North America Acrylic Monomers Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

1,107,202.15 Thousand

USD

1,608,199.90 Thousand

2022

2030

USD

1,107,202.15 Thousand

USD

1,608,199.90 Thousand

2022

2030

| 2023 –2030 | |

| USD 1,107,202.15 Thousand | |

| USD 1,608,199.90 Thousand | |

| % | |

Mercado de monómeros acrílicos de América del Norte, por producto (acrilato, ácidos acrílicos y sales, acrílicos polifuncionales, acrílicos de bisfenol, acrílicos fluorados, acrilonitrilo, acrilamida y metacrilamida, monómeros de carbohidratos, malemida y otros), aplicación (plástico, adhesivos y selladores, resinas sintéticas, fibras acrílicas, materiales de construcción, telas, caucho acrílico y otros), uso final (pinturas y recubrimientos, construcción y edificación, automotriz, bienes de consumo, empaque, tratamiento de agua, marino, aeroespacial y otros) - Tendencias de la industria y pronóstico hasta 2030.

Análisis y tamaño del mercado de monómeros acrílicos de América del Norte

El mercado de monómeros acrílicos de América del Norte está impulsado por el aumento del gasto en el sector de la construcción. Además, una perspectiva positiva hacia la industria de pinturas y revestimientos es un factor importante para el mercado. Además, se espera que el cambio de enfoque de los fabricantes hacia monómeros acrílicos ecológicos impulse el crecimiento del mercado. Sin embargo, se espera que el cumplimiento de estándares regulatorios complejos y cambiantes frene el crecimiento del mercado.

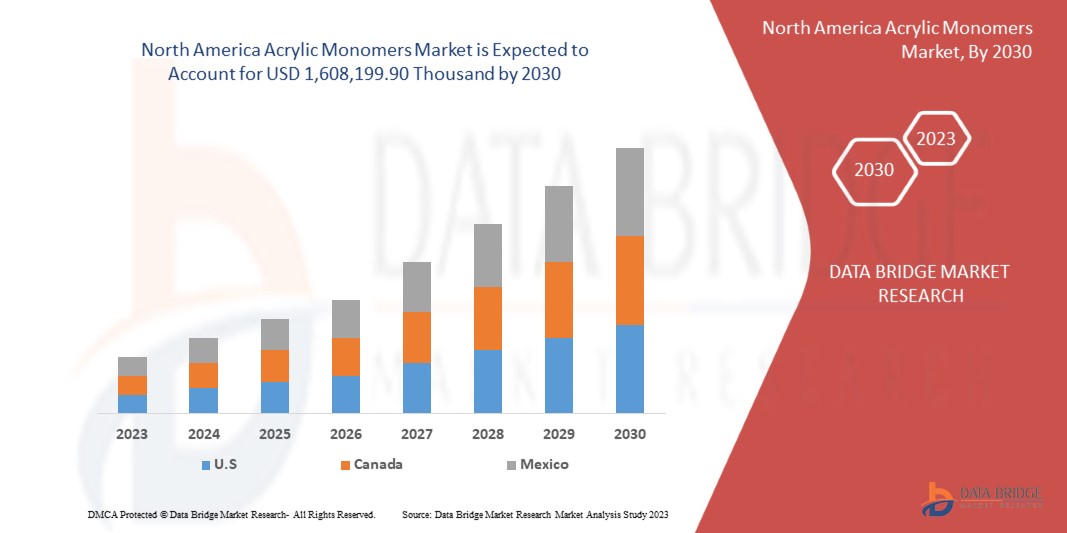

Data Bridge Market Research analiza que se espera que el mercado de monómeros acrílicos de América del Norte alcance los USD 1.608.199,90 mil para 2030 desde USD 1.107.202,15 mil en 2022, creciendo con una CAGR del 4,9% durante el período de pronóstico de 2023 a 2030.

|

Métrica del informe |

Detalles |

|

Período de pronóstico |

2023 a 2030 |

|

Año base |

2022 |

|

Años históricos |

2021 (Personalizable 2015-2020) |

|

Unidades cuantitativas |

Ingresos en miles de USD, Volumen en miles de litros |

|

Segmentos cubiertos |

Producto (Acrilato, Ácidos y sales acrílicos, Acrílicos polifuncionales, Acrílicos de bisfenol, Acrílicos fluorados, Acrilonitrilo, Acrilamida y metacrilamida, Monómeros de carbohidratos, Malemida y otros), Aplicación (Plástico, Adhesivos y selladores, Resinas sintéticas, Fibras acrílicas, Materiales de construcción, Telas, Caucho acrílico y otros), Uso final (Pinturas y recubrimientos, Construcción y edificación, Automotriz, Bienes de consumo, Empaques, Tratamiento de agua , Marina, Aeroespacial y otros) |

|

Países cubiertos |

Estados Unidos, Canadá y México |

|

Actores del mercado cubiertos |

BASF SE, Arkema, Mitsubishi Chemical Group Corporation, Dow, LG Chem, Evonik Industries AG, NIPPON SHOKUBAI CO., LTD., LobaChemie Pvt Ltd., Solventis y Tokyo Chemical Industries CO., Ltd. |

Definición de mercado

Los monómeros acrílicos están compuestos por ácido acrílico y sus acrilatos asociados. Estos compuestos constituyen principalmente acrilatos, ácido acrílico o polímeros. Los monómeros acrílicos son conocidos por su alta reactividad. Se suelen combinar con polvo de polímero para crear uñas acrílicas duraderas. El metacrilato de etilo (EMA) es un componente típico de los monómeros acrílicos debido a su excepcional resistencia, curado rápido y excelentes propiedades de adhesión.

