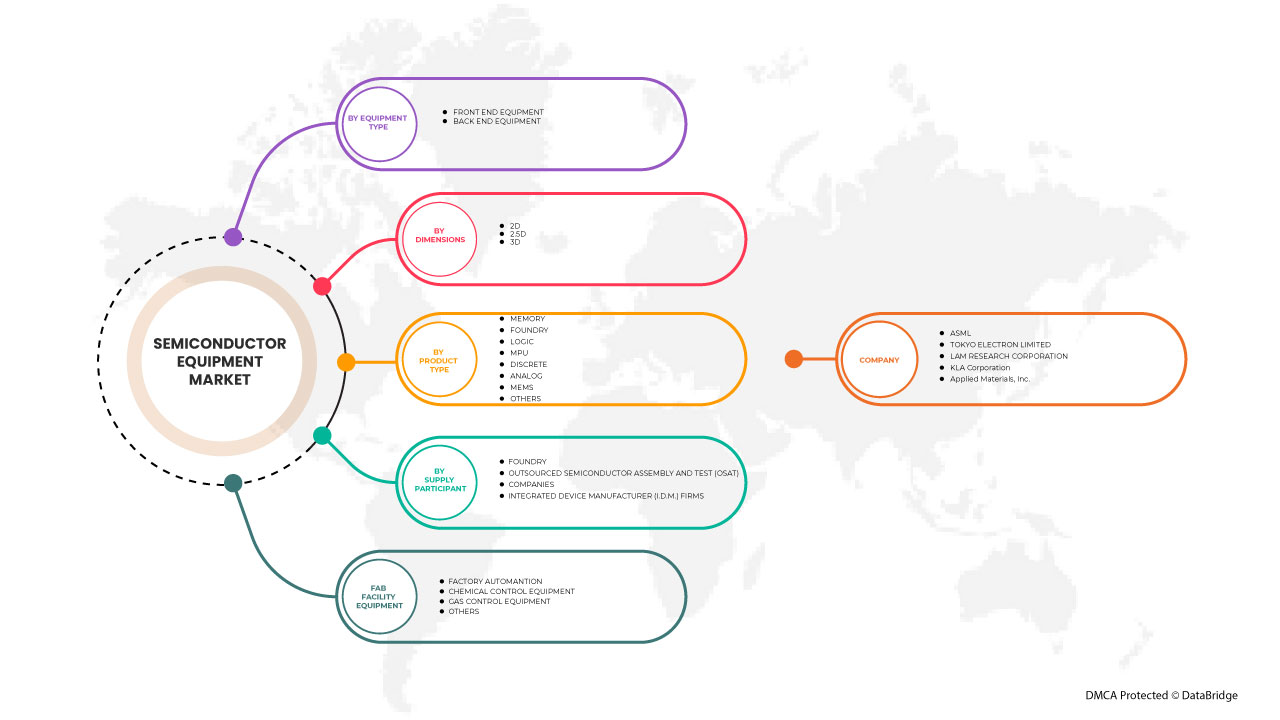

Tipo de equipo

- Equipo de Front End

- Equipo de back-end

Según el tipo de equipo, el mercado se segmenta en equipos frontales y equipos posteriores.

Dimensiones

- 2D

- 2.5D

- 3D

En función de las dimensiones, el mercado está segmentado en 2D, 2,5D y 3D.

Tipo de producto

- Memoria

- Fundición

- Lógica

- Unidad de potencia multimolecular

- Discreto

- Cosa análoga

- MEMS

- Otro

Según el tipo de producto, el mercado está segmentado en memoria, fundición, lógica, MPU, discreto, analógico, MEMS y otros.

Participante de la cadena de suministro

- Fundición

- Empresas subcontratadas de ensamblaje y prueba de semiconductores (OSAT)

- Empresas fabricantes de dispositivos integrados (IDM)

Sobre la base de los participantes de la cadena de suministro, el mercado está segmentado en fundiciones, empresas de ensamblaje y prueba de semiconductores subcontratadas (OSAT) y empresas fabricantes de dispositivos integrados (IDM).

Equipos para instalaciones de fabricación

- Automatización de fábrica

- Equipos de control químico

- Equipos de control de gas

- Otro

Sobre la base de los equipos de las instalaciones de fabricación, el mercado está segmentado en automatización de fábrica, equipos de control químico, equipos de control de gas y otros.

