Global Cancer Diagnostics Market

Marktgröße in Milliarden USD

CAGR :

%

USD

110.11 Billion

USD

199.32 Billion

2024

2032

USD

110.11 Billion

USD

199.32 Billion

2024

2032

| 2025 –2032 | |

| USD 110.11 Billion | |

| USD 199.32 Billion | |

| % | |

|

Globale Marktsegmentierung für Krebsdiagnostik nach Produkt (Verbrauchsmaterialien und Instrumente), Technologie (IVD-Tests, Bildgebung und Biopsietechnik), Typ (Bildgebungstests, Biomarkertests, In-vitro-Diagnosetests, Biopsie und andere), Anwendung (Lungenkrebs, Brustkrebs, Dickdarmkrebs, Melanomkrebs, Prostatakrebs, Leberkrebs und andere), Endbenutzer (Diagnosezentren, Krankenhäuser und Kliniken, Forschungsinstitute und andere) – Branchentrends und Prognose bis 2032

Marktgröße für Krebsdiagnostik

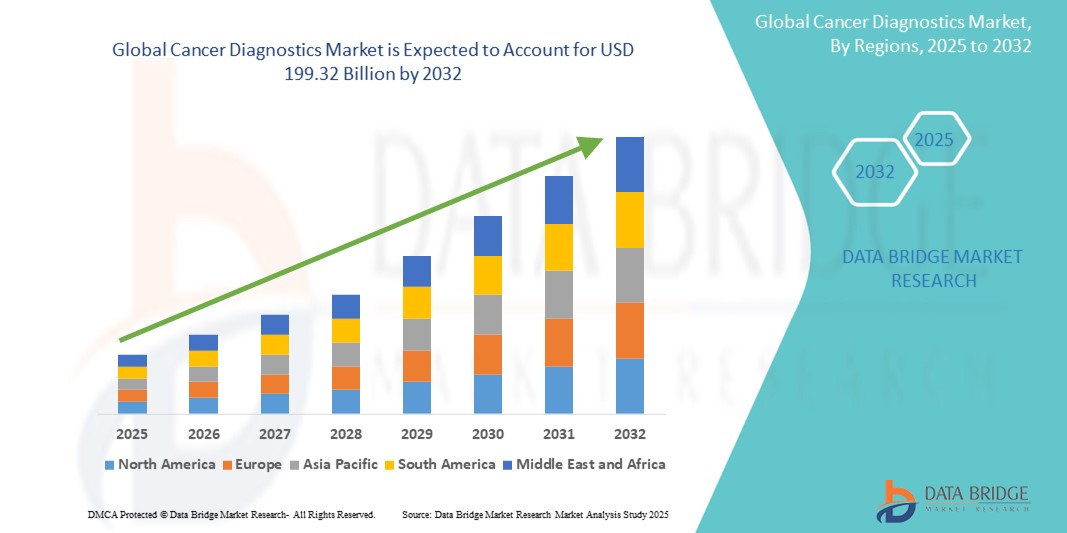

- Der globale Markt für Krebsdiagnostik wird im Jahr 2024 auf 110,11 Milliarden US-Dollar geschätzt und soll bis 2032 einen Wert von 199,32 Milliarden US-Dollar erreichen , was einer jährlichen Wachstumsrate (CAGR) von 7,70 % im Prognosezeitraum entspricht.

- Dieses Wachstum wird durch Faktoren wie die steigende globale Krebsbelastung, das wachsende Bewusstsein für die Früherkennung von Krebs und Fortschritte in der Diagnosetechnologie, einschließlich der Flüssigbiopsie und der KI-gestützten Bildgebung, vorangetrieben.

Marktanalyse für Krebsdiagnostik

- Krebsdiagnostikinstrumente sind für die Früherkennung, Diagnose und Überwachung verschiedener Krebsarten von entscheidender Bedeutung. Dabei kommen Methoden wie Bildgebung, Biopsie, Tumormarker und Molekulardiagnostik zum Einsatz.

- Die Nachfrage nach Krebsdiagnostik wird maßgeblich durch die weltweit steigende Krebsinzidenz, das wachsende Bewusstsein für die Vorteile der Früherkennung und den technologischen Fortschritt bei den Diagnosemodalitäten getrieben.

- Nordamerika wird voraussichtlich den Markt für Krebsdiagnostik mit einem größten Marktanteil von 41,18 % dominieren, aufgrund der gut ausgebauten Gesundheitsinfrastruktur, der hohen Krebsprävalenz und erheblicher Investitionen in Forschung und Entwicklung.

