Global Spinal Implants And Spinal Devices Market

Marktgröße in Milliarden USD

CAGR :

%

USD

10.60 Billion

USD

17.87 Billion

2023

2031

USD

10.60 Billion

USD

17.87 Billion

2023

2031

| 2024 –2031 | |

| USD 10.60 Billion | |

| USD 17.87 Billion | |

| % | |

|

Global Spinal Implants Market Segmentation, By Procedure (Open Surgery, Minimally Invasive Surgery, and Others), Product Type (Artificial Discs, Dynamic Stabilization Devices, Spinal Fusion Implants, Plates, and Cages), Application (Cervical, Thoracic, and Lumber), Material (Stainless Steel, Titanium, Cobalt Chrome, and Polyetheretherketone (PEEK), Indication (Spinal Trauma and Deformity), Configuration (Spinal Fusion Devices, Non-Fusion Devices/Motion Preservation Devices, Vertebral Compression Fracture (VCF) Treatment Devices, Spinal Bone Stimulators, and Spine Biologics) – Industry Trends and Forecast to 2031

Spinal Implants Market Analysis

The spinal implants market is experiencing significant growth, driven by the increasing prevalence of spinal disorders, the rising aging population, and advancements in surgical technologies. Spinal implants, including devices such as artificial discs, spinal fusion implants, and dynamic stabilization devices, are essential in treating conditions such as spinal trauma, deformities, and degenerative diseases. The introduction of minimally invasive surgical techniques has further enhanced the demand for these implants, as they reduce recovery times and minimize patient discomfort. Recent developments include innovations in implant materials and designs, improving the integration and longevity of devices within the body. Moreover, the growing awareness of spinal health and an increase in healthcare expenditure contribute to the market's expansion. Overall, the spinal implants market is poised for robust growth in the coming years, supported by technological advancements and a greater emphasis on effective spine care solutions.

Spinal Implants Market Size

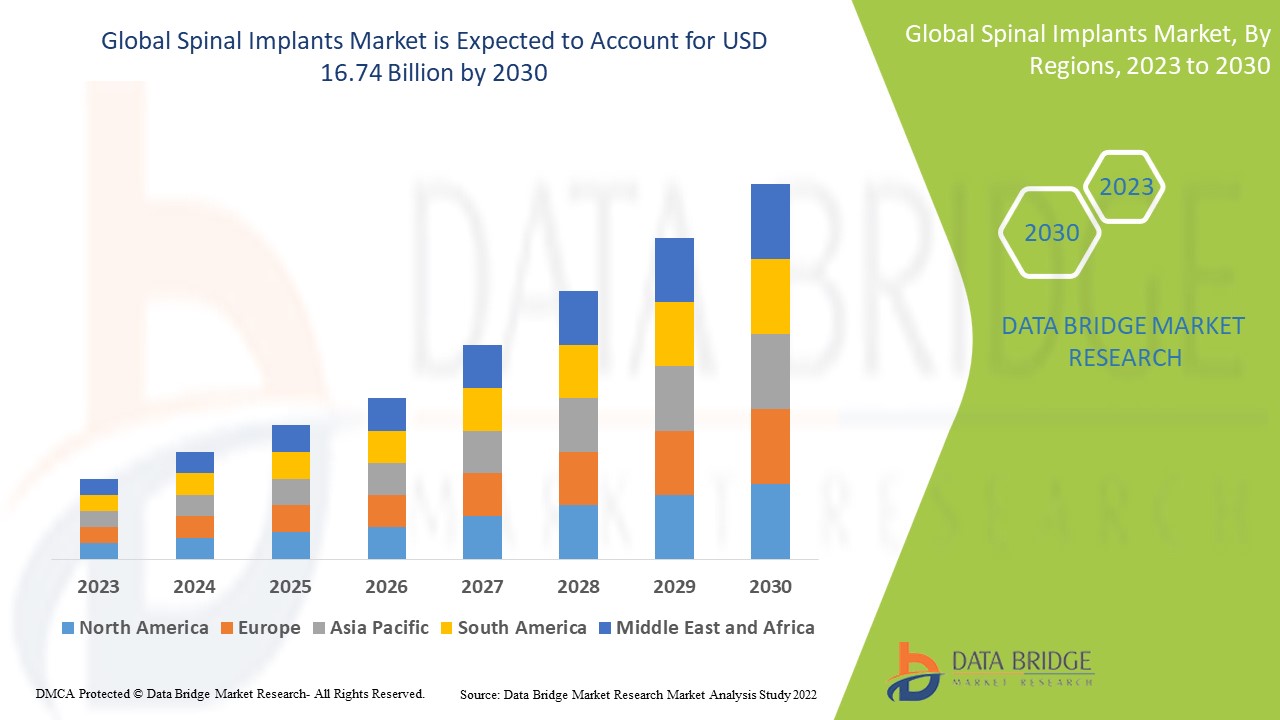

The global spinal implants market size was valued at USD 10.60 billion in 2023 and is projected to reach USD 17.87 billion by 2031, with a CAGR of 6.75% during the forecast period of 2024 to 2031. In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework.

