Mercado europeo de automatización de laboratorio, por tipo de producto (equipo, software e informática y analizador), tipo de automatización (automatización modular y automatización total de laboratorio), aplicación (descubrimiento de fármacos, diagnóstico clínico, soluciones genómicas, soluciones proteómicas, bioanálisis, ingeniería de proteínas, liofilización, biología de sistemas, química analítica y otros), usuarios finales (biotecnología y productos farmacéuticos, hospitales y laboratorios, instituciones de investigación y académicas y otros) - Tendencias de la industria y pronóstico hasta 2029.

Análisis y perspectivas del mercado de automatización de laboratorios en Europa

La demanda del mercado de automatización de laboratorios está aumentando debido al avance de la tecnología en todo el mundo. Para el sector de la salud se utilizan equipos y herramientas de automatización de laboratorio. Como el gasto en atención médica ha aumentado debido a varios factores, las principales empresas farmacéuticas y de atención médica tienen que automatizar los laboratorios para brindar servicios de atención médica avanzados en la puerta de su casa en menos tiempo.

La creciente demanda de atención médica en el mercado es la principal causa de la competencia entre las principales empresas de atención médica y farmacéuticas en la mejora de la automatización de laboratorios en todo el mundo. El aumento en el uso de equipos, analizadores y software para el laboratorio se ha aprovechado. El enfoque de los actores del mercado es proporcionar variabilidad de herramientas, equipos, máquinas y técnicas para respaldar el desarrollo y la fabricación de infraestructura de laboratorio automatizada. Los actores del mercado están aportando más inversiones y financiación para construir tecnología y métodos avanzados.

El gasto en atención médica ha aumentado debido a varios factores, como el envejecimiento de la población, la prevalencia de enfermedades crónicas, el aumento de los precios de los medicamentos, los costos de los servicios de atención médica y los costos administrativos, entre otros. Además, los hospitales, los laboratorios privados, los centros de investigación clínica y de diagnóstico están aumentando, lo que aumenta la demanda del mercado de automatización de laboratorios.

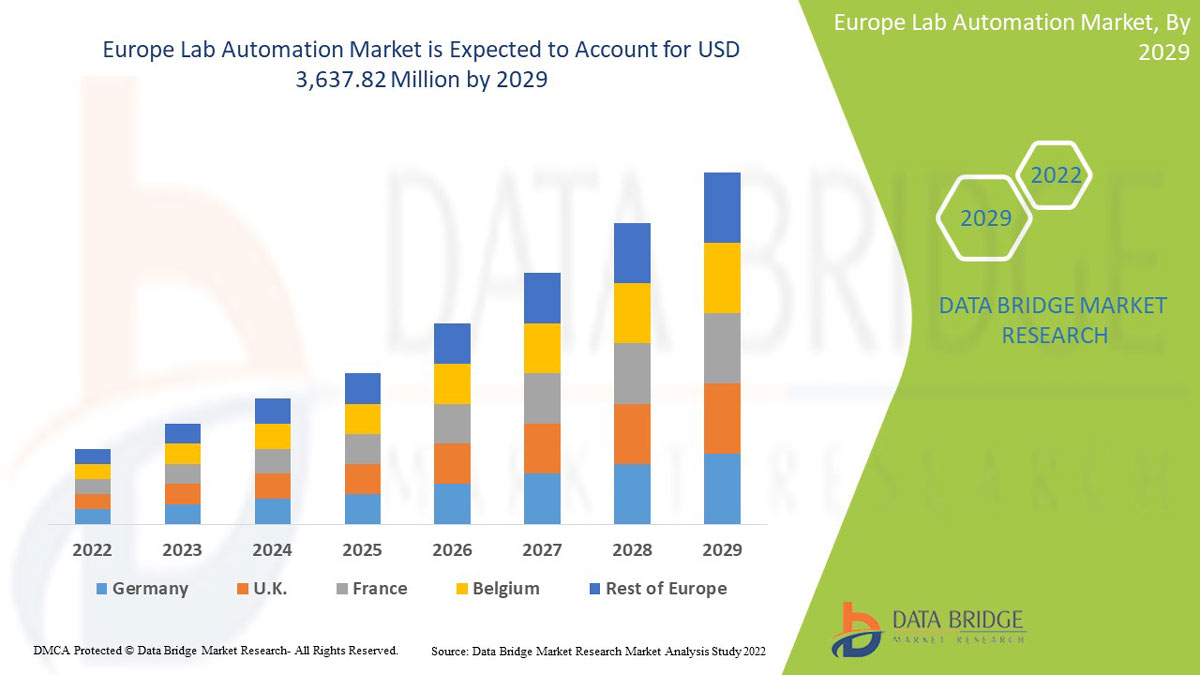

Se espera que el mercado de automatización de laboratorios de Europa gane crecimiento de mercado en el período de pronóstico de 2022 a 2029. Data Bridge Market Research analiza que el mercado está creciendo con una CAGR del 6,0% en el período de pronóstico de 2022 a 2029 y se espera que alcance los USD 3.637,82 millones para 2029.

