North America Genetic Testing Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

5,688.94 Billion

USD

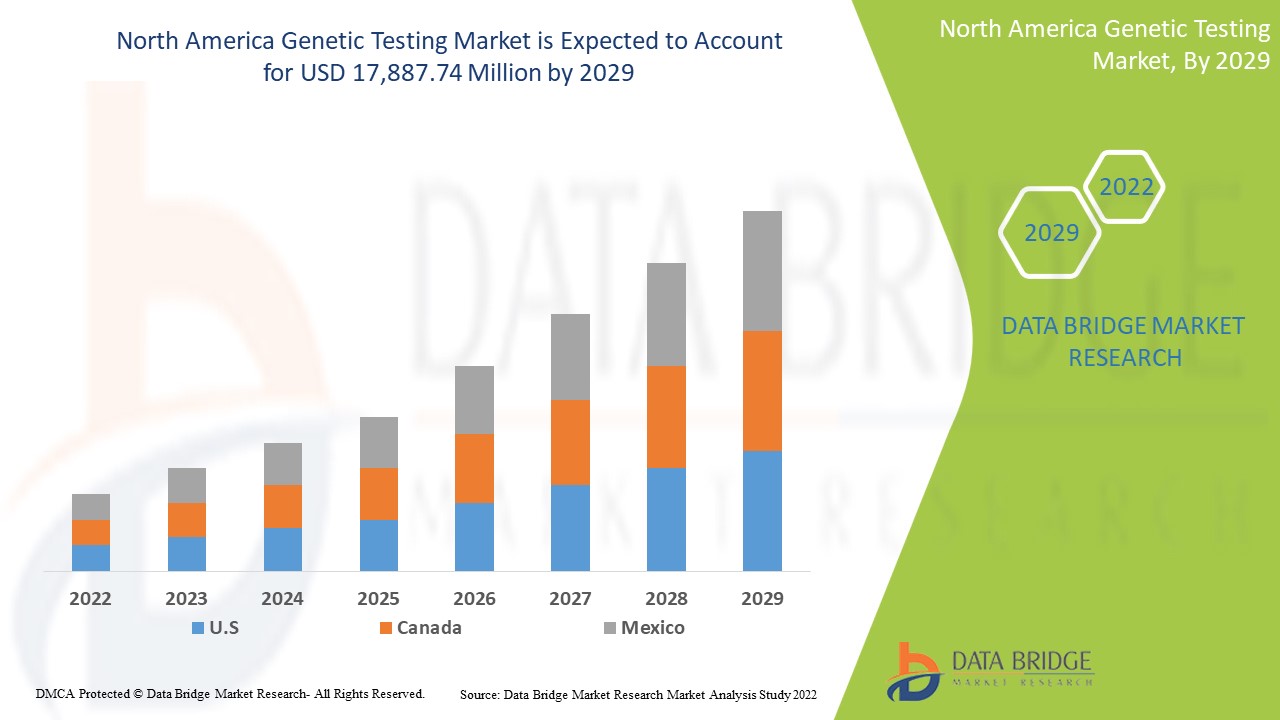

17,887.74 Billion

2021

2029

USD

5,688.94 Billion

USD

17,887.74 Billion

2021

2029

| 2022 –2029 | |

| USD 5,688.94 Billion | |

| USD 17,887.74 Billion | |

| % | |

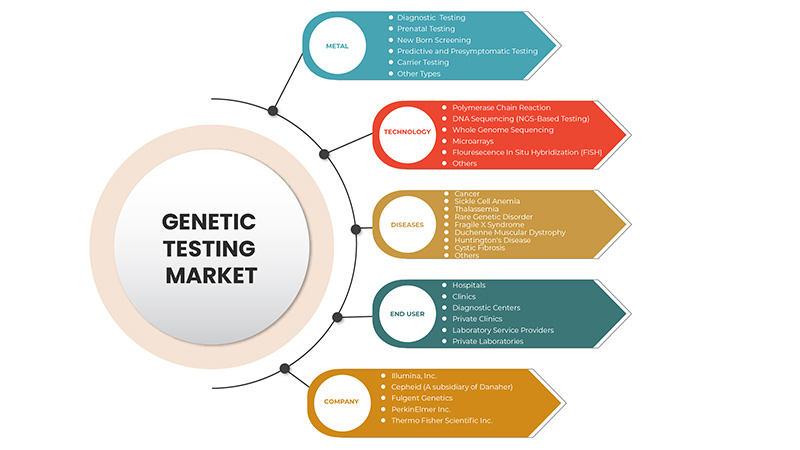

North America Genetic Testing Market, By Type (Carrier Testing, Diagnostic Testing, Prenatal Testing, New Born Screening, Predictive And Presymptomatic Testing, Other Types), Technology (DNA Sequencing (NGS-Based Testing), Polymerase Chain Reaction, Microarrays, Whole Genome Sequencing, Fluorescence In Situ Hybridization (FISH), Others), Diseases (Rare Genetic Disorder, CancerCystic Fibrosis, Sickle Cell Anemia, Duchenne Muscular Dystrophy, Thalassemia, Huntington’s Disease, Fragile X Syndrome, Duchenne Muscular Dystrophy, Others) End User (Hospitals, Clinics, Diagnostic Centres, Private Clinics, Laboratory Service Providers, Private Laboratories) Industry Trends and Forecast to 2029

Market Analysis and Insights

North America genetic testing market is driven by the factors such as the high prevalence of genetic disorders, growing technological advancements in the genetic testing market which enhance its demand, as well as increasing investment in research and development, which leads to market growth. Currently, healthcare expenditure has increased across developed and emerging countries which is expected to create a competitive advantage for manufacturers to develop new and innovative genetic testing markets. However, the high cost associated with genetic testing and stringent regulatory frameworks for genetic testing.