Dinámica del mercado de monómeros acrílicos en América del Norte

En esta sección se aborda la comprensión de los factores impulsores, las limitaciones, las oportunidades y los desafíos del mercado. Todos ellos se analizan en detalle a continuación:

Conductores

- Perspectivas positivas para la industria de pinturas y recubrimientos

La industria de pinturas y recubrimientos tiene una perspectiva positiva con respecto al mercado de monómeros acrílicos, impulsada por varios factores y aplicaciones que contribuyen a su crecimiento. Uno de los principales impulsores de la perspectiva positiva para la industria de pinturas y recubrimientos es el uso extensivo de monómeros acrílicos, específicamente acrilato de N-butilo. Estos monómeros sirven como bloques de construcción esenciales para los copolímeros utilizados en la formulación de pinturas y recubrimientos. Estas propiedades incluyen la capacidad de formar polímeros hidrófobos, que son cruciales para crear recubrimientos que brinden protección y durabilidad. Esta propiedad los hace particularmente valiosos en la formulación de recubrimientos, donde la resistencia al agua y la durabilidad son esenciales. El metacrilato, otro monómero acrílico esencial derivado del ácido metacrílico, disfruta de un uso generalizado en diversas aplicaciones, incluidas las pantallas de computadora y las pinturas.

La demanda de recubrimientos de alto rendimiento con una durabilidad excepcional, resistencia a la intemperie y claridad ha ido en aumento. Los monómeros acrílicos, con su naturaleza hidrófoba y su capacidad para formar polímeros resistentes, satisfacen estas demandas de manera eficaz. Los fabricantes de la industria de pinturas y recubrimientos recurren cada vez más a los copolímeros acrílicos para mejorar la calidad y la longevidad de sus productos. La expansión de los proyectos de construcción e infraestructura en todo el mundo ha generado una demanda significativa de pinturas y recubrimientos, lo que está impulsando el crecimiento del mercado.

- Aumento del gasto en el sector de la construcción

El sector de la construcción es un pilar fundamental del desarrollo económico de América del Norte, ya que configura el perfil de las ciudades y sienta las bases para el crecimiento de la infraestructura. El aumento del gasto en construcción se atribuye principalmente a la creciente urbanización y expansión de la población. Con el aumento de la población mudándose a las ciudades, existe una creciente demanda de desarrollo residencial, comercial y de infraestructura. Los gobiernos y los inversores privados están invirtiendo fondos sustanciales en proyectos de construcción para satisfacer estas demandas. Este aumento de la actividad de la construcción actúa como catalizador para el mercado de monómeros acrílicos.

Los monómeros acrílicos, con su capacidad para fortalecer el hormigón, son la solución ideal. Refuerzan la matriz del hormigón, reduciendo el riesgo de grietas y fracturas. Esta mayor durabilidad garantiza que las estructuras puedan soportar la prueba del tiempo, alineándose perfectamente con los objetivos a largo plazo de los proyectos de construcción. Los monómeros acrílicos desempeñan un papel fundamental en este esfuerzo al mejorar la trabajabilidad y la fluidez del hormigón. Con relaciones agua-cemento optimizadas y una mayor fluidez, los equipos de construcción pueden verter y consolidar el hormigón de manera eficiente, lo que permite la realización de diseños intrincados y atrevidos. Esto no solo ahorra tiempo, sino que también reduce los costos de mano de obra, lo que lo convierte en una opción económicamente atractiva para los proyectos de construcción. Los monómeros acrílicos proporcionan la adherencia, la resistencia al agua y la durabilidad requeridas, lo que los convierte en un componente indispensable en la construcción de estas estructuras monumentales, lo que impulsa el crecimiento del mercado.