|

Métrica del informe |

Detalles |

|

Período de pronóstico |

2022 a 2029 |

|

Año base |

2021 |

|

Años históricos |

2020 (Personalizable para 2019-2014) |

|

Unidades cuantitativas |

Ingresos en millones de USD |

|

Segmentos cubiertos |

Por tipo de producto (equipos, software e informática y analizadores), tipo de automatización (automatización modular y automatización total de laboratorio), aplicación (descubrimiento de fármacos, diagnóstico clínico, soluciones genómicas, soluciones proteómicas, bioanálisis, ingeniería de proteínas , liofilización, biología de sistemas, química analítica y otros), usuarios finales ( biotecnología y productos farmacéuticos, hospitales y laboratorios, instituciones académicas y de investigación y otros) |

|

Países cubiertos |

Alemania, Francia, Reino Unido, Italia, España, Países Bajos, Rusia, Bélgica, Suiza, Turquía, Resto de Europa |

|

Actores del mercado cubiertos |

QIAGEN, Siemens Healthcare, F. Hoffman Roche, Hamilton Company, Hudson Robotics, LabVantage Solutions Inc., Abbott, BD, BIOMERIEUX, Aurora Biomed Inc., Danaher, Tecan Trading AG, PerkinElmer Inc, Thermo Fisher Scientific, Agilent Technologies, Azenta US Inc, Eppendorf SE y Labware, entre otros. |

Definición de mercado

La automatización de laboratorio es la combinación de tecnologías automatizadas en el laboratorio para permitir procesos nuevos y mejorados. Se utiliza como estrategia para investigar, desarrollar, optimizar y aprovechar las tecnologías en el laboratorio. Se utiliza especialmente para automatizar procesos de laboratorio que requieren una intervención humana mínima y eliminan el error humano. La automatización de laboratorio se utiliza con el objetivo de proporcionar pruebas y diagnósticos más eficientes.

La automatización de laboratorios permite a los investigadores y técnicos producir resultados de manera eficiente y eficaz en menos tiempo, lo que se espera que impulse el mercado de la automatización de laboratorios. Además, la rápida propagación de enfermedades, junto con los nuevos descubrimientos en el campo de la atención médica, aumentan la demanda de diagnósticos y tratamientos, lo que se espera que impulse el mercado de la automatización de laboratorios. La alta financiación gubernamental y privada para la investigación y el descubrimiento y la presencia de importantes actores del mercado también contribuyen al crecimiento del mercado.

Dinámica del mercado de automatización de laboratorios

Conductores

- Aumento de la inversión y de las iniciativas estratégicas de los actores del mercado

El mercado de la automatización de laboratorios está aumentando debido a la gran demanda de servicios automatizados avanzados especializados que eliminen los errores humanos. El objetivo de los actores del mercado y las empresas es proporcionar una variabilidad de herramientas, equipos, máquinas y técnicas para respaldar el desarrollo y la fabricación de infraestructura de laboratorio automatizada. El mercado de la automatización de laboratorios está aumentando debido a la gran demanda de servicios automatizados avanzados especializados que eliminen los errores humanos. Para captar la participación de mercado, los actores del mercado están realizando más inversiones y financiación para desarrollar tecnología y métodos avanzados. Estos actores están más centrados en reducir los esfuerzos manuales y el tiempo de trabajo práctico para el proceso tradicionalmente intensivo en mano de obra. Se espera que esto impulse el crecimiento del mercado.

- Iniciativas gubernamentales para fortalecer las infraestructuras de laboratorio

Para fortalecer aún más el sector de la atención médica y la infraestructura de laboratorio, las organizaciones gubernamentales desempeñan un papel importante. La financiación y la iniciativa del gobierno para expandir la automatización de laboratorios ayudarán al crecimiento del mercado y aumentarán el número de actores del mercado. Las colaboraciones y los acuerdos del gobierno con los actores clave del mercado fortalecerán aún más la infraestructura de laboratorio.

- Creciente gasto en herramientas y equipos de automatización de laboratorio

El gasto en herramientas y equipos de automatización de laboratorio va en aumento. Esto se debe principalmente a que la demanda de análisis de laboratorio aumenta rápidamente por diversas razones, como el envejecimiento de la población, el aumento de enfermedades crónicas, el descubrimiento de biomarcadores nuevos y más eficaces y un aumento de las demandas generales de salud o de diagnóstico.

