La creciente prevalencia de la hepatitis, en particular la hepatitis B, está influyendo significativamente en el mercado mundial de la infección por el virus de la hepatitis delta (VHD). La hepatitis D es una infección hepática causada por el virus de la hepatitis D (VHD), que requiere la presencia del virus de la hepatitis B (VHB) para replicarse. A medida que aumentan las infecciones por hepatitis B a nivel mundial, también aumenta el número de personas susceptibles a la infección por VHD. Este creciente número de personas infectadas por el VHB crea una población objetivo más amplia para el VHD, lo que impulsa la demanda de soluciones diagnósticas y terapéuticas específicas para el VHD.

Según un artículo publicado por la Organización Mundial de la Salud (OMS), en abril de 2024, se estimó que 1,3 millones de personas fallecieron por hepatitis virales crónicas B y C en 2022, lo que representa casi 3500 muertes diarias. Además, se estima que 254 millones de personas viven con hepatitis B y 50 millones con hepatitis C en todo el mundo.

La creciente incidencia de la hepatitis B ha aumentado la conciencia sobre los riesgos de coinfección, lo que ha impulsado mayores esfuerzos de investigación y desarrollo centrados en el VHD. Esta mayor concienciación se traduce en una mayor inversión en el diagnóstico del VHD, incluyendo métodos de prueba más precisos y eficientes, y en el desarrollo de agentes terapéuticos específicos para el VHD. Las compañías farmacéuticas y las instituciones de investigación están respondiendo a la creciente necesidad de tratamientos eficaces contra el VHD, contribuyendo al crecimiento del mercado mediante la introducción de terapias innovadoras y la ampliación de sus carteras.

Cada año, el 28 de julio, la OMS colabora con otras organizaciones para fomentar la concienciación y la comprensión sobre la hepatitis viral y las enfermedades que causa en el Día Mundial contra la Hepatitis. Esta fecha conmemora el natalicio del profesor Baruch Samuel Blumberg, Premio Nobel y descubridor del virus de la hepatitis B. Brindó la oportunidad de intensificar los esfuerzos nacionales e internacionales contra la hepatitis, fomentar la acción y la participación de las personas, los asociados y el público en general, y destacar la necesidad de una respuesta mundial más amplia.

Además, el aumento de las infecciones por VHD debido a la mayor prevalencia de la hepatitis B ha generado un aumento del gasto sanitario relacionado con el manejo de las coinfecciones. Los sistemas de salud de todo el mundo se enfrentan a mayores desafíos financieros y logísticos, lo que genera un mercado en expansión para tratamientos e intervenciones específicos contra el VHD. Los gobiernos y las organizaciones sanitarias están invirtiendo más en programas de prevención, detección y tratamiento para abordar la carga del VHD y sus complicaciones, lo que impulsa aún más el crecimiento del mercado.

Además del impacto directo en los sistemas de salud, la creciente prevalencia de la hepatitis B y las consiguientes infecciones por VHD ha impulsado colaboraciones e iniciativas globales para combatir la enfermedad. Organizaciones internacionales de salud y grupos de apoyo trabajan para mejorar la vigilancia, promover la vacunación contra la hepatitis B y ampliar el acceso al tratamiento. Estos esfuerzos globales no solo generan concienciación, sino que también impulsan la demanda de soluciones médicas específicas para el VHD, acelerando así el crecimiento del mercado de la infección por VHD.