Spinal Implants Market Trends

“Minimally Invasive Surgical Techniques”

Der Markt für Wirbelsäulenimplantate erlebt mehrere Trends, die durch technologische Fortschritte und sich ändernde Patientenbedürfnisse vorangetrieben werden. Ein bemerkenswerter Trend ist die zunehmende Einführung minimalinvasiver Operationstechniken, die die Patientenergebnisse verbessern, indem sie die Genesungszeiten und Operationsrisiken verkürzen. Innovationen im Implantatdesign, wie die Entwicklung bioresorbierbarer Materialien und intelligenter Implantate mit Sensoren, gewinnen ebenfalls an Bedeutung und bieten verbesserte Funktionalität und Möglichkeiten zur Patientenüberwachung. Darüber hinaus verbessert die Integration von Robotern und Navigationssystemen in Wirbelsäulenoperationen die Präzision und Genauigkeit während der Eingriffe. Da sich Gesundheitsdienstleister auf die Verbesserung der Patientenversorgung und -ergebnisse konzentrieren, deuten diese Trends auf eine Verlagerung hin zu fortschrittlicheren, effizienteren und patientenzentrierteren Wirbelsäulenimplantatlösungen auf dem Markt hin.

Berichtsumfang und Marktsegmentierung für Wirbelsäulenimplantate

|

Eigenschaften |

Wichtige Markteinblicke für Wirbelsäulenimplantate |

|

Abgedeckte Segmente |

|

|

Abgedeckte Länder |

USA, Kanada und Mexiko in Nordamerika, Deutschland, Frankreich, Großbritannien, Niederlande, Schweiz, Belgien, Russland, Italien, Spanien, Türkei, Restliches Europa in Europa, China, Japan, Indien, Südkorea, Singapur, Malaysia, Australien, Thailand, Indonesien, Philippinen, Restlicher Asien-Pazifik-Raum (APAC) im Asien-Pazifik-Raum (APAC), Saudi-Arabien, Vereinigte Arabische Emirate, Südafrika, Ägypten, Israel, Restlicher Naher Osten und Afrika (MEA) als Teil des Nahen Ostens und Afrikas (MEA), Brasilien, Argentinien und Restliches Südamerika als Teil von Südamerika. |

|

Wichtige Marktteilnehmer |

Medtronic (Irland), Zimmer Biomet (USA), ATEC Spine, Inc (USA), RTI Surgical (USA), Stryker (USA), Orthofix Medical Inc. (USA), NuVasive Inc. (USA), Globus Medical (USA), Aesculap, Inc. (USA), Apollo Hospitals Enterprise Ltd. (Indien), Centinel Spine, LLC (USA), Premia Spine (USA), Lumitex, LLC (USA), Life Spine, Inc. (USA) und Integra LifeSciences Corporation. (USA) |

|

Marktchancen |

|

|

Wertschöpfende Dateninfosets |

Zusätzlich zu den Einblicken in Marktszenarien wie Marktwert, Wachstumsrate, Segmentierung, geografische Abdeckung und wichtige Akteure enthalten die von Data Bridge Market Research zusammengestellten Marktberichte auch ausführliche Expertenanalysen, Patientenepidemiologie, Pipeline-Analysen, Preisanalysen und regulatorische Rahmenbedingungen. |

Marktdefinition für Wirbelsäulenimplantate

Wirbelsäulenimplantate sind medizinische Geräte, die bei verschiedenen chirurgischen Eingriffen zur Unterstützung und Stabilisierung der Wirbelsäule eingesetzt werden. Sie wurden entwickelt, um Wirbelsäulendeformationen zu korrigieren, den Druck auf Rückenmark und Nerven zu verringern und den Heilungsprozess der Wirbelstrukturen zu unterstützen. Zu den gängigen Arten von Wirbelsäulenimplantaten gehören Stäbe, Schrauben, Platten und Zwischenwirbelkäfige, die aus Materialien wie Titan, Edelstahl oder bioresorbierbaren Polymeren hergestellt werden können . Diese Implantate werden typischerweise bei Eingriffen wie Wirbelsäulenversteifungen , Dekompressionen und der Behandlung von Wirbelsäulenfrakturen oder -deformationen eingesetzt und tragen dazu bei, die Funktionsfähigkeit wiederherzustellen und die Lebensqualität von Patienten mit Wirbelsäulenerkrankungen zu verbessern.

