North America Corneal Transplant Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

219.85 Million

USD

355.74 Million

2024

2032

USD

219.85 Million

USD

355.74 Million

2024

2032

| 2025 –2032 | |

| USD 219.85 Million | |

| USD 355.74 Million | |

| % | |

|

Segmentación del mercado de trasplantes de córnea en Norteamérica, por tipo de procedimiento (queratoplastia endotelial, queratoplastia penetrante, queratoplastia lamelar anterior (ALK), trasplante de células madre limbares corneales, trasplante de córnea artificial y otros), tipo (córnea humana y sintética), tipo de donante (autoinjerto y aloinjerto), tipo de injerto (injertos de espesor parcial [lamelar] e injertos de espesor completo [penetrantes]), tipo de cirugía (cirugía convencional y cirugía asistida por láser), indicación (distrofia endotelial de Fuchs, queratitis infecciosa, queratopatía bullosa, queratocono, procedimientos de reinjerto, cicatrización corneal, úlceras corneales y otros), género (femenino y masculino), grupo de edad (geriátrico, adulto y pediátrico), usuario final (hospitales, clínicas oftalmológicas, centros de cirugía ambulatoria, instituciones académicas y de investigación). Institutos y otros): Tendencias de la industria y pronóstico hasta 2032

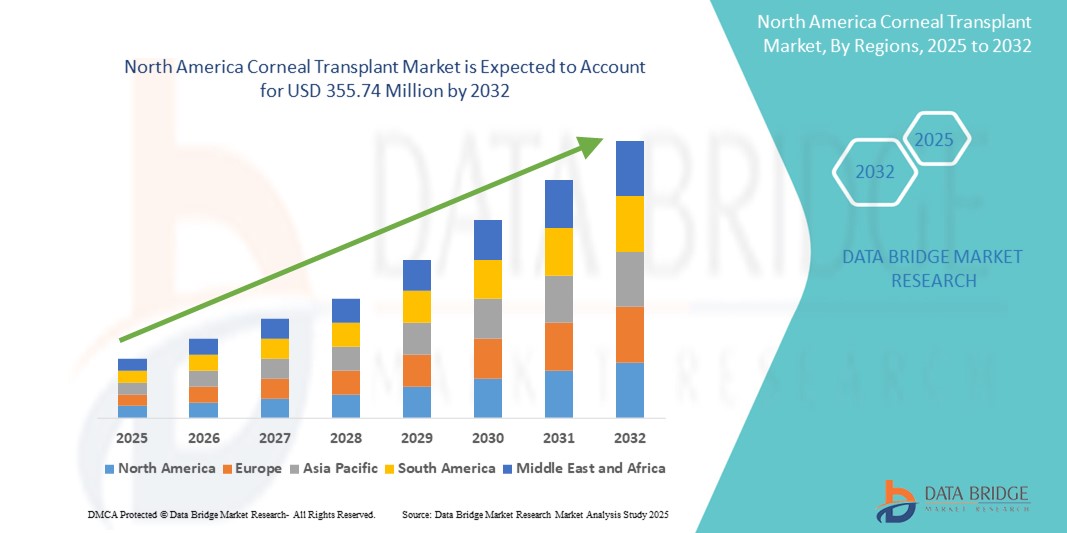

Tamaño del mercado de trasplante de córnea en América del Norte

- El tamaño del mercado de trasplante de córnea de América del Norte se valoró en USD 219,85 millones en 2024 y se espera que alcance los USD 355,74 millones para 2032 , con una CAGR del 6,20 % durante el período de pronóstico.

- El crecimiento del mercado está impulsado en gran medida por la creciente prevalencia de trastornos de la córnea, avances en técnicas de trasplante y una mejor disponibilidad de tejidos de donantes en toda la región.

- Además, la creciente concienciación sobre la salud ocular, las estructuras de reembolso favorables y la creciente adopción de procedimientos quirúrgicos mínimamente invasivos están consolidando el trasplante de córnea como el tratamiento de elección para restaurar la visión. Estos factores convergentes están acelerando la adopción de procedimientos de trasplante de córnea, impulsando así significativamente el crecimiento del mercado en la región.