- Reducir los esfuerzos humanos y eliminar el error humano

Existen varias formas tradicionales de reducir los errores humanos, pero desarrollar un sistema para minimizar el riesgo de errores humanos ayudará a garantizar que no se repitan los mismos errores nuevamente. Las instalaciones de fabricación se centran en la creación de sistemas avanzados para utilizar tecnología de inteligencia artificial para reconocer y corregir problemas antes de que ocurran.

Oportunidades

-

Aumento del gasto sanitario

El gasto en atención médica ha aumentado debido a varios factores, como el envejecimiento de la población, la prevalencia de enfermedades crónicas, el aumento de los precios de los medicamentos, los costos de los servicios de atención médica y los costos administrativos, entre otros. Sin embargo, 2020 fue el punto de inflexión en el que los gastos ocuparon el primer lugar debido a la pandemia de COVID-19. Se ha descubierto que en 2020, el gasto en atención médica creció al ritmo de crecimiento más rápido experimentado desde 2002 debido a la pandemia .

-

Iniciativas estratégicas de actores clave

Las principales empresas farmacéuticas y de atención médica han tomado varias iniciativas para automatizar los laboratorios y ofrecer servicios de atención médica avanzados en menos tiempo. La creciente demanda de atención médica en el mercado es la principal causa de competencia entre las principales empresas farmacéuticas y de atención médica en la mejora de la automatización de laboratorios en todo el mundo. Por lo tanto, se espera que las iniciativas estratégicas de los actores del mercado actúen como una oportunidad para el crecimiento del mercado de automatización de laboratorios.

-

Aumento del número de empresas farmacéuticas

La industria farmacéutica ha experimentado un crecimiento significativo durante las últimas dos décadas. El aumento de los ingresos disponibles, el mayor acceso a los servicios de salud, la creciente concienciación sobre la atención sanitaria entre las personas y la mayor penetración de los servicios médicos están haciendo que las empresas farmacéuticas aumenten en número para satisfacer la demanda.

La pandemia de COVID-19 tuvo un gran impacto en la industria farmacéutica debido al aumento de la demanda de servicios médicos y suministros de medicamentos. Las industrias farmacéuticas han estado creciendo rápidamente en todo el mundo para satisfacer la alta demanda de la humanidad y, por lo tanto, el servicio debe brindarse lo antes posible. Por lo tanto, para lograr instalaciones de atención médica avanzadas que brinden un servicio rápido y sin errores en menos tiempo, se necesita la automatización de laboratorios. Por lo tanto, se espera que el aumento en el número de empresas farmacéuticas actúe como una oportunidad para el crecimiento del mercado de automatización de laboratorios.

Restricciones/Desafíos

- Limitación del análisis de nuevos productos complejos

Existen diversos factores que contribuyen a la complejidad de los nuevos productos que se utilizan en los laboratorios automatizados. La interacción constante entre el personal y los fabricantes de dispositivos en las primeras fases del proceso de desarrollo es muy necesaria y se vuelve obligatoria para comprender el funcionamiento de la pieza o la configuración general. Las limitaciones en la detección y el análisis de nuevos productos complejos, como máquinas, herramientas y equipos, están obstaculizando la instalación y el funcionamiento de los laboratorios automatizados en el mercado.

- Alto costo de instalación y configuración

La instalación y configuración de sistemas automatizados de laboratorio son procedimientos mucho más complejos y que requieren mucho trabajo. La instalación de laboratorios automatizados requiere mucho tiempo, esfuerzo, planificación, implementación y aprobaciones de varios departamentos gubernamentales. Además, lo esencial para la instalación de un nuevo laboratorio requiere una inversión crítica en infraestructura debido al alto costo de las máquinas, herramientas y equipos avanzados.

- Actualización, mantenimiento y revisiones periódicas

La operación eficiente de los laboratorios es la principal preocupación después de la instalación. El mantenimiento, la actualización y las revisiones periódicas de los equipos son necesarios para la operación. El gasto que se requiere para esto es uno de los principales factores restrictivos para los actores del mercado. Los propietarios de los laboratorios están obligados por la regulación o el control de calidad a probar sus productos independientemente de las empresas fabricantes para operar sin problemas y evitar circunstancias que puedan frenar el crecimiento del mercado.

Impacto posterior a la COVID-19 en el mercado de automatización de laboratorios de Europa

El COVID-19 ha afectado positivamente al mercado de la automatización. Debido a la pandemia, la salud de las personas se ha visto afectada, por lo que se han realizado muchas pruebas de diagnóstico y ha aumentado la demanda. Los laboratorios privados, los hospitales y la investigación clínica aumentaron debido a la pandemia. Por lo tanto, el COVID-19 aumentó positivamente el mercado de la automatización de laboratorios.

