Europäischer Markt für Laborautomatisierung, nach Produkttyp (Geräte, Software & Informatik und Analysatoren), Automatisierungstyp (Modulare Automatisierung und vollständige Laborautomatisierung), Anwendung (Arzneimittelentdeckung, Klinische Diagnostik, Genomiklösungen, Proteomiklösungen, Bioanalyse, Protein-Engineering, Gefriertrocknung, Systembiologie, Analytische Chemie und andere), Endbenutzer (Biotechnologie & Pharmazeutika, Krankenhäuser & Labore, Forschungs- und akademische Einrichtungen und andere) – Branchentrends und Prognose bis 2029.

Marktanalyse und Einblicke in die Laborautomatisierung in Europa

Die Nachfrage auf dem Markt für Laborautomatisierung steigt aufgrund des technologischen Fortschritts auf der ganzen Welt. Im Gesundheitssektor werden Laborautomatisierungsgeräte und -werkzeuge eingesetzt. Da die Gesundheitsausgaben aufgrund verschiedener Faktoren gestiegen sind, müssen die führenden Pharma- und Gesundheitsunternehmen die Labore automatisieren, um fortschrittliche Gesundheitsdienstleistungen in kürzerer Zeit direkt vor der Haustür anbieten zu können.

Die wachsende Nachfrage nach Gesundheitsprodukten auf dem Markt ist der Hauptgrund für den Wettbewerb zwischen den führenden Gesundheits- und Pharmaunternehmen bei der Verbesserung der Laborautomatisierung weltweit. Der Anstieg der Nutzung von Geräten, Analysegeräten und Software für das Labor wurde genutzt. Der Schwerpunkt der Marktteilnehmer liegt darauf, eine Vielfalt an Werkzeugen, Geräten, Maschinen und Techniken bereitzustellen, um die Entwicklung und Herstellung einer automatisierten Laborinfrastruktur zu unterstützen. Die Marktteilnehmer investieren mehr und finanzieren mehr, um fortschrittliche Technologien und Methoden zu entwickeln.

Die Gesundheitsausgaben sind aufgrund verschiedener Faktoren gestiegen, wie beispielsweise der alternden Bevölkerung, der Häufigkeit chronischer Krankheiten, steigender Medikamentenpreise, Kosten für Gesundheitsdienstleistungen und Verwaltungskosten. Darüber hinaus gibt es immer mehr Krankenhäuser, private Labore, Zentren für klinische Forschung und Diagnostik, was die Nachfrage nach Laborautomatisierung erhöht.

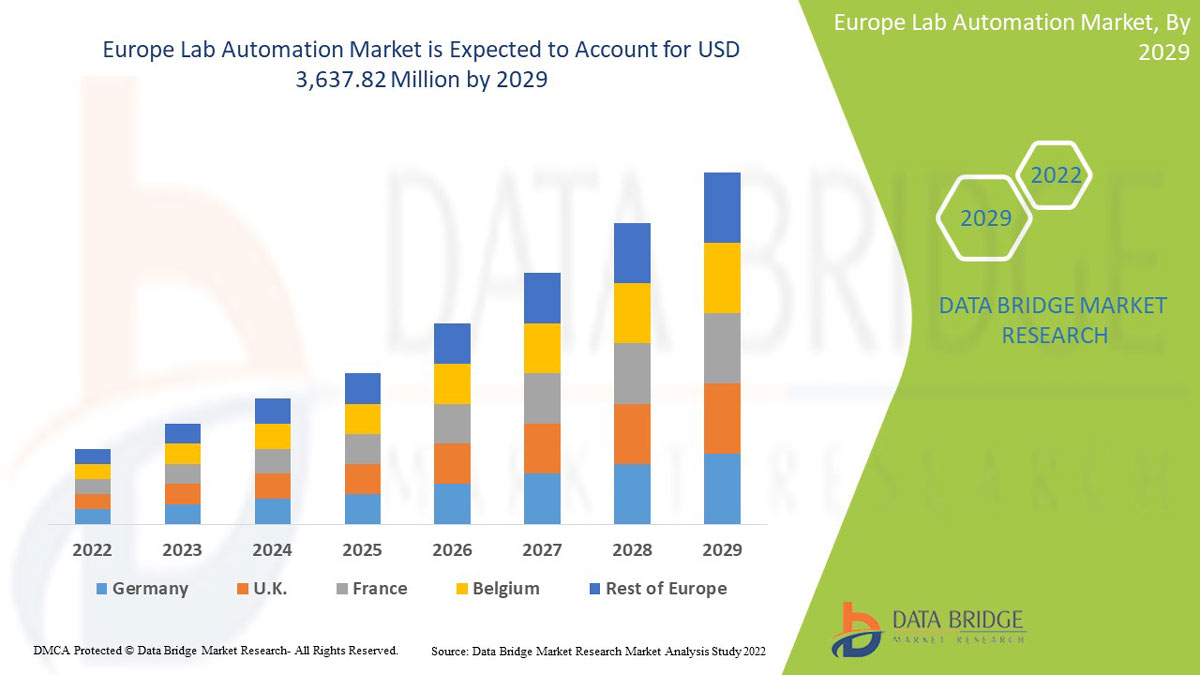

Der europäische Markt für Laborautomatisierung wird im Prognosezeitraum von 2022 bis 2029 voraussichtlich ein Marktwachstum verzeichnen. Data Bridge Market Research analysiert, dass der Markt im Prognosezeitraum von 2022 bis 2029 mit einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 6,0 % wächst und bis 2029 voraussichtlich 3.637,82 Millionen USD erreichen wird.