Análisis del mercado de trasplantes de córnea en América del Norte

- Los trasplantes de córnea, que implican el reemplazo de tejido corneal dañado o enfermo con tejido de donante sano, son procedimientos cada vez más vitales dentro de la atención oftalmológica en entornos de atención médica públicos y privados debido a su eficacia para restaurar la visión y mejorar la calidad de vida del paciente.

- La creciente demanda de trasplantes de córnea se ve impulsada principalmente por una prevalencia creciente de enfermedades de la córnea, como el queratocono y la distrofia de Fuchs, junto con los avances en las técnicas quirúrgicas y la mayor disponibilidad de tejido de donantes.

- Estados Unidos dominó el mercado norteamericano de trasplantes de córnea con la mayor participación en ingresos, un 42,8 % en 2024. Este país se caracteriza por una infraestructura sanitaria bien desarrollada, políticas de reembolso favorables y la presencia de bancos de ojos y centros de trasplante líderes. El país está experimentando un gran volumen de procedimientos, impulsado por iniciativas de concienciación e innovaciones en las técnicas de queratoplastia endotelial.

- Se espera que Canadá sea el país de más rápido crecimiento en el mercado de trasplante de córnea de América del Norte durante el período de pronóstico debido a la expansión del acceso a la atención ocular especializada y al aumento de las inversiones en tecnologías quirúrgicas oftálmicas.

- El segmento de queratoplastia penetrante dominó el mercado de trasplante de córnea de América del Norte con una participación de mercado del 47,2 % en 2024, impulsado por su uso generalizado, resultados clínicos establecidos y capacidad para tratar daños corneales de espesor completo.

Alcance del informe y segmentación del mercado de trasplante de córnea en América del Norte

|

Atributos |

Perspectivas clave del mercado de trasplantes de córnea en América del Norte |

|

Segmentos cubiertos |

|

|

Países cubiertos |

América del norte

|

|

Actores clave del mercado |

|

|

Oportunidades de mercado |

|

|

Conjuntos de información de datos de valor añadido |

Además de los conocimientos sobre escenarios de mercado, como valor de mercado, tasa de crecimiento, segmentación, cobertura geográfica y actores principales, los informes de mercado seleccionados por Data Bridge Market Research también incluyen análisis en profundidad de expertos, análisis de precios, análisis de participación de marca, encuesta de consumidores, análisis demográfico, análisis de la cadena de suministro, análisis de la cadena de valor, descripción general de materias primas/consumibles, criterios de selección de proveedores, análisis PESTLE, análisis de Porter y marco regulatorio. |

Tendencias del mercado de trasplantes de córnea en América del Norte

Avances tecnológicos en las técnicas de queratoplastia

- Una tendencia significativa y en auge en el mercado norteamericano de trasplantes de córnea es la transición hacia técnicas de queratoplastia avanzadas y mínimamente invasivas, como la queratoplastia endotelial de la membrana de Descemet (DMEK) y la queratoplastia endotelial de desprendimiento de la membrana de Descemet (DSEK). Estos procedimientos ofrecen mejores resultados visuales, tiempos de recuperación más rápidos y menor riesgo de complicaciones en comparación con los trasplantes tradicionales de espesor completo.

- Por ejemplo, los centros de trasplantes con sede en EE. UU. están adoptando cada vez más DMEK para tratar la disfunción endotelial, respaldados por los avances en la instrumentación quirúrgica y la preparación de tejido de donantes por parte de bancos de ojos especializados.

- Estas nuevas técnicas preservan mayor parte de la estructura corneal del paciente, lo que contribuye a una mejor supervivencia del injerto a largo plazo y reduce la probabilidad de rechazo inmunológico. Además, las mejoras en la visualización intraoperatoria y los procedimientos asistidos por láser mejoran aún más la precisión quirúrgica y las tasas de éxito.

- Esta tendencia también se ve reforzada por la creciente preferencia de los cirujanos por técnicas que ofrecen una rehabilitación más rápida y menos complicaciones postoperatorias. Como resultado, la demanda de tejido pre-extraído y precargado de bancos de ojos como el Lions Eye Institute for Transplant & Research está en aumento.

- Este avance hacia procedimientos de trasplante de córnea de última generación está transformando las prácticas clínicas y estableciendo nuevos estándares en la atención oftalmológica en Norteamérica. Por consiguiente, las empresas de dispositivos médicos y los bancos de tejidos de donantes están invirtiendo en programas de capacitación e infraestructura avanzada para impulsar su adopción generalizada.