North America genetic testing market report provides details of market share, new developments, and product pipeline analysis, the impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, product approvals, strategic decisions, product launches, geographic expansions, and technological innovations in the market. To understand the analysis and the market scenario contact us for an analyst brief, our team will help you create a revenue impact solution to achieve your desired goal. The scalability and business expansion of the retail units in the developing countries of various region and partnership with suppliers for safe distribution of machine and drugs products are the major drivers which propelled the demand of the market in the forecast period.

Market Definition

Genetic testing is a kind of medical test that identifies changes in genes, chromosomes, or proteins. The outcome of a genetic test can confirm or rule out a suspected genetic condition or aid in determining a person’s chance of developing or passing on a genetic disorder. Over 77,000 genetic tests are currently in use, and others are being developed.

The increasing innovations and technologies and rising number of players in the market, and novel product launches are also propelling the growth of the North America genetic testing market.

Se espera que el mercado de pruebas genéticas de América del Norte gane crecimiento de mercado en el período de pronóstico de 2022 a 2029. Data Bridge Market Research analiza que el mercado está creciendo con una CAGR del 15,6% en el período de pronóstico de 2022 a 2029 y se espera que alcance los USD 17.887,74 millones para 2029 desde USD 5.688,94 millones en 2021.

|

Métrica del informe |

Detalles |

|

Período de pronóstico |

2022 a 2029 |

|

Año base |

2021 |

|

Años históricos |

2020 |

|

Unidades cuantitativas |

Ingresos en millones de USD |

|

Segmentos cubiertos |

Por tipo (Pruebas de portadores, Pruebas diagnósticas, Pruebas prenatales, Detección en recién nacidos, Pruebas predictivas y presintomáticas, Otros tipos), Tecnología (Secuenciación de ADN (Pruebas basadas en NGS), Reacción en cadena de la polimerasa, Microarrays, Secuenciación del genoma completo, Hibridación in situ con fluorescencia (FISH), Otros), Enfermedades (Trastorno genético raro, Cáncer, Fibrosis quística, Anemia de células falciformes, Distrofia muscular de Duchenne, Talasemia, Enfermedad de Huntington, Síndrome del cromosoma X frágil, Distrofia muscular de Duchenne, Otros) Usuario final (Hospitales, Clínicas, Centros de diagnóstico, Clínicas privadas, Proveedores de servicios de laboratorio, Laboratorios privados) |

|

Países cubiertos |

Estados Unidos, Canadá, México |

|

Actores del mercado cubiertos |

Thermo Fisher Scientific Inc., Invitae Corporation, Bio-Rad Laboratories, Inc., PerkinElmer Inc., Illumina, Inc., QIAGEN, F. Hoffmann-La Roche Ltd., Fulgent Genetics, Myriad Genetics, Inc., Abbott, Eurofins Scientific, Sorenson Genomics, Biocartis, Cepheid (una subsidiaria de Danaher), PacBio, Otogenetics, BioReference, Sema4 OpCo, Inc., Natera, Inc., entre otros. |

Dinámica del mercado de pruebas genéticas en América del Norte

Conductores

-

Creciente prevalencia de enfermedades genéticas

Los trastornos genéticos pueden causar problemas de salud tan graves que son incompatibles con la vida. En los casos más graves, estas afecciones pueden provocar un aborto espontáneo del embrión o feto afectado. La creciente prevalencia de enfermedades genéticas y defectos congénitos aumenta la demanda de pruebas genéticas.

Según el artículo Trastornos genéticos y anomalías congénitas: estrategias para reducir la carga en la Región, 2022,

-

Los trastornos genéticos y las anomalías congénitas se presentan en aproximadamente el 2% al 5% de todos los nacidos vivos, lo que representa hasta el 30% de las admisiones hospitalarias pediátricas y causa alrededor del 50% de las muertes infantiles en los países industrializados.

Por lo tanto, esto está aumentando la demanda del mercado de pruebas genéticas.

-

Aumento de la adopción de la secuenciación de próxima generación

A medida que la farmacología centrada en la genómica continúa desempeñando un papel más importante en el tratamiento de diversas enfermedades crónicas, especialmente el cáncer, la secuenciación de próxima generación (NGS) está evolucionando como una herramienta poderosa para proporcionar una visión más profunda y precisa de las bases moleculares de tumores individuales y receptores específicos.

La NGS ofrece ventajas en cuanto a precisión, sensibilidad y velocidad en comparación con los métodos tradicionales que tienen el potencial de tener un impacto significativo en el campo de la oncología. Debido a que la NGS puede evaluar múltiples genes en un solo ensayo, se elimina la necesidad de solicitar múltiples pruebas para identificar la mutación causal.

Por ejemplo,

-

La NGS también se ha explorado para la elaboración de perfiles integrales de farmacogenética con relevancia para la farmacocinética y farmacodinamia de los medicamentos; los informes iniciales de 2017 sugieren que esta tecnología puede representar una herramienta confiable y eficiente para descubrir variaciones genéticas comunes y raras en estos genes.

Por lo tanto, se espera que esto actúe como motor del crecimiento del mercado de pruebas genéticas.

Oportunidades

-

Aumento de la renta disponible

El gasto de dinero que un país destina a su atención sanitaria y su tasa de crecimiento a lo largo del tiempo están condicionados por una amplia variedad de factores económicos y sociales, entre ellos, los mecanismos de financiación y la estructura de la organización del sistema de salud. En particular, existe una fuerte correlación entre el nivel de ingresos total de un país y el gasto de su población en atención sanitaria.