|

Berichtsmetrik |

Details |

|

Prognosezeitraum |

2022 bis 2029 |

|

Basisjahr |

2021 |

|

Historische Jahre |

2020 (anpassbar auf 2019–2014) |

|

Quantitative Einheiten |

Umsatz in Mio. USD |

|

Abgedeckte Segmente |

Nach Produkttyp (Ausrüstung, Software & Informatik und Analysator), Automatisierungstyp (Modulare Automatisierung und vollständige Laborautomatisierung), Anwendung (Arzneimittelentdeckung, klinische Diagnostik, Genomiklösungen, Proteomiklösungen, Bioanalyse, Protein-Engineering , Gefriertrocknung, Systembiologie, analytische Chemie und andere), Endbenutzer ( Biotechnologie & Pharmazeutika, Krankenhäuser & Labore, Forschungs- und akademische Einrichtungen und andere) |

|

Abgedeckte Länder |

Deutschland, Frankreich, Großbritannien, Italien, Spanien, Niederlande, Russland, Belgien, Schweiz, Türkei, Restliches Europa |

|

Abgedeckte Marktteilnehmer |

QIAGEN, Siemens Healthcare, F. Hoffman Roche, Hamilton Company, Hudson Robotics, LabVantage Solutions Inc., Abbott, BD, BIOMERIEUX, Aurora Biomed Inc., Danaher, Tecan Trading AG, PerkinElmer Inc, Thermo Fisher Scientific, Agilent Technologies, Azenta US Inc, Eppendorf SE und Labware unter anderem |

Marktdefinition

Laborautomatisierung ist die Kombination automatisierter Technologien im Labor, um neue und verbesserte Prozesse zu ermöglichen. Sie wird als Strategie zur Erforschung, Entwicklung, Optimierung und Nutzung von Technologien im Labor eingesetzt. Sie wird speziell zur Automatisierung von Laborprozessen verwendet, die nur minimalen menschlichen Aufwand erfordern und menschliche Fehler ausschließen. Laborautomatisierung wird mit dem Ziel eingesetzt, effizientere Tests und Diagnosen bereitzustellen.

Durch Laborautomatisierung können Forscher und Techniker in kürzerer Zeit effizient und effektiv Ergebnisse erzielen, was den Markt für Laborautomatisierung voraussichtlich ankurbeln wird. Darüber hinaus lässt die schnelle Verbreitung von Krankheiten sowie neue Erkenntnisse im Gesundheitsbereich die Nachfrage nach Diagnosen und Behandlungen steigen, was den Markt für Laborautomatisierung voraussichtlich ankurbeln wird. Hohe staatliche und private Mittel für Forschung und Entdeckungsforschung sowie die Präsenz wichtiger Marktteilnehmer tragen ebenfalls zum Marktwachstum bei.

Marktdynamik für Laborautomatisierung

Treiber

- Steigende Investitionen und strategische Initiativen der Marktteilnehmer

Der Markt für Laborautomatisierung wächst, da eine hohe Nachfrage nach spezialisierten, fortschrittlichen Automatisierungsdiensten besteht, die menschliche Fehler ausschließen. Der Schwerpunkt der Marktteilnehmer und Unternehmen liegt darauf, eine Vielfalt an Werkzeugen, Geräten, Maschinen und Techniken bereitzustellen, um die Entwicklung und Herstellung automatisierter Laborinfrastruktur zu unterstützen. Der Markt für Laborautomatisierung wächst, da eine hohe Nachfrage nach spezialisierten, fortschrittlichen Automatisierungsdiensten besteht, die menschliche Fehler ausschließen. Um Marktanteile zu gewinnen, investieren die Marktteilnehmer mehr und finanzieren die Entwicklung fortschrittlicher Technologien und Methoden. Diese Akteure konzentrieren sich stärker darauf, manuelle Anstrengungen und praktische Zeit für den traditionell arbeitsintensiven Prozess zu reduzieren. Dies dürfte das Marktwachstum vorantreiben.

- Regierungsinitiativen zur Stärkung der Laborinfrastruktur

Um den Gesundheitssektor und die Laborinfrastruktur weiter zu stärken, spielen Regierungsorganisationen eine wichtige Rolle. Die staatliche Finanzierung und Initiative zur Ausweitung der Laborautomatisierung wird das Marktwachstum fördern und die Zahl der Marktteilnehmer erhöhen. Die Zusammenarbeit und Vereinbarungen der Regierung mit den wichtigsten Marktteilnehmern werden die Laborinfrastruktur weiter stärken.

- Steigende Ausgaben für Werkzeuge und Geräte zur Laborautomatisierung

Die Ausgaben für Werkzeuge und Geräte zur Laborautomatisierung steigen. Dies liegt vor allem daran, dass die Nachfrage nach Laboruntersuchungen aus verschiedenen Gründen rapide zunimmt, beispielsweise aufgrund der alternden Bevölkerung, der Zunahme chronischer Krankheiten, der Entdeckung neuer und wirksamerer Biomarker und der Zunahme allgemeiner Anforderungen an die Gesundheit oder Diagnostik.

- Reduzierung des menschlichen Aufwands und Beseitigung menschlicher Fehler

Es gibt mehrere traditionelle Möglichkeiten, menschliche Fehler zu reduzieren, aber die Entwicklung eines Systems zur Minimierung des Risikos menschlicher Fehler wird dazu beitragen, dass Sie dieselben Fehler nicht noch einmal wiederholen. Produktionsstätten konzentrieren sich auf den Aufbau fortschrittlicher Systeme, um mithilfe künstlicher Intelligenz Probleme zu erkennen und zu beheben, bevor sie auftreten.