Acceda al informe completo en https://www.databridgemarketresearch.com/reports/global-hepatitis-delta-virus-hdv-infection-market

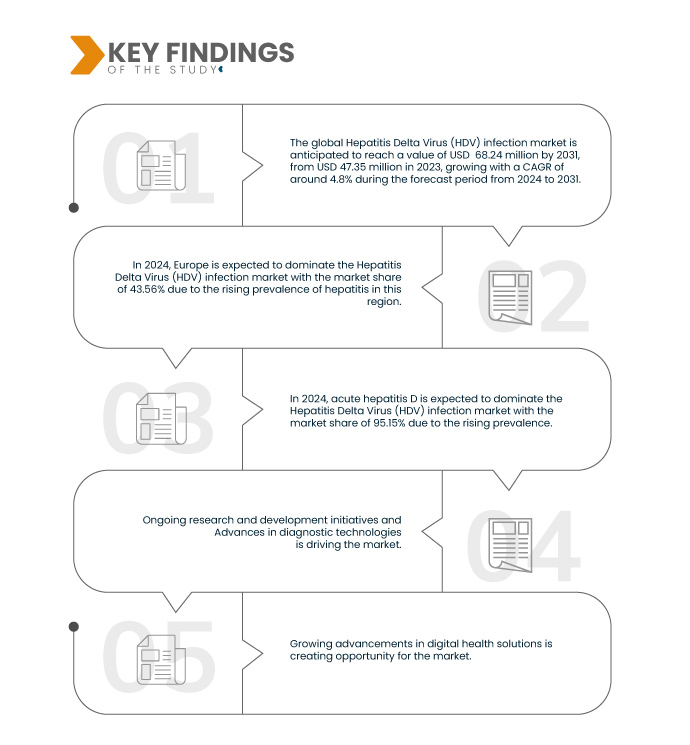

Data Bridge Market Research analiza que se espera que el mercado mundial de infección por el virus delta de la hepatitis (HDV) alcance los USD 68,24 millones para 2031 desde USD 47,34 millones en 2023, creciendo a una CAGR del 4,8% en el período de pronóstico de 2024 a 2031.

Principales hallazgos del estudio

Aumento del gasto en atención sanitaria

El aumento del gasto sanitario tiene un impacto significativo en el crecimiento del mercado mundial de la infección por el virus de la hepatitis delta (VHD), al facilitar una mayor inversión en tecnologías de diagnóstico y opciones de tratamiento. A medida que aumentan los presupuestos sanitarios, los gobiernos y las organizaciones sanitarias pueden asignar más recursos a herramientas de diagnóstico avanzadas para el VHD. Esta inversión conduce al desarrollo y la implementación de métodos de prueba más sensibles y precisos, lo que mejora las tasas de detección temprana e impulsa la demanda de servicios de diagnóstico. La mayor disponibilidad de pruebas diagnósticas de alta calidad contribuye directamente al crecimiento del mercado al incrementar las actividades generales de prueba y cribado. Además, un mayor gasto sanitario suele traducirse en un mejor acceso y asequibilidad de las opciones de tratamiento para el VHD. A medida que aumenta la financiación, existe un mayor potencial para el desarrollo y la distribución de terapias antivirales innovadoras y otras intervenciones médicas. Este mayor acceso a tratamientos eficaces no solo mejora los resultados de los pacientes, sino que también estimula el crecimiento del mercado al crear una base más amplia de pacientes que buscan opciones de tratamiento. La mejora de las opciones terapéuticas puede conducir a un mejor manejo de la enfermedad y a mayores tasas de adherencia al tratamiento, lo que impulsa aún más la demanda en el mercado de la infección por VHD.

Alcance del informe y segmentación del mercado

Métrica del informe

|

Detalles

|

Período de pronóstico

|

2024 a 2031

|

Año base

|

2023

|

Años históricos

|

2022 (personalizable para 2016-2021)

|

Unidades cuantitativas

|

Ingresos en millones de USD

|

Segmentos cubiertos

|

Tipo (Hepatitis D aguda y crónica), Tratamiento (Cirugía [ Trasplante de hígado ] y Medicación), Tipo de fármaco (de marca y genérico), Vía de administración (Oral y Parenteral), Grupo de edad (Adultos, Geriatría y Pediatría), Género (Femenino y Masculino), Transmisión (Agujas contaminadas, Exposición a sangre infectada, Transfusión de productos de sangre y plasma, y otros), Usuario final (Hospitales, Clínicas especializadas, Entornos de atención domiciliaria, Institutos de investigación y Centros académicos, Centros de cirugía ambulatoria, y otros), Canal de distribución (Licitación directa, Ventas minoristas, y otros)