Además, las iniciativas estratégicas adoptadas por los actores clave del mercado proporcionarán integridad estructural y oportunidades futuras para el mercado de pruebas genéticas en el período de pronóstico de 2022 a 2029.

Restricciones/Desafíos

- Alto costo de las pruebas genéticas

Las pruebas genéticas pueden ser costosas y es posible que no estén cubiertas por algunos planes de seguro médico. Las numerosas pruebas genéticas difieren en costos según la enfermedad específica para la que se realizan las pruebas.

Según Breastcancer.org, el costo de las pruebas genéticas para detectar el cáncer puede variar mucho y oscilar entre 300 y 5000 dólares. El costo de las pruebas genéticas depende del tipo de prueba y de su complejidad.

Las pruebas genéticas pueden costar entre 100 y más de 2000 dólares, según la naturaleza y la complejidad de la prueba. Si se requiere más de una prueba o si es necesario realizar la prueba a varios miembros de la familia para obtener un resultado significativo, el gasto aumenta. El costo de las pruebas de detección neonatal varía según el estado.

Impacto de la COVID-19 en el mercado de pruebas genéticas de América del Norte

El COVID-19 ha afectado positivamente al mercado, ya que se realizaron muchas pruebas genéticas y serológicas para el COVID-19, lo que aumenta la demanda de pruebas genéticas durante este período.

Desarrollo reciente

- En diciembre de 2021, Thermo Fisher Scientific Inc. anunció que había completado la adquisición de PPD, Inc., un proveedor líder mundial de servicios de investigación clínica para la industria biofarmacéutica y biotecnológica, por 17 400 millones de dólares. Esta adquisición ayudó a generar más ingresos e impulsó el crecimiento del mercado.

Alcance del mercado de pruebas genéticas en América del Norte

El mercado de pruebas genéticas de América del Norte está segmentado por tipo, tecnología, enfermedades y usuario final. El crecimiento entre estos segmentos le ayudará a analizar los segmentos de crecimiento reducido de las industrias y brindará a los usuarios una valiosa descripción general del mercado y conocimientos del mercado para tomar decisiones estratégicas a fin de identificar las principales aplicaciones del mercado.

Tipo

- Pruebas de diagnóstico

- Pruebas prenatales

- Evaluación del recién nacido

- Pruebas predictivas y presintomáticas

- Pruebas de portadores

- Otros tipos

Según el tipo, el mercado de pruebas genéticas de América del Norte está segmentado en pruebas de diagnóstico, pruebas prenatales, detección de recién nacidos, pruebas predictivas y presintomáticas, pruebas de portadores y otros tipos.

Tecnología

- Reacción en cadena de la polimerasa

- Secuenciación de ADN (prueba basada en NGS)

- Secuenciación del genoma completo

- Microarrays

- Hibridación in situ con fluorescencia (FISH)

- Otros

Sobre la base de la tecnología, el mercado de pruebas genéticas de América del Norte está segmentado en secuenciación de ADN (pruebas basadas en NGS), reacción en cadena de la polimerasa, microarrays, secuenciación del genoma completo, hibridación in situ con fluorescencia (FISH) y otros.

Enfermedades

- Cáncer

- Anemia de células falciformes

- Talasemia

- Trastorno genético raro

- Síndrome del cromosoma X frágil

- Distrofia muscular de Duchenne

- Enfermedad de Huntington

- Fibrosis quística

- Otros

Sobre la base de las enfermedades, el mercado de pruebas genéticas de América del Norte está segmentado en trastornos genéticos raros, cáncer, fibrosis quística, anemia de células falciformes, distrofia muscular de Duchenne, talasemia, enfermedad de Huntington, síndrome del cromosoma X frágil y otros.

Usuario final

- Hospitales

- Clínicas

- Centros de diagnóstico

- Clínicas privadas

- Proveedores de servicios de laboratorio

- Laboratorios privados

Sobre la base de los usuarios finales, el mercado de pruebas genéticas de América del Norte está segmentado en hospitales, clínicas, centros de diagnóstico, clínicas privadas, proveedores de servicios de laboratorio y laboratorios privados.

Análisis y perspectivas regionales del mercado de pruebas genéticas

Se analiza el mercado de pruebas genéticas y se proporcionan información y tendencias del tamaño del mercado por país, tipo, tecnología, enfermedades y usuario final como se menciona anteriormente.

Estados Unidos es el principal país dominante en el mercado debido a la creciente prevalencia de trastornos genéticos entre la población de estos países. Además, dominan el mercado de pruebas genéticas en términos de participación de mercado e ingresos de mercado y seguirán manteniendo su dominio durante el período de pronóstico. Esto se debe a los defectos genéticos y las aberraciones cromosómicas en la población de las regiones y al rápido desarrollo de la investigación que está impulsando el mercado.

La sección de países del informe también proporciona factores de impacto de mercado individuales y cambios en las regulaciones del mercado que afectan las tendencias actuales y futuras del mercado. Los puntos de datos, como las ventas nuevas y de reemplazo, la demografía del país, la epidemiología de las enfermedades y los aranceles de importación y exportación, son algunos de los principales indicadores utilizados para pronosticar el escenario del mercado para países individuales. Además, la presencia y disponibilidad de marcas globales y sus desafíos enfrentados debido a la alta competencia de las marcas locales y nacionales, y el impacto de los canales de venta se consideran al proporcionar un análisis de pronóstico de los datos del país.

