سوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا، حسب نوع الوقود (الوقود الحيوي، وقود الهيدروجين، والطاقة إلى وقود سائل)، تكنولوجيا التصنيع (إسترات الأحماض الدهنية المعالجة بالهيدروجين والأحماض الدهنية - الكيروسين البارافيني الاصطناعي (HEFA-SPK)، الكيروسين البارافيني الاصطناعي من فيشر تروبش (FT-SPK)، البارافين الاصطناعي ISO من السكر المعالج بالهيدروجين المخمر (HFS-SIP)، الكيروسين البارافيني الاصطناعي من فيشر تروبش (FT) مع العطريات (FT-SPK / A)، الكحول إلى Jet SPK (ATJ-SPK) و Jet التحلل الحراري المائي التحفيزي (CHJ))، قدرة المزج (أقل من 30٪، 30٪ إلى 50٪ وفوق 50٪)، منصة المزج (الطيران التجاري، الطيران العسكري، الطيران التجاري والعام، والمركبات الجوية بدون طيار) اتجاهات الصناعة والتوقعات حتى عام 2029.

تحليل وحجم سوق الوقود المستدام للطيران في الشرق الأوسط وأفريقيا

تحرص صناعة الطيران على تقليل البصمة الكربونية لتحقيق بيئة مستدامة وتلبية المعايير التنظيمية الصارمة للانبعاثات. يتم اعتماد حلول بديلة، مثل تحسين كفاءة محركات الطائرات من خلال تعديلات التصميم، والطائرات الكهربائية الهجينة والكهربائية بالكامل، ووقود الطائرات المتجدد، وما إلى ذلك، من قبل مختلف أصحاب المصلحة في صناعة الطيران. ومع ذلك، من بين هذه الحلول، فإن اعتماد وقود الطائرات المستدام مثل الوقود الإلكتروني والوقود الاصطناعي ووقود الطائرات الأخضر ووقود الطائرات الحيوي ووقود الهيدروجين هو أحد أكثر الحلول البديلة جدوى فيما يتعلق بالفوائد الاجتماعية والاقتصادية مقارنة بالآخرين، مما يساهم بشكل كبير في التخفيف من التأثيرات البيئية الحالية والمتوقعة في المستقبل للطيران.

تشكل الوقود المستدام للطائرات عنصراً أساسياً في الوفاء بالتزامات صناعة الطيران بفصل الزيادة في انبعاثات الكربون عن نمو حركة المرور. وتساهم عوامل مثل زيادة عدد ركاب الطائرات، ونمو الدخل المتاح، وزيادة النقل الجوي، وزيادة استهلاك مواد التشحيم الاصطناعية في تعزيز نمو سوق الوقود المستدام للطائرات في الشرق الأوسط وأفريقيا. ومع ذلك، فإن الافتقار إلى البنية الأساسية يعمل كعامل مقيد للسوق.