- Se espera que la creciente disponibilidad de capacitación quirúrgica especializada, la mejora de la logística de los tejidos de los donantes y la preparación del sistema de atención médica consoliden aún más esta tendencia como piedra angular del panorama cambiante del trasplante de córnea en los EE. UU. y Canadá.

Dinámica del mercado de trasplantes de córnea en América del Norte

Conductor

Aumento de la prevalencia de enfermedades corneales y mejor acceso al tejido donante

- La creciente incidencia de enfermedades de la córnea, como el queratocono, la distrofia endotelial de Fuchs y la cicatrización corneal, es un importante impulsor de la expansión del mercado de trasplantes de córnea en América del Norte.

- Por ejemplo, la Asociación de Bancos de Ojos de Estados Unidos (EBAA) informó que se realizaron más de 80.000 trasplantes de córnea en los EE. UU. en 2023, lo que destaca una sólida demanda de procedimientos.

- La mayor disponibilidad de tejido de donantes, apoyada por una red bien organizada de bancos de ojos y campañas de concientización sobre la donación, garantiza un acceso oportuno a injertos de calidad, lo que mejora significativamente los resultados del trasplante.

- Además, los sólidos marcos de reembolso y la mayor cobertura de seguros para procedimientos oftálmicos en los EE. UU. y Canadá están haciendo que los trasplantes de córnea sean más accesibles para una base de pacientes más amplia.

- Las iniciativas de los sectores público y privado para promover el diagnóstico temprano y el tratamiento oportuno de las enfermedades de la córnea contribuyen aún más a la creciente adopción de procedimientos de trasplante, en particular en los centros urbanos con instalaciones de atención médica avanzadas.

Restricción/Desafío

“Escasez de cirujanos cualificados y disparidades regionales en el acceso”

- A pesar del progreso tecnológico, la escasez de cirujanos oftálmicos capacitados en técnicas avanzadas de queratoplastia plantea un desafío para la adopción generalizada de procedimientos modernos de trasplante de córnea en América del Norte.

- Por ejemplo, las zonas rurales tanto de los EE. UU. como de Canadá a menudo enfrentan un acceso limitado a atención especializada, lo que resulta en tiempos de espera más largos y menos opciones quirúrgicas para los pacientes en regiones desatendidas.

- Además, si bien los hospitales urbanos pueden estar bien equipados, las disparidades en la financiación y la infraestructura médica entre provincias y estados dificultan el acceso uniforme a una atención de alta calidad.

- Garantizar una formación más amplia de cirujanos, aumentar la financiación de los servicios oftalmológicos en zonas remotas y fortalecer las redes interregionales de intercambio de tejidos serán esenciales para superar estas limitaciones y asegurar un acceso equitativo a la atención del trasplante de córnea.

- Si bien los trasplantes de córnea están cubiertos por el seguro en muchos casos, el costo total (incluidas las evaluaciones preoperatorias, las herramientas quirúrgicas avanzadas, el procesamiento del tejido del donante y la atención posoperatoria) puede ser alto.

- La carga financiera es especialmente significativa para procedimientos que implican técnicas de vanguardia como la DMEK o la queratoplastia asistida por láser de femtosegundo. Para los pacientes sin seguro médico integral o en regiones con políticas de reembolso limitadas, el costo se convierte en una barrera crítica para el acceso.

Alcance del mercado de trasplante de córnea en América del Norte

El mercado está segmentado según el tipo de procedimiento, tipo, tipo de donante, tipo de injerto, tipo de cirugía, indicación, género, grupo de edad y usuario final.

- Por tipo de procedimiento

Según el tipo de procedimiento, el mercado norteamericano de trasplante de córnea se segmenta en queratoplastia endotelial, queratoplastia penetrante, queratoplastia lamelar anterior (ALK), trasplante de células madre limbares corneales, trasplante de córnea artificial, entre otros. El segmento de la queratoplastia penetrante dominó el mercado con la mayor participación en ingresos, con un 47,2 % en 2024, gracias a su reconocida utilidad clínica y eficacia en el tratamiento de enfermedades corneales de espesor completo. Continúa siendo ampliamente utilizado en casos de cicatrices corneales graves y queratocono.