Análisis del panorama competitivo y de la cuota de mercado de las pruebas genéticas

El panorama competitivo del mercado de pruebas genéticas proporciona detalles sobre los competidores. Los detalles incluidos son una descripción general de la empresa, las finanzas de la empresa, los ingresos generados, el potencial de mercado, la inversión en investigación y desarrollo, las nuevas iniciativas de mercado, la presencia global, los sitios e instalaciones de producción, las capacidades de producción, las fortalezas y debilidades de la empresa, el lanzamiento de productos, la amplitud y variedad de productos y el dominio de las aplicaciones. Los puntos de datos proporcionados anteriormente solo están relacionados con el enfoque de las empresas en el mercado de pruebas genéticas.

Algunos de los principales actores que operan en el mercado de pruebas genéticas son Thermo Fisher Scientific Inc., Invitae Corporation, Bio-Rad Laboratories, Inc., PerkinElmer Inc., Illumina, Inc., QIAGEN, F. Hoffmann-La Roche Ltd., Fulgent Genetics, Myriad Genetics, Inc., Abbott, Eurofins Scientific, Sorenson Genomics, Biocartis, Cepheid (una subsidiaria de Danaher), PacBio, Otogenetics, BioReference, Sema4 OpCo, Inc., Natera, Inc., entre otros.

Metodología de la investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con tamaños de muestra grandes. Los datos del mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Aparte de esto, los modelos de datos incluyen la cuadrícula de posicionamiento de proveedores, el análisis de la línea de tiempo del mercado, la descripción general y la guía del mercado, la cuadrícula de posicionamiento de la empresa, el análisis de la participación de mercado de la empresa, los estándares de medición, el análisis global frente a regional y el análisis de la participación de los proveedores. Solicite una llamada de un analista en caso de tener más consultas.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Tabla de contenido

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE NORTH AMERICA GENETIC TESTING MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 TYPE LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET APPLICATION COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.2 PORTER’S FIVE FORCES

4.3 STRATEGIC INITIATIVES:

4.4 CONCLUSION:

4.5 INDUSTRY INSIGHTS

4.5.1 CANCER GENETICS RISK ASSESSMENT AND COUNSELING

4.5.2 GENETIC TESTS PRICING

4.5.3 KEY INSIGHTS

5 EPIDERMIOLOGY

6 NORTH AMERICA GENETIC TESTING MARKET: REGULATIONS

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 GROWING PREVALENCE OF GENETIC DISORDERS