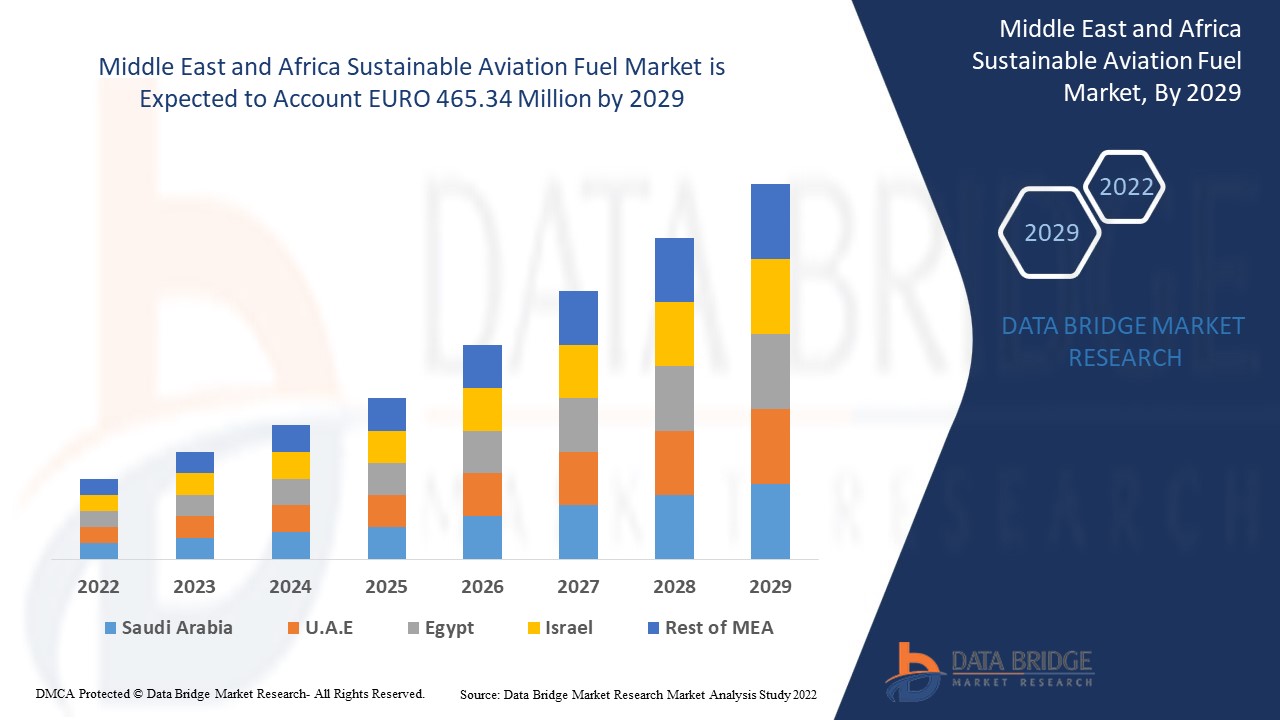

تحلل شركة Data Bridge Market Research أن سوق وقود الطيران المستدام من المتوقع أن تصل قيمته إلى 465.34 مليون يورو بحلول عام 2029، بمعدل نمو سنوي مركب يبلغ 40.7% خلال الفترة المتوقعة. يشكل "الوقود الحيوي" أكبر شريحة تقنية في سوق وقود الطيران المستدام بسبب زيادة استهلاك النقل الجوي للزيوت الاصطناعية. يغطي تقرير سوق وقود الطيران المستدام أيضًا تحليل الأسعار وتحليل براءات الاختراع والتقدم التكنولوجي بعمق.

|

تقرير القياس |

تفاصيل |

|

فترة التنبؤ |

2022 إلى 2029 |

|

سنة الأساس |

2021 |

|

سنوات تاريخية |

2020 |

|

وحدات كمية |

الإيرادات بمليون يورو، الأحجام بالوحدات، التسعير باليورو |

|

القطاعات المغطاة |

حسب نوع الوقود (الوقود الحيوي ووقود الهيدروجين والطاقة إلى وقود سائل)، حسب تكنولوجيا التصنيع (إسترات الأحماض الدهنية المعالجة بالهيدروجين والأحماض الدهنية - الكيروسين البارافيني الصناعي (Hefa-Spk)، الكيروسين البارافيني الصناعي من فيشر تروبش (FT-SPK)، إيزوبارافين صناعي من سكر معالج بالهيدروجين المخمر (Hfs-Sip)، الكيروسين البارافيني الصناعي من فيشر تروبش (Ft) مع المواد العطرية (FT-SPK/A)، الكحول إلى جيت سبي (ATJ-SPK) وجيت التحلل الحراري المائي التحفيزي (CHJ))، حسب سعة المزج (أقل من 30%، 30% إلى 50% وأعلى من 50%)، حسب منصة المزج (الطيران التجاري، الطيران العسكري، الطيران التجاري والعام، والطائرات بدون طيار) |

|

الدول المغطاة |

جنوب أفريقيا والمملكة العربية السعودية والإمارات العربية المتحدة وإسرائيل ومصر وبقية دول الشرق الأوسط وأفريقيا في الشرق الأوسط وأفريقيا، |

|

الجهات الفاعلة في السوق المشمولة |

Neste، Gevo، VELOCYS، Fulcrum BioEnergy، SkyNRG، Prometheus Fuels، World Energy، Avfuel Corporation، LanzaTech، Preem AB، Eni، Sasol Ltd، BP plc وغيرها. |