Gelegenheiten

-

Steigende Gesundheitsausgaben

Die Gesundheitsausgaben sind aufgrund verschiedener Faktoren gestiegen, darunter die alternde Bevölkerung, die Prävalenz chronischer Krankheiten, steigende Medikamentenpreise, Kosten für Gesundheitsdienstleistungen und Verwaltungskosten. Der Wendepunkt war jedoch das Jahr 2020, in dem die Ausgaben aufgrund der COVID-19-Pandemie am höchsten waren. Es wurde festgestellt, dass die Gesundheitsausgaben im Jahr 2020 aufgrund der Pandemie mit der höchsten Wachstumsrate seit 2002 wuchsen .

-

Strategische Initiativen wichtiger Akteure

Die führenden Pharma- und Gesundheitsunternehmen haben verschiedene Initiativen ergriffen, um die Labore zu automatisieren und so fortschrittliche Gesundheitsdienstleistungen in kürzerer Zeit direkt an die Haustür zu liefern. Die wachsende Nachfrage nach Gesundheitsdienstleistungen auf dem Markt ist der Hauptgrund für den Wettbewerb zwischen den führenden Gesundheits- und Pharmaunternehmen bei der Verbesserung der Laborautomatisierung weltweit. Daher wird erwartet, dass die strategischen Initiativen der Marktteilnehmer eine Chance für das Wachstum des Laborautomatisierungsmarktes darstellen.

-

Anstieg der Zahl der Pharmaunternehmen

Die Pharmaindustrie hat in den letzten zwei Jahrzehnten ein starkes Wachstum erlebt. Steigende verfügbare Einkommen, verbesserter Zugang zu Gesundheitseinrichtungen, wachsendes Gesundheitsbewusstsein in der Bevölkerung und eine zunehmende Verbreitung medizinischer Dienstleistungen führen dazu, dass die Zahl der Pharmaunternehmen steigt, um die Nachfrage zu decken.

Die COVID-19-Pandemie hatte große Auswirkungen auf die Pharmaindustrie, da die Nachfrage nach medizinischen Dienstleistungen und Medikamentenlieferungen gestiegen ist. Die Pharmaindustrie wächst weltweit schnell, um die hohe Nachfrage der Menschheit zu decken, und daher müssen die Dienstleistungen so schnell wie möglich erbracht werden. Um also eine fehlerfreie, schnelle Versorgung moderner Gesundheitseinrichtungen in kürzerer Zeit zu erreichen, ist eine Laborautomatisierung erforderlich. Daher wird erwartet, dass der Anstieg der Zahl der Pharmaunternehmen eine Chance für das Wachstum des Marktes für Laborautomatisierung darstellt.

Einschränkungen/Herausforderungen

- Einschränkung bei der Analyse neuartiger komplexer Produkte

Es gibt verschiedene Faktoren, die zur Komplexität neuartiger Produkte beitragen, die in automatisierten Laboren verwendet werden. Die kontinuierliche Zusammenarbeit zwischen Mitarbeitern und Geräteherstellern zu Beginn des Entwicklungsprozesses ist dringend erforderlich und wird zum Verständnis zwingend erforderlich, um das Teil oder das Gesamtsystem zu betreiben. Einschränkungen bei der Erkennung und Analyse neuartiger komplexer Produkte wie Maschinen, Werkzeuge und Geräte erschweren die Installation und den Betrieb automatisierter Labore auf dem Markt.

- Hohe Kosten für Installation und Einrichtung

Die Installation und Einrichtung von Laborautomatisierungssystemen sind wesentlich arbeitsintensivere und komplexere Verfahren. Die Einrichtung automatisierter Labors erfordert viel Zeit, Aufwand, Planung, Umsetzung und Genehmigungen verschiedener Regierungsbehörden. Darüber hinaus ist für die Einrichtung eines neuen Labors aufgrund der hohen Kosten für moderne Maschinen, Werkzeuge und Geräte eine erhebliche Investition in die Infrastruktur erforderlich.

- Upgrade, Wartung und regelmäßige Überprüfungen

Nach der Einrichtung ist der effiziente Betrieb von Laboren das Hauptanliegen. Für den Betrieb sind Wartung, Aufrüstung und regelmäßige Überprüfung der Geräte erforderlich. Die dafür erforderlichen Kosten sind einer der Haupthemmfaktoren für die Marktteilnehmer. Die Laborinhaber sind durch Vorschriften oder Qualitätskontrollen verpflichtet, ihre Produkte unabhängig von den Herstellerfirmen zu testen, um einen reibungslosen Betrieb zu gewährleisten und Umstände zu vermeiden. Dies kann das Marktwachstum hemmen.

Auswirkungen von COVID-19 auf den europäischen Markt für Laborautomatisierung

COVID-19 hat sich positiv auf den Automatisierungsmarkt ausgewirkt. Aufgrund der Pandemie wurde die Gesundheit der Menschen beeinträchtigt, wodurch viele Diagnosetests durchgeführt wurden und die Nachfrage stieg. Private Labore, Krankenhäuser und klinische Forschung nahmen aufgrund der Pandemie zu. Somit hat COVID-19 den Markt für Laborautomatisierung positiv beeinflusst.

