Europe 3d Printing Materials Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

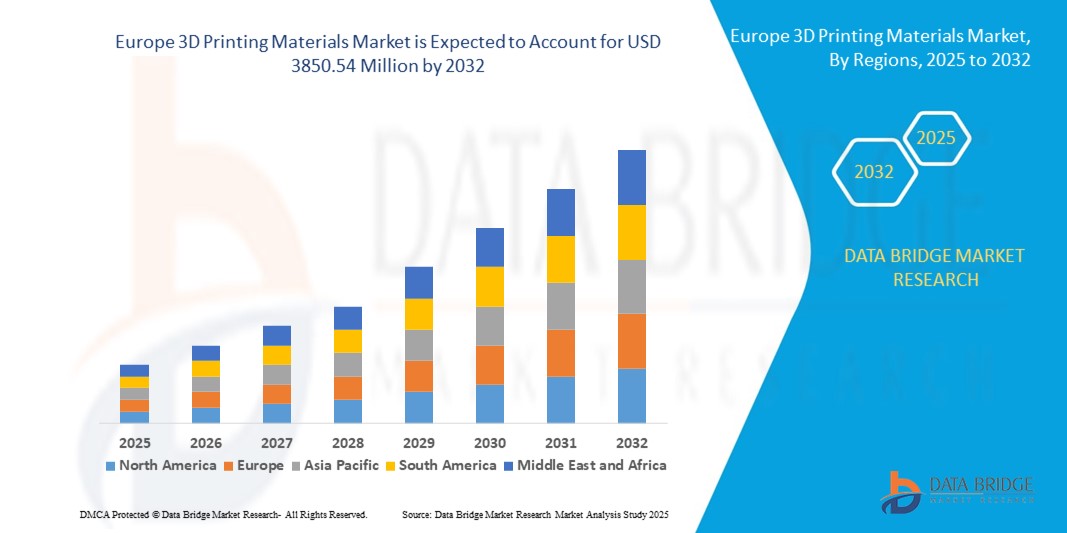

901.50 Million

USD

3,850.54 Million

2024

2032

USD

901.50 Million

USD

3,850.54 Million

2024

2032

| 2025 –2032 | |

| USD 901.50 Million | |

| USD 3,850.54 Million | |

| % | |

|

Segmentación del mercado europeo de materiales de impresión 3D por tipo (plásticos/polímeros, metal, cerámica , etc.), forma (polvo, filamento y líquido), tecnología (modelado por deposición fundida [FDM], sinterización selectiva por láser [SLS], estereolitografía [SLA], sinterización directa por láser de metal [DMLS], fabricación aditiva de área grande [BAAM], fabricación aditiva por arco de alambre [WAAM], ColorJet, etc.), uso final (fabricación industrial, automoción, aeroespacial y defensa, salud, bienes de consumo, electrónica, educación, construcción, etc.): tendencias y pronóstico del sector hasta 2032.

¿Cuál es el tamaño y la tasa de crecimiento del mercado de materiales de impresión 3D en Europa?

- El tamaño del mercado de materiales de impresión 3D de Europa se valoró en USD 901,50 millones en 2024 y se espera que alcance los USD 3850,54 millones para 2032 , con una CAGR del 19,90 % durante el período de pronóstico.

- La creciente adopción de la impresión 3D en diversas industrias, el aumento de la creación de prototipos y herramientas rápidas, y la creciente accesibilidad y asequibilidad de las tecnologías de impresión 3D a nivel universal son algunos de los factores impulsores que se espera que impulsen el crecimiento del mercado.

¿Cuáles son las principales conclusiones del mercado europeo de materiales de impresión 3D?

- Existe un aumento correspondiente en la demanda de materiales que puedan satisfacer los diversos requisitos de este innovador proceso de fabricación a medida que las industrias adoptan las revolucionarias capacidades de la impresión 3D. La versatilidad de la impresión 3D, también conocida como fabricación aditiva, abarca industrias como la aeroespacial, la sanitaria, la automoción y los bienes de consumo, donde la tecnología se emplea para la creación rápida de prototipos, la producción personalizada y la fabricación de diseños complejos.