Acontecimientos recientes

- En junio de 2022, BD anunció que había completado la adquisición de Straub Medical AG, una empresa privada. Con esta adquisición, la empresa ha incorporado la valiosa experiencia y conocimientos de Straub Medical AG y ha ampliado su cartera de productos.

- En enero de 2022, QIAGEN anunció que había iniciado nuevas colaboraciones con Atlia Biosystems para proporcionar soluciones de pruebas prenatales no invasivas.

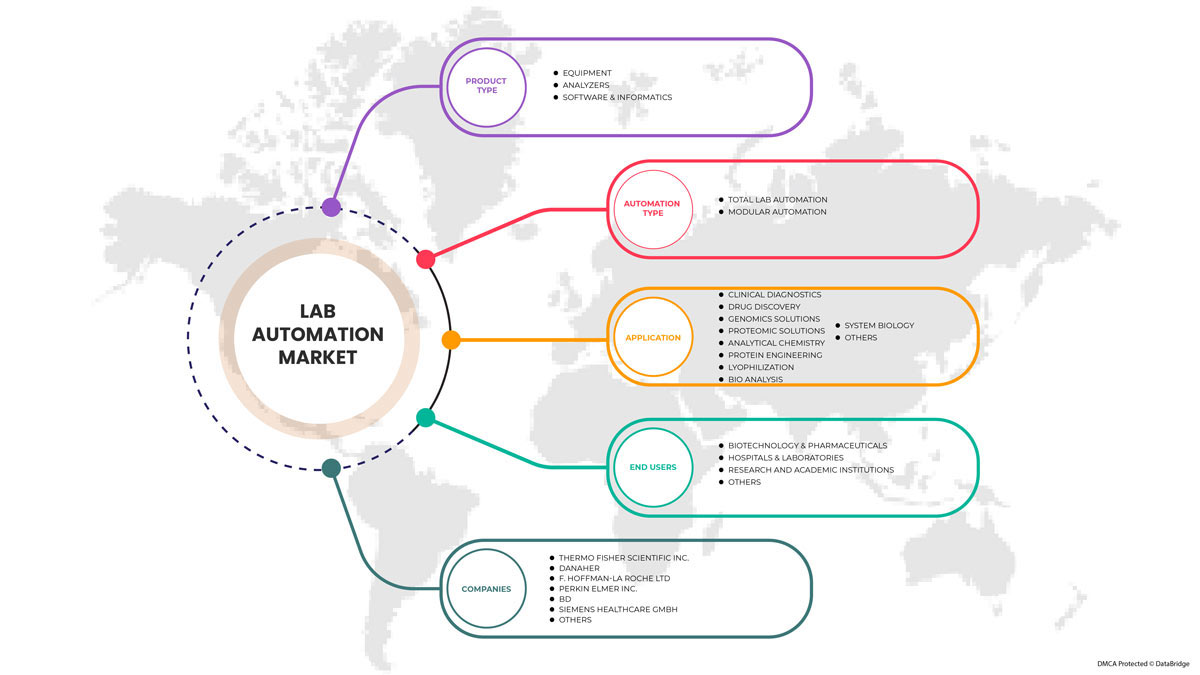

Alcance del mercado de automatización de laboratorios en Europa

El mercado europeo de automatización de laboratorios está segmentado por tipo de producto, sistemas automatizados, aplicación y usuario final. El crecimiento entre estos segmentos le ayudará a analizar segmentos de crecimiento reducido en las industrias y brindará a los usuarios una valiosa descripción general del mercado y conocimientos del mercado para tomar decisiones estratégicas para identificar las principales aplicaciones del mercado.

Tipo de producto

- Equipo

- Analizador

- Software e informática

Según el tipo de producto, el mercado de automatización de laboratorio se segmenta en equipos, analizadores y software e informática.

Sistemas automatizados

- Automatización total del laboratorio

- Automatización de laboratorio modular

Basado en sistemas automatizados, el mercado de automatización de laboratorio está segmentado en automatización total de laboratorio y automatización modular de laboratorio.

Solicitud

- Diagnóstico clínico

- Descubrimiento de fármacos

- Soluciones genómicas

- Soluciones proteómicas

- Química Analítica

- Ingeniería de proteínas

- Liofilización

- Análisis biológico

- Biología de sistemas

- Otros

Según la aplicación, el mercado de automatización de laboratorio está segmentado en descubrimiento de fármacos, diagnóstico clínico, soluciones genómicas, soluciones proteómicas, bioanálisis, ingeniería de proteínas, liofilización, biología de sistemas, química analítica y otros.