Jüngste Entwicklungen

- Im Juni 2022 gab BD bekannt, dass die Übernahme der Straub Medical AG, eines Privatunternehmens, abgeschlossen wurde. Mit dieser Übernahme hat das Unternehmen das wertvolle Know-how und die Erfahrung der Straub Medical AG hinzugefügt und sein Produktportfolio erweitert

- Im Januar 2022 gab QIAGEN bekannt, dass es neue Kooperationen mit Atlia Biosystems eingegangen ist, um nicht-invasive pränatale Testlösungen anzubieten.

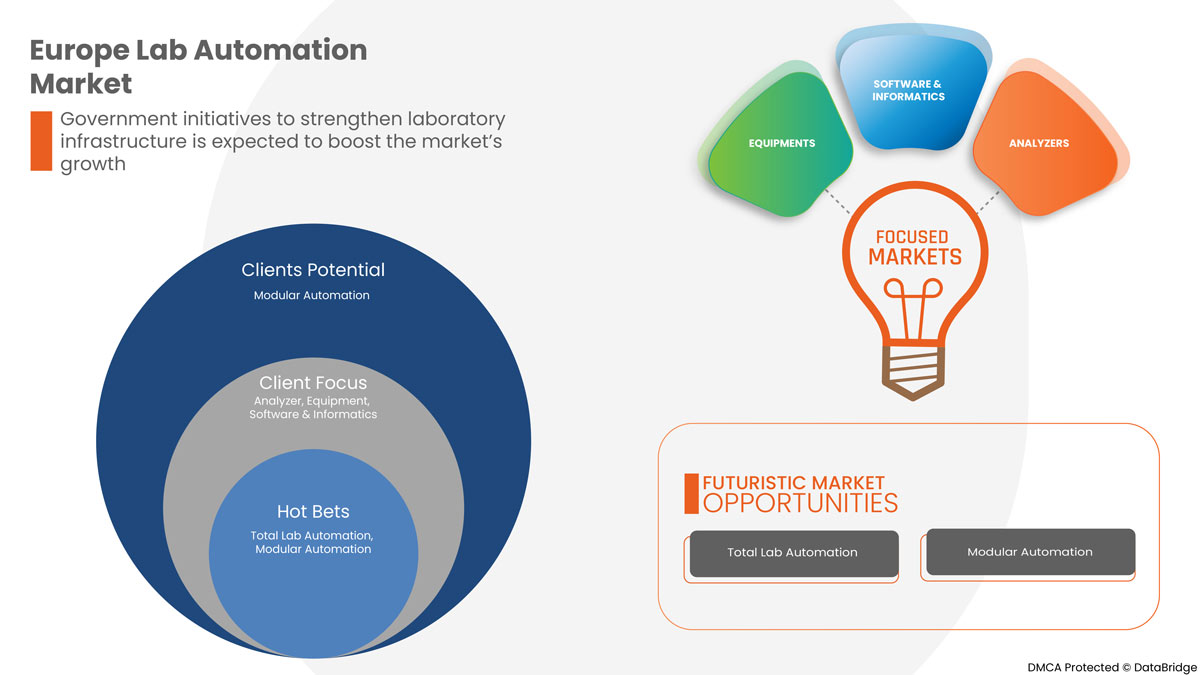

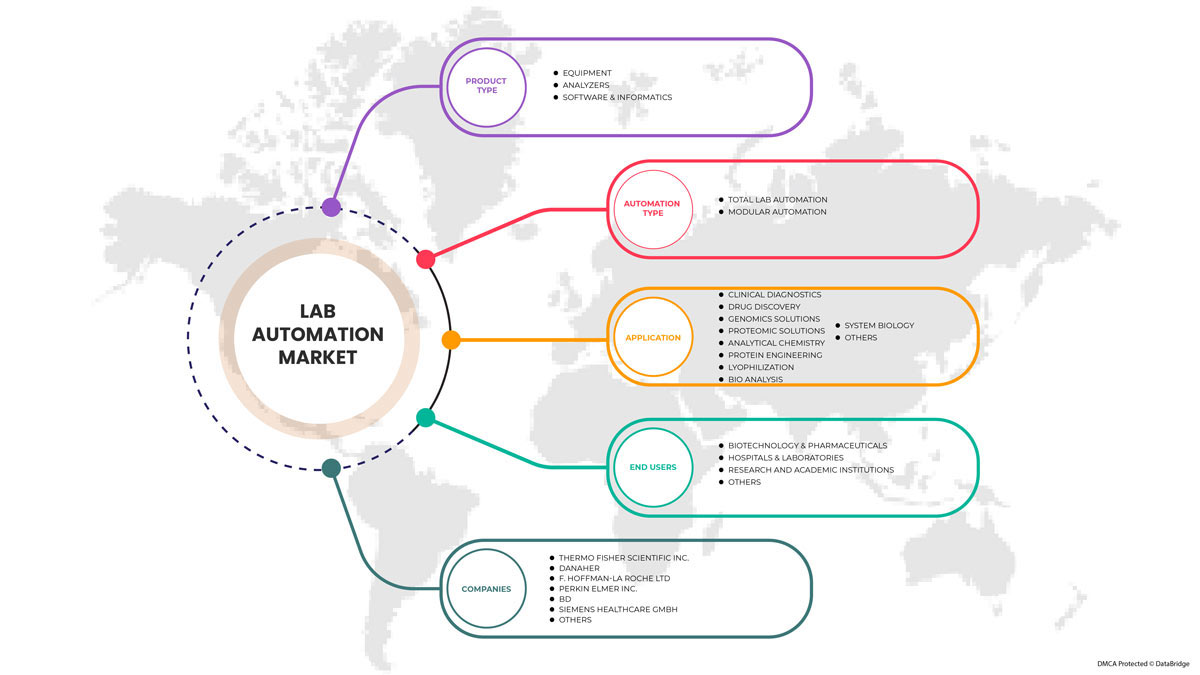

Marktumfang für Laborautomatisierung in Europa

Der europäische Markt für Laborautomatisierung ist in Produkttyp, automatisierte Systeme, Anwendung und Endbenutzer unterteilt. Das Wachstum dieser Segmente hilft Ihnen bei der Analyse schwacher Wachstumssegmente in den Branchen und bietet den Benutzern einen wertvollen Marktüberblick und Markteinblicke, um strategische Entscheidungen zur Identifizierung der wichtigsten Marktanwendungen zu treffen.