|

Países cubiertos

|

EE. UU., Canadá, México, Alemania, Francia, Reino Unido, Italia, España, Países Bajos, Suiza, Rusia, Bélgica, Turquía, Dinamarca, Suecia, Polonia, Noruega, Finlandia, Resto de Europa, China, Japón, India, Corea del Sur, Australia, Tailandia, Malasia, Indonesia, Singapur, Filipinas, Nueva Zelanda, Vietnam, Taiwán, Resto de Asia-Pacífico, Brasil, Argentina, Resto de Sudamérica, Sudáfrica, Arabia Saudita, Emiratos Árabes Unidos, Egipto, Baréin, Kuwait, Omán, Catar y Resto de Oriente Medio y África.

|

Actores del mercado cubiertos

|

Gilead Sciences, Inc. (EE. UU.), Genentech, Inc. (EE. UU.), Eiger BioPharmaceuticals (EE. UU.), Johnson & Johnson Services, Inc. (EE. UU.), Assembly Biosciences, Inc. (EE. UU.), PharmaEssentia Corporation (Taiwán), Vir Biotechnology, Inc. (EE. UU.), Huahui Health Ltd. (China), Replicor (Canadá), GlobeImmune Inc. (EE. UU.) y Alnylam Pharmaceuticals, Inc. (EE. UU.), entre otros.

|

Puntos de datos cubiertos en el informe

|

Además de los conocimientos sobre escenarios de mercado, como el valor de mercado, la tasa de crecimiento, la segmentación, la cobertura geográfica y los principales actores, los informes de mercado seleccionados por Data Bridge Market Research también incluyen un análisis profundo de expertos, epidemiología de pacientes, análisis de la cartera de productos, análisis de precios y marco regulatorio.

|

Análisis de segmentos

El mercado mundial de la infección por el virus delta de la hepatitis (VHD) está segmentado en nueve segmentos notables que son tipo, tratamiento, tipo de fármaco, vía de administración, grupo etario, género, transmisión, usuario final y canal de distribución.

- Según el tipo, el mercado mundial de infección por el virus de la hepatitis delta (VHD) se segmenta en hepatitis D aguda y hepatitis D crónica.

Se espera que en 2024, el segmento de hepatitis D aguda domine el mercado mundial de infecciones por el virus de la hepatitis delta (VHD).

Se espera que en 2024, el segmento de hepatitis D aguda domine el mercado con una participación de mercado del 95,15 % debido a su alta tasa de mortalidad, rápida progresión a insuficiencia hepática y opciones de tratamiento limitadas, lo que lo convierte en un área crítica de enfoque para investigadores y profesionales de la salud.

- Sobre la base del tratamiento, el mercado mundial de la infección por el virus de la hepatitis delta (VHD) se segmenta en cirugía (trasplante de hígado) y medicación.

Se espera que en 2024, el segmento de cirugía (trasplante de hígado) domine el mercado mundial de la infección por el virus de la hepatitis delta (VHD).

Se espera que en 2024, el segmento de cirugía (trasplante de hígado) domine el mercado con una participación de mercado del 63,75% debido a su creciente adopción como tratamiento de último recurso para pacientes con enfermedad hepática terminal o insuficiencia hepática causada por infección por VHD, lo que ofrece una posibilidad de supervivencia y una mejor calidad de vida.

- Según el tipo de fármaco, el mercado global de la infección por el virus de la hepatitis delta (VHD) se segmenta en medicamentos de marca y genéricos. Se prevé que en 2024, el segmento de medicamentos de marca domine el mercado con una cuota de mercado del 65,94 %.