- Der asiatisch-pazifische Raum dürfte im Prognosezeitraum aufgrund der zunehmenden Alterung der Bevölkerung, der steigenden Gesundheitsausgaben und des verbesserten Zugangs zu Diagnosediensten die am schnellsten wachsende Region im Markt für Krebsdiagnostik sein.

- Das Segment der In-vitro-Diagnostik wird voraussichtlich den Markt mit einem Marktanteil von 52,1 % dominieren, da IVD aufgrund der zunehmenden Testanzahl während der COVID-19-Pandemie zunehmend eingesetzt wird. Die Entwicklung automatisierter IVD-Systeme für Krankenhäuser und Labore, die eine genaue, effiziente und fehlerfreie Diagnose ermöglichen, dürfte das Marktwachstum ankurbeln.

Berichtsumfang und Marktsegmentierung für Krebsdiagnostik

|

Eigenschaften |

Wichtige Markteinblicke zur Krebsdiagnostik |

|

Abgedeckte Segmente |

|

|

Abgedeckte Länder |

Nordamerika

Europa

Asien-Pazifik

Naher Osten und Afrika

Südamerika

|

|

Wichtige Marktteilnehmer |

|

|

Marktchancen |

|

|

Wertschöpfungsdaten-Infosets |

Zusätzlich zu den Einblicken in Marktszenarien wie Marktwert, Wachstumsrate, Segmentierung, geografische Abdeckung und wichtige Akteure enthalten die von Data Bridge Market Research kuratierten Marktberichte auch ausführliche Expertenanalysen, Patientenepidemiologie, Pipeline-Analysen, Preisanalysen und regulatorische Rahmenbedingungen. |

Markttrends in der Krebsdiagnostik

„Aufkommen von KI, Liquid Biopsy und Multi-Cancer Early Detection (MCED) als bahnbrechende Trends“

- Ein herausragender Trend auf dem globalen Markt für Krebsdiagnostik ist die schnelle Integration von Technologien für künstliche Intelligenz (KI), Flüssigbiopsie und Multi-Krebs-Früherkennung (MCED) in die gängigen Diagnoseverfahren.

- Diese Innovationen verändern die diagnostische Landschaft, indem sie eine frühere, präzisere und weniger invasive Erkennung mehrerer Krebsarten anhand einer einzigen Probe ermöglichen.

- So können beispielsweise Liquid-Biopsy-Plattformen zirkulierende Tumor-DNA (ctDNA) im Blut erkennen und so Echtzeit-Einblicke in Tumormutationen bieten, ohne dass eine chirurgische Biopsie erforderlich ist. Gleichzeitig verbessern KI-gestützte Bildgebungstools die diagnostische Genauigkeit in der Radiologie und Pathologie.

- Diese Trends treiben den Wandel hin zur personalisierten Medizin voran, verbessern die klinische Entscheidungsfindung und erweitern das Potenzial für groß angelegte Krebsvorsorgeuntersuchungen, insbesondere bei asymptomatischen Bevölkerungsgruppen.

Marktdynamik für Krebsdiagnostik

Treiber

„Steigende Krebsbelastung und Notwendigkeit einer Früherkennung“

- Die weltweit wachsende Krebsbelastung, die durch die alternde Bevölkerung, veränderte Lebensstile und Umweltfaktoren verursacht wird, erhöht die Nachfrage nach fortschrittlichen Krebsdiagnoseinstrumenten erheblich.

- As cancer remains a leading cause of death worldwide, early detection has become a critical public health priority, prompting governments and healthcare providers to invest heavily in screening and diagnostic infrastructure

- The availability of innovative diagnostics—including molecular testing, imaging, and next-generation sequencing—enables earlier intervention and improves survival rates by identifying cancers at treatable stages

For instance,

- According to the World Health Organization (WHO), there were an estimated 20 million new cancer cases and 10 million cancer-related deaths globally in 2022, with projections suggesting a sharp increase in incidence over the coming decades

- As a result of the rising cancer prevalence and the recognized benefits of early diagnosis, the global demand for precise, rapid, and scalable cancer diagnostic solutions is experiencing significant growth

Opportunity

“Expansion of Cancer Screening Programs in Emerging Economies”

- Rapid urbanization, increasing healthcare investments, and improved awareness are driving the expansion of organized cancer screening programs in low- and middle-income countries