Usuario final

- Biotecnología y productos farmacéuticos

- Hospitales y laboratorios

- Institutos de investigación y académicos

- Otros

Según el usuario final, el mercado de automatización de laboratorio está segmentado en biotecnología y productos farmacéuticos, hospitales y laboratorios, instituciones de investigación y académicas y otros.

Análisis y perspectivas regionales del mercado de automatización de laboratorios en Europa

Se analiza el mercado de automatización de laboratorio de Europa y se proporcionan información y tendencias del tamaño del mercado por país, tipo de producto, sistemas automatizados, aplicación y usuario final.

Los países que abarca el mercado son Alemania, Francia, Reino Unido, Italia, España, Países Bajos, Rusia, Bélgica, Suiza, Turquía y el resto de Europa. Se espera que Alemania domine el mercado europeo de automatización de laboratorios debido al aumento de la demanda de equipos, analizadores y software en el mercado regional.

La sección de regiones del informe también proporciona factores de impacto individuales en el mercado y cambios en las regulaciones del mercado que afectan las tendencias actuales y futuras del mercado. Los puntos de datos, como las ventas de productos nuevos y de reemplazo, la demografía del país, la epidemiología de las enfermedades y los aranceles de importación y exportación, son algunos de los principales indicadores utilizados para pronosticar el escenario del mercado para cada país. Además, se consideran la presencia y disponibilidad de las marcas de América Central y los desafíos que enfrentan debido a la alta competencia de las marcas locales y nacionales, y el impacto de los canales de venta al proporcionar un análisis de pronóstico de los datos del país.

Análisis del panorama competitivo y de la cuota de mercado de la automatización de laboratorios

El panorama competitivo del mercado de automatización de laboratorios en Europa ofrece información detallada de los competidores. Los detalles incluidos son una descripción general de la empresa, las finanzas de la empresa, los ingresos generados, el potencial de mercado, la inversión en investigación y desarrollo, las nuevas iniciativas de mercado, la presencia en Europa, los sitios e instalaciones de producción, las capacidades de producción, las fortalezas y debilidades de la empresa, el lanzamiento de productos, la amplitud y la variedad de productos y el dominio de las aplicaciones. Los puntos de datos anteriores proporcionados solo están relacionados con el enfoque de las empresas en el mercado de automatización de laboratorios de Europa.

Algunos de los principales actores que operan en el mercado de automatización de laboratorios de Europa son QIAGEN, Siemens Healthcare, F. Hoffman Roche, Hamilton Company, Hudson Robotics, LabVantage Solutions Inc., Abbott, BD, BIOMERIEUX, Aurora Biomed Inc., Danaher, Tecan Trading AG, PerkinElmer Inc, Thermo Fisher Scientific, Agilent Technologies, Azenta US Inc, Eppendorf SE y Labware, entre otros.

Metodología de la investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con tamaños de muestra grandes. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Aparte de esto, los modelos de datos incluyen una cuadrícula de posicionamiento de proveedores, un análisis de la línea de tiempo del mercado, una descripción general y una guía del mercado, una cuadrícula de posicionamiento de la empresa, un análisis de la participación de mercado de la empresa, estándares de medición, Europa frente a la región y un análisis de la participación de los proveedores. Solicite una llamada de un analista en caso de tener más consultas.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Tabla de contenido

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE EUROPE LAB AUTOMATION MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRODUCT TYPE LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.2 PORTER’S FIVE FORCES