- Según la vía de administración, el mercado mundial de la infección por el virus de la hepatitis delta (VHD) se segmenta en oral y parenteral. Se prevé que en 2024, el segmento oral domine el mercado con una cuota de mercado del 65,65 %.

- Según el grupo de edad, el mercado global de la infección por el virus de la hepatitis delta (VHD) se segmenta en adultos, ancianos y niños. Se prevé que en 2024, el segmento de adultos domine el mercado con una cuota de mercado del 68,16 %.

- En función del género, el mercado global de la infección por el virus de la hepatitis delta (VHD) se segmenta en mujeres y hombres. Se prevé que en 2024, el segmento femenino domine el mercado con una cuota de mercado del 69,36 %.

- En función de la transmisión, el mercado global de la infección por el virus de la hepatitis delta (VHD) se segmenta en agujas contaminadas, exposición a sangre infectada, transfusión de productos sanguíneos y plasmáticos, entre otros. Se prevé que en 2024, el segmento de agujas contaminadas domine el mercado con una cuota de mercado del 50,91 %.

- Según el usuario final, el mercado global de la infección por el virus de la hepatitis delta (VHD) se segmenta en hospitales, clínicas especializadas, centros de atención domiciliaria, institutos de investigación y centros académicos, centros de cirugía ambulatoria , entre otros. Se prevé que en 2024, el segmento hospitalario domine el mercado con una cuota de mercado del 48,66 %.

- Según el canal de distribución, el mercado global de la infección por el virus de la hepatitis delta (VHD) se segmenta en licitación directa, venta minorista y otros. Se prevé que en 2024, el segmento de licitación directa domine el mercado con una cuota de mercado del 58,71 %.

Actores principales

Data Bridge Market Research analiza a Gilead Sciences, Inc. (EE. UU.), Genentech, Inc. (EE. UU.), Eiger BioPharmaceuticals (EE. UU.), Johnson & Johnson Services, Inc. (EE. UU.), Assembly Biosciences, Inc. (EE. UU.) como los principales actores que operan en el mercado.

Desarrollo del mercado

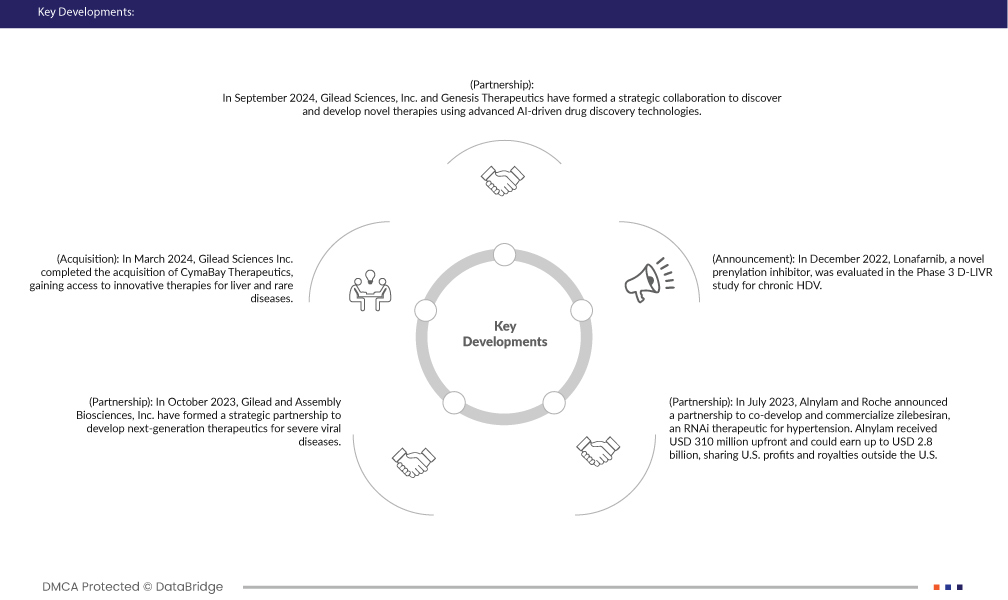

- En septiembre de 2024, Gilead Sciences, Inc. y Genesis Therapeutics firmaron una colaboración estratégica para descubrir y desarrollar nuevas terapias mediante tecnologías avanzadas de descubrimiento de fármacos basadas en IA. Esta alianza busca acelerar la creación de tratamientos innovadores, optimizar la cartera de productos de Gilead y fortalecer su posición en la competitiva industria biofarmacéutica.