Marktdynamik für Wirbelsäulenimplantate

Treiber

- Steigende Prävalenz von Wirbelsäulenerkrankungen

Die steigende Prävalenz von Wirbelsäulenerkrankungen, darunter degenerative Bandscheibenerkrankungen, Skoliose und Spinalkanalstenose, treibt die Nachfrage nach Wirbelsäulenimplantaten erheblich an. Da die Bevölkerung altert und der Lebensstil immer bewegungsärmer wird, steigt die Häufigkeit dieser Erkrankungen, was zu einem höheren Bedarf an chirurgischen Eingriffen führt. Patienten mit chronischen Rückenschmerzen und Mobilitätsproblemen greifen immer häufiger auf chirurgische Optionen zurück, was Gesundheitsdienstleister dazu veranlasst, fortschrittliche Technologien für Wirbelsäulenimplantate einzusetzen. Diese Implantate bieten eine verbesserte Lebensqualität, ermöglichen schnellere Genesungszeiten und verbessern die Gesamtergebnisse der Operation. Folglich macht die wachsende Patientenzahl, die nach wirksamen Lösungen für Wirbelsäulenerkrankungen sucht, Wirbelsäulenimplantate zu einem entscheidenden Bestandteil der Behandlungslandschaft, was diesen Trend zu einem wichtigen Markttreiber macht.

- Fortschritte in der Technologie

Innovationen im Design und bei Materialien für Wirbelsäulenimplantate schaffen erhebliche Marktchancen, insbesondere durch die Einführung minimalinvasiver Techniken, des 3D-Drucks und intelligenter Implantate. Minimalinvasive Operationen verkürzen die Genesungszeiten der Patienten, minimieren die Narbenbildung und verringern das allgemeine Operationsrisiko, was sie sowohl für Patienten als auch für Gesundheitsdienstleister zu einer attraktiven Option macht. Darüber hinaus ermöglicht die 3D-Drucktechnologie die individuelle Anpassung der Implantate an die Anatomie des Patienten, was eine bessere Passform und verbesserte Funktionalität gewährleistet. Intelligente Implantate, die mit Sensoren und Überwachungsfunktionen ausgestattet sind, ermöglichen die Datenerfassung in Echtzeit und ermöglichen so eine personalisierte postoperative Versorgung und verbesserte Patientenergebnisse. Wenn diese Innovationen an Zugkraft gewinnen, verbessern sie die Erfolgsraten bei Operationen und ermutigen Gesundheitseinrichtungen, fortschrittliche Wirbelsäulenimplantatlösungen einzuführen, was das allgemeine Marktwachstum ankurbelt.

Gelegenheiten

- Erweiterung des Produktportfolios

Hersteller auf dem Markt für Wirbelsäulenimplantate haben eine große Chance, ihre Marktpräsenz durch die Diversifizierung ihres Produktangebots zu stärken. Durch die Entwicklung ergänzender Produkte wie Wirbelsäulenfusionsgeräte, Biologika und Lösungen für die postoperative Pflege können sie umfassende Behandlungsoptionen schaffen, die den unterschiedlichen Anforderungen der Gesundheitsdienstleister gerecht werden. Dieser ganzheitliche Ansatz verbessert die Patientenergebnisse und fördert die Loyalität von Medizinern, die nach zuverlässigen und integrierten Lösungen für die Wirbelsäulenbehandlung suchen. Darüber hinaus kann das Angebot einer breiteren Produktpalette den Herstellern helfen, verschiedene Marktsegmente zu erschließen, sodass sie sowohl spezialisierte chirurgische Zentren als auch allgemeine Krankenhäuser bedienen können. Letztendlich verbessert diese Strategie den Wettbewerbsvorteil und fördert das Wachstum, indem sie den sich entwickelnden Anforderungen der Gesundheitslandschaft gerecht wird.