- El factor que contribuye a la demanda de materiales de impresión 3D es la capacidad de esta tecnología para producir componentes complejos y altamente personalizados. Los métodos de fabricación tradicionales no son tan eficientes ni rápidos, ya que las industrias buscan piezas más complejas y con diseños más precisos. La impresión 3D soluciona esta deficiencia al permitir la creación de estructuras geométricamente complejas con mayor eficiencia.

- La demanda de materiales especializados aumenta con la evolución de las necesidades de sectores industriales como el aeroespacial, la salud, la automoción y los bienes de consumo, que implementan esta tecnología transformadora, a medida que la impresión 3D continúa revolucionando los procesos de fabricación. Por lo tanto, la creciente adopción de la impresión 3D en diversas industrias está impulsando el crecimiento del mercado.

- El mercado alemán de materiales de impresión 3D representó la mayor participación en Europa en 2024, con un 28,11 % de los ingresos regionales. Este crecimiento se ve impulsado por la demanda de sistemas de seguridad de alta tecnología, hogares inteligentes energéticamente eficientes y mejoras en la infraestructura digital.

- Se espera que el mercado de materiales de impresión 3D del Reino Unido crezca a una CAGR sólida del 12,23 % durante el período de pronóstico, impulsado por las crecientes preocupaciones sobre la seguridad residencial y comercial, la popularidad de las configuraciones de hogares inteligentes de bricolaje y una fuerte penetración minorista y en línea.

- El segmento de plásticos/polímeros dominó el mercado con la mayor participación en los ingresos del 45,8 % en 2024, debido a su versatilidad, asequibilidad y adopción generalizada en prototipos y aplicaciones industriales.

Alcance del informe y segmentación del mercado de materiales de impresión 3D en Europa

|

Atributos |

Perspectivas clave del mercado de materiales de impresión 3D en Europa |

|

Segmentos cubiertos |

|

|

Países cubiertos |

Europa

|

|

Actores clave del mercado |

|

|

Oportunidades de mercado |

|

|

Conjuntos de información de datos de valor añadido |

Además de los conocimientos sobre escenarios de mercado como valor de mercado, tasa de crecimiento, segmentación, cobertura geográfica y actores principales, los informes de mercado seleccionados por Data Bridge Market Research también incluyen análisis de expertos en profundidad, análisis de precios, análisis de participación de marca, encuesta de consumidores, análisis demográfico, análisis de la cadena de suministro, análisis de la cadena de valor, descripción general de materias primas/consumibles, criterios de selección de proveedores, análisis PESTLE, análisis de Porter y marco regulatorio. |

¿Cuál es la tendencia clave en el mercado de materiales de impresión 3D en Europa?

Cambio hacia materiales funcionales y de alto rendimiento

- Una tendencia definitoria en el mercado de materiales de impresión 3D es el creciente desarrollo y adopción de materiales funcionales y de alto rendimiento, incluidos compuestos, aleaciones metálicas y polímeros de base biológica, que amplían la gama de aplicaciones industriales, médicas y de consumo.

- Por ejemplo, empresas como Markforged y EOS están introduciendo filamentos reforzados con fibra de carbono y polvos de polímeros de alta temperatura que permiten la producción de piezas ligeras pero duraderas para maquinaria aeroespacial, automotriz e industrial.

- Los materiales de impresión 3D funcionales permiten cada vez más la impresión de múltiples materiales, la integración de componentes electrónicos o la incorporación de vías conductoras, transformando así los flujos de trabajo de fabricación convencionales en procesos aditivos integrados.

- La tendencia también incluye biotintas y polímeros biocompatibles para la impresión 3D médica, incluidos andamios de tejidos, implantes y prótesis personalizadas, que brindan mayor precisión, diseños específicos para el paciente y ciclos de producción más rápidos.

- A medida que las industrias avanzan hacia la fabricación digital y la producción bajo demanda, empresas como Formlabs y 3D Systems están desarrollando resinas y polvos especializados para prototipos avanzados, herramientas y aplicaciones de uso final, impulsando la innovación en todos los sectores.

- La creciente adopción de materiales de impresión 3D funcionales, duraderos y listos para la industria está cambiando las expectativas de los usuarios y expandiendo las aplicaciones en los sectores automotriz, de atención médica, aeroespacial y de electrónica de consumo.

¿Cuáles son los impulsores clave del mercado europeo de materiales de impresión 3D?