5 REGULATION

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 INCREASING INVESTMENT & STRATEGIC INITIATIVES BY MARKET PLAYERS

6.1.2 GOVERNMENT INITIATIVES TO STRENGTHEN LABORATORY INFRASTRUCTURES

6.1.3 GROWING EXPENDITURE ON LAB AUTOMATION TOOLS AND EQUIPMENT

6.1.4 REDUCING HUMAN EFFORTS AND ELIMINATING HUMAN ERROR

6.2 RESTRAINTS

6.2.1 LIMITATION ANALYZING NOVEL COMPLEX PRODUCT

6.2.2 HIGH COST FOR INSTALLATION AND SETUP

6.2.3 UPGRADATION, MAINTENANCE, AND PERIODICAL CHECKUPS

6.3 OPPORTUNITIES

6.3.1 RISING HEALTHCARE EXPENDITURE

6.3.2 STRATEGIC INITIATIVES BY KEY PLAYERS

6.3.3 RISE IN THE NUMBER OF PHARMA COMPANIES

6.4 CHALLENGES

6.4.1 SLOW ADOPTION OF AUTOMATION AMONG SMALL AND MEDIUM SIZED LABORATORIES

6.4.2 LIMITED FEASIBILITY WITH TECHNOLOGY INTEGRATION IN ANALYTICAL LABS

7 EUROPE LAB AUTOMATION MARKET, BY PRODUCT TYPE

7.1 OVERVIEW

7.2 EQUIPMENT

7.2.1 AUTOMATED WORKSTATIONS

7.2.1.1 AUTOMATED LIQUID HANDLING SYSTEMS

7.2.1.2 AUTOMATED INTEGRATED WORKSTATIONS

7.2.1.3 PIPETTING SYSTEMS

7.2.1.4 MICROPLATE WASHERS

7.2.1.5 REAGENT DISPENSERS

7.2.2 MICROPLATE READERS

7.2.2.1 MULTI-MODE MICROPLATE READERS

7.2.2.2 SINGLE-MODE MICROPLATE READERS

7.2.2.3 AUTOMATED NUCLEIC ACID PURIFICATION SYSTEMS

7.2.2.4 AUTOMATED ELISA SYSTEMS

7.2.3 OFF-THE-SHELF AUTOMATED WORKCELLS

7.2.4 ROBOTIC SYSTEMS

7.2.4.1 ROBOTIC ARMS

7.2.4.2 TRACK ROBOTS

7.2.5 AUTOMATE STORAGE & RETRIEVALS (ASRS)

7.2.6 OTHERS

7.3 ANALYZER

7.3.1 BIO CHEMISTRY ANALYZERS

7.3.2 HAEMATOLOGY ANALYZERS

7.3.3 IMMUNO-BASED ANALYZERS

7.4 SOFTWARE & INFORMATICS

7.4.1 LABORATORY INFORMATION MANAGEMENT SYSTEM (LIMS)

7.4.2 ELECTRONIC LABORATORY NOTEBOOK (ELN)

7.4.3 LABORATORY EXECUTION SYSTEMS (LES)

7.4.4 SCIENTIFIC DATA MANAGEMENT SYSTEMS (SDMS)

8 EUROPE LAB AUTOMATION MARKET, BY AUTOMATION TYPE

8.1 OVERVIEW

8.2 TOTAL LAB AUTOMATION

8.3 MODULAR AUTOMATION

9 EUROPE LAB AUTOMATION MARKET, BY APPLICATION

9.1 OVERVIEW

9.2 CLINICAL DIAGNOSTICS

9.3 DRUG DISCOVERY

9.4 GENOMICS SOLUTIONS

9.5 PROTEOMIC SOLUTIONS

9.6 ANALYTICAL CHEMISTRY

9.7 PROTEIN ENGINEERING

9.8 BIO ANALYSIS

9.9 SYSTEM BIOLOGY

9.1 OTHERS

10 EUROPE LAB AUTOMATION MARKET, BY END USER

10.1 OVERVIEW

10.2 BIOTECHNOLOGY & PHARMACEUTICALS

10.3 HOSPITALS & LABORATORIES

10.4 RESEARCH & ACADEMIC INSTITUTES

10.5 OTHERS

11 EUROPE LAB AUTOMATION MARKET, BY REGION

11.1 EUROPE

11.1.1 GERMANY

11.1.2 FRANCE

11.1.3 U.K.

11.1.4 ITALY

11.1.5 RUSSIA

11.1.6 SPAIN

11.1.7 NETHERLANDS

11.1.8 SWITZERLAND

11.1.9 TURKEY

11.1.10 BELGIUM

11.1.11 REST OF EUROPE

12 EUROPE LAB AUTOMATION MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: EUROPE

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 THERMO FISHER SCIENTIFIC INC.