- Zunehmender Fokus auf vorbeugende Pflege

Da die Gesundheitsbranche immer mehr Wert auf vorbeugende Pflege legt, bietet sich eine bemerkenswerte Chance für die Entwicklung von Wirbelsäulenimplantaten, die eine frühzeitige Intervention bei Wirbelsäulenerkrankungen ermöglichen sollen. Durch die Konzentration auf proaktive Lösungen können Hersteller Implantate entwickeln, die bestehende Probleme angehen und dazu beitragen, das Fortschreiten von Wirbelsäulenerkrankungen zu verhindern. Diese Innovationen können das Risiko schwerer Komplikationen erheblich verringern und so die Notwendigkeit invasiverer Eingriffe später reduzieren. Darüber hinaus kann eine frühzeitige Intervention die Gesamtwirksamkeit von Behandlungen verbessern, was zu besseren Behandlungsergebnissen und einer höheren Zufriedenheit der Patienten führt. Indem sie ihre Produktentwicklungsstrategien auf den Trend zur vorbeugenden Pflege ausrichten, können sich Unternehmen als Marktführer für Wirbelsäulenimplantate positionieren und der wachsenden Nachfrage nach effektiven, zukunftsweisenden Lösungen im Bereich des Wirbelsäulengesundheitsmanagements gerecht werden.

Einschränkungen/Herausforderungen

- Infektion und Komplikationen

Chirurgische Eingriffe, darunter auch solche mit Wirbelsäulenimplantaten, bergen von Natur aus das Risiko von Infektionen und anderen Komplikationen, was sowohl für Gesundheitsdienstleister als auch für Hersteller eine erhebliche Herausforderung darstellt. Diese Risiken können Patienten von chirurgischen Eingriffen abhalten, insbesondere wenn sie Bedenken hinsichtlich postoperativer Infektionen, verlängerter Genesungszeiten oder der Möglichkeit weiterer Operationen haben. Die Angst vor negativen Ergebnissen kann dazu führen, dass Patienten nach alternativen, nicht-invasiven Behandlungsmöglichkeiten suchen, was den Markt für Wirbelsäulenimplantate einschränkt. Darüber hinaus können Komplikationen den Ruf der Hersteller von Wirbelsäulenimplantaten stark beeinträchtigen, da negative Erfahrungen zu Misstrauen gegenüber ihren Produkten führen können. Dies stellt eine erhebliche Herausforderung dar, Vertrauen bei Gesundheitsdienstleistern und Patienten aufzubauen, was sich letztlich auf das Marktwachstum und die Akzeptanz neuer Wirbelsäulenimplantattechnologien auswirkt.

- Hohe Kosten für Implantate

Die hohen Kosten für Wirbelsäulenimplantate, insbesondere für moderne und innovative Geräte, stellen sowohl für Gesundheitseinrichtungen als auch für Patienten eine erhebliche Zugangsbarriere dar. Chirurgische Implantate können unerschwinglich teuer sein und finanzielle Belastungen verursachen, die die Optionen für Patienten einschränken, die möglicherweise einen chirurgischen Eingriff wegen Wirbelsäulenerkrankungen benötigen. Dieses Problem ist besonders in Entwicklungsregionen ausgeprägt, wo die Gesundheitsbudgets begrenzt und die Ressourcen oft begrenzt sind. Folglich können die erhöhten Kosten zu verschobenen Operationen oder der Entscheidung führen, ganz auf eine chirurgische Behandlung zu verzichten. Infolgedessen erhalten viele Patienten möglicherweise nicht die notwendige Versorgung, was ihren Zustand verschlimmern und sich auf die allgemeinen Gesundheitsergebnisse auswirken kann. Diese finanzielle Barriere ist eine kritische Einschränkung auf dem Markt für Wirbelsäulenimplantate und unterstreicht den Bedarf an erschwinglicheren Lösungen.

Dieser Marktbericht enthält Einzelheiten zu neuen Entwicklungen, Handelsvorschriften, Import-Export-Analysen, Produktionsanalysen, Wertschöpfungskettenoptimierungen, Marktanteilen, Auswirkungen inländischer und lokaler Marktteilnehmer, analysiert Chancen in Bezug auf neue Einnahmequellen, Änderungen der Marktvorschriften, strategische Marktwachstumsanalysen, Marktgröße, Kategoriemarktwachstum, Anwendungsnischen und -dominanz, Produktzulassungen, Produkteinführungen, geografische Expansionen und technologische Innovationen auf dem Markt. Um weitere Informationen zum Markt zu erhalten, wenden Sie sich an Data Bridge Market Research, um einen Analystenbericht zu erhalten. Unser Team hilft Ihnen dabei, eine fundierte Marktentscheidung zu treffen, um Marktwachstum zu erzielen.