Oportunidades

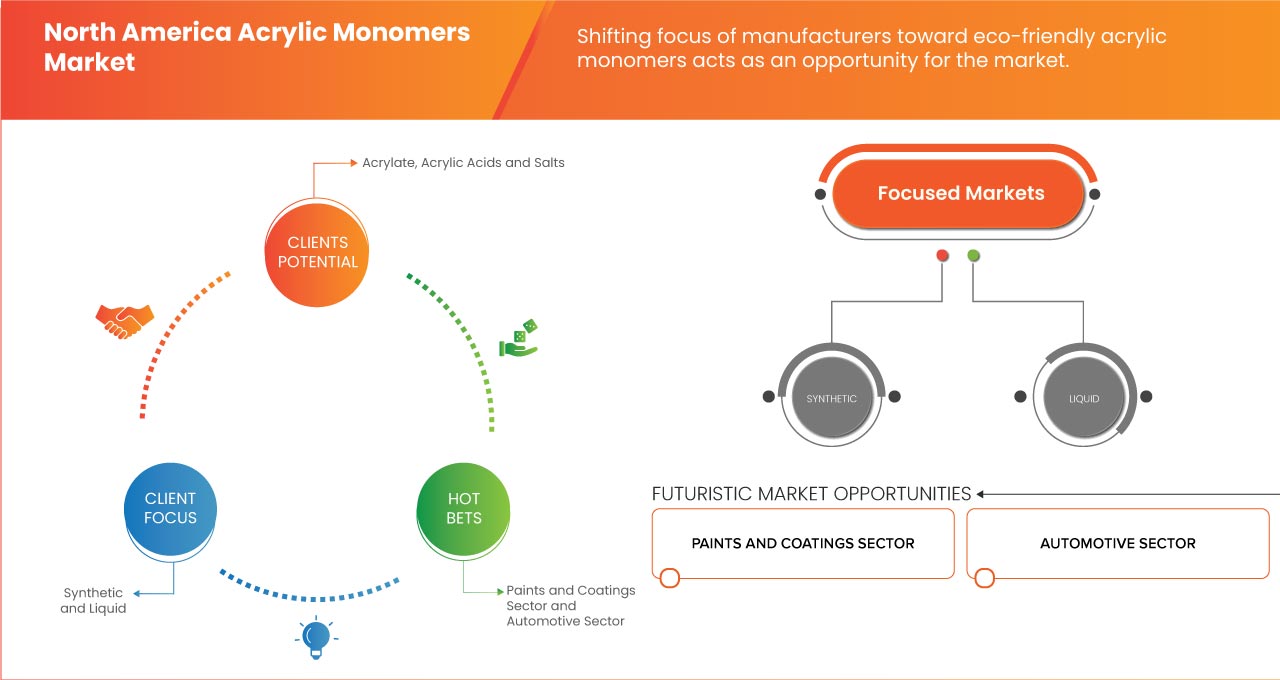

- Los fabricantes están cambiando su enfoque hacia los monómeros acrílicos ecológicos

El mercado de los monómeros acrílicos está experimentando actualmente un cambio de enfoque significativo, ya que los fabricantes están centrando cada vez más su atención en los monómeros acrílicos ecológicos. Un factor clave detrás de este cambio es la creciente preocupación por el medio ambiente. En los últimos años, ha habido una creciente conciencia del impacto ambiental de los monómeros acrílicos tradicionales, que a menudo se derivan de combustibles fósiles y pueden liberar emisiones nocivas durante su producción. Esto ha llevado a una mayor demanda de alternativas más respetuosas con el medio ambiente. Los fabricantes ahora están invirtiendo en investigación y desarrollo para crear monómeros acrílicos que se deriven de recursos renovables y tengan un impacto ambiental reducido.

Además, las estrictas regulaciones y políticas gubernamentales destinadas a reducir las emisiones de gases de efecto invernadero están impulsando a los fabricantes a adoptar prácticas más sostenibles. Esta presión regulatoria está impulsando el desarrollo y la adopción de monómeros acrílicos ecológicos como un medio para cumplir con las normas ambientales. Como resultado, los fabricantes que adopten este cambio de enfoque probablemente obtendrán una ventaja competitiva en el mercado. El cambio hacia monómeros acrílicos ecológicos también se alinea con las preferencias cambiantes de los consumidores. Los consumidores de hoy son más conscientes del medio ambiente y buscan cada vez más productos que se produzcan mediante procesos sostenibles y ecológicos, lo que brinda la oportunidad de crecimiento del mercado.

- Inmenso potencial en la industria del tratamiento del agua

La industria del tratamiento del agua está experimentando actualmente un inmenso potencial, lo que crea una oportunidad prometedora para el mercado de monómeros acrílicos. En los últimos años, las preocupaciones sobre la contaminación y la escasez del agua han aumentado significativamente, lo que impulsa la necesidad de soluciones efectivas para el tratamiento del agua. Los monómeros acrílicos, en particular el ácido acrílico glacial, desempeñan un papel crucial en esta industria, ya que se utilizan como polímeros floculantes. Estos polímeros ayudan a eliminar impurezas y contaminantes del agua, lo que la hace más segura y adecuada para diversas aplicaciones.

Una de las principales aplicaciones de los monómeros acrílicos, como el ácido acrílico glacial, es su papel como polímeros floculantes. En los procesos de tratamiento de agua, los floculantes son sustancias que ayudan en la aglomeración y precipitación de partículas suspendidas. El ácido acrílico glacial puede servir como monómero para la producción de estos polímeros floculantes. Cuando se añaden al agua, estos polímeros se unen a las impurezas y contaminantes, haciendo que formen copos aglomerados. Este proceso es fundamental para la eliminación de contaminantes, incluida la materia orgánica, los productos químicos y los metales pesados, de las fuentes de agua. Los copos aglomerados formados con la ayuda de monómeros acrílicos se pueden filtrar fácilmente, lo que da como resultado un agua más limpia. Esto es particularmente valioso en industrias donde la calidad del agua es de suma importancia, como plantas de tratamiento de agua municipales, procesos industriales e incluso en la producción de agua potable. La capacidad de los monómeros acrílicos para mejorar la eficiencia de los procesos de tratamiento de agua al facilitar la eliminación de impurezas es un factor significativo que contribuye a su relevancia en la industria del tratamiento de agua.