Análisis y perspectivas regionales del mercado de equipos de fabricación de semiconductores

Se analiza el mercado de equipos de fabricación de semiconductores y se proporcionan información y tendencias del tamaño del mercado por tipo de equipo, dimensiones, tipo de producto, participante de la cadena de suministro y equipos de las instalaciones de fabricación.

Los países cubiertos en el informe del mercado de equipos de fabricación de semiconductores son Estados Unidos, Canadá y México en América del Norte.

En América del Norte, se espera que Estados Unidos domine el mercado debido al aumento de la cadena de suministro digital en todo el mundo.

La sección de países del informe también proporciona factores de impacto de mercado individuales y cambios en las regulaciones en el mercado a nivel nacional que afectan las tendencias actuales y futuras del mercado. Los puntos de datos como nuevas ventas, ventas de reemplazo, demografía del país, epidemiología de enfermedades y aranceles de importación y exportación son algunos de los principales indicadores utilizados para pronosticar el escenario del mercado para países individuales. Además, la presencia y disponibilidad de marcas de América del Norte y sus desafíos enfrentados debido a la competencia grande o escasa de las marcas locales y nacionales, el impacto de los canales de venta se consideran al proporcionar un análisis de pronóstico de los datos del país.

Análisis del panorama competitivo y de la cuota de mercado de los equipos de fabricación de semiconductores

El panorama competitivo del mercado de equipos de fabricación de semiconductores proporciona detalles por competidor. Los detalles incluidos son una descripción general de la empresa, las finanzas de la empresa, los ingresos generados, el potencial de mercado, la inversión en investigación y desarrollo, las nuevas iniciativas de mercado, la presencia en América del Norte, los sitios e instalaciones de producción, las capacidades de producción, las fortalezas y debilidades de la empresa, el lanzamiento de soluciones, la amplitud y la variedad de productos, el dominio de las aplicaciones. Los puntos de datos anteriores proporcionados solo están relacionados con el enfoque de las empresas en relación con el mercado de equipos de fabricación de semiconductores.

Algunos de los principales actores que operan en el mercado de equipos de fabricación de semiconductores de América del Norte son ASML, KLA Corporation, Plasma-Therm, LAM RESEARCH CORPORATION, Veeco Instruments Inc., EV Group, Tokyo Electron Limited, Canon Machinery Inc., Nordson Corporation, Hitachi High-Tech Corporation, Advanced Dicing Technologies, Evatec AG, NOIVION, Modutek.com, QP Technologies, Applied Materials, Inc., SCREEN Holdings Co., Ltd., Teradyne Inc., Onto Innovation, ADVANTEST CORPORATION, TOKYO SEIMITSU CO., LTD., SÜSS MicroTec SE, ASMPT, FormFactor, UNITES Systems as, Gigaphoton Inc. y Palomar Technologies, entre otros.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Tabla de contenido

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELING

2.9 COMPONENT TYPE TIMELINE CURVE

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 INCREASING CONSUMPTION OF CONSUMER ELECTRONICS

5.1.2 GROWING DEMAND FOR SEMICONDUCTORS ACROSS THE GLOBE

5.1.3 EMERGENCE OF A LARGE NUMBER OF SEMICONDUCTOR MANUFACTURING FACILITIES

5.1.4 TECHNOLOGICAL ADVANCEMENTS AND THE ADOPTION OF INNOVATIVE TECHNOLOGIES SUCH AS ARTIFICIAL INTELLIGENCE AND BLOCKCHAIN