تعريف السوق

الوقود المستدام للطائرات هو شكل فريد من أشكال الوقود المصمم للاستخدام في الطائرات وفي نفس الوقت يزيد من أداء الطائرات. يتم استخلاص الوقود المستدام للطائرات من مواد خام مستدامة ويمكن مقارنته في تركيبته الكيميائية بالوقود الأحفوري القياسي للطائرات. يؤدي زيادة فائدة الوقود المستدام للطائرات إلى انخفاض انبعاثات الكربون مقارنة بالوقود النفاث التقليدي لأنه يحل محل دورة حياة الوقود.

إن شركات الطيران على استعداد لتقليص البصمة الكربونية للحصول على بيئة مستدامة وتلبية المتطلبات التنظيمية الصارمة للانبعاثات. علاوة على ذلك، فإن تعزيز أداء محركات الطائرات من خلال تعديلات التصميم والطائرات الهجينة الكهربائية والكهربائية بالكامل ووقود الطائرات المتجدد، يتم تبنيها من قبل العديد من أصحاب المصلحة في صناعة الطيران، ومع ذلك فإن اعتماد وقود الطيران المستدام يعتبر من أكثر الحلول الموثوقة والقابلة للتطبيق فيما يتعلق بالمزايا الاجتماعية والاقتصادية مقارنة بالآخرين، مما يساهم بشكل كبير في التخفيف من التأثيرات البيئية الحديثة والمتوقعة في المستقبل للطيران.

ديناميكيات سوق وقود الطيران المستدام

يتناول هذا القسم فهم محركات السوق والمزايا والفرص والقيود والتحديات. ويتم مناقشة كل هذا بالتفصيل على النحو التالي:

- الحاجة المتزايدة إلى الحد من انبعاثات غازات الاحتباس الحراري في صناعة الطيران

إن انبعاثات الغازات المسببة للاحتباس الحراري الناتجة عن الأنشطة البشرية تعمل على تضخيم تأثير الاحتباس الحراري، مما يتسبب في تغير المناخ. ينبعث ثاني أكسيد الكربون في المقام الأول من خلال احتراق الوقود الأحفوري مثل الفحم والنفط والغاز الطبيعي. تعد الصين وروسيا من أكبر الدول الملوثة في الشرق الأوسط وأفريقيا. يحدث هذا التلوث في الغالب بسبب شركات الفحم والنفط والغاز المملوكة لمنظمة أوبك. لقد زادت مستويات ثاني أكسيد الكربون في الغلاف الجوي بنحو 50٪ عن أوقات ما قبل الصناعة بسبب الانبعاثات الناجمة عن الأنشطة البشرية.

إن الملوثات المنبعثة من محركات الطائرات تعادل تلك المنبعثة من احتراق الوقود الأحفوري. وعلى ارتفاعات أعلى، تكون انبعاثات الطائرات أكثر تركيزًا من الملوثات. وتخلق هذه الانبعاثات مشاكل بيئية خطيرة، سواء من حيث تأثيرها على الشرق الأوسط وأفريقيا أو تأثيرها على جودة الهواء المحلي.