Produkttyp

- Ausrüstung

- Analysator

- Software & Informatik

Basierend auf dem Produkttyp ist der Markt für Laborautomatisierung in Geräte, Analysatoren sowie Software und Informatik segmentiert.

Automatisierte Systeme

- Vollständige Laborautomatisierung

- Modulare Laborautomatisierung

Basierend auf automatisierten Systemen ist der Markt für Laborautomatisierung in die Bereiche Gesamtlaborautomatisierung und modulare Laborautomatisierung segmentiert.

Anwendung

- Klinische Diagnostik

- Arzneimittelforschung

- Genomik-Lösungen

- Proteomische Lösungen

- Analytische Chemie

- Protein-Engineering

- Gefriertrocknung

- Bioanalyse

- Systembiologie

- Sonstiges

Basierend auf der Anwendung ist der Markt für Laborautomatisierung in Arzneimittelforschung, klinische Diagnostik, genomische Lösungen, proteomische Lösungen, Bioanalyse, Protein-Engineering, Gefriertrocknung, Systembiologie, analytische Chemie und andere unterteilt.

Endbenutzer

- Biotechnologie und Pharmazeutik

- Krankenhäuser und Labore

- Forschungs- und akademische Institute

- Sonstiges

Basierend auf dem Endbenutzer ist der Markt für Laborautomatisierung in die Bereiche Biotechnologie und Pharmazie, Krankenhäuser und Labore, Forschungs- und akademische Einrichtungen und andere unterteilt.

Regionale Analyse/Einblicke zum europäischen Markt für Laborautomatisierung

Der europäische Markt für Laborautomatisierung wird analysiert und es werden Einblicke in die Marktgröße und Trends nach Land, Produkttyp, automatisierten Systemen, Anwendung und Endbenutzer bereitgestellt.

Die vom Markt abgedeckten Länder sind Deutschland, Frankreich, Großbritannien, Italien, Spanien, die Niederlande, Russland, Belgien, die Schweiz, die Türkei und das übrige Europa. Es wird erwartet, dass Deutschland den europäischen Markt für Laborautomatisierung dominieren wird, da die Nachfrage nach Geräten, Analysegeräten und Software auf dem regionalen Markt steigt.

Der regionale Abschnitt des Berichts enthält auch Angaben zu einzelnen marktbeeinflussenden Faktoren und Änderungen der Marktvorschriften, die sich auf die aktuellen und zukünftigen Markttrends auswirken. Datenpunkte wie Neu- und Ersatzverkäufe, demografische Daten des Landes, Krankheitsepidemiologie und Import- und Exportzölle sind einige der wichtigsten Anhaltspunkte, die zur Prognose des Marktszenarios für einzelne Länder verwendet werden. Darüber hinaus werden bei der Prognoseanalyse der Länderdaten die Präsenz und Verfügbarkeit zentralamerikanischer Marken und ihre Herausforderungen aufgrund der hohen Konkurrenz durch lokale und inländische Marken sowie die Auswirkungen der Vertriebskanäle berücksichtigt.

Wettbewerbsumfeld und Laborautomatisierung Marktanteilsanalyse

Die Wettbewerbslandschaft des europäischen Marktes für Laborautomatisierung liefert Einzelheiten zu den Wettbewerbern. Zu den enthaltenen Einzelheiten gehören Unternehmensübersicht, Unternehmensfinanzen, erzielter Umsatz, Marktpotenzial, Investitionen in Forschung und Entwicklung, neue Marktinitiativen, Präsenz in Europa, Produktionsstandorte und -anlagen, Produktionskapazitäten, Stärken und Schwächen des Unternehmens, Produkteinführung, Produktbreite und -umfang und Anwendungsdominanz. Die oben angegebenen Datenpunkte beziehen sich nur auf den Fokus der Unternehmen auf den europäischen Markt für Laborautomatisierung.

Zu den wichtigsten Akteuren auf dem europäischen Markt für Laborautomatisierung zählen unter anderem QIAGEN, Siemens Healthcare, F. Hoffman Roche, Hamilton Company, Hudson Robotics, LabVantage Solutions Inc., Abbott, BD, BIOMERIEUX, Aurora Biomed Inc., Danaher, Tecan Trading AG, PerkinElmer Inc, Thermo Fisher Scientific, Agilent Technologies, Azenta US Inc, Eppendorf SE und Labware.

Forschungsmethodik

Die Datenerfassung und die Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Die wichtigste Forschungsmethode, die das DBMR-Forschungsteam verwendet, ist die Datentriangulation, die Data Mining, Analyse der Auswirkungen von Datenvariablen auf den Markt und primäre (Branchenexperten-)Validierung umfasst. Abgesehen davon umfassen die Datenmodelle ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, einen Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Firmenmarktanteilsanalyse, Messstandards, Europa vs. Region und Lieferantenanteilsanalyse. Bitte fordern Sie bei weiteren Fragen einen Analystenanruf an.