Marktumfang für Wirbelsäulenimplantate

Der Markt ist nach Verfahren, Produkttyp, Anwendung, Material, Indikation und Konfiguration segmentiert. Das Wachstum dieser Segmente hilft Ihnen bei der Analyse schwacher Wachstumssegmente in den Branchen und bietet den Benutzern einen wertvollen Marktüberblick und Markteinblicke, die ihnen bei der strategischen Entscheidungsfindung zur Identifizierung der wichtigsten Marktanwendungen helfen.

Verfahren

- Offene Chirurgie

- Minimalinvasive Chirurgie

- Sonstiges

Produkttyp

- Künstliche Bandscheiben

- Dynamische Stabilisierungsgeräte

- Wirbelsäulenfusionsimplantate

- Platten

- Käfige

Anwendung

- Gebärmutterhals

- Thorax

- Lendenwirbelsäule

Material

Anzeige

- Wirbelsäulentrauma

- Deformität

Konfiguration

- Geräte zur Wirbelsäulenfusion

- Nichtfusionsgeräte/Geräte zur Bewegungserhaltung

- Geräte zur Behandlung von Wirbelkompressionsfrakturen (VCF)

- Wirbelsäulen-Knochenstimulatoren

- Wirbelsäulenbiologie

Regionale Analyse des Marktes für Wirbelsäulenimplantate

Der Markt wird analysiert und es werden Einblicke in die Marktgröße und Trends nach Land, Verfahren, Produkttyp, Anwendung, Material, Indikation und Konfiguration wie oben angegeben bereitgestellt.

Die im Marktbericht abgedeckten Länder sind die USA, Kanada und Mexiko in Nordamerika, Deutschland, Frankreich, Großbritannien, Niederlande, Schweiz, Belgien, Russland, Italien, Spanien, Türkei, Restliches Europa in Europa, China, Japan, Indien, Südkorea, Singapur, Malaysia, Australien, Thailand, Indonesien, Philippinen, Restlicher Asien-Pazifik-Raum (APAC) in Asien-Pazifik (APAC), Saudi-Arabien, Vereinigte Arabische Emirate, Südafrika, Ägypten, Israel, Restlicher Naher Osten und Afrika (MEA) als Teil von Naher Osten und Afrika (MEA), Brasilien, Argentinien und Restliches Südamerika als Teil von Südamerika.

Nordamerika ist Marktführer bei Wirbelsäulenimplantaten, was vor allem auf die umfassende Verfügbarkeit der Produkte und die hohe Nutzungsrate in der gesamten Region zurückzuführen ist. Die Kombination aus fortschrittlicher Gesundheitsinfrastruktur und erheblicher Nachfrage nach Wirbelsäuleneingriffen untermauert diese Dominanz noch weiter. Daher bleibt Nordamerika ein wichtiger Akteur auf dem globalen Markt für Wirbelsäulenimplantate.

Der asiatisch-pazifische Raum wird voraussichtlich von 2024 bis 2031 die höchste Wachstumsrate verzeichnen, was auf die erhebliche ungedeckte Nachfrage nach Wirbelsäulenimplantaten zurückzuführen ist. Der laufende Aufbau von Produktionsanlagen durch wichtige Akteure der Branche sowie das zunehmende Bewusstsein der Patienten für innovative Technologien tragen zu dieser Wachstumskurve bei. Infolgedessen ist die Region bereit für erhebliche Fortschritte auf dem Markt für Wirbelsäulenimplantate.

Der Länderabschnitt des Berichts enthält auch Angaben zu einzelnen marktbeeinflussenden Faktoren und Änderungen der Regulierung auf dem Inlandsmarkt, die sich auf die aktuellen und zukünftigen Trends des Marktes auswirken. Datenpunkte wie Downstream- und Upstream-Wertschöpfungskettenanalysen, technische Trends und Porters Fünf-Kräfte-Analyse sowie Fallstudien sind einige der Anhaltspunkte, die zur Prognose des Marktszenarios für einzelne Länder verwendet werden. Bei der Prognoseanalyse der Länderdaten werden auch die Präsenz und Verfügbarkeit globaler Marken und ihre Herausforderungen aufgrund großer oder geringer Konkurrenz durch lokale und inländische Marken sowie die Auswirkungen inländischer Zölle und Handelsrouten berücksichtigt.