7.1.2 INCREASE IN THE ADOPTION OF NEXT GENERATION SEQUENCING

7.1.3 WIDE PRODUCT PORTFOLIO OFFERED BY A MAJOR PLAYER

7.1.4 INCREASE TREND TOWARD PERSONALIZED MEDICATION

7.2 RESTRAINTS

7.2.1 HIGH COST OF GENETIC TESTING

7.2.2 CYBER SECURITY CONCERNS IN GENOMICS

7.3 OPPORTUNITIES

7.3.1 STRATEGIC INITIATIVES BY THE KEY MARKET PLAYER

7.3.2 TECHNOLOGICAL ADVANCEMENT

7.3.3 INCREASING RESEARCH AND DEVELOPMENT

7.3.4 RISING DISPOSABLE INCOME

7.4 CHALLENGES

7.4.1 LACK OF SKILLED PROFESSIONALS TO PERFORM GENETIC TESTING

7.4.2 STRINGENT REGULATION POLICY

8 NORTH AMERICA GENETIC TESTING MARKET, BY TYPE

8.1 OVERVIEW

8.2 DIAGNOSTIC TESTING

8.3 PRENATAL TESTING

8.3.1 NON-INVASIVE SCREENING

8.3.1.1 BY SCREENING METHOD

8.3.1.1.1 WHOLE GENOME SEQUENCING

8.3.1.1.2 COUNTING OF cfDNA FRAGMENTS

8.3.1.1.3 OTHERS

8.3.1.2 BY CONDITION

8.3.1.2.1 TRISOMY 21

8.3.1.2.2 KLINEFELTER SYNDROME

8.3.1.2.3 JACOBS SYNDROME

8.3.1.2.4 CYSTIC FIBROSIS

8.3.1.2.5 TURNER SYNDROME

8.3.1.2.6 TRISOMY 18

8.3.1.2.7 HEMOPHILIA

8.3.1.2.8 TRISOMY 13

8.3.1.2.9 MICRODELETION SYNDROME

8.3.1.2.10 FETAL GENDER

8.3.1.2.11 OTHERS

8.3.1.3 BY SCREENING TYPE

8.3.1.3.1 CARRIER SEQUENCING

8.3.1.3.2 SEQUENTIAL SEQUENCING

8.3.2 MATERNAL SERUM QUAD SCREENING

8.4 NEW BORN SCREENING

8.4.1.1 SICKLE CELL DISEASE

8.4.1.2 CONGENITAL HYPOTHYROIDISM

8.4.1.3 PHENYLKETONURIA (PKU)

8.4.1.4 GALACTOSEMIA

8.4.1.5 MAPLE SYRUP URINE DISEASE

8.4.1.6 OTHERS

8.5 PREDICTIVE AND PRESYMPTOMATIC TESTING

8.6 CARRIER TESTING

8.6.1 BY TEST TYPE

8.6.1.1 MOLECULAR SCREENING TEST

8.6.1.2 BIOCHEMICAL SCREENING TEST

8.6.2 BY TYPE

8.6.2.1 EXPANDED CARRIER SCREENING

8.6.2.1.1 PREDESIGNED PANEL TESTING

8.6.2.1.2 CUSTOM-MADE PANEL TESTING

8.6.2.2 TARGETED DISEASE CARRIER SCREENING

8.6.2.2.1 BY MEDICAL CONDITION

8.6.2.2.2 HEMATOLOGICAL CONDITIONS

8.6.2.2.3 PULMONARY CONDITIONS

8.6.2.2.4 NEUROLOGICAL CONDITIONS

8.6.2.2.5 OTHER CONDITIONS

8.7 OTHER TYPES

9 NORTH AMERICA GENETIC TESTING MARKET, BY TECHNOLOGY

9.1 OVERVIEW

9.2 POLYMERASE CHAIN REACTION

9.2.1 REAL-TIME PCR (QPCR)

9.2.2 DIGITAL PCR (DPCR)

9.2.3 REVERSE TRANSCRIPTION PCR (RT-PCR)

9.2.4 HOT-START PCR

9.2.5 MULTIPLEX PCR

9.2.6 OTHER PCR

9.3 DNA SEQUENCING (NGS-BASED TESTING)

9.3.1 NEXT GENERATION SEQUENCING (NGS)

9.3.2 SANGER SEQUENCING (SINGLE GENE)

9.3.3 OTHER

9.4 WHOLE GENOME SEQUENCING

9.5 MICROARRAYS

9.5.1 DNA MICROARRAYS

9.5.2 PROTEIN MICROARRAYS

9.5.3 OTHER MICROARRAYS

9.6 FLUORESCENCE IN SITU HYBRIDIZATION (FISH)

9.7 OTHERS

10 NORTH AMERICA GENETIC TESTING MARKET, BY DISEASES

10.1 OVERVIEW

10.2 CANCER

10.2.1 BREAST

10.2.2 COLON

10.2.3 LUNG

10.2.4 PROSTATE

10.2.5 OTHERS

10.3 SICKLE CELL ANEMIA

10.4 THALASSEMIA

10.5 RARE GENETIC DISORDER

10.5.1 TRISOMY 21

10.5.2 MONOSOMY X

10.5.3 TRISOMY 13

10.5.4 MICRODELETION SYNDROME

10.5.5 TRISOMY 18

10.5.6 OTHERS

10.6 FRAGILE X SYNDROME

10.7 DUCHENNE MUSCULAR DYSTROPHY

10.8 HUNTINGTON'S DISEASE

10.9 CYSTIC FIBROSIS

10.1 OTHERS

11 NORTH AMERICA GENETIC TESTING MARKET, BY END USER

11.1 OVERVIEW

11.2 HOSPITALS

11.3 CLINICS

11.4 DIAGNOSTIC CENTERS

11.5 PRIVATE CLINICS

11.6 LABORATORY SERVICE PROVIDERS

11.7 PRIVATE LABORATORIES

12 NORTH AMERICA GENETIC TESTING MARKET, BY REGION

12.1 NORTH AMERICA

12.1.1 U.S.

12.1.2 CANADA

12.1.3 MEXICO

13 NORTH AMERICA GENETIC TESTING MARKET, COMPANY LANDSCAPE

13.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

14 SWOT ANALYSIS

15 COMPANY PROFILE

15.1 ILLUMINA, INC.

15.1.1 COMPANY SNAPSHOT

15.1.2 COMPANY SHARE ANALYSIS

15.1.3 PRODUCT PORTFOLIO

15.1.4 RECENT DEVELOPMENT

15.1.4.1 ACQUISITION

15.1.4.2 COLLABORATION

15.2 CEPHEID

15.2.1 COMPANY SNAPSHOT

15.2.2 REVENUE ANALYSIS

15.2.3 COMPANY SHARE ANALYSIS

15.2.4 PRODUCT PORTFOLIO

15.2.5 RECENT DEVELOPMENT

15.2.5.1 BUSINEES EXPANSION

15.3 FULGENT GENETICS

15.3.1 COMPANY SNAPSHOT

15.3.2 REVENUE ANALYSIS

15.3.3 COMPANY SHARE ANALYSIS

15.3.4 PRODUCT PORTFOLIO

15.3.5 RECENT DEVELOPMENT

15.3.5.1 ACQUISITION

15.4 PERKINELMER INC.

15.4.1 COMPANY SNAPSHOT

15.4.2 REVENUE ANALYSIS

15.4.3 COMPANY SHARE ANALYSIS

15.4.4 PRODUCT PORTFOLIO

15.4.5 RECENT DEVELOPMENT

15.4.5.1 PRODUCT LAUNCH

15.5 THERMO FISHER SCIENTIFIC INC.

15.5.1 COMPANY SNAPSHOT

15.5.2 REVENUE ANALYSIS

15.5.3 COMPANY SHARE ANALYSIS

15.5.4 PRODUCT PORTFOLIO

15.5.5 RECENT DEVELOPMENT

15.5.5.1 COLLABORATION

15.6 ABBOTT

15.6.1 COMPANY SNAPSHOT

15.6.2 REVENUE ANALYSIS

15.6.3 PRODUCT PORTFOLIO

15.6.4 RECENT DEVELOPMENT

15.7 BIOCARTIS

15.7.1 COMPANY SNAPSHOT

15.7.2 REVENUE ANALYSIS

15.7.3 PRODUCT PORTFOLIO

15.7.4 RECENT DEVELOPMENT