5.1.5 GROWING ADOPTION OF IOT ACROSS THE SEMICONDUCTOR INDUSTRY

5.2 RESTRAINTS

5.2.1 HIGH COMPETITION IN THE SEMICONDUCTOR MANUFACTURING MARKET

5.2.2 HIGH R&D COST IN THE SEMICONDUCTOR EQUIPMENT MARKET

5.3 OPPORTUNITIES

5.3.1 RISE IN DIGITAL SUPPLY CHAIN ACROSS THE GLOBE

5.3.2 INTRODUCTION OF KERFLESS WAFER OVER TRADITIONAL WAFER

5.3.3 VERY HIGH GROWTH OF THE AUTOMOBILE INDUSTRY

5.4 CHALLENGES

5.4.1 DISRUPTION IN THE SUPPLY CHAIN INDUSTRY

5.4.2 ENVIRONMENTAL CONCERNS RAISED DUE TO SEMICONDUCTOR PRODUCTION

6 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE

6.1 OVERVIEW

6.2 FRONT END EQUIPMENT

6.2.1 LITHOGRAPHY

6.2.1.1 DUV

6.2.1.2 EUV

6.2.2 DEPOSITION

6.2.2.1 PVD

6.2.2.2 CVD

6.2.3 WAFER SURFACE CONDITIONING

6.2.3.1 ETCHING

6.2.3.2 CHEMICAL

6.2.4 CLEANING

6.2.4.1 BATCH SPRAY CLEANING SYSTEM

6.2.4.2 SINGLE-WAFER SPRAY SYSTEM

6.2.4.3 SINGLE-WAFER CRYOGENIC SYSTEM

6.2.4.4 BATCH IMMERSION CLEANING SYSTEM

6.2.4.5 SCRUBBER

6.2.5 OTHER EQUIPMENT

6.3 BACK END EQUIPMENT

6.3.1 TESTING

6.3.2 ASSEMBLY AND PACKING

6.3.3 DICING EQUIPMENT

6.3.4 BONDING EQUIPMENT

6.3.5 METROLOGY

7 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS

7.1 OVERVIEW

7.2 3D

7.3 2.5D

7.4 2D

8 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE

8.1 OVERVIEW

8.2 MEMORY

8.3 MEMS

8.4 FOUNDRY

8.5 ANALOG

8.6 MPU

8.7 LOGIC

8.8 DISCRETE

8.9 OTHERS

9 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT

9.1 OVERVIEW

9.2 INTEGRATED DEVICE MANUFACTURER (IDM) FIRMS

9.3 FOUNDRY

9.4 OUTSOURCED SEMICONDUCTOR ASSEMBLY AND TEST (OSAT) COMPANIES

10 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT

10.1 OVERVIEW

10.2 FACTORY AUTOMATION

10.2.1 FRONT END EQUIPMENT

10.2.2 BACK END EQUIPMENT

10.3 GAS CONTROL EQUIPMENT

10.3.1 FRONT END EQUIPMENT

10.3.2 BACK END EQUIPMENT

10.4 CHEMICAL CONTROL EQUIPMENT

10.4.1 FRONT END EQUIPMENT

10.4.2 BACK END EQUIPMENT

10.5 OTHERS

11 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION

11.1 NORTH AMERICA

11.1.1 U.S.

11.1.2 CANADA

11.1.3 MEXICO

12 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 ASML

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENT

14.2 TOKYO ELECTRON LIMITED

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENTS

14.3 LAM RESEARCH CORPORATION

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENT

14.4 KLA CORPORATION

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENT

14.5 APPLIED MATERIALS, I.N.C.

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT AND TECHNOLOGIES PORTFOLIO