Se prevé que el segmento de la queratoplastia endotelial experimente el mayor crecimiento entre 2025 y 2032, impulsado por avances en técnicas quirúrgicas como la DMEK y la DSAEK. Estos enfoques ofrecen una mejor recuperación visual, reducen las complicaciones y son cada vez más preferidos por los cirujanos para el tratamiento de trastornos endoteliales como la distrofia de Fuchs.

- Por tipo

Según el tipo, el mercado norteamericano de trasplantes de córnea se segmenta en córnea humana y sintética. El segmento de córnea humana obtuvo la mayor cuota de mercado en 2024, gracias a la sólida presencia de bancos de ojos y al uso generalizado de tejido de donantes en procedimientos de trasplante. Las altas tasas de supervivencia de los injertos y la disponibilidad a través de los sistemas nacionales de donación contribuyen al predominio de este segmento.

Se prevé que el segmento sintético se expanda a un ritmo constante entre 2025 y 2032, impulsado por la innovación en implantes corneales artificiales para pacientes con rechazos múltiples de injertos o aquellos que no son aptos para injertos corneales humanos. El aumento de la investigación en materiales biocompatibles también respalda este crecimiento.

- Por tipo de donante

Según el tipo de donante, el mercado norteamericano de trasplantes de córnea se segmenta en autoinjerto y aloinjerto. El segmento de aloinjerto representó la mayor cuota de mercado en 2024, gracias a su amplia aplicación con tejido de donantes cadavéricos en procedimientos de espesor total y parcial.

Se anticipa que el segmento de autoinjertos experimentará un crecimiento moderado durante el período de pronóstico, particularmente en aplicaciones específicas como trasplantes de células madre limbares y reconstrucción de la superficie ocular donde se utiliza tejido derivado del paciente.

- Por tipo de injerto

Según el tipo de injerto, el mercado norteamericano de trasplantes de córnea se segmenta en injertos de espesor parcial (lamelares) e injertos de espesor completo (penetrantes). El segmento de injertos de espesor completo dominó el mercado en 2024, principalmente debido a la continua dependencia de la queratoplastia penetrante para casos de degeneración corneal avanzada y traumatismos.

Se espera que el segmento de injertos de espesor parcial crezca al ritmo más rápido entre 2025 y 2032, impulsado por la creciente adopción de técnicas endoteliales y lamelares anteriores que ofrecen mejores resultados posoperatorios y tasas de rechazo más bajas.

- Por tipo de cirugía

Según el tipo de cirugía, el mercado norteamericano de trasplante de córnea se segmenta en cirugía convencional y cirugía asistida por láser. El segmento de cirugía convencional obtuvo la mayor participación en los ingresos del mercado en 2024 gracias a su uso prolongado, su rentabilidad y su amplia accesibilidad en centros de cirugía oftalmológica general.

Se prevé que el segmento de cirugía asistida por láser experimente la tasa de crecimiento más rápida entre 2025 y 2032, impulsada por la creciente adopción de la tecnología láser de femtosegundo que mejora la precisión, reduce el tiempo operatorio y mejora la alineación de la interfaz injerto-huésped.

- Por indicación

Según las indicaciones, el mercado norteamericano de trasplantes de córnea se segmenta en distrofia endotelial de Fuchs, queratitis infecciosa, queratopatía bullosa, queratocono, procedimientos de reimplante, cicatrización corneal, úlceras corneales y otras. El segmento de distrofia endotelial de Fuchs dominó el mercado en 2024 debido a su alta prevalencia entre la población de edad avanzada y a la creciente preferencia por las técnicas de queratoplastia endotelial.

Se proyecta que el segmento del queratocono crecerá al ritmo más rápido entre 2025 y 2032, apoyado por la detección temprana de la enfermedad, una mayor concientización y un número cada vez mayor de procedimientos de injerto lamelar selectivo en grupos de pacientes más jóvenes.

- Por género

En cuanto al género, el mercado norteamericano de trasplantes de córnea se segmenta en hombres y mujeres. El segmento masculino obtuvo la mayor participación en los ingresos del mercado en 2024, debido principalmente a la mayor incidencia de lesiones corneales relacionadas con traumatismos y a la exposición ocupacional a riesgos oculares.

Se espera que el segmento femenino registre un crecimiento notable durante el período de pronóstico, apoyado por el aumento del diagnóstico de distrofia de Fuchs entre mujeres mayores y la creciente conciencia de la salud ocular.