- زيادة النقل الجوي وزيادة استهلاك زيوت التشحيم الاصطناعية

إن السفر الجوي يشكل عنصراً بالغ الأهمية في تحقيق النمو الاقتصادي والتنمية. وعلى المستوى الوطني والإقليمي والعالمي، يعزز السفر الجوي التكامل مع اقتصاد الشرق الأوسط وأفريقيا ويوفر روابط حيوية. كما يساهم في نمو التجارة والسياحة وفرص العمل. إن نظام الطيران يتطور وسوف يستمر في التطور. ومع ذلك، ففي الأمد البعيد، سيكون من الصعب على نظام النقل الجوي التكيف بسرعة كافية لتلبية الاحتياجات المتغيرة من حيث القدرة والتأثير البيئي وسعادة المستهلك والسلامة والأمن، كل ذلك مع الحفاظ على الجدوى الاقتصادية لمقدمي الخدمات.

لقد أدى جائحة كوفيد-19، إلى جانب الدعم الحكومي والاكتشافات التكنولوجية، وخاصة في مجال تكنولوجيا الوقود، إلى تسريع انتقال صناعة الطيران إلى وقود الطيران المستدام. وفي حين يتزايد استخدام وقود الطيران المستدام، فإن زيوت التشحيم غير الاصطناعية آخذة في الانحدار. ومن المتوقع أن تستفيد زيوت التشحيم الاصطناعية وشبه الاصطناعية من هذا التحول لأن معظم الطائرات تستخدم زيوت تشحيم من الدرجة المتقدمة. ومن المتوقع أن يكون سوق وقود الطيران المستدام العالمي مدفوعًا بهذا العامل.

- زيادة الطلب على وقود الطيران المستدام من قبل شركات الطيران

يتبنى قطاع الطيران "إجراءات عاجلة" لتحقيق هدف المناخ العالمي، والذي يتضمن الحد من نمو السفر الجوي والتوسع السريع في استخدام الوقود المستدام للطائرات. والغرض من الوقود المستدام للطائرات هو إعادة تدوير الكربون من الكتلة الحيوية المستدامة الحالية أو الغازات إلى وقود الطائرات كبديل للوقود الأحفوري للطائرات المكرر من النفط الخام البترولي. والغرض من الوقود المستدام للطائرات هو إعادة تدوير الكربون من الكتلة الحيوية المستدامة الحالية أو الغازات إلى وقود الطائرات كبديل للوقود الأحفوري للطائرات المكرر من النفط الخام البترولي. ويلتزم قطاع الطيران ككل، وكذلك شركات الطيران الأعضاء في اتحاد النقل الجوي الدولي، بتحقيق أهداف خفض الانبعاثات العدوانية. وقد تم تسليط الضوء على الوقود المستدام للطائرات كمكون رئيسي في تحقيق هذه الأهداف. وسوف يتطلب الأمر دعمًا حكوميًا لاستخدام الوقود المستدام للطائرات لتلبية أهداف المناخ في الصناعة

وبما أن اللاعبين الرئيسيين في الصناعة يدركون الحاجة إلى وقود الطيران المستدام، فقد بدأ مزودو الخدمة في تبني العديد من بدائل وقود الطيران المستدام في العديد من شركات الطيران، وهو ما من المتوقع أن يدفع نمو وقود الطيران المستدام بشكل كبير.

- عدم كفاية توافر المواد الخام والمصافي لتلبية الطلب المستدام على إنتاج وقود الطيران

تشكل الوقود المستدام للطائرات، المصنوع من مواد خام بيولوجية، جزءًا مهمًا من الخطة الرامية إلى تقليل البصمة الكربونية للطيران. ومن الناحية الفنية، من الممكن استبدال الوقود المستدام للطائرات وخلطه بالوقود النفاث؛ والواقع أن صناعة الطيران تستخدم الوقود المستدام للطائرات منذ أكثر من عقد من الزمان. ومع ذلك، وبسبب قيود العرض والطلب، تظل مستويات الاستهلاك منخفضة للغاية.