- Governments and health organizations are launching initiatives aimed at early detection of high-burden cancers such as breast, cervical, and colorectal cancers, creating significant demand for affordable and scalable diagnostic technologies

- Additionally, the availability of portable diagnostic devices and telemedicine solutions is making it easier to deliver screening services in rural and underserved areas

For instance,

- In October 2023, the World Health Organization (WHO) launched the Global Breast Cancer Initiative to reduce breast cancer mortality globally through improved early detection and timely diagnosis, with a strong focus on supporting low- and middle-income countries

- As global efforts to reduce cancer-related deaths intensify, emerging markets offer substantial growth opportunities for diagnostic companies to introduce cost-effective, accessible, and innovative cancer detection solutions

Restraint/Challenge

“High Cost and Limited Accessibility of Advanced Diagnostic Technologies”

- The high cost of advanced cancer diagnostic tools, such as molecular testing, next-generation sequencing (NGS), and PET/CT imaging, presents a major barrier to widespread adoption—particularly in low- and middle-income countries

- These technologies, while highly accurate, often require sophisticated infrastructure, skilled personnel, and ongoing operational costs, which can strain healthcare budgets in resource-limited settings

- This financial burden limits the scalability of comprehensive cancer screening programs and contributes to late-stage diagnoses, especially in underserved regions

For instance,

- In einem Bericht der Internationalen Agentur für Krebsforschung (IARC) aus dem Jahr 2023 wurden erhebliche Unterschiede beim Zugang zu Diagnosediensten festgestellt. In Ländern mit niedrigem Einkommen lag die Diagnoseabdeckung für Krebsarten wie Gebärmutterhals- und Dickdarmkrebs bei weniger als 30 % – im Vergleich zu über 80 % in Ländern mit hohem Einkommen.

- Infolgedessen behindert der eingeschränkte Zugang zu fortschrittlicher Diagnostik weiterhin die Früherkennung und eine gerechte Gesundheitsversorgung und stellt eine große Herausforderung für die weltweite Verbreitung der Krebsdiagnostik dar.

Marktumfang für Krebsdiagnostik

Der Markt ist nach Produkt, Technologie, Typ, Anwendung und Endbenutzer segmentiert

|

Segmentierung |

Untersegmentierung |

|

Nach Produkt |

|

|

Nach Technologie |

|

|

Nach Typ |

|

|

Nach Anwendung |

|

|

Nach Endbenutzer |

|

Im Jahr 2025 wird erwartet, dass die In-vitro-Diagnostik den Markt mit dem größten Anteil im Typsegment dominieren wird

Das Segment der In-vitro-Diagnostik wird voraussichtlich den Markt für Krebsdiagnostik mit einem Anteil von 52,1 % dominieren. Dies ist auf die zunehmende Verbreitung von IVD aufgrund der steigenden Anzahl an Tests während der COVID-19-Pandemie zurückzuführen. Die Entwicklung automatisierter IVD-Systeme für Krankenhäuser und Labore, die eine genaue, effiziente und fehlerfreie Diagnose ermöglichen, dürfte das Marktwachstum ankurbeln.

Die Verbrauchsmaterialien werden voraussichtlich den größten Anteil im Prognosezeitraum im Produktsegment ausmachen

Im Jahr 2025 wird das Verbrauchsmaterialsegment voraussichtlich den Markt mit einem Marktanteil von 58,5 % dominieren. Dies ist auf die Entwicklung bildgebender Diagnoseverfahren oder effektiver monoklonaler Antikörper-basierter Assays zum Nachweis von Antigenen und kleinen, von malignen Zellen erzeugten Chemikalien zurückzuführen, die die diagnostische Medizin erheblich verbessern würden. Obwohl sich die mAb-Technologie noch in einem frühen Stadium befindet, haben neue Entwicklungen in der rekombinanten Antigensynthese und der Antikörperherstellung ihr Potenzial in der Diagnostik erheblich erweitert.

Regionale Analyse des Krebsdiagnostikmarktes

„Nordamerika hält den größten Anteil am Markt für Krebsdiagnostik“

- Nordamerika dominiert den globalen Markt für Krebsdiagnostik mit dem größten Marktanteil von 41,18 %, was auf die fortschrittliche Gesundheitsinfrastruktur, die hohe Akzeptanz modernster Diagnosetechnologien und die Präsenz führender Krebsforschungseinrichtungen und Diagnoseunternehmen zurückzuführen ist.