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENTS

14.2 DANAHER

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENTS

14.3 F. HOFFMANN- LA ROCHE LTD

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENTS

14.4 PERKINELMER INC

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENTS

14.5 BD

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT PORTFOLIO

14.5.5 RECENT DEVELOPMENTS

14.6 ABBOTT

14.6.1 COMPANY SNAPSHOT

14.6.2 REVENUE ANALYSIS

14.6.3 PRODUCT PORTFOLIO

14.6.3 RECENT DEVELOPMENTS

14.7 AGILENT TECHNOLOGIES

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCT PORTFOLIO

14.7.4 RECENT DEVELOPMENTS

14.8 AURORA BIOMED INC.

14.8.1 COMPANY SNAPSHOT

14.8.2 PRODUCT PORTFOLIO

14.8.3 RECENT DEVELOPMENTS

14.9 AZENTA US INC

14.9.1 COMPANY SNAPSHOT

14.9.2 REVENUE ANALYSIS

14.9.3 PRODUCT PORTFOLIO

14.9.4 RECENT DEVELOPMENTS

14.1 BIOMERIEUX

14.10.1 COMPANY SNAPSHOT

14.10.2 REVENUE ANALYSIS

14.10.3 PRODUCT PORTFOLIO

14.10.4 RECENT DEVELOPMENTS

14.11 EPPENDORF SE

14.11.1 COMPANY SNAPSHOT

14.11.2 PRODUCT PORTFOLIO

14.11.3 RECENT DEVELOPMENTS

14.12 HAMILTON COMPANY

14.12.1 COMPANY SNAPSHOT

14.12.2 PRODUCT PORTFOLIO

14.12.3 RECENT DEVELOPMENTS

14.13 HUDSON ROBOTICS

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCT PORTFOLIO

14.13.3 RECENT DEVELOPMENTS

14.14 LABLYNX LIMS

14.14.1 COMPANY SNAPSHOT

14.14.2 PRODUCT PORTFOLIO

14.14.3 RECENT DEVELOPMENTS

14.15 LABVANTAGE SOLUTIONS INC.

14.15.1 COMPANY SNAPSHOT

14.15.2 PRODUCT PORTFOLIO

14.15.3 RECENT DEVELOPMENTS

14.16 LABWARE

14.16.1 COMPANY SNAPSHOT

14.16.2 PRODUCT PORTFOLIO

14.16.3 RECENT DEVELOPMENTS

14.17 QIAGEN

14.17.1 COMPANY SNAPSHOT

14.17.2 REVENUE ANALYSIS

14.17.3 PRODUCT PORTFOLIO

14.17.4 RECENT DEVELOPMENTS

14.18 SIEMENS HEALTHCARE GMBH

14.18.1 COMPANY SNAPSHOT

14.18.2 REVENUE ANALYSIS

14.18.3 PRODUCT PORTFOLIO

14.18.4 RECENT DEVELOPMENTS

14.19 TECAN TRADING AG

14.19.1 COMPANY SNAPSHOT

14.19.2 REVENUE ANALYSIS

14.19.3 PRODUCT PORTFOLIO

14.19.4 RECENT DEVELOPMENTS

15 QUESTIONNAIRE

16 RELATED REPORTS

Lista de Tablas

TABLE 1 EUROPE LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 2 EUROPE EQUIPMENT IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 3 EUROPE AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 4 EUROPE MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 5 EUROPE ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 6 EUROPE ANALYZER IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 7 EUROPE ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 8 EUROPE SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 9 EUROPE SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 10 EUROPE LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 11 EUROPE TOTAL LAB AUTOMATION IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 12 EUROPE MODULAR AUTOMATION IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 13 EUROPE LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 14 EUROPE CLINICAL DIAGNOSTICS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 15 EUROPE DRUG DISCOVERY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 16 EUROPE GENOMICS SOLUTIONS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 17 EUROPE PROTEOMIC SOLUTIONS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 18 EUROPE ANALYTICAL CHEMISTRY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 19 EUROPE PROTEIN ENGINEERING IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 20 EUROPE BIO ANALYSIS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 21 EUROPE SYSTEM BIOLOGY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 22 EUROPE OTHERS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 23 EUROPE LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 24 EUROPE BIOTECHNOLOGY & PHARMACEUTICALS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 25 EUROPE HOSPITALS & LABORATORIES IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 26 EUROPE RESEARCH & ACADEMIC INSTITUTES IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 27 EUROPE OTHERS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 28 EUROPE LAB AUTOMATION MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 29 EUROPE LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 30 EUROPE EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 31 EUROPE AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 32 EUROPE MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 33 EUROPE ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 34 EUROPE ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 35 EUROPE SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 36 EUROPE LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 37 EUROPE LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 38 EUROPE LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 39 GERMANY LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 40 GERMANY EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 41 GERMANY AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 42 GERMANY MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 43 GERMANY ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 44 GERMANY ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 45 GERMANY SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 46 GERMANY LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 47 GERMANY LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 48 GERMANY LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 49 FRANCE LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 50 FRANCE EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 51 FRANCE AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 52 FRANCE MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 53 FRANCE ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 54 FRANCE ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 55 FRANCE SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 56 FRANCE LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 57 FRANCE LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 58 FRANCE LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 59 U.K. LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 60 U.K. EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 61 U.K. AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 62 U.K. MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 63 U.K. ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 64 U.K. ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 65 U.K. SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 66 U.K. LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 67 U.K. LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 68 U.K. LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 69 ITALY LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 70 ITALY EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 71 ITALY AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 72 ITALY MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 73 ITALY ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 74 ITALY ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 75 ITALY SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 76 ITALY LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 77 ITALY LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 78 ITALY LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 79 RUSSIA LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 80 RUSSIA EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 81 RUSSIA AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 82 RUSSIA MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 83 RUSSIA ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 84 RUSSIA ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 85 RUSSIA SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 86 RUSSIA LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 87 RUSSIA LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 88 RUSSIA LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 89 SPAIN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 90 SPAIN EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 91 SPAIN AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 92 SPAIN MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 93 SPAIN ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 94 SPAIN ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 95 SPAIN SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 96 SPAIN LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 97 SPAIN LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 98 SPAIN LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 99 NETHERLANDS LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 100 NETHERLANDS EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 101 NETHERLANDS AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 102 NETHERLANDS MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 103 NETHERLANDS ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 104 NETHERLANDS ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 105 NETHERLANDS SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 106 NETHERLANDS LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 107 NETHERLANDS LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 108 NETHERLANDS LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 109 SWITZERLAND LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 110 SWITZERLAND EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 111 SWITZERLAND AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 112 SWITZERLAND MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 113 SWITZERLAND ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 114 SWITZERLAND ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 115 SWITZERLAND SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 116 SWITZERLAND LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 117 SWITZERLAND LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 118 SWITZERLAND LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 119 TURKEY LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 120 TURKEY EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 121 TURKEY AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 122 TURKEY MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 123 TURKEY ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 124 TURKEY ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 125 TURKEY SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 126 TURKEY LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 127 TURKEY LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 128 TURKEY LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 129 BELGIUM LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 130 BELGIUM EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 131 BELGIUM AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 132 BELGIUM MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 133 BELGIUM ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 134 BELGIUM ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 135 BELGIUM SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 136 BELGIUM LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 137 BELGIUM LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 138 BELGIUM LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 139 REST OF EUROPE LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