Restricciones/ Desafíos

- Fluctuaciones en los precios de las materias primas

Los monómeros acrílicos se fabrican a partir de ingredientes como el propileno y el isobutileno. Cuando los precios de estas materias primas aumentan repentinamente, la producción de monómeros acrílicos se encarece. Los fabricantes podrían verse obligados a cobrar más por sus productos o ver disminuir sus ganancias.

Las empresas que utilizan monómeros acrílicos para fabricar pinturas, adhesivos o revestimientos dependen de un suministro y un coste estables de estos monómeros para planificar sus presupuestos y precios. Cuando los precios de las materias primas suben, se trastocan estos planes, lo que provoca incertidumbre en el mercado.

Además, estas fluctuaciones de precios pueden afectar más a las empresas más pequeñas y a las empresas emergentes, ya que podrían no tener los recursos para afrontar aumentos repentinos de costos, lo que puede dificultarles competir en el mercado.

Además, las industrias que utilizan monómeros acrílicos, como la construcción, la automoción y las pinturas y revestimientos , también sienten el impacto. Los costos impredecibles pueden afectar sus proyectos y presupuestos, lo que puede provocar retrasos o mayores gastos.

- Cumplimiento de normas regulatorias complejas y en constante evolución

En la industria de los monómeros acrílicos, existen normas establecidas por los gobiernos y las agencias ambientales de todo el mundo. Estas normas están ahí para garantizar la seguridad de los trabajadores, los consumidores y el medio ambiente. Pueden incluir límites en el uso de determinados productos químicos o directrices sobre cómo deben gestionarse los residuos.

Cumplir con estas normativas suele requerir inversiones significativas en investigación y desarrollo. Es posible que las empresas deban reformular sus productos, cambiar sus procesos de producción o invertir en nuevos equipos para cumplir con estas normas. La documentación y los trámites necesarios para el cumplimiento también pueden ser abrumadores, lo que puede ralentizar el desarrollo de productos y aumentar los costes.

Además, el incumplimiento puede dar lugar a multas, problemas legales y daños a la reputación de la empresa, lo que se espera que suponga un desafío para el crecimiento del mercado.

Acontecimientos recientes

- En septiembre de 2023, BASF SE amplió su creciente cartera de monómeros de base biológica 14C con un proceso patentado para la producción de acrilato de 2-octilo (2-OA). El nuevo producto subraya el fuerte compromiso de BASF con la innovación para un futuro sostenible con un 73 % de contenido de base biológica trazable al 14C de acuerdo con la norma ISO 16620. Además del acrilato de 2-octilo 14C de base biológica habitual, BASF también lanzó un nuevo producto, el acrilato de 2-octilo BMB ISCC Plus.

- En abril de 2023, Evonik recibió la certificación DIN CERTCO para sus monómeros de metacrilato de base biológica VISIOMER Terra, lo que confirma un biocontenido de hasta el 85 %. Esta certificación, basada en el método de radiocarbono C14 y el protocolo ASTM D 6866:2021, destaca el compromiso de Evonik con la sostenibilidad y la mitigación del cambio climático.

- En enero de 2023, Mitsubishi Chemical Group Corporation y Mitsui Chemicals iniciaron una investigación conjunta para estandarizar y optimizar la logística química, que es la base tanto de la sociedad como de la industria. Las corporaciones quieren implementar gradualmente actividades en una variedad de temas clave, y se espera que las que se puedan ejecutar de inmediato comiencen este año fiscal. Las empresas trabajarán juntas para desarrollar una logística química más sólida y sostenible.

- En septiembre de 2019, Archer Daniels Midland y LG Chem formaron una asociación para desarrollar ácido acrílico de origen biológico, un componente clave en los polímeros superabsorbentes utilizados en productos como los pañales. Este esfuerzo conjunto se centra en proporcionar alternativas sostenibles al ácido acrílico de origen petroquímico que se utiliza actualmente.

Alcance del mercado de monómeros acrílicos en América del Norte

El mercado de monómeros acrílicos de América del Norte se divide en tres segmentos según el producto, la aplicación y el uso final. El crecimiento entre estos segmentos le ayudará a analizar los principales segmentos de crecimiento en las industrias y brindará a los usuarios una valiosa descripción general del mercado y conocimientos del mercado para ayudarlos a tomar decisiones estratégicas para identificar las principales aplicaciones del mercado.

Producto

- Acrilato

- Ácidos y sales acrílicos

- Acrílicos polifuncionales

- Acrílicos de bisfenol

- Acrílicos fluorados

- Acrilonitrilo

- Acrilamida y metacrilamida

- Monómeros de carbohidratos

- Malemida

- Otros

Sobre la base del producto, el mercado está segmentado en acrilamida y metacrilamida, acrilato, ácidos y sales acrílicas, acrilonitrilo, acrílicos de bisfenol, monómeros de carbohidratos, acrílicos fluorados, malemida, acrílicos polifuncionales y otros.