15.7.4.1 PARTNERSHIP

15.7.4.2 AGREEMENT

15.8 BIO-HELIX

15.8.1 COMPANY SNAPSHOT

15.8.2 PRODUCT PORTFOLIO

15.8.3 RECENT DEVELOPMENT

15.9 BIO-RAD LABORATORIES, INC.

15.9.1 COMPANY SNAPSHOT

15.9.2 REVENUE ANALYSIS

15.9.3 PRODUCT PORTFOLIO

15.9.4 RECENT DEVELOPMENTS

15.9.4.1 ACQUISITION

15.9.4.2 PARTNERSHIP

15.1 BIOREFERENCE

15.10.1 COMPANY SNAPSHOT

15.10.2 REVENUE ANALYSIS

15.10.3 PRODUCT PORTFOLIO

15.10.4 RECENT DEVELOPMENT

15.10.4.1 ACQUISITION

15.11 ELITECHGROUP

15.11.1 COMPANY SNAPSHOT

15.11.2 PRODUCT PORTFOLIO

15.11.3 RECENT DEVELOPMENTS

15.11.3.1 PRODUCT LAUNCH

15.11.3.2 BUSINESS EXPANSION

15.12 EUROFINS SCIENTIFIC

15.12.1 COMPANY SNAPSHOT

15.12.2 REVENUE ANALYSIS

15.12.3 PRODUCT PORTFOLIO

15.12.4 RECENT DEVELOPMENT

15.12.4.1 PRODUCT LAUNCH

15.13 EUGENE LABS

15.13.1 COMPANY SNAPSHOT

15.13.2 PRODUCT PORTFOLIO

15.13.3 RECENT DEVELOPMENT

15.14 F. HOFFMANN-LA ROCHE LTD)

15.14.1 COMPANY SNAPSHOT

15.14.2 REVENUE ANALYSIS (PARENT COMPANY)

15.14.3 PRODUCT PORTFOLIO

15.14.4 RECENT DEVELOPMENTS

15.14.4.1 PRODUCT LAUNCH

15.15 GENES2ME

15.15.1 COMPANY SNAPSHOT

15.15.2 PRODUCT PORTFOLIO

15.15.3 RECENT DEVELOPMENT

15.16 INVITAE CORPORATION

15.16.1 COMPANY SNAPSHOT

15.16.2 REVENUE ANALYSIS

15.16.3 PRODUCT PORTFOLIO

15.16.4 RECENT DEVELOPMENTS

15.17 MAPMYGENOME

15.17.1 COMPANY SNAPSHOT

15.17.2 PRODUCT PORTFOLIO

15.17.3 RECENT DEVELOPMENT

15.18 MEDGENOME

15.18.1 COMPANY SNAPSHOT

15.18.2 PRODUCT PORTFOLIO

15.18.3 RECENT DEVELOPMENT

15.19 MYRIAD GENETICS

15.19.1 COMPANY SNAPSHOT

15.19.2 REVENUE ANALYSIS

15.19.3 PRODUCT PORTFOLIO

15.19.4 RECENT DEVELOPMENT

15.2 NATERA, INC.

15.20.1 COMPANY SNAPSHOT

15.20.2 PRODUCT PORTFOLIO

15.20.3 RECENT DEVELOPMENT

15.20.3.1 PARTNERSHIP

15.21 OTOGENRTICS

15.21.1 COMPANY SNAPSHOT

15.21.2 PRODUCT PORTFOLIO

15.21.3 RECENT DEVELOPMENT

15.22 PACBIO

15.22.1 COMPANY SNAPSHOT

15.22.2 REVENUE ANALYSIS

15.22.3 PRODUCT PORTFOLIO

15.22.4 RECENT DEVELOPMENT

15.23 QIAGEN

15.23.1 COMPANY SNAPSHOT

15.23.2 PRODUCT PORTFOLIO

15.23.3 RECENT DEVELOPMENTS

15.23.3.1 PARTNERSHIP

15.23.3.2 PRODUCT LAUNCH

15.24 SEMA4 OPCO, INC.

15.24.1 COMPANY SNAPSHOT

15.24.2 REVENUE ANALYSIS

15.24.3 PRODUCT PORTFOLIO

15.24.4 RECENT DEVELOPMENT

15.25 SORENSON GENOMICS

15.25.1 COMPANY SNAPSHOT

15.25.2 PRODUCT PORTFOLIO

15.25.3 RECENT DEVELOPMENT

16 QUESTIONNAIRE

17 RELATED REPORTS

Lista de Tablas

TABLE 1 NORTH AMERICA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 2 NORTH AMERICA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 3 NORTH AMERICA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 4 NORTH AMERICA DIAGNOSTIC TESTING IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 5 NORTH AMERICA PRENATAL TESTING IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 6 NORTH AMERICA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 7 NORTH AMERICA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 8 NORTH AMERICA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 9 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (USD MILLION)

TABLE 10 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (UNITS)

TABLE 11 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (ASP)

TABLE 12 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY CONDITION, 2020-2029 (USD MILLION)

TABLE 13 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (USD MILLION)

TABLE 14 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (UNITS)

TABLE 15 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (ASP)

TABLE 16 NORTH AMERICA NEW BORN SCREENING IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 17 NORTH AMERICA NEW-BORN SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 18 NORTH AMERICA PREDICTIVE AND PRESYMPTOMATIC TESTING IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 19 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 20 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (USD MILLION)

TABLE 21 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (UNITS)

TABLE 22 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (ASP)

TABLE 23 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 24 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 25 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 26 NORTH AMERICA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 27 NORTH AMERICA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 28 NORTH AMERICA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 29 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY MEDICAL CONDITION, 2020-2029 (USD MILLION)