Marktanteil für Wirbelsäulenimplantate

Die Wettbewerbslandschaft des Marktes liefert Einzelheiten zu den einzelnen Wettbewerbern. Die enthaltenen Einzelheiten umfassen Unternehmensübersicht, Unternehmensfinanzen, erzielten Umsatz, Marktpotenzial, Investitionen in Forschung und Entwicklung, neue Marktinitiativen, globale Präsenz, Produktionsstandorte und -anlagen, Produktionskapazitäten, Stärken und Schwächen des Unternehmens, Produkteinführung, Produktbreite und -umfang, Anwendungsdominanz. Die oben angegebenen Datenpunkte beziehen sich nur auf den Fokus der Unternehmen in Bezug auf den Markt.

Die Marktführer für Wirbelsäulenimplantate sind:

- Medtronic (Irland)

- Zimmer Biomet (US)

- ATEC Spine, Inc (USA)

- RTI Surgical (USA)

- Stryker (USA)

- Orthofix Medical Inc. (USA)

- NuVasive Inc. (USA)

- Globus Medical (USA)

- Aesculap, Inc. (USA)

- Apollo Hospitals Enterprise Ltd. (Indien)

- Centinel Spine, LLC (USA)

- Premia Spine (USA)

- Lumitex, LLC (USA)

- Life Spine, Inc. (USA)

- Integra LifeSciences Corporation. (USA)

Neueste Entwicklungen auf dem Markt für Wirbelsäulenimplantate

- Im Januar 2024 stellte Accelus, ein US-amerikanisches Medizintechnikunternehmen, das Linesider Modular-Cortical System vor, das die Präzision und Effizienz von Wirbelsäulenimplantatoperationen verbessern soll. Dieses innovative System erleichtert das frühzeitige Einsetzen von Schraubenschäften während der Eingriffe und bietet die Flexibilität, die chirurgische Konstruktion mithilfe modularer Tulpen und Stäbe individuell anzupassen. Sein Design ermöglicht eine Reihe von chirurgischen Techniken sowohl in kortikalen als auch in offenen modularen Konfigurationen.

- Im April 2024 kündigte Proprio eine mehrphasige Zusammenarbeit mit der Biedermann Group an, einem führenden Anbieter fortschrittlicher Wirbelsäulenbehandlungslösungen und Implantatsysteme. Ziel dieser Partnerschaft ist die Integration der innovativen Wirbelsäulenimplantate von Biedermann mit dem Paradigm-System von Proprio, das künstliche Intelligenz, Computervision und Augmented Reality nutzt, um eine hervorragende Echtzeitvisualisierung und -führung bei chirurgischen Eingriffen zu ermöglichen. Ziel der Zusammenarbeit ist es, die Operationsergebnisse durch die kombinierte Expertise beider Unternehmen zu verbessern.

- Im Oktober 2023 gab Johnson & Johnson MedTech bekannt, dass DePuy Synthes, seine orthopädische Abteilung, von der US-amerikanischen FDA die 510(k)-Zulassung für das TriALTIS Spine System und die TriALTIS Navigation Enabled Instruments erhalten hat. Das TriALTIS Spine System verfügt über eine hochmoderne Palette von Pedikelschrauben, die speziell für die hintere thorakolumbale Region entwickelt wurden und eine vielfältige Auswahl an Implantaten und fortschrittlichen Instrumenten bieten. Diese Zulassung stellt einen bedeutenden Fortschritt bei den verfügbaren Optionen für die Wirbelsäulenchirurgie dar.

- In September 2023, Silony Medical International AG completed the acquisition of Centinel Spine’s Global Fusion Business. This strategic acquisition merged Silony’s posterior screw and rod fusion systems with Centinel Spine’s Fusion Products, which include cervical stand-alone cages, lateral stand-alone cages, anterior cervical plates, and ALIF devices. As a result, Silony enhanced its technological capabilities and expanded its geographic reach, allowing the company to provide a comprehensive array of spinal fusion solutions for both open and minimally invasive procedures

- In January 2023, Companion Spine announced its acquisition of Backbone SAS, significantly enhancing its medical implant solutions portfolio. The addition of Backbone's LISA implant allows Companion Spine to offer a comprehensive range of therapies for spinal disorders, including lumbar stenosis and degenerative disc disease. This strategic move enables the company to tailor its implants to align with the severity of various spinal conditions, improving treatment options for patients

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.