Solicitud

- Plástico

- Adhesivos y selladores

- Resinas Sintéticas

- Fibras acrílicas

- Materiales de construcción

- Telas

- Caucho acrílico

- Otros

Según la aplicación, el mercado está segmentado en plásticos, adhesivos y selladores, resinas sintéticas, fibras acrílicas, materiales de construcción, telas, caucho acrílico y otros.

Uso final

- Pinturas y recubrimientos

- Construcción y edificación

- Automotor

- Bienes de consumo

- Embalaje

- Aeroespacial

- Marina

- Tratamiento de agua

- Otros

En función del uso final, el mercado está segmentado en pinturas y recubrimientos, construcción y edificación, automoción, bienes de consumo, embalaje, tratamiento de agua, marino, aeroespacial y otros.

Análisis y perspectivas regionales del mercado de monómeros acrílicos de América del Norte

Se analiza el mercado de monómeros acrílicos de América del Norte y se proporciona información sobre el tamaño del mercado en función del producto, la aplicación y el uso final.

Los países cubiertos en este informe de mercado son Estados Unidos, Canadá y México.

Se espera que Estados Unidos domine el mercado de monómeros acrílicos de América del Norte debido a la creciente demanda de monómeros acrílicos en la industria de la construcción en el país.

La sección de países del informe también proporciona factores individuales que impactan en el mercado y cambios en la regulación en el mercado a nivel nacional que afectan las tendencias actuales y futuras del mercado. Los puntos de datos como nuevas ventas, ventas de reemplazo, demografía del país, leyes regulatorias y aranceles de importación y exportación son algunos de los principales indicadores utilizados para pronosticar el escenario del mercado para países individuales. Además, la presencia y disponibilidad de marcas regionales y sus desafíos enfrentados debido a la competencia grande o escasa de las marcas locales y nacionales y el impacto de los canales de venta se consideran al proporcionar un análisis de pronóstico de los datos del país.

Análisis del panorama competitivo y de la cuota de mercado de monómeros acrílicos en América del Norte

El panorama competitivo del mercado de monómeros acrílicos de América del Norte proporciona detalles de los competidores. Los detalles incluidos son una descripción general de la empresa, las finanzas de la empresa, los ingresos generados, el potencial de mercado, la inversión en investigación y desarrollo, las nuevas iniciativas de mercado, la presencia regional, los sitios e instalaciones de producción, las capacidades de producción, las fortalezas y debilidades de la empresa, el lanzamiento de productos, la amplitud y variedad de productos y el dominio de las aplicaciones. Los puntos de datos anteriores proporcionados solo están relacionados con el enfoque de las empresas en el mercado.

Algunos de los principales actores del mercado que operan en el mercado de monómeros acrílicos de América del Norte son BASF SE, Arkema, Mitsubishi Chemical Group Corporation, Dow, LG Chem, Evonik Industries AG, NIPPON SHOKUBAI CO., LTD., LobaChemie Pv.t Ltd., Solventis y Tokyo Chemical Industries CO., Ltd., entre otros.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Tabla de contenido

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 PRODUCT LIFE LINE CURVE

2.7 MULTIVARIATE MODELING

2.8 MARKET END-USE COVERAGE GRID

2.9 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.1 DBMR MARKET CHALLENGE MATRIX