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Inhaltsverzeichnis

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE EUROPE LAB AUTOMATION MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRODUCT TYPE LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.2 PORTER’S FIVE FORCES

5 REGULATION

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 INCREASING INVESTMENT & STRATEGIC INITIATIVES BY MARKET PLAYERS

6.1.2 GOVERNMENT INITIATIVES TO STRENGTHEN LABORATORY INFRASTRUCTURES

6.1.3 GROWING EXPENDITURE ON LAB AUTOMATION TOOLS AND EQUIPMENT

6.1.4 REDUCING HUMAN EFFORTS AND ELIMINATING HUMAN ERROR

6.2 RESTRAINTS

6.2.1 LIMITATION ANALYZING NOVEL COMPLEX PRODUCT

6.2.2 HIGH COST FOR INSTALLATION AND SETUP

6.2.3 UPGRADATION, MAINTENANCE, AND PERIODICAL CHECKUPS

6.3 OPPORTUNITIES

6.3.1 RISING HEALTHCARE EXPENDITURE

6.3.2 STRATEGIC INITIATIVES BY KEY PLAYERS

6.3.3 RISE IN THE NUMBER OF PHARMA COMPANIES

6.4 CHALLENGES

6.4.1 SLOW ADOPTION OF AUTOMATION AMONG SMALL AND MEDIUM SIZED LABORATORIES

6.4.2 LIMITED FEASIBILITY WITH TECHNOLOGY INTEGRATION IN ANALYTICAL LABS

7 EUROPE LAB AUTOMATION MARKET, BY PRODUCT TYPE

7.1 OVERVIEW

7.2 EQUIPMENT

7.2.1 AUTOMATED WORKSTATIONS

7.2.1.1 AUTOMATED LIQUID HANDLING SYSTEMS

7.2.1.2 AUTOMATED INTEGRATED WORKSTATIONS

7.2.1.3 PIPETTING SYSTEMS

7.2.1.4 MICROPLATE WASHERS

7.2.1.5 REAGENT DISPENSERS

7.2.2 MICROPLATE READERS

7.2.2.1 MULTI-MODE MICROPLATE READERS

7.2.2.2 SINGLE-MODE MICROPLATE READERS

7.2.2.3 AUTOMATED NUCLEIC ACID PURIFICATION SYSTEMS

7.2.2.4 AUTOMATED ELISA SYSTEMS

7.2.3 OFF-THE-SHELF AUTOMATED WORKCELLS

7.2.4 ROBOTIC SYSTEMS

7.2.4.1 ROBOTIC ARMS

7.2.4.2 TRACK ROBOTS

7.2.5 AUTOMATE STORAGE & RETRIEVALS (ASRS)

7.2.6 OTHERS

7.3 ANALYZER

7.3.1 BIO CHEMISTRY ANALYZERS

7.3.2 HAEMATOLOGY ANALYZERS

7.3.3 IMMUNO-BASED ANALYZERS

7.4 SOFTWARE & INFORMATICS

7.4.1 LABORATORY INFORMATION MANAGEMENT SYSTEM (LIMS)

7.4.2 ELECTRONIC LABORATORY NOTEBOOK (ELN)

7.4.3 LABORATORY EXECUTION SYSTEMS (LES)

7.4.4 SCIENTIFIC DATA MANAGEMENT SYSTEMS (SDMS)

8 EUROPE LAB AUTOMATION MARKET, BY AUTOMATION TYPE

8.1 OVERVIEW

8.2 TOTAL LAB AUTOMATION

8.3 MODULAR AUTOMATION

9 EUROPE LAB AUTOMATION MARKET, BY APPLICATION

9.1 OVERVIEW

9.2 CLINICAL DIAGNOSTICS

9.3 DRUG DISCOVERY

9.4 GENOMICS SOLUTIONS

9.5 PROTEOMIC SOLUTIONS

9.6 ANALYTICAL CHEMISTRY

9.7 PROTEIN ENGINEERING

9.8 BIO ANALYSIS

9.9 SYSTEM BIOLOGY

9.1 OTHERS

10 EUROPE LAB AUTOMATION MARKET, BY END USER

10.1 OVERVIEW

10.2 BIOTECHNOLOGY & PHARMACEUTICALS

10.3 HOSPITALS & LABORATORIES

10.4 RESEARCH & ACADEMIC INSTITUTES

10.5 OTHERS

11 EUROPE LAB AUTOMATION MARKET, BY REGION

11.1 EUROPE

11.1.1 GERMANY

11.1.2 FRANCE

11.1.3 U.K.

11.1.4 ITALY

11.1.5 RUSSIA

11.1.6 SPAIN

11.1.7 NETHERLANDS

11.1.8 SWITZERLAND

11.1.9 TURKEY

11.1.10 BELGIUM

11.1.11 REST OF EUROPE

12 EUROPE LAB AUTOMATION MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: EUROPE

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 THERMO FISHER SCIENTIFIC INC.