14.5.5 RECENT DEVELOPMENTS

14.6 ADVANCED DICING TECHNOLOGIES

14.6.1 COMPANY SNAPSHOT

14.6.2 PRODUCT PORTFOLIO

14.6.3 RECENT DEVELOPMENTS

14.7 ADVANTEST CORPORATION

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCTS PORTFOLIO

14.7.4 RECENT DEVELOPMENTS

14.8 ASMPT

14.8.1 COMPANY SNAPSHOT

14.8.2 REVENUE ANALYSIS

14.8.3 PRODUCTS PORTFOLIO

14.8.4 RECENT DEVELOPMENTS

14.9 CANON MACHINERY INC.

14.9.1 COMPANY SNAPSHOT

14.9.2 PRODUCT PORTFOLIO

14.9.3 RECENT DEVELOPMENT

14.1 EV GROUP

14.10.1 COMPANY SNAPSHOT

14.10.2 PRODUCT PORTFOLIO

14.10.3 RECENT DEVELOPMENTS

14.11 EVATEC AG

14.11.1 COMPANY SNAPSHOT

14.11.2 PRODUCT PORTFOLIO

14.11.3 RECENT DEVELOPMENT

14.12 FORMFACTOR.

14.12.1 COMPANY SNAPSHOT

14.12.2 REVENUE ANALYSIS

14.12.3 PRODUCTS PORTFOLIO

14.12.4 RECENT DEVELOPMENTS

14.13 GIGAPHOTON INC.

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCTS PORTFOLIO

14.13.3 RECENT DEVELOPMENTS

14.14 HITACHI HIGH-TECH CORPORATION

14.14.1 COMPANY SNAPSHOT

14.14.2 PRODUCT PORTFOLIO

14.14.3 RECENT DEVELOPMENTS

14.15 MODUTEK CORPORATION

14.15.1 COMPANY SNAPSHOT

14.15.2 PRODUCT PORTFOLIO

14.15.3 RECENT DEVELOPMENTS

14.16 NOIVION S.R.L.

14.16.1 COMPANY SNAPSHOT

14.16.2 PRODUCT PORTFOLIO

14.16.3 RECENT DEVELOPMENTS

14.17 NORDSON CORPORATION

14.17.1 COMPANY SNAPSHOT

14.17.2 REVENUE ANALYSIS

14.17.3 PRODUCT PORTFOLIO

14.17.4 RECENT DEVELOPMENTS

14.18 ONTO INNOVATION.

14.18.1 COMPANY SNAPSHOT

14.18.2 REVENUE ANALYSIS

14.18.3 PRODUCTS PORTFOLIO

14.18.4 RECENT DEVELOPMENTS

14.19 PALOMAR TECHNOLOGIES

14.19.1 COMPANY SNAPSHOT

14.19.2 PRODUCTS PORTFOLIO

14.19.3 RECENT DEVELOPMENTS

14.2 PLASMA-THERM

14.20.1 COMPANY SNAPSHOT

14.20.2 PRODUCT PORTFOLIO

14.20.3 RECENT DEVELOPMENTS

14.21 QP TECHNOLOGIES

14.21.1 COMPANY SNAPSHOT

14.21.2 SERVICE PORTFOLIO

14.21.3 RECENT DEVELOPMENT

14.22 SCREEN HOLDINGS CO., LTD.

14.22.1 COMPANY SNAPSHOT

14.22.2 REVENUE ANALYSIS

14.22.3 PRODUCTS PORTFOLIO

14.22.4 RECENT DEVELOPMENTS

14.23 SÜSS MICROTEC SE

14.23.1 COMPANY SNAPSHOT

14.23.2 REVENUE ANALYSIS

14.23.3 PRODUCT PORTFOLIO

14.23.4 RECENT DEVELOPMENTS

14.24 TERADYNE INC.

14.24.1 COMPANY SNAPSHOT

14.24.2 REVENUE ANALYSIS

14.24.3 PRODUCTS PORTFOLIO

14.24.4 RECENT DEVELOPMENTS

14.25 TOKYO SEIMITSU CO., LTD

14.25.1 COMPANY SNAPSHOT

14.25.2 REVENUE ANALYSIS

14.25.3 PRODUCTS PORTFOLIO

14.25.4 RECENT DEVELOPMENTS

14.26 UNITES SYSTEMS A.S.

14.26.1 COMPANY SNAPSHOT

14.26.2 PRODUCT PORTFOLIO

14.26.3 RECENT DEVELOPMENTS

14.27 VEECO INSTRUMENTS INC.

14.27.1 COMPANY SNAPSHOT

14.27.2 REVENUE ANALYSIS

14.27.3 PRODUCT PORTFOLIO

14.27.4 RECENT DEVELOPMENT

15 QUESTIONNAIRE

16 RELATED REPORTS

Lista de Tablas

TABLE 1 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 2 NORTH AMERICA FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 3 NORTH AMERICA FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 4 NORTH AMERICA LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 5 NORTH AMERICA DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 6 NORTH AMERICA WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 7 NORTH AMERICA CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 8 NORTH AMERICA BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 9 NORTH AMERICA BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 10 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 11 NORTH AMERICA 3D IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 12 NORTH AMERICA 2.5D IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 13 NORTH AMERICA 2D IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 14 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 15 NORTH AMERICA MEMORY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 16 NORTH AMERICA MEMS IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 17 NORTH AMERICA FOUNDRY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 18 NORTH AMERICA ANALOG IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 19 NORTH AMERICA MPU IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 20 NORTH AMERICA LOGIC IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 21 NORTH AMERICA DISCRETE IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 22 NORTH AMERICA OTHERS IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 23 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 24 NORTH AMERICA INTEGRATED DEVICE MANUFACTURER (IDM) FIRMS IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 25 NORTH AMERICA FOUNDRY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 26 NORTH AMERICA OUTSOURCED SEMICONDUCTOR ASSEMBLY AND TEST (OSAT) COMPANIES IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 27 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 28 NORTH AMERICA FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 29 NORTH AMERICA FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 30 NORTH AMERICA GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 31 NORTH AMERICA GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 32 NORTH AMERICA CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 33 NORTH AMERICA CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 34 NORTH AMERICA OTHERS IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY REGION, 2021-2030 (USD MILLION)