2.11 DBMR MARKET POSITION GRID

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTLE ANALYSIS

4.1.1 POLITICAL FACTORS

4.1.2 ECONOMIC FACTORS

4.1.3 SOCIAL FACTORS

4.1.4 TECHNOLOGICAL FACTORS

4.1.5 LEGAL FACTORS

4.1.6 ENVIRONMENTAL FACTORS

4.2 PORTER’S FIVE FORCES

4.2.1 THREAT OF NEW ENTRANTS

4.2.2 THREAT OF SUBSTITUTES

4.2.3 CUSTOMER BARGAINING POWER

4.2.4 SUPPLIER BARGAINING POWER

4.2.5 INTERNAL COMPETITION (RIVALRY)

4.3 VENDOR SELECTION CRITERIA

4.4 RAW MATERIAL COVERAGE

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 POSITIVE OUTLOOK TOWARD PAINTS AND COATINGS INDUSTRY

5.1.2 INCREASING SPENDING IN THE CONSTRUCTION SECTOR

5.1.3 HIGH ADOPTION OF ADHESIVES AND SEALANTS

5.2 RESTRAINTS

5.2.1 FLUCTUATIONS IN THE PRICES OF RAW MATERIALS

5.2.2 AVAILABILITY OF ALTERNATIVE MATERIALS AND TECHNOLOGIES

5.3 OPPORTUNITIES

5.3.1 SHIFTING FOCUS OF MANUFACTURERS TOWARD ECO-FRIENDLY ACRYLIC MONOMERS

5.3.2 IMMENSE POTENTIAL IN THE WATER TREATMENT INDUSTRY

5.4 CHALLENGES

5.4.1 MEETING COMPLEX AND CHANGING REGULATORY STANDARDS

5.4.2 INTERNAL COMPETITION IN THE MARKET

6 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY PRODUCT

6.1 OVERVIEW

6.2 ACRYLATE

6.2.1 BUTYL ACRYLATE MONOMER

6.2.2 METHYL ACRYLATE MONOMER

6.2.3 METHYL METHACRYLATE MONOMER

6.2.4 ETHYL HEXYL ACRYLATE MONOMER

6.2.5 ETHYL ACRYLATE MONOMER

6.2.6 OTHERS

6.3 ACRYLIC ACIDS AND SALTS

6.4 POLYFUNCTIONAL ACRYLICS

6.5 BISPHENOL ACRYLICS

6.6 FLUORINATED ACRYLICS

6.7 ACRYLONITRILE

6.8 ACRYLAMIDE AND METHACRYLAMIDE

6.9 CARBOHYDRATE MONOMERS

6.1 MALEMIDE

6.11 OTHERS

7 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY APPLICATION

7.1 OVERVIEW

7.2 PLASTIC

7.2.1 PLASTIC MANUFACTURING

7.2.2 PLASTIC ADDITIVES

7.3 ADHESIVES AND SEALANTS

7.4 SYNTHETIC RESINS

7.5 ACRYLIC FIBERS

7.6 BUILDING MATERIALS

7.7 FABRICS

7.7.1 KNITTED

7.7.2 WOVEN

7.7.3 NONWOVEN

7.7.4 OTHERS

7.8 ACRYLIC RUBBER

7.9 OTHERS

8 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY END-USE

8.1 OVERVIEW

8.2 PAINTS AND COATINGS

8.2.1 ACRYLIC ACIDS AND SALTS

8.2.2 BISPHENOL ACRYLICS

8.2.3 POLYFUNCTIONAL ACRYLICS

8.2.4 FLUORINATED ACRYLICS

8.2.5 ACRYLONITRILE

8.2.6 ACRYLAMIDE AND METHACRYLAMIDE

8.2.7 MALEMIDE

8.2.8 CARBOHYDRATE MONOMERS

8.2.9 OTHERS

8.3 BUILDING AND CONSTRUCTION

8.3.1 ACRYLATE

8.3.2 POLYFUNCTIONAL ACRYLICS

8.3.3 ACRYLIC ACIDS AND SALTS

8.3.4 BISPHENOL ACRYLICS

8.3.5 ACRYLONITRILE

8.3.6 CARBOHYDRATE MONOMERS

8.3.7 FLUORINATED ACRYLICS

8.3.8 ACRYLAMIDE AND METHACRYLAMIDE

8.3.9 MALEMIDE

8.3.10 OTHERS

8.4 AUTOMOTIVE

8.4.1 ACRYLATE

8.4.2 POLYFUNCTIONAL ACRYLICS

8.4.3 ACRYLONITRILE

8.4.4 ACRYLIC ACIDS AND SALTS

8.4.5 BISPHENOL ACRYLICS

8.4.6 FLUORINATED ACRYLICS

8.4.7 ACRYLAMIDE AND METHACRYLAMIDE

8.4.8 MALEMIDE

8.4.9 CARBOHYDRATE MONOMERS

8.4.10 OTHERS

8.5 CONSUMER GOODS

8.5.1 ACRYLATE

8.5.2 ACRYLIC ACIDS AND SALTS

8.5.3 POLYFUNCTIONAL ACRYLICS

8.5.4 BISPHENOL ACRYLICS

8.5.5 FLUORINATED ACRYLICS

8.5.6 CARBOHYDRATE MONOMERS

8.5.7 ACRYLAMIDE AND METHACRYLAMIDE

8.5.8 ACRYLONITRILE

8.5.9 MALEMIDE

8.5.10 OTHERS

8.6 PACKAGING

8.6.1 ACRYLATE

8.6.2 POLYFUNCTIONAL ACRYLICS

8.6.3 ACRYLIC ACIDS AND SALTS

8.6.4 BISPHENOL ACRYLICS

8.6.5 FLUORINATED ACRYLICS

8.6.6 CARBOHYDRATE MONOMERS

8.6.7 ACRYLAMIDE AND METHACRYLAMIDE

8.6.8 MALEMIDE

8.6.9 OTHERS

8.7 AEROSPACE

8.7.1 ACRYLATE

8.7.2 POLYFUNCTIONAL ACRYLICS

8.7.3 FLUORINATED ACRYLICS

8.7.4 BISPHENOL ACRYLICS

8.7.5 ACRYLIC ACIDS AND SALTS

8.7.6 ACRYLAMIDE AND METHACRYLAMIDE

8.7.7 CARBOHYDRATE MONOMERS

8.7.8 ACRYLONITRILE

8.7.9 MALEMIDE

8.7.10 OTHERS

8.8 MARINE

8.8.1 ACRYLATE

8.8.2 POLYFUNCTIONAL ACRYLICS

8.8.3 FLUORINATED ACRYLICS

8.8.4 ACRYLIC ACIDS AND SALTS

8.8.5 BISPHENOL ACRYLICS

8.8.6 ACRYLAMIDE AND METHACRYLAMIDE