- La creciente demanda de piezas ligeras, de alta resistencia y personalizadas en industrias como la aeroespacial, la automotriz y la atención médica es un impulsor importante del mercado de materiales de impresión 3D.

- Por ejemplo, en marzo de 2024, Stratasys lanzó termoplásticos ignífugos de alta temperatura diseñados para herramientas aeroespaciales e industriales, mejorando la durabilidad y el cumplimiento normativo.

- La creciente adopción de la fabricación aditiva en la creación de prototipos, la producción de lotes pequeños y las geometrías complejas está impulsando la innovación de materiales, lo que permite una personalización precisa al tiempo que reduce el desperdicio y los plazos de entrega.

- Además, las iniciativas de sostenibilidad están impulsando el uso de filamentos de origen biológico y polímeros reciclables, alineándose con los objetivos ESG y reduciendo el impacto ambiental.

- La integración de materiales de impresión 3D con impresoras 3D automatizadas y a escala industrial, incluidos sistemas de múltiples materiales y de fibra continua, está impulsando la eficiencia, la rentabilidad y una adopción más amplia en múltiples industrias de uso final.

¿Qué factor está frenando el crecimiento del mercado europeo de materiales de impresión 3D?

- El alto costo y la disponibilidad limitada de materiales avanzados de impresión 3D, en particular compuestos funcionales, polvos metálicos y resinas biocompatibles, son barreras importantes para su adopción generalizada.

- Por ejemplo, los polvos metálicos de primera calidad para aplicaciones aeroespaciales y médicas a menudo tienen costos de adquisición elevados y requieren almacenamiento y manipulación especializados, lo que limita su uso a aplicaciones de alto valor.

- La consistencia del rendimiento del material, el control de calidad y la estandarización siguen siendo desafíos, especialmente para piezas de grado industrial que requieren un estricto cumplimiento normativo e integridad mecánica.

- Además, la falta de profesionales capacitados y experiencia técnica en el manejo de materiales de impresión 3D especializados restringe su adopción en mercados emergentes y empresas más pequeñas.

- Superar estos desafíos mediante la reducción de costos, la innovación de materiales y programas de capacitación será fundamental para permitir una adopción más amplia y un crecimiento sostenido del mercado a nivel mundial.

¿Cómo está segmentado el mercado de materiales de impresión 3D en Europa?

El mercado está segmentado según el tipo, la forma, la tecnología y el uso final.

- Por tipo

Según el tipo, el mercado de materiales de impresión 3D se segmenta en plásticos/polímeros, metal, cerámica y otros. El segmento de plásticos/polímeros dominó el mercado con la mayor participación en los ingresos, con un 45,8 % en 2024, gracias a su versatilidad, asequibilidad y amplia adopción en prototipos y aplicaciones industriales. Los plásticos/polímeros son los preferidos para piezas ligeras, prototipos funcionales y productos de consumo debido a su fácil procesamiento, buenas propiedades mecánicas y compatibilidad con diversas tecnologías de impresión 3D.

Se proyecta que el segmento de metales crecerá a la tasa de crecimiento anual compuesta (TCAC) más rápida entre 2025 y 2032, impulsado por la demanda de componentes de alta resistencia, resistentes al calor y duraderos en las industrias aeroespacial, automotriz y médica. Los polvos y aleaciones metálicas permiten la producción de estructuras complejas y resistentes que la fabricación tradicional no puede lograr fácilmente. Por otro lado, los materiales cerámicos están ganando terreno para aplicaciones de alta temperatura y biocompatibles en la atención médica y la electrónica, aunque su adopción sigue limitada por los mayores costos y los requisitos de equipos especializados.

- Por formulario

Según su forma, el mercado de materiales de impresión 3D se segmenta en polvo, filamento y líquido. El segmento de filamentos obtuvo la mayor cuota de mercado, con un 52,3%, en 2024, gracias a su amplio uso en impresoras de modelado por deposición fundida (FDM), su fácil manejo y su asequibilidad para aplicaciones industriales y de consumo. Los filamentos están disponibles en termoplásticos, compuestos y polímeros de origen biológico, lo que ofrece versatilidad para la creación de prototipos, el mecanizado y la fabricación de piezas funcionales para uso final.