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENTS

14.2 DANAHER

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENTS

14.3 F. HOFFMANN- LA ROCHE LTD

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENTS

14.4 PERKINELMER INC

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENTS

14.5 BD

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT PORTFOLIO

14.5.5 RECENT DEVELOPMENTS

14.6 ABBOTT

14.6.1 COMPANY SNAPSHOT

14.6.2 REVENUE ANALYSIS

14.6.3 PRODUCT PORTFOLIO

14.6.3 RECENT DEVELOPMENTS

14.7 AGILENT TECHNOLOGIES

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCT PORTFOLIO

14.7.4 RECENT DEVELOPMENTS

14.8 AURORA BIOMED INC.

14.8.1 COMPANY SNAPSHOT

14.8.2 PRODUCT PORTFOLIO

14.8.3 RECENT DEVELOPMENTS

14.9 AZENTA US INC

14.9.1 COMPANY SNAPSHOT

14.9.2 REVENUE ANALYSIS

14.9.3 PRODUCT PORTFOLIO

14.9.4 RECENT DEVELOPMENTS

14.1 BIOMERIEUX

14.10.1 COMPANY SNAPSHOT

14.10.2 REVENUE ANALYSIS

14.10.3 PRODUCT PORTFOLIO

14.10.4 RECENT DEVELOPMENTS

14.11 EPPENDORF SE

14.11.1 COMPANY SNAPSHOT

14.11.2 PRODUCT PORTFOLIO

14.11.3 RECENT DEVELOPMENTS

14.12 HAMILTON COMPANY

14.12.1 COMPANY SNAPSHOT

14.12.2 PRODUCT PORTFOLIO

14.12.3 RECENT DEVELOPMENTS

14.13 HUDSON ROBOTICS

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCT PORTFOLIO

14.13.3 RECENT DEVELOPMENTS

14.14 LABLYNX LIMS

14.14.1 COMPANY SNAPSHOT

14.14.2 PRODUCT PORTFOLIO

14.14.3 RECENT DEVELOPMENTS

14.15 LABVANTAGE SOLUTIONS INC.

14.15.1 COMPANY SNAPSHOT

14.15.2 PRODUCT PORTFOLIO

14.15.3 RECENT DEVELOPMENTS

14.16 LABWARE

14.16.1 COMPANY SNAPSHOT

14.16.2 PRODUCT PORTFOLIO

14.16.3 RECENT DEVELOPMENTS

14.17 QIAGEN

14.17.1 COMPANY SNAPSHOT

14.17.2 REVENUE ANALYSIS

14.17.3 PRODUCT PORTFOLIO

14.17.4 RECENT DEVELOPMENTS

14.18 SIEMENS HEALTHCARE GMBH

14.18.1 COMPANY SNAPSHOT

14.18.2 REVENUE ANALYSIS

14.18.3 PRODUCT PORTFOLIO

14.18.4 RECENT DEVELOPMENTS

14.19 TECAN TRADING AG

14.19.1 COMPANY SNAPSHOT

14.19.2 REVENUE ANALYSIS

14.19.3 PRODUCT PORTFOLIO

14.19.4 RECENT DEVELOPMENTS

15 QUESTIONNAIRE

16 RELATED REPORTS

Tabellenverzeichnis

TABLE 1 EUROPE LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 2 EUROPE EQUIPMENT IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 3 EUROPE AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 4 EUROPE MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 5 EUROPE ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 6 EUROPE ANALYZER IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 7 EUROPE ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 8 EUROPE SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 9 EUROPE SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 10 EUROPE LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 11 EUROPE TOTAL LAB AUTOMATION IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 12 EUROPE MODULAR AUTOMATION IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 13 EUROPE LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 14 EUROPE CLINICAL DIAGNOSTICS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 15 EUROPE DRUG DISCOVERY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 16 EUROPE GENOMICS SOLUTIONS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 17 EUROPE PROTEOMIC SOLUTIONS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 18 EUROPE ANALYTICAL CHEMISTRY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 19 EUROPE PROTEIN ENGINEERING IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 20 EUROPE BIO ANALYSIS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 21 EUROPE SYSTEM BIOLOGY IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 22 EUROPE OTHERS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 23 EUROPE LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 24 EUROPE BIOTECHNOLOGY & PHARMACEUTICALS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 25 EUROPE HOSPITALS & LABORATORIES IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 26 EUROPE RESEARCH & ACADEMIC INSTITUTES IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 27 EUROPE OTHERS IN LAB AUTOMATION MARKET, BY REGION, 2020-2029 (USD MILLION)

TABLE 28 EUROPE LAB AUTOMATION MARKET, BY COUNTRY, 2020-2029 (USD MILLION)