TABLE 35 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY COUNTRY, 2021-2030 (USD MILLION)

TABLE 36 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 37 NORTH AMERICA FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 38 NORTH AMERICA LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 39 NORTH AMERICA DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 40 NORTH AMERICA WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 41 NORTH AMERICA CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 42 NORTH AMERICA BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 43 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 44 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 45 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 46 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 47 NORTH AMERICA FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 48 NORTH AMERICA GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 49 NORTH AMERICA CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 50 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 51 U.S. FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 52 U.S. LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 53 U.S. DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 54 U.S. WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 55 U.S. CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 56 U.S. BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 57 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 58 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 59 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 60 U.S. SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 61 U.S. FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 62 U.S. GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 63 U.S. CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 64 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 65 CANADA FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 66 CANADA LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 67 CANADA DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 68 CANADA WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 69 CANADA CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 70 CANADA BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 71 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 72 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 73 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 74 CANADA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 75 CANADA FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 76 CANADA GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 77 CANADA CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 78 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 79 MEXICO FRONT END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 80 MEXICO LITHOGRAPHY IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 81 MEXICO DEPOSITION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 82 MEXICO WAFER SURFACE CONDITIONING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 83 MEXICO CLEANING IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY INDUSTRY, 2021-2030 (USD MILLION)

TABLE 84 MEXICO BACK END EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY TYPE, 2021-2030 (USD MILLION)

TABLE 85 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY DIMENSIONS, 2021-2030 (USD MILLION)

TABLE 86 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY PRODUCT TYPE, 2021-2030 (USD MILLION)

TABLE 87 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY SUPPLY CHAIN PARTICIPANT, 2021-2030 (USD MILLION)

TABLE 88 MEXICO SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY FAB FACILITY EQUIPMENT, 2021-2030 (USD MILLION)

TABLE 89 MEXICO FACTORY AUTOMATION IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 90 MEXICO GAS CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

TABLE 91 MEXICO CHEMICAL CONTROL EQUIPMENT IN SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE, 2021-2030 (USD MILLION)

Lista de figuras

FIGURE 1 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET :DBMR MARKET POSITION GRID

FIGURE 8 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: VENDOR SHARE ANALYSIS

FIGURE 9 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: SEGMENTATION

FIGURE 10 GROWING DEMAND FOR SEMICONDUCTOR ACROSS THE GLOBE IS BOOSTING THE GROWTH OF THE SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET IN THE FORECAST PERIOD OF 2023 -2030

FIGURE 11 EQUIPMENT TYPE SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET IN 2023 - 2030

FIGURE 12 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET

FIGURE 13 DESKTOP VS MOBILE VS TABLET MARKET SHARE WORLDWIDE, APRIL 2020

FIGURE 14 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY EQUIPMENT TYPE, 2022

FIGURE 15 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY DIMENSIONS, 2022

FIGURE 16 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY PRODUCT TYPE, 2022

FIGURE 17 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY SUPPLY CHAIN PARTICIPANT, 2022

FIGURE 18 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY FAB FACILITY EQUIPMENT, 2022

FIGURE 19 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: SNAPSHOT (2022)

FIGURE 20 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY COUNTRY (2022)

FIGURE 21 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY COUNTRY (2023 & 2030)

FIGURE 22 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY COUNTRY (2022 & 2030)

FIGURE 23 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: BY EQUIPMENT TYPE (2023-2030)

FIGURE 24 NORTH AMERICA SEMICONDUCTOR MANUFACTURING EQUIPMENT MARKET: COMPANY SHARE 2022 (%)

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.