المحاصيل الزيتية، ومحاصيل السكر، والطحالب، والزيوت المستعملة، وغيرها من الموارد البيولوجية وغير البيولوجية هي المواد الخام التي تلعب دورًا أساسيًا في سلسلة الإنتاج الكاملة للوقود البديل للطيران مثل الوقود الاصطناعي، والوقود الإلكتروني، ووقود الطائرات الحيوي. قد تتوقف الحاجة إلى وقود الطيران المستدام بسبب ندرة المواد الخام اللازمة للتصنيع. وبسبب ندرة المواد الخام اللازمة لتصنيعه، قد يتوقف الطلب على وقود الطيران المستدام. وعلاوة على ذلك، فإن القيود المفروضة على التكرير، والتي تلعب دورًا حاسمًا في الاستغلال الأمثل لهذه المواد الخام، تضيف إلى العملية الإجمالية لتصنيع وقود الطيران المستدام. كما يفرض انخفاض إمدادات الوقود ضغطًا على قدرة خلط الوقود، مما يؤدي إلى انخفاض الكفاءة.

عندما تتزايد المنافسة من قطاع البنزين على الطرق للحصول على المواد الخام التي تلبي معايير الاستدامة، يصبح توافر المواد الخام بمثابة عنق زجاجة. تشكل تكاليف المواد الخام جزءًا كبيرًا من تكلفة وقود الطائرات المستدام، ويمكن أن يتسبب تقلب الأسعار في حدوث مشكلات في العرض لمنتجي الوقود. وبالتالي، فإن زيادة رسوم الوقود من قبل شركة النقل تعيق نمو السوق إلى حد ما.

- التقلبات في أسعار النفط الخام وتلوث مواد التشحيم

إن المنافسة المتزايدة وضغوط التكلفة في الشرق الأوسط وأفريقيا تجبر الشركات وسلاسل التوريد على اكتشاف إمكانات غير مكتشفة لتوفير التكاليف. وعلى وجه الخصوص، تشكل الواجهات مع سوق النفط الخام مجالاً واعداً للتحسين. وفي بيئة الأعمال اليوم، تواجه كل منظمة بعض مخاطر التقلب في أسعار النفط الخام والسلع الأساسية للتشحيم. وفي الإنتاج، قد يعتمد المصنعون على كمية كبيرة من السلع الأساسية النفطية، ونتيجة لذلك يمكن أن يتأثروا بشكل خاص بتقلب الأسعار في المنتجات النفطية التي يشترونها بشكل مباشر وغير مباشر من خلال المكونات والتجمعات الفرعية. إن الأسواق المتقلبة وغير المستقرة في الشرق الأوسط وأفريقيا لها آثار واسعة النطاق على منظمات التصنيع. من ارتفاع تكاليف الطاقة إلى التقلبات غير المتوقعة في تكاليف تصنيع النفط الخام، تعمل العقبات غير المتوقعة على زعزعة استقرار سلاسل التوريد وتجعل من الصعب على المصنعين البقاء في الربح. ومع تزايد صعوبة تأمين إمدادات العديد من المواد الخام، فإن تقلب أسعار السلع الأساسية قد لا يكون مجرد ظاهرة مؤقتة، ويتعين على الشركات المصنعة إما استيعاب التكاليف الإضافية، أو إيجاد طرق جديدة للتخفيف من النفقات، أو تمرير زيادات الأسعار إلى العملاء الذين يترددون بالفعل في الإنفاق. وبما أن الأسعار تتأثر بتضييق أسواق العرض، فإن هذا الاتجاه لا يظهر أي مؤشر على التغيير في أي وقت قريب. وبالتالي، فإن تقلب تكلفة النفط الخام وغيره من مواد التشحيم يشكل قيداً رئيسياً على سوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا.

إن شظايا الكربون ليست صلبة أو كبيرة بالقدر الكافي لتسبب فشل المضخة. ومع ذلك، قد تكون كبيرة بالقدر الكافي لسد المرشحات أو الفوهات الصغيرة. وهناك سبب آخر للتلوث التشغيلي وهو وجود الرمال والحصى والجسيمات المعدنية في نظام التزييت. وهو ما يعمل كعامل مقيد لسوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا.