Lista de figuras

FIGURE 1 EUROPE LAB AUTOMATION MARKET: SEGMENTATION

FIGURE 2 EUROPE LAB AUTOMATION MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE LAB AUTOMATION MARKET: DROC ANALYSIS

FIGURE 4 EUROPE LAB AUTOMATION MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE LAB AUTOMATION MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE LAB AUTOMATION MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE LAB AUTOMATION MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE LAB AUTOMATION MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 EUROPE LAB AUTOMATION MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 EUROPE LAB AUTOMATION MARKET: SEGMENTATION

FIGURE 11 GROWING EXPENDITURE ON LAB AUTOMATION TOOLS AND EQUIPMENT IS EXPECTED TO DRIVE THE EUROPE LAB AUTOMATION MARKET GROWTH IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 12 EQUIPMENT SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE LAB AUTOMATION MARKET IN 2022 & 2029

FIGURE 13 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE EUROPE LAB AUTOMATION MARKET

FIGURE 14 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE, 2021

FIGURE 15 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE, 2022-2029 (USD MILLION)

FIGURE 16 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE, CAGR (2022-2029)

FIGURE 17 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE, LIFELINE CURVE

FIGURE 18 EUROPE LAB AUTOMATION MARKET: BY AUTOMATION TYPE, 2021

FIGURE 19 EUROPE LAB AUTOMATION MARKET: BY AUTOMATION TYPE, 2022-2029 (USD MILLION)

FIGURE 20 EUROPE LAB AUTOMATION MARKET: BY AUTOMATION TYPE, CAGR (2022-2029)

FIGURE 21 EUROPE LAB AUTOMATION MARKET: BY AUTOMATION TYPE, LIFELINE CURVE

FIGURE 22 EUROPE LAB AUTOMATION MARKET: BY APPLICATION, 2021

FIGURE 23 EUROPE LAB AUTOMATION MARKET: BY APPLICATION, 2022-2029 (USD MILLION)

FIGURE 24 EUROPE LAB AUTOMATION MARKET: BY APPLICATION, CAGR (2022-2029)

FIGURE 25 EUROPE LAB AUTOMATION MARKET: BY APPLICATION, LIFELINE CURVE

FIGURE 26 EUROPE LAB AUTOMATION MARKET: BY END USER, 2021

FIGURE 27 EUROPE LAB AUTOMATION MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 28 EUROPE LAB AUTOMATION MARKET: BY END USER, CAGR (2022-2029)

FIGURE 29 EUROPE LAB AUTOMATION MARKET: BY END USER, LIFELINE CURVE

FIGURE 30 EUROPE LAB AUTOMATION MARKET: SNAPSHOT (2021)

FIGURE 31 EUROPE LAB AUTOMATION MARKET: BY COUNTRY (2021)

FIGURE 32 EUROPE LAB AUTOMATION MARKET: BY COUNTRY (2022 & 2029)

FIGURE 33 EUROPE LAB AUTOMATION MARKET: BY COUNTRY (2021 & 2029)

FIGURE 34 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE (2022-2029)

FIGURE 35 EUROPE LAB AUTOMATION MARKET: COMPANY SHARE 2021 (%)

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.