Se prevé que el polvo presente la tasa de crecimiento anual compuesta (TCAC) más rápida entre 2025 y 2032, en gran medida debido a su papel crucial en la sinterización selectiva por láser (SLS), la sinterización directa por láser de metal (DMLS) y otros procesos de fabricación aditiva de metales y polímeros de alta precisión. Los materiales líquidos de impresión 3D, utilizados principalmente en estereolitografía (SLA) e impresoras basadas en resina, son los preferidos para piezas de alta resolución y geometrías complejas, pero están limitados por el coste y los requisitos de posprocesamiento.

- Por tecnología

En cuanto a la tecnología, el mercado de materiales de impresión 3D se segmenta en modelado por deposición fundida (FDM), sinterización selectiva por láser (SLS), estereolitografía (SLA), sinterización directa por láser de metal (DMLS), fabricación aditiva de área grande (BAAM), fabricación aditiva por arco de alambre (WAAM), ColorJet y otros. El segmento FDM dominó el mercado con la mayor participación en los ingresos, con un 40,9 %, en 2024, gracias a su accesibilidad, asequibilidad y capacidad para procesar una amplia variedad de termoplásticos y compuestos. El FDM se utiliza ampliamente para la creación de prototipos, pruebas funcionales y fines educativos, lo que lo ha popularizado en múltiples industrias.

Se prevé que SLS y DMLS experimenten el mayor crecimiento entre 2025 y 2032, gracias a su capacidad para producir piezas complejas y de alta resistencia para aplicaciones aeroespaciales, automotrices y médicas. SLA, BAAM, WAAM y ColorJet se adaptan a aplicaciones específicas que requieren alta precisión, velocidad o producción a gran escala, ampliando aún más el alcance tecnológico del mercado.

- Por uso final

Según el uso final, el mercado de materiales de impresión 3D se segmenta en Fabricación Industrial, Automotriz, Aeroespacial y Defensa, Salud, Bienes de Consumo, Electrónica, Educación, Construcción y otros. El segmento de Fabricación Industrial obtuvo la mayor cuota de mercado en ingresos, con un 38,6%, en 2024, impulsado por la rápida adopción de la fabricación aditiva para la creación de prototipos, herramientas, plantillas y piezas de producción. Las industrias aprovechan los materiales de impresión 3D para reducir los plazos de entrega, optimizar los diseños y mejorar la eficiencia.

Se proyecta que los segmentos de Salud y Aeroespacial y Defensa crecerán a la tasa de crecimiento anual compuesta (TCAC) más alta entre 2025 y 2032, impulsados por la creciente demanda de implantes personalizados, prótesis, componentes estructurales ligeros y piezas esenciales. Las aplicaciones educativas y de consumo están impulsando el conocimiento y la adopción de la impresión 3D, mientras que los segmentos de electrónica y construcción están integrando gradualmente la impresión 3D para componentes especializados, estructuras a gran escala y productos personalizados.

¿Qué región posee la mayor participación en el mercado europeo de materiales de impresión 3D?

- El mercado alemán de materiales de impresión 3D representó la mayor participación en Europa en 2024, con un 28,11 % de los ingresos regionales. Este crecimiento se ve impulsado por la demanda de sistemas de seguridad de alta tecnología, hogares inteligentes energéticamente eficientes y mejoras en la infraestructura digital.

- Los consumidores prefieren productos compatibles con plataformas populares de hogares inteligentes como Alexa y Google Assistant, mientras que el énfasis del país en la sostenibilidad y la innovación acelera aún más la adopción en el mercado.

Análisis del mercado de materiales de impresión 3D en Francia

El mercado francés de materiales de impresión 3D está en constante expansión, impulsado por la urbanización, la adopción de hogares inteligentes y la concienciación de los consumidores sobre las soluciones de seguridad digital. Los incentivos gubernamentales para la modernización de edificios energéticamente eficientes y la creciente presencia de integradores de hogares inteligentes fomentan la adopción tanto en viviendas como en comercios.

Análisis del mercado italiano de materiales de impresión 3D

Se prevé un crecimiento significativo del mercado italiano de materiales de impresión 3D, impulsado por el creciente uso de dispositivos domésticos conectados, el creciente interés de los consumidores por la domótica y la modernización de edificios residenciales antiguos. La integración con plataformas de control por voz y aplicaciones para smartphones aumenta el atractivo del mercado.