TABLE 30 NORTH AMERICA OTHER TYPES IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 31 NORTH AMERICA GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 32 NORTH AMERICA POLYMERASE CHAIN REACTION IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 33 NORTH AMERICA POLYMERASE CHAIN REACTION IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 34 NORTH AMERICA DNA SEQUENCING (NGS-BASED TESTING) IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 35 NORTH AMERICA DNA SEQUENCING (NGS-BASED TESTING) IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 36 NORTH AMERICA WHOLE GENOME SEQUENCING IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 37 NORTH AMERICA MICROARRAYS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 38 NORTH AMERICA MICROARRAYS IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 39 NORTH AMERICA FLUORESCENCE IN SITU HYBRIDIZATION (FISH) IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 40 NORTH AMERICA OTHERS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 41 NORTH AMERICA GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 42 NORTH AMERICA CANCER IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 43 NORTH AMERICA CANCER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 44 NORTH AMERICA SICKLE CELL ANEMIA IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 45 NORTH AMERICA THALASSEMIA IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 46 NORTH AMERICA RARE GENETIC DISORDER IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 47 NORTH AMERICA RARE GENETIC DISORDER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 48 NORTH AMERICA FRAGILE X SYNDROME IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 49 NORTH AMERICA DUCHENNE MUSCULAR DYSTROPHY IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 50 NORTH AMERICA HUNTINGTON'S DISEASE IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 51 NORTH AMERICA CYSTIC FIBROSIS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 52 NORTH AMERICA OTHERS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 53 NORTH AMERICA GENETIC TESTING MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 54 NORTH AMERICA HOSPITALS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 55 NORTH AMERICA CLINICS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 56 NORTH AMERICA DIAGNOSTIC CENTERS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 57 NORTH AMERICA PRIVATE CLINICS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 58 NORTH AMERICA LABORATORY SERVICE PROVIDERS IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 59 NORTH AMERICA PRIVATE LABORATORIES IN GENETIC TESTING MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 60 NORTH AMERICA GENETIC TESTING MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 61 NORTH AMERICA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 62 NORTH AMERICA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 63 NORTH AMERICA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 64 NORTH AMERICA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 65 NORTH AMERICA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 66 NORTH AMERICA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 67 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (USD MILLION)

TABLE 68 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (UNITS)

TABLE 69 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (ASP)

TABLE 70 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY CONDITION, 2020-2029 (USD MILLION)

TABLE 71 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (USD MILLION)

TABLE 72 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (UNITS)

TABLE 73 NORTH AMERICA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (ASP)

TABLE 74 NORTH AMERICA NEW-BORN SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 75 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (USD MILLION)

TABLE 76 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (UNITS)

TABLE 77 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (ASP)

TABLE 78 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 79 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 80 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 81 NORTH AMERICA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 82 NORTH AMERICA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 83 NORTH AMERICA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 84 NORTH AMERICA CARRIER TESTING IN GENETIC TESTING MARKET, BY MEDICAL CONDITION, 2020-2029 (USD MILLION)

TABLE 85 NORTH AMERICA GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 86 NORTH AMERICA POLYMERASE CHAIN REACTION IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 87 NORTH AMERICA DNA SEQUENCING IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 88 NORTH AMERICA MICROARRAYS IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 89 NORTH AMERICA GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 90 NORTH AMERICA RARE GENETIC DISORDER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 91 NORTH AMERICA CANCER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 92 NORTH AMERICA GENETIC TESTING MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 93 U.S. GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 94 U.S. GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 95 U.S. GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 96 U.S. PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 97 U.S. PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 98 U.S. PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 99 U.S. NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (USD MILLION)

TABLE 100 U.S. NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (UNITS)

TABLE 101 U.S. NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (ASP)

TABLE 102 U.S. NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY CONDITION, 2020-2029 (USD MILLION)

TABLE 103 U.S. NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (USD MILLION)

TABLE 104 U.S. NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (UNITS)

TABLE 105 U.S. NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (ASP)

TABLE 106 U.S. NEW-BORN SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 107 U.S. CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (USD MILLION)

TABLE 108 U.S. CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (UNITS)

TABLE 109 U.S. CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (ASP)

TABLE 110 U.S. CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 111 U.S. CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 112 U.S. CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 113 U.S. EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 114 U.S. EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 115 U.S. EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 116 U.S. CARRIER TESTING IN GENETIC TESTING MARKET, BY MEDICAL CONDITION, 2020-2029 (USD MILLION)

TABLE 117 U.S. GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 118 U.S. POLYMERASE CHAIN REACTION IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 119 U.S. DNA SEQUENCING IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 120 U.S. MICROARRAYS IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 121 U.S. GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 122 U.S. RARE GENETIC DISORDER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 123 U.S. CANCER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 124 U.S. GENETIC TESTING MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 125 CANADA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 126 CANADA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 127 CANADA GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 128 CANADA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 129 CANADA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 130 CANADA PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 131 CANADA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (USD MILLION)

TABLE 132 CANADA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (UNITS)

TABLE 133 CANADA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (ASP)

TABLE 134 CANADA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY CONDITION, 2020-2029 (USD MILLION)

TABLE 135 CANADA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (USD MILLION)

TABLE 136 CANADA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (UNITS)

TABLE 137 CANADA NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (ASP)

TABLE 138 CANADA NEW-BORN SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 139 CANADA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (USD MILLION)

TABLE 140 CANADA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (UNITS)

TABLE 141 CANADA CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (ASP)

TABLE 142 CANADA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 143 CANADA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 144 CANADA CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 145 CANADA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 146 CANADA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 147 CANADA EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 148 CANADA CARRIER TESTING IN GENETIC TESTING MARKET, BY MEDICAL CONDITION, 2020-2029 (USD MILLION)

TABLE 149 CANADA GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 150 CANADA POLYMERASE CHAIN REACTION IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 151 CANADA DNA SEQUENCING IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 152 CANADA MICROARRAYS IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 153 CANADA GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 154 CANADA RARE GENETIC DISORDER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 155 CANADA CANCER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 156 CANADA GENETIC TESTING MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 157 MEXICO GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 158 MEXICO GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 159 MEXICO GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 160 MEXICO PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 161 MEXICO PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 162 MEXICO PRENATAL TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 163 MEXICO NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (USD MILLION)

TABLE 164 MEXICO NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (UNITS)

TABLE 165 MEXICO NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING METHOD, 2020-2029 (ASP)