TABLE 29 EUROPE LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 30 EUROPE EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 31 EUROPE AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 32 EUROPE MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 33 EUROPE ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 34 EUROPE ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 35 EUROPE SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 36 EUROPE LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 37 EUROPE LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 38 EUROPE LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 39 GERMANY LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 40 GERMANY EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 41 GERMANY AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 42 GERMANY MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 43 GERMANY ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 44 GERMANY ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 45 GERMANY SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 46 GERMANY LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 47 GERMANY LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 48 GERMANY LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 49 FRANCE LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 50 FRANCE EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 51 FRANCE AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 52 FRANCE MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 53 FRANCE ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 54 FRANCE ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 55 FRANCE SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 56 FRANCE LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 57 FRANCE LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 58 FRANCE LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 59 U.K. LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 60 U.K. EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 61 U.K. AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 62 U.K. MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 63 U.K. ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 64 U.K. ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 65 U.K. SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 66 U.K. LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 67 U.K. LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 68 U.K. LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 69 ITALY LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 70 ITALY EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 71 ITALY AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 72 ITALY MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 73 ITALY ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 74 ITALY ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 75 ITALY SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 76 ITALY LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 77 ITALY LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 78 ITALY LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 79 RUSSIA LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 80 RUSSIA EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 81 RUSSIA AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 82 RUSSIA MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 83 RUSSIA ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 84 RUSSIA ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 85 RUSSIA SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 86 RUSSIA LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 87 RUSSIA LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 88 RUSSIA LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 89 SPAIN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 90 SPAIN EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 91 SPAIN AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 92 SPAIN MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 93 SPAIN ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 94 SPAIN ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 95 SPAIN SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 96 SPAIN LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 97 SPAIN LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 98 SPAIN LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 99 NETHERLANDS LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 100 NETHERLANDS EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 101 NETHERLANDS AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 102 NETHERLANDS MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 103 NETHERLANDS ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 104 NETHERLANDS ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 105 NETHERLANDS SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 106 NETHERLANDS LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 107 NETHERLANDS LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 108 NETHERLANDS LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 109 SWITZERLAND LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 110 SWITZERLAND EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 111 SWITZERLAND AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 112 SWITZERLAND MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 113 SWITZERLAND ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 114 SWITZERLAND ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 115 SWITZERLAND SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 116 SWITZERLAND LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 117 SWITZERLAND LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 118 SWITZERLAND LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 119 TURKEY LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 120 TURKEY EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 121 TURKEY AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 122 TURKEY MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 123 TURKEY ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 124 TURKEY ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 125 TURKEY SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 126 TURKEY LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 127 TURKEY LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 128 TURKEY LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 129 BELGIUM LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 130 BELGIUM EQUIPMENT IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 131 BELGIUM AUTOMATED WORKSTATIONS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 132 BELGIUM MICROPLATE READERS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 133 BELGIUM ROBOTIC SYSTEMS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 134 BELGIUM ANALYZER IN LAB AUTOMATION MARKET, BY PRODUCT TYPE , 2020-2029 (USD MILLION)

TABLE 135 BELGIUM SOFTWARE & INFORMATICS IN LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

TABLE 136 BELGIUM LAB AUTOMATION MARKET, BY AUTOMATION TYPE, 2020-2029 (USD MILLION)

TABLE 137 BELGIUM LAB AUTOMATION MARKET, BY APPLICATION, 2020-2029 (USD MILLION)

TABLE 138 BELGIUM LAB AUTOMATION MARKET, BY END USER, 2020-2029 (USD MILLION)

TABLE 139 REST OF EUROPE LAB AUTOMATION MARKET, BY PRODUCT TYPE, 2020-2029 (USD MILLION)

Abbildungsverzeichnis

FIGURE 1 EUROPE LAB AUTOMATION MARKET: SEGMENTATION

FIGURE 2 EUROPE LAB AUTOMATION MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE LAB AUTOMATION MARKET: DROC ANALYSIS

FIGURE 4 EUROPE LAB AUTOMATION MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE LAB AUTOMATION MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE LAB AUTOMATION MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE LAB AUTOMATION MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE LAB AUTOMATION MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 EUROPE LAB AUTOMATION MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 EUROPE LAB AUTOMATION MARKET: SEGMENTATION

FIGURE 11 GROWING EXPENDITURE ON LAB AUTOMATION TOOLS AND EQUIPMENT IS EXPECTED TO DRIVE THE EUROPE LAB AUTOMATION MARKET GROWTH IN THE FORECAST PERIOD OF 2022 TO 2029

FIGURE 12 EQUIPMENT SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE LAB AUTOMATION MARKET IN 2022 & 2029

FIGURE 13 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE EUROPE LAB AUTOMATION MARKET

FIGURE 14 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE, 2021

FIGURE 15 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE, 2022-2029 (USD MILLION)

FIGURE 16 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE, CAGR (2022-2029)

FIGURE 17 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE, LIFELINE CURVE

FIGURE 18 EUROPE LAB AUTOMATION MARKET: BY AUTOMATION TYPE, 2021

FIGURE 19 EUROPE LAB AUTOMATION MARKET: BY AUTOMATION TYPE, 2022-2029 (USD MILLION)

FIGURE 20 EUROPE LAB AUTOMATION MARKET: BY AUTOMATION TYPE, CAGR (2022-2029)

FIGURE 21 EUROPE LAB AUTOMATION MARKET: BY AUTOMATION TYPE, LIFELINE CURVE

FIGURE 22 EUROPE LAB AUTOMATION MARKET: BY APPLICATION, 2021

FIGURE 23 EUROPE LAB AUTOMATION MARKET: BY APPLICATION, 2022-2029 (USD MILLION)

FIGURE 24 EUROPE LAB AUTOMATION MARKET: BY APPLICATION, CAGR (2022-2029)

FIGURE 25 EUROPE LAB AUTOMATION MARKET: BY APPLICATION, LIFELINE CURVE

FIGURE 26 EUROPE LAB AUTOMATION MARKET: BY END USER, 2021

FIGURE 27 EUROPE LAB AUTOMATION MARKET: BY END USER, 2022-2029 (USD MILLION)

FIGURE 28 EUROPE LAB AUTOMATION MARKET: BY END USER, CAGR (2022-2029)

FIGURE 29 EUROPE LAB AUTOMATION MARKET: BY END USER, LIFELINE CURVE

FIGURE 30 EUROPE LAB AUTOMATION MARKET: SNAPSHOT (2021)

FIGURE 31 EUROPE LAB AUTOMATION MARKET: BY COUNTRY (2021)

FIGURE 32 EUROPE LAB AUTOMATION MARKET: BY COUNTRY (2022 & 2029)

FIGURE 33 EUROPE LAB AUTOMATION MARKET: BY COUNTRY (2021 & 2029)

FIGURE 34 EUROPE LAB AUTOMATION MARKET: BY PRODUCT TYPE (2022-2029)

FIGURE 35 EUROPE LAB AUTOMATION MARKET: COMPANY SHARE 2021 (%)

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.