- The U.S. holds a significant share of 36.4%, due to the increasing prevalence of cancer, a well-established reimbursement system, and continuous advancements in molecular diagnostics and imaging technologies

- Strong government initiatives for cancer research, high healthcare spending, and a growing focus on early cancer detection are key factors driving the market in this region

- Additionally, the expanding availability of personalized and precision medicine, along with high rates of cancer screening, are contributing to the growth of the cancer diagnostics market in North America

“Asia-Pacific is Projected to Register the Highest CAGR in the Cancer Diagnostics Market”

- The Asia-Pacific region is expected to witness the highest growth rate in the cancer diagnostics market, driven by rapid advancements in healthcare infrastructure, increasing awareness about cancer, and improving access to diagnostic technologies

- Countries like China, India, and Japan are emerging as key markets due to the growing aging population, rising cancer incidence, and improvements in healthcare facilities

- Japan, with its strong healthcare system and focus on innovative diagnostic solutions, remains a leading market for cancer diagnostics. The country continues to adopt advanced technologies such as AI-based imaging and liquid biopsy for early cancer detection

- China and India, with their large populations and increasing cancer burden, are witnessing heightened investments in cancer screening and diagnostic services. The growing presence of global diagnostic companies and government initiatives to expand healthcare access are further fueling market growth in the region

Cancer Diagnostics Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Thermo Fisher Scientific (U.S.)

- Abbott (U.S.)

- Siemens Healthineers (Germany)

- Koninklijke Philips N.V. (Netherlands)

- BD (U.S.)

- GE Healthcare (U.S.)

- Hologic, Inc. (U.S.)

- Illumina, Inc. (U.S.)

- Exact Sciences Corporation (U.S.)

- Guardant Health (U.S.)

- Myriad Genetics (U.S.)

- NeoGenomics Laboratories (U.S.)

- BioMérieux SA (France)

- Qiagen N.V. (Germany)

- Leica Biosystems (Germany)

- Cepheid (U.S.)

- Danaher Corporation (U.S.)

- Agilent Technologies (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

Latest Developments in Global Cancer Diagnostics Market

- In July 2024, DELFI Diagnostics announced that it has secured an equity investment from the Merck Global Health Innovation Fund. This strategic funding will accelerate the development of DELFI’s AI-driven fragmentomics platform designed for advanced cancer screening. The collaboration is focused on enhancing diagnostic capabilities and advancing the methodologies used for more accurate cancer detection. This partnership aligns with the growing trend towards AI-powered diagnostic solutions and precision oncology. The investment will support the development of cutting-edge technologies that are poised to revolutionize early cancer detection, driving innovation in the market and expanding the availability of advanced diagnostic tools globally

- In May 2024, Quest Diagnostics revealed the separation of PathAI’s digital pathology laboratory as part of a strategic initiative to deepen its focus on artificial intelligence (AI) integration. This move is designed to expedite the adoption of AI technologies within the company's operations, with the goal of enhancing its digital pathology capabilities and improving diagnostic accuracy. This development highlights the growing trend of incorporating AI-driven solutions into diagnostic workflows. By advancing its digital pathology offerings, Quest Diagnostics is positioning itself at the forefront of the shift toward more precise and efficient cancer detection

- In February 2023, F. Hoffmann-La Roche announced the expansion of its collaboration with Janssen to further advance personalized healthcare initiatives. This strengthened partnership will focus on the development of companion diagnostics, with the goal of improving treatment outcomes for patients by enabling more precise and tailored therapeutic approaches. This collaboration underscores the increasing shift towards precision oncology and the growing importance of companion diagnostics in improving cancer treatment

- In November 2023, Abbott received FDA approval for its HPV test, developed for use with the Alinity m platform. This diagnostic tool is designed for primary screening of HPV and detection of high-risk HPV types linked to cancer, particularly cervical cancer. This approval significantly strengthens Abbott’s portfolio in cervical cancer prevention and diagnosis, aligning with the growing demand for advanced screening solutions in the global cancer diagnostics market

- In 2022, Precipio, Inc. entered into a distribution agreement for its HemeScreen product with a prominent distribution partner in the U.S. The company is strategically pursuing an expansive growth plan for HemeScreen, targeting physician-owned laboratories, national and regional hospital networks, and reference laboratories. This move emphasizes the increasing demand for advanced diagnostic tools that enable more precise and efficient detection of hematologic cancers

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.