TABLE 166 MEXICO NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY CONDITION, 2020-2029 (USD MILLION)

TABLE 167 MEXICO NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (USD MILLION)

TABLE 168 MEXICO NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (UNITS)

TABLE 169 MEXICO NON-INVASIVE SCREENING IN GENETIC TESTING MARKET, BY SCREENING TYPE, 2020-2029 (ASP)

TABLE 170 MEXICO NEW-BORN SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 171 MEXICO CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (USD MILLION)

TABLE 172 MEXICO CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (UNITS)

TABLE 173 MEXICO CARRIER TESTING IN GENETIC TESTING MARKET, BY TEST TYPE, 2020-2029 (ASP)

TABLE 174 MEXICO CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 175 MEXICO CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 176 MEXICO CARRIER TESTING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 177 MEXICO EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (USD MILLION)

TABLE 178 MEXICO EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (UNITS)

TABLE 179 MEXICO EXPANDED CARRIER SCREENING IN GENETIC TESTING MARKET, BY TYPE, 2020-2029 (ASP)

TABLE 180 MEXICO CARRIER TESTING IN GENETIC TESTING MARKET, BY MEDICAL CONDITION, 2020-2029 (USD MILLION)

TABLE 181 MEXICO GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 182 MEXICO POLYMERASE CHAIN REACTION IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 183 MEXICO DNA SEQUENCING IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 184 MEXICO MICROARRAYS IN GENETIC TESTING MARKET, BY TECHNOLOGY, 2020-2029 (USD MILLION)

TABLE 185 MEXICO GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 186 MEXICO RARE GENETIC DISORDER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 187 MEXICO CANCER IN GENETIC TESTING MARKET, BY DISEASES, 2020-2029 (USD MILLION)

TABLE 188 MEXICO GENETIC TESTING MARKET, BY END USER, 2020-2029 (USD MILLION)

Lista de figuras

FIGURE 1 NORTH AMERICA GENETIC TESTING MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA GENETIC TESTING MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA GENETIC TESTING MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA GENETIC TESTING MARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA GENETIC TESTING MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA GENETIC TESTING MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA GENETIC TESTING MARKET: DBMR MARKET POSITION GRID

FIGURE 8 NORTH AMERICA GENETIC TESTING MARKET: APPLICATION COVERAGE GRID

FIGURE 9 NORTH AMERICA GENETIC TESTING MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 NORTH AMERICA GENETIC TESTING MARKET: SEGMENTATION

FIGURE 11 INCREASING PREVALENCE OF LYMPHEDEMA AND RISING HEALTHCARE EXPENDITURE ARE EXPECTED TO DRIVE THE NORTH AMERICA GENETIC TESTING MARKET IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 12 DIAGNOSTIC TESTING SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA GENETIC TESTING MARKET IN 2022 & 2029

FIGURE 13 NORTH AMERICA IS EXPECTED TO DOMINATE THE NORTH AMERICA GENETIC TESTING MARKET AND ASIA-PACIFIC EXPECTED TO GROW WITH THE HIGHEST CAGR IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 14 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF NORTH AMERICA GENETIC TESTING MARKET

FIGURE 15 NORTH AMERICA GENETIC TESTING MARKET: BY TYPE, 2021

FIGURE 16 NORTH AMERICA GENETIC TESTING MARKET: BY TYPE, 2022-2029 (USD MILLION)

FIGURE 17 NORTH AMERICA GENETIC TESTING MARKET: BY TYPE, CAGR (2022-2029)

FIGURE 18 NORTH AMERICA GENETIC TESTING MARKET: BY TYPE, LIFELINE CURVE

FIGURE 19 NORTH AMERICA GENETIC TESTING MARKET: BY TECHNOLOGY, 2021

FIGURE 20 NORTH AMERICA GENETIC TESTING MARKET: BY TECHNOLOGY, 2022-2029 (USD MILLION)

FIGURE 21 NORTH AMERICA GENETIC TESTING MARKET: BY TECHNOLOGY, CAGR (2022-2029)

FIGURE 22 NORTH AMERICA GENETIC TESTING MARKET: BY TECHNOLOGY, LIFELINE CURVE

FIGURE 23 NORTH AMERICA GENETIC TESTING MARKET: BY DISEASES, 2021

FIGURE 24 NORTH AMERICA GENETIC TESTING MARKET: BY DISEASES, 2022-2029 (USD MILLION)

FIGURE 25 NORTH AMERICA GENETIC TESTING MARKET: BY DISEASES, CAGR (2022-2029)

FIGURE 26 NORTH AMERICA GENETIC TESTING MARKET: BY DISEASES, LIFELINE CURVE

FIGURE 27 NORTH AMERICA GENETIC TESTING MARKET: BY END USER, 2021

FIGURE 28 NORTH AMERICA GENETIC TESTING MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 29 NORTH AMERICA GENETIC TESTING MARKET: BY END USER, CAGR (2022-2029)

FIGURE 30 NORTH AMERICA GENETIC TESTING MARKET: BY END USER, LIFELINE CURVE

FIGURE 31 NORTH AMERICA GENETIC TESTING MARKET: SNAPSHOT (2021)

FIGURE 32 NORTH AMERICA GENETIC TESTING MARKET: BY COUNTRY (2021)

FIGURE 33 NORTH AMERICA GENETIC TESTING MARKET: BY COUNTRY (2022 & 2029)

FIGURE 34 NORTH AMERICA GENETIC TESTING MARKET: BY COUNTRY (2021 & 2029)

FIGURE 35 NORTH AMERICA GENETIC TESTING MARKET: BY TYPE (2022-2029)

FIGURE 36 NORTH AMERICA GENETIC TESTING MARKET: COMPANY SHARE 2021 (%)

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.