- En junio de 2024, Assembly Biosciences, Inc. presentó nuevos datos sobre ABI-6250, un prometedor inhibidor de la entrada del virus de la hepatitis D. Esta innovación demuestra un gran potencial para dirigir la entrada del virus, lo que podría mejorar la eficacia del tratamiento y posicionar a la empresa como líder en el avance de las terapias contra la hepatitis D.

- En marzo de 2024, Gilead Sciences Inc. completó la adquisición de CymaBay Therapeutics, obteniendo acceso a terapias innovadoras para enfermedades hepáticas y raras. Esta adquisición amplía la cartera de investigación de Gilead y fortalece su cartera de productos, mejorando su capacidad para abordar necesidades médicas no cubiertas. La adquisición de CymaBay proporciona a Gilead nuevos fármacos candidatos prometedores y experiencia en enfermedades hepáticas y raras, impulsando su capacidad de investigación y ampliando su oferta terapéutica.

- En marzo de 2024, Gilead Sciences, Inc. y Merus anunciaron una colaboración para descubrir nuevos anticuerpos que activen células T triespecíficas, con el objetivo de mejorar la inmunoterapia contra el cáncer . Esta colaboración combina la experiencia de Gilead con la tecnología innovadora de Merus para desarrollar tratamientos avanzados contra el cáncer.

- En abril de 2023, el HH-003 de Huahui Health, un novedoso tratamiento para la infección crónica por el virus de la hepatitis D (VHD), recibió la designación de terapia innovadora de la NMPA de China. Esta designación acelera su desarrollo y revisión. El HH-003 ha mostrado resultados prometedores en ensayos clínicos iniciales y aborda una brecha en los tratamientos actuales para el VHD.

Análisis regional

Geográficamente, los países cubiertos en el informe de mercado global de infección por el virus de la hepatitis delta (HDV) son EE. UU., Canadá, México, Alemania, Francia, Reino Unido, Italia, España, Países Bajos, Suiza, Rusia, Bélgica, Turquía, Dinamarca, Suecia, Polonia, Noruega, Finlandia, Resto de Europa, China, Japón, India, Corea del Sur, Australia, Tailandia, Malasia, Indonesia, Singapur, Filipinas, Nueva Zelanda, Vietnam, Taiwán, Resto de Asia-Pacífico, Brasil, Argentina, Resto de Sudamérica, Sudáfrica, Arabia Saudita, Emiratos Árabes Unidos, Egipto, Baréin, Kuwait, Omán, Qatar y Resto de Medio Oriente y África.

Según el análisis de investigación de mercado de Data Bridge:

Europa es la región dominante y de más rápido crecimiento en el mercado mundial de infecciones por el virus de la hepatitis delta (VHD).

Se espera que Europa domine el mercado debido a la alta prevalencia del VHD en países como Rusia, Ucrania y países de Europa del Este, donde constituye un importante problema de salud pública e impulsa la demanda de soluciones de diagnóstico y tratamiento. Se prevé un crecimiento durante el período de pronóstico debido a la creciente prevalencia del VHD, la pronta aprobación de la bulevirtida y la sólida infraestructura sanitaria que respalda los tratamientos avanzados.

Para obtener información más detallada sobre el informe de mercado global sobre la infección por el virus de la hepatitis delta (HDV), haga clic aquí: https://www.databridgemarketresearch.com/reports/global-hepatitis-delta-virus-hdv-infection-market