- انخفاض البصمة الكربونية بسبب انخفاض قدرة وقود الطيران المستدام

إن الوقود المستدام للطائرات يقلل من انبعاثات الكربون على مدى عمر الوقود مقارنة بالوقود النفاث التقليدي الذي يحل محله. ومن بين المواد الخام الشائعة زيت الطهي وغيره من زيوت النفايات الحيوانية أو النباتية غير النخيلية، وكذلك النفايات الصلبة من المنازل والشركات، مثل مواد التغليف والورق والمنسوجات وبقايا الطعام التي كان من الممكن التخلص منها في مكبات النفايات أو حرقها. كما تعد حطام الغابات، مثل نفايات الخشب، والمحاصيل الطاقية، مثل النباتات والطحالب سريعة النمو، مصادر محتملة أيضًا.

اعتمادًا على المواد الخام المستدامة المستخدمة، وعملية الإنتاج، وسلسلة التوريد إلى المطار، يمكن للوقود المستدام أن يقلل انبعاثات الكربون بنسبة تصل إلى 80% خلال عمر الوقود مقارنة بالوقود النفاث التقليدي الذي يحل محله.

يمكن خلط الوقود المستدام للطائرات بنسبة تصل إلى 50% مع وقود الطائرات العادي، ويخضع لنفس اختبارات الجودة التي يخضع لها وقود الطائرات التقليدي. بعد ذلك، يتم إعادة اعتماد الخليط باعتباره Jet A أو Jet A-1. ويمكن التعامل معه بنفس الطريقة التي يتم بها التعامل مع وقود الطائرات العادي، وبالتالي لا يلزم إجراء أي تغييرات على البنية الأساسية للتزويد بالوقود أو الطائرات التي ترغب في استخدام الوقود المستدام للطائرات، مما يخلق فرصة لنمو سوق وقود الطائرات المستدام في الشرق الأوسط وأفريقيا.

- تطوير زيوت التشحيم للطيران الصديقة للبيئة والآمنة

في عالم اليوم، تشهد صناعة الطيران ازدهارًا كبيرًا، مما يؤدي إلى زيادة المنافسة بين منتجي وقود الطائرات في جميع المجالات. ومن المتوقع أن يكون للمصادر البديلة الصديقة للبيئة لإنتاج وقود الطائرات على المدى الطويل تأثير مستقبلي على قطاع وقود الطائرات. لقد نما سوق وقود الطائرات المستدام بشكل كبير على مر السنين، وذلك بسبب الاتجاه المتزايد لاستخدام الوقود المتقدم في الطائرات في جميع أنحاء العالم.

كما أن زراعة محاصيل الكتلة الحيوية لإنتاج وقود الطائرات المستدام يسمح للمزارعين بكسب المزيد من المال في غير موسم الزراعة من خلال المساهمة في توفير المواد الخام لهذه الصناعة الجديدة، وفي الوقت نفسه تأمين مزايا زراعية مثل الحد من فقدان العناصر الغذائية وتحسين جودة التربة. وبالتالي، خلق فرصة لنمو سوق وقود الطائرات المستدام في الشرق الأوسط وأفريقيا.

- ارتفاع تكلفة الوقود المستدام للطيران يزيد من تكاليف تشغيل شركات الطيران

إن نفقات العمالة والوقود هما أهم النفقات التي تواجهها شركات الطيران. ففي الأمد القريب، تكون نفقات العمالة مستقرة عادة، ولكن أسعار الوقود تتقلب بشكل كبير اعتمادًا على سعر النفط. ويشكل الوقود جزءًا كبيرًا من تكلفة تشغيل شركة طيران، حيث يمثل 20-30% من إجمالي النفقات. وكانت ارتفاعات أسعار النفط من أصعب اللحظات التي مرت بها شركات الطيران. ويمكن لشركات الطيران الاستعداد للارتفاع التدريجي للأسعار من خلال رفع أسعار التذاكر أو خفض عدد الرحلات، ولكن الزيادات غير المتوقعة في الأسعار تتسبب في خسارة العديد من شركات الطيران للأموال.