- Por grupo de edad

Según el grupo de edad, el mercado norteamericano de trasplantes de córnea se segmenta en geriátrico, adulto y pediátrico. El segmento adulto representó la mayor participación en los ingresos del mercado en 2024, ya que la mayoría de los procedimientos de trasplante se realizan en este grupo demográfico, impulsado por el queratocono y la queratitis infecciosa.

Se proyecta que el segmento geriátrico crecerá al ritmo más rápido entre 2025 y 2032, atribuido a la mayor prevalencia de disfunciones endoteliales y enfermedades oculares degenerativas en las poblaciones envejecidas, particularmente en Estados Unidos y Canadá.

- Por el usuario final

En cuanto al usuario final, el mercado norteamericano de trasplantes de córnea se segmenta en hospitales, clínicas oftalmológicas, centros de cirugía ambulatoria, institutos académicos y de investigación, entre otros. El segmento hospitalario dominó el mercado con la mayor participación en ingresos en 2024, impulsado por la presencia de centros de cirugía oftalmológica avanzados y la alta afluencia de pacientes que buscan atención integral.

Se espera que el segmento de centros quirúrgicos ambulatorios crezca al ritmo más rápido durante el período de pronóstico, debido a tiempos de procedimiento más cortos, rentabilidad y una mayor preferencia de los pacientes por intervenciones quirúrgicas ambulatorias en oftalmología.

Análisis regional del mercado de trasplante de córnea en América del Norte

- Estados Unidos dominó el mercado de trasplante de córnea de América del Norte con la mayor participación en los ingresos del 42,8 % en 2024, caracterizado por una infraestructura de atención médica bien desarrollada, políticas de reembolso de apoyo y la presencia de bancos de ojos y centros de trasplante líderes.

- Los pacientes estadounidenses se benefician de un acceso simplificado al tejido corneal de donantes, la disponibilidad de cirujanos oftálmicos altamente capacitados y una mayor conciencia pública sobre los procedimientos de restauración de la visión, como DMEK y DSAEK.

- Esta posición de liderazgo está respaldada además por una cobertura de seguro favorable, inversiones crecientes en atención oftálmica y la adopción generalizada de técnicas de trasplante innovadoras, posicionando a los EE. UU. como un centro central para los procedimientos de trasplante de córnea en la región.

Perspectiva del mercado de trasplantes de córnea en EE. UU.

El mercado estadounidense de trasplantes de córnea obtuvo la mayor participación en los ingresos en 2024 en Norteamérica, impulsado por la creciente prevalencia de trastornos corneales y la sólida presencia de bancos de ojos y centros quirúrgicos especializados. La avanzada infraestructura sanitaria del país, sumada a la amplia disponibilidad de tejidos de donantes y a la gran cantidad de procedimientos de trasplante, respalda un sólido desempeño del mercado. Además, la creciente adopción de técnicas de queratoplastia endotelial como DMEK y DSAEK, junto con marcos de reembolso favorables, impulsa aún más el mercado. Las continuas innovaciones en el procesamiento de injertos de córnea y la mayor concienciación de los pacientes contribuyen significativamente a un crecimiento sostenido.

Perspectivas del mercado canadiense de trasplantes de córnea

Se proyecta que el mercado canadiense de trasplantes de córnea se expandirá a una tasa de crecimiento anual compuesta (TCAC) notable durante el período de pronóstico, impulsado por mejoras en la atención médica, servicios oftalmológicos financiados por el gobierno y la ampliación del acceso a la atención oftalmológica tanto en zonas urbanas como remotas. El mayor enfoque nacional en la salud ocular, junto con el crecimiento de los programas de capacitación quirúrgica y la colaboración con bancos de ojos estadounidenses, está mejorando la capacidad para realizar procedimientos. La creciente demanda de opciones de trasplante mínimamente invasivas, las iniciativas de concienciación pública y la creciente inversión en investigación oftalmológica contribuyen al avance constante del mercado en todo Canadá.