8.8.7 CARBOHYDRATE MONOMERS

8.8.8 ACRYLONITRILE

8.8.9 MALEMIDE

8.8.10 OTHERS

8.9 WATER TREATMENT

8.9.1 ACRYLAMIDE AND METHACRYLAMIDE

8.9.2 POLYFUNCTIONAL ACRYLICS

8.9.3 ACRYLIC ACIDS AND SALTS

8.9.4 ACRYLATE

8.9.5 OTHERS

8.1 OTHERS

8.10.1 ACRYLATE

8.10.2 ACRYLIC ACIDS AND SALTS

8.10.3 BISPHENOL ACRYLICS

8.10.4 POLYFUNCTIONAL ACRYLICS

8.10.5 FLUORINATED ACRYLICS

8.10.6 ACRYLONITRILE

8.10.7 ACRYLAMIDE AND METHACRYLAMIDE

8.10.8 MALEMIDE

8.10.9 CARBOHYDRATE MONOMERS

8.10.10 OTHERS

9 NORTH AMERICA ACRYLIC MONOMERS MARKET: BY REGION

9.1 NORTH AMERICA

9.1.1 U.S.

9.1.2 CANADA

9.1.3 MEXICO

10 COMPANY SHARE ANALYSIS: NORTH AMERICA

11 SWOT ANALYSIS

12 COMPANY PROFILE

12.1 DOW

12.1.1 COMPANY SNAPSHOT

12.1.2 REVENUE ANALYSIS

12.1.3 PRODUCT PORTFOLIO

12.1.4 RECENT DEVELOPMENT

12.2 BASF SE

12.2.1 COMPANY SNAPSHOT

12.2.2 REVENUE ANALYSIS

12.2.3 PRODUCT PORTFOLIO

12.2.4 RECENT DEVELOPMENT

12.3 EVONIK INDUSTRIES AG

12.3.1 COMPANY SNAPSHOT

12.3.2 REVENUE ANALYSIS

12.3.3 PRODUCT PORTFOLIO

12.3.4 RECENT DEVELOPMENT

12.4 MITSUBISHI CHEMICAL GROUP CORPORATION

12.4.1 COMPANY SNAPSHOT

12.4.2 REVENUE ANALYSIS

12.4.3 PRODUCT PORTFOLIO

12.4.4 RECENT DEVELOPMENT

12.5 ARKEMA

12.5.1 COMPANY SNAPSHOT

12.5.2 REVENUE ANALYSIS

12.5.3 PRODUCT PORTFOLIO

12.5.4 RECENT DEVELOPMENTS

12.6 LG CHEM

12.6.1 COMPANY SNAPSHOT

12.6.2 REVENUE ANALYSIS

12.6.3 PRODUCT PORTFOLIO

12.6.4 RECENT DEVELOPMENT

12.7 LOBACHEMIE PVT. LTD.

12.7.1 COMPANY SNAPSHOT

12.7.2 PRODUCT PORTFOLIO

12.7.3 RECENT DEVELOPMENT

12.8 NIPPON SHOKUBAI CO., LTD.

12.8.1 COMPANY SNAPSHOT

12.8.2 REVENUE ANALYSIS

12.8.3 PRODUCT PORTFOLIO

12.8.4 RECENT DEVELOPMENT

12.9 SOLVENTIS

12.9.1 COMPANY SNAPSHOT

12.9.2 PRODUCT PORTFOLIO

12.9.3 RECENT DEVELOPMENTS

12.1 TOKYO CHEMICAL INDUSTRY CO., LTD.

12.10.1 COMPANY SNAPSHOT

12.10.2 PRODUCT PORTFOLIO

12.10.3 RECENT DEVELOPMENTS

13 QUESTIONNAIRE

14 RELATED REPORTS

Lista de Tablas

TABLE 1 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 2 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (THOUSAND LITERS)

TABLE 3 NORTH AMERICA ACRYLATE IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 4 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY APPLICATION, 2021-2030 (USD THOUSAND)

TABLE 5 NORTH AMERICA PLASTIC IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 6 NORTH AMERICA FABRICS IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 7 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY END-USE, 2021-2030 (USD THOUSAND)

TABLE 8 NORTH AMERICA PAINTS AND COATINGS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 9 NORTH AMERICA BUILDING AND CONSTRUCTION IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 10 NORTH AMERICA AUTOMOTIVE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 11 NORTH AMERICA CONSUMER GOODS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 12 NORTH AMERICA PACKAGING IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 13 NORTH AMERICA AEROSPACE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 14 NORTH AMERICA MARINE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 15 NORTH AMERICA WATER TREATMENT IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 16 NORTH AMERICA OTHERS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 17 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY COUNTRY, 2021-2030 (USD THOUSAND)

TABLE 18 NORTH AMERICA ACRYLIC MONOMERS MARKET, BY COUNTRY, 2021-2030 (THOUSAND LITERS)

TABLE 19 U.S. ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 20 U.S. ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (THOUSAND LITERS)

TABLE 21 U.S. ACRYLATE IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 22 U.S. ACRYLIC MONOMERS MARKET, BY APPLICATION, 2021-2030 (USD THOUSAND)