ستبدأ أهداف استخدام وقود الطيران المستدام في زيادة تكلفة الوقود هذا العام، مما يجعل الأمور أكثر صعوبة بالنسبة لشركات الطيران. ووفقًا لاتحاد النقل الجوي الدولي (IATA)، فإن إنتاج وقود الطيران المستدام في الشرق الأوسط وأفريقيا يبلغ حوالي 100 مليون لتر فقط سنويًا، أو 0.1 في المائة من إجمالي وقود الطيران المستخدم. من ناحية أخرى، تعهدت شركات الطيران المختلفة بزيادة هذه النسبة إلى 10٪ بحلول عام 2030، وهو هدف نبيل حقًا.

ولكن من المؤسف أن التكلفة باهظة أيضاً بسبب حجم التصنيع المحدود. وتقدر تكلفة وقود الطائرات المستدام بما يتراوح بين ضعفي وأربعة أمثال تكلفة الوقود الأحفوري وفقاً لتقديرات اتحاد النقل الجوي الدولي، في حين أشارت إفصاحات حديثة لشركة الخطوط الجوية الفرنسية ـ كيه إل إم إلى أن الفارق في التكلفة ربما يكون أقرب إلى أربعة إلى ثمانية أمثال الفارق في تكلفة الكيروسين.

وقد حثت رابطة النقل الجوي الدولي (IATA) وغيرها من الهيئات الحكومات على تشجيع تطوير وقود الطيران المستدام، ولكن في شكل تحفيز اقتصادي. وهذا يمهد الطريق لزيادة أسعار وقود الطيران المستدام، وبالتالي يشكل تحديًا لسوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا.

تأثير ما بعد كوفيد-19 على سوق وقود الطيران المستدام

أحدثت جائحة كوفيد-19 تأثيرًا كبيرًا على سوق وقود الطيران المستدام حيث اختارت كل دولة تقريبًا إغلاق جميع مرافق الإنتاج باستثناء تلك التي تتعامل مع إنتاج السلع الأساسية. اتخذت الحكومة بعض الإجراءات الصارمة مثل إغلاق إنتاج وبيع السلع غير الأساسية، وحظر التجارة الدولية، وغير ذلك الكثير لمنع انتشار كوفيد-19. العمل الوحيد الذي يتعامل في هذا الوضع الوبائي هو الخدمات الأساسية المسموح لها بالفتح وتشغيل العمليات.

يتزايد نمو سوق وقود الطيران المستدام بسبب الحاجة إلى تقليل انبعاثات غازات الاحتباس الحراري في صناعة الطيران. ومع ذلك، فإن عوامل مثل عدم كفاية توافر المواد الخام والمصافي لتلبية الطلب على إنتاج وقود الطيران المستدام تعمل على تقييد نمو السوق. كان لإغلاق مرافق الإنتاج أثناء حالة الوباء تأثير كبير على السوق.

يتخذ المصنعون قرارات استراتيجية مختلفة للتعافي بعد جائحة كوفيد-19. ويجري اللاعبون أنشطة بحث وتطوير متعددة لتحسين التكنولوجيا المستخدمة في وقود الطيران المستدام. وبهذا، ستجلب الشركات وحدات تحكم متقدمة ودقيقة إلى السوق. بالإضافة إلى ذلك، أدى استخدام السلطات الحكومية لوقود الطيران المستدام في الشحن الجوي إلى نمو السوق.

التطورات الأخيرة

- في مارس 2022، أعلنت Neste بالتعاون مع DHL Express عن واحدة من أكبر صفقات الوقود المستدام للطائرات على الإطلاق. هذه الاتفاقية هي الأكبر من نوعها لشركة Neste للوقود المستدام للطائرات (SAF) حتى الآن وواحدة من أكبر اتفاقيات الوقود المستدام للطائرات في صناعة الطيران. سيعمل هذا التعاون على تعزيز شبكة Neste الحالية من خلال تقديم اتصال سلس في جميع أنحاء العالم