Perspectiva del mercado de trasplante de córnea en México

Se prevé que el mercado mexicano de trasplantes de córnea crezca de forma sostenida durante el período de pronóstico, impulsado por el aumento de la inversión pública y privada en servicios de atención oftalmológica, el aumento de la prevalencia de ceguera corneal y la mejora gradual de la accesibilidad a la atención médica. Los programas gubernamentales que promueven la donación de órganos y tejidos, junto con la expansión de la capacidad quirúrgica oftalmológica en hospitales urbanos, están impulsando el desarrollo del mercado. Si bien el acceso a las córneas de donantes sigue siendo un desafío en algunas regiones, las colaboraciones internacionales y las iniciativas sin fines de lucro están ayudando a reducir la brecha en la disponibilidad de tejidos y la capacitación quirúrgica. A medida que se mejora la concientización y la infraestructura de atención médica, México se prepara para presenciar un crecimiento sostenido en los procedimientos de trasplante de córnea.

Cuota de mercado de trasplante de córnea en América del Norte

La industria de trasplante de córnea de América del Norte está liderada principalmente por empresas bien establecidas, entre las que se incluyen:

- CorneaGen, Inc. (EE. UU.)

- KeraLink International (EE. UU.)

- SightLife (EE. UU.)

- Eversight (EE. UU.)

- Instituto Lions Eye para Trasplantes e Investigación (EE. UU.)

- Bausch + Lomb (EE. UU.)

- Alcon Inc. (Suiza)

- Aurolab (India)

- Bancos de Tejidos Internacionales (EE. UU.)

- El Banco de Ojos para la Restauración de la Vista (EE. UU.)

- Banco de ojos de San Diego (EE. UU.)

- Lions VisionGift (EE. UU.)

- Hospital Oftalmológico Wills (EE. UU.)

- New World Medical, Inc. (EE. UU.)

- AJL Oftalmológica SA (España)

- Banco de ojos para la restauración de la vista (EE. UU.)

- DIOPTEX GmbH (Austria)

- Red para la Intercambio de Órganos Pancreáticos (EE. UU.)

- Keramed, Inc. (EE. UU.)

- Stryker (EE. UU.)

¿Cuáles son los desarrollos recientes en el mercado de trasplante de córnea en América del Norte?

- En mayo de 2024, la Asociación Americana de Bancos de Ojos (EBAA) lanzó una campaña nacional de concienciación en todo Estados Unidos para promover la donación de córneas y educar al público sobre el impacto transformador de los trasplantes. La iniciativa busca abordar la creciente demanda de tejidos de donantes y mejorar las tasas de donación. Mediante la colaboración con hospitales, centros de trasplantes y grupos de apoyo, la campaña refuerza la importancia de la salud corneal y fortalece la cadena de suministro de donantes para los procedimientos de trasplante.

- En abril de 2024, la Universidad de Columbia Británica (Canadá) anunció la aplicación clínica exitosa de un novedoso implante corneal de bioingeniería, desarrollado en colaboración con investigadores internacionales. Esta innovación ofrece una alternativa prometedora para pacientes con difícil acceso a tejidos donantes, en particular aquellos con queratocono avanzado. Este avance representa un avance significativo en la oftalmología regenerativa y amplía las posibilidades futuras del trasplante de córnea sintética en Norteamérica.

- En marzo de 2024, CorneaGen, Inc., empresa estadounidense de suministro e innovación de tejido corneal, amplió su red de distribución en Canadá y México con el objetivo de optimizar el acceso a tejidos preextraídos y precargados para la queratoplastia endotelial. Esta iniciativa mejora la eficiencia del procedimiento y apoya a los cirujanos oftalmológicos con injertos listos para usar, estandarizando aún más la atención de trasplantes de alta calidad en toda Norteamérica.

- En febrero de 2024, el Hospital Toronto Western inauguró un Centro de Cirugía Corneal Avanzada, enfocado en la capacitación de oftalmólogos en técnicas de vanguardia como DMEK y DALK. Esta iniciativa aborda la escasez de cirujanos especializados en Canadá y refuerza los esfuerzos regionales para mejorar los resultados mediante la excelencia quirúrgica y la educación.

- En enero de 2024, SightLife, un banco de ojos global sin fines de lucro con sede en EE. UU., se asoció con la Secretaría de Salud de México para fortalecer el marco nacional de donación de córneas. El programa incluye capacitación técnica, iniciativas de concientización pública y sistemas de garantía de calidad para el manejo de tejidos, lo que representa un paso significativo para mejorar la infraestructura y los resultados de los trasplantes en regiones marginadas de Norteamérica.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.