¿Qué país tiene el mercado de materiales de impresión 3D de más rápido crecimiento en Europa?

Se espera que el mercado británico de materiales de impresión 3D crezca a una sólida tasa de crecimiento anual compuesta (TCAC) del 12,23 % durante el período de pronóstico, impulsado por la creciente preocupación por la seguridad residencial y comercial, la popularidad de las casas inteligentes caseras y la sólida penetración del comercio minorista y online. La adopción de sistemas de acceso sin llave y conectados en oficinas, apartamentos y viviendas multifamiliares está impulsando aún más la demanda.

Análisis del mercado de materiales de impresión 3D en Polonia

El mercado polaco está cobrando impulso gracias a la expansión urbana, la creciente adopción de hogares inteligentes y el creciente interés en sistemas de acceso seguros y energéticamente eficientes. Los consumidores polacos integran cada vez más materiales de impresión 3D con dispositivos compatibles con IoT para mayor comodidad y seguridad.

¿Cuáles son las principales empresas del mercado europeo de materiales de impresión 3D?

La industria europea de materiales de impresión 3D está liderada principalmente por empresas bien establecidas, entre las que se incluyen:

- Formlabs (EE. UU.)

- EOS (Alemania)

- ENVISIONTEC US LLC (EE. UU.)

- Elementos americanos (EE. UU.)

- Höganäs AB (Suecia)

- UltiMaker (Países Bajos)

- Carbon, Inc. (EE. UU.)

- KRAIBURG TPE GmbH & Co. KG (Alemania)

- Covestro AG (Alemania)

- Markforged, Inc. (EE. UU.)

- Stratasys (EE. UU.)

- ExOne (EE. UU.)

- Arkema (Francia)

- 3D Systems, Inc. (EE. UU.)

- Evonik Industries AG (Alemania)

- Materialise (Bélgica)

- BASF SE (Alemania)

- Sandvik AB (Suecia)

- Solvay (Bélgica)

¿Cuáles son los desarrollos recientes en el mercado europeo de materiales de impresión 3D?

- En octubre de 2023, EOS lanzó su red de Arquitectos de Espuma Digital, diseñada para acelerar el desarrollo y la fabricación aditiva (FA) de productos de consumo, médicos e industriales con aplicaciones de Espuma Digital. Espuma Digital no es un producto, sino un enfoque para la impresión 3D de productos similares a la espuma. Esto marcará una nueva dirección para la empresa en el sector de los materiales de impresión 3D.

- En octubre de 2023, Arkema anunció nuevas alianzas con líderes del sector como EOS, HP y Stratasys para diseñar la próxima generación de materiales y soluciones de impresión 3D. Esto impulsará sus capacidades de innovación y ampliará su cartera de productos.

- En febrero de 2023, Bauer Hockey, líder europeo en innovación de equipamiento de hockey, y EOS, empresa pionera y líder del mercado en la impresión 3D industrial, colaboraron para incorporar la fabricación aditiva (FA o impresión 3D) al programa de equipos personalizados MyBauer de Bauer. EOS y su enfoque patentado de espuma digital para la impresión de polímeros proporcionaron a Bauer una ventaja distintiva. Esto fortalecerá la presencia de EOS en el mercado europeo de materiales de impresión 3D.

- En noviembre de 2021, Covestro AG presentó cuatro nuevos materiales de impresión 3D en Formnext 2021, que abarcan diversas tecnologías. Entre ellos se encuentra Addigy FPC SOL1 HT, un material de soporte soluble para la impresión FDM de materiales de alta temperatura, que ofrece fácil remoción y sostenibilidad. Arnitel AM3001 (P) para SLS, un material blando con alto retorno energético, logró una impresión 3D exitosa cumpliendo con las normas de seguridad de los juguetes. Covestro también lanzó las versiones SLS y HSS de su polvo de TPU, Addigy PPU 86AW6, conocido por su rebote, fácil posprocesamiento y alta tasa de reutilización. Estas incorporaciones amplían la gama de polímeros de Covestro para la impresión 3D, tras la adquisición del negocio de fabricación aditiva de DSM a principios de este año.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.