TABLE 23 U.S. PLASTIC IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 24 U.S. FABRICS IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 25 U.S. ACRYLIC MONOMERS MARKET, BY END-USE, 2021-2030 (USD THOUSAND)

TABLE 26 U.S. PAINTS AND COATINGS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 27 U.S. BUILDING AND CONSTRUCTION IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 28 U.S. AUTOMOTIVE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 29 U.S. CONSUMER GOODS IN ACRYLIC MONOMERS MARKET, PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 30 U.S. PACKAGING IN ACRYLIC MONOMERS MARKET, PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 31 U.S. AEROSPACE IN ACRYLIC MONOMERS MARKET, PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 32 U.S. MARINE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 33 U.S. WATER TREATMENT IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 34 U.S. OTHERS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 35 CANADA ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 36 CANADA ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (THOUSAND LITERS)

TABLE 37 CANADA ACRYLATE IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 38 CANADA ACRYLIC MONOMERS MARKET, BY APPLICATION, 2021-2030 (USD THOUSAND)

TABLE 39 CANADA PLASTIC IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 40 CANADA FABRICS IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 41 CANADA ACRYLIC MONOMERS MARKET, BY END-USE, 2021-2030 (USD THOUSAND)

TABLE 42 CANADA PAINTS AND COATINGS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 43 CANADA BUILDING AND CONSTRUCTION IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 44 CANADA AUTOMOTIVE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 45 CANADA CONSUMER GOODS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 46 CANADA PACKAGING IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 47 CANADA AEROSPACE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 48 CANADA MARINE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 49 CANADA WATER TREATMENT IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 50 CANADA OTHERS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 51 MEXICO ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 52 MEXICO ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (THOUSAND LITERS)

TABLE 53 MEXICO ACRYLATE IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 54 MEXICO ACRYLIC MONOMERS MARKET, BY APPLICATION, 2021-2030 (USD THOUSAND)

TABLE 55 MEXICO PLASTIC IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 56 MEXICO FABRICS IN ACRYLIC MONOMERS MARKET, BY TYPE, 2021-2030 (USD THOUSAND)

TABLE 57 MEXICO ACRYLIC MONOMERS MARKET, BY END-USE, 2021-2030 (USD THOUSAND)

TABLE 58 MEXICO PAINTS AND COATINGS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 59 MEXICO BUILDING AND CONSTRUCTION IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 60 MEXICO AUTOMOTIVE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 61 MEXICO CONSUMER GOODS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 62 MEXICO PACKAGING IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 63 MEXICO AEROSPACE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 64 MEXICO MARINE IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 65 MEXICO WATER TREATMENT IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

TABLE 66 MEXICO OTHERS IN ACRYLIC MONOMERS MARKET, BY PRODUCT, 2021-2030 (USD THOUSAND)

Lista de figuras

FIGURE 1 NORTH AMERICA ACRYLIC MONOMERS MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA ACRYLIC MONOMERS MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA ACRYLIC MONOMERS MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA ACRYLIC MONOMERS MARKET: REGIONAL VS COUNTRY MARKET ANALYSIS

FIGURE 5 NORTH AMERICA ACRYLIC MONOMERS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA ACRYLIC MONOMERS MARKET: PRODUCT LIFE LINE CURVE

FIGURE 7 NORTH AMERICA ACRYLIC MONOMERS MARKET: MULTIVARIATE MODELLING

FIGURE 8 NORTH AMERICA ACRYLIC MONOMERS MARKET: MARKET END-USE COVERAGE GRID

FIGURE 9 NORTH AMERICA ACRYLIC MONOMERS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 10 NORTH AMERICA ACRYLIC MONOMERS MARKET: DBMR MARKET CHALLENGE MATRIX

FIGURE 11 NORTH AMERICA ACRYLIC MONOMERS MARKET: DBMR MARKET POSITION GRID

FIGURE 12 NORTH AMERICA ACRYLIC MONOMERS MARKET: SEGMENTATION

FIGURE 13 INCREASING SPENDING IN THE CONSTRUCTION SECTOR IS EXPECTED TO DRIVE THE GROWTH OF THE NORTH AMERICA ACRYLIC MONOMERS MARKET IN THE FORECAST PERIOD

FIGURE 14 THE ACRYLATE SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST MARKET SHARE OF THE NORTH AMERICA ACRYLIC MONOMERS MARKET IN 2023 AND 2030

FIGURE 15 VENDOR SELECTION CRITERIA

FIGURE 16 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE NORTH AMERICA ACRYLIC MONOMERS MARKET

FIGURE 17 NORTH AMERICA ACRYLIC MONOMERS MARKET: BY PRODUCT, 2022

FIGURE 18 NORTH AMERICA ACRYLIC MONOMERS MARKET: BY APPLICATION, 2022

FIGURE 19 NORTH AMERICA ACRYLIC MONOMERS MARKET: BY END-USE, 2022

FIGURE 20 NORTH AMERICA ACRYLIC MONOMERS MARKET: SNAPSHOT (2022)

FIGURE 21 NORTH AMERICA ACRYLIC MONOMERS MARKET: COMPANY SHARE 2022 (%)

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.