- في مارس 2022، قامت شركة BP ventures باستثمار 3 ملايين جنيه إسترليني في شركة Flylogix - وهي شركة رائدة في مجال الطائرات بدون طيار (UAV) تستخدم الطائرات بدون طيار للمساعدة في اكتشاف غاز الميثان. تركز مشاريع BP هذه على ربط وتنمية أعمال الطاقة الجديدة والشبكة الحالية من خلال تقديم اتصال سلس في جميع أنحاء العالم

نطاق سوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا

يتم تقسيم سوق وقود الطيران المستدام على أساس نوع الوقود وتكنولوجيا التصنيع وسعة المزج ومنصة المزج. سيساعدك النمو بين هذه القطاعات على تحليل قطاعات النمو الضئيلة في الصناعات وتزويد المستخدمين بنظرة عامة قيمة على السوق ورؤى السوق لمساعدتهم على اتخاذ قرارات استراتيجية لتحديد تطبيقات السوق الأساسية.

نوع الوقود

- الوقود الحيوي

- وقود الهيدروجين

- الطاقة إلى الوقود السائل

على أساس نوع الوقود، يتم تقسيم سوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا إلى وقود حيوي ووقود هيدروجيني وتحويل الطاقة إلى وقود سائل

تكنولوجيا التصنيع

- إسترات الأحماض الدهنية المعالجة بالهيدروجين والأحماض الدهنية - الكيروسين البارافيني الصناعي (HEFA-SPK)

- الكيروسين البارافيني الاصطناعي من شركة فيشر تروبش (FT-SPK)

- البارافين الاصطناعي من السكر المعالج بالهيدروجين المخمر (HFS-SIP)

- الكيروسين البارافيني الاصطناعي مع المواد العطرية من شركة فيشر تروبش (FT) (FT-SPK/A)

- الكحول إلى جيت سبك (ATJ-SPK)

- نفاثات التحلل الحراري المائي التحفيزي (CHJ)

على أساس تكنولوجيا التصنيع، تم تقسيم سوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا إلى إسترات الأحماض الدهنية المعالجة بالهيدروجين والأحماض الدهنية - الكيروسين البارافيني الاصطناعي (HEFA-SPK)، الكيروسين البارافيني الاصطناعي من فيشر تروبش (FT-SPK)، إيزوبارافين اصطناعي من سكر معالج بالهيدروجين المخمر (HFS-SIP)، الكيروسين البارافيني الاصطناعي من فيشر تروبش (FT) مع العطريات (FT-SPK / A)، الكحول إلى جيت SPK (ATJ-SPK) وجيت التحليل الحراري المائي التحفيزي (CHJ).

قدرة المزج

- أقل من 30%

- 30% إلى 50%

- فوق 50%

على أساس قدرة المزج، تم تقسيم سوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا إلى أقل من 30%، ومن 30% إلى 50%، وفوق 50%.

منصة المزج

- الطيران التجاري

- الطيران العسكري

- الطيران التجاري والعام

- مركبة جوية بدون طيار

على أساس منصة المزج، تم تقسيم سوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا إلى الطيران التجاري، والطيران العسكري، والطيران التجاري والعام، والمركبات الجوية بدون طيار

تحليل/رؤى إقليمية لسوق وقود الطيران المستدام

يتم تحليل سوق وقود الطيران المستدام وتوفير رؤى حول حجم السوق والاتجاهات حسب البلد ونوع الوقود وتكنولوجيا التصنيع وسعة المزج وصناعة منصة المزج كما هو مذكور أعلاه.

الدول التي يغطيها تقرير سوق وقود الطيران المستدام هي جنوب أفريقيا والمملكة العربية السعودية والإمارات العربية المتحدة وإسرائيل ومصر وبقية دول الشرق الأوسط وأفريقيا في الشرق الأوسط وأفريقيا

تهيمن جنوب أفريقيا على سوق وقود الطيران المستدام في الشرق الأوسط وأفريقيا، ويرجع هذا إلى الطلب المتزايد واللوائح التنظيمية لسوق وقود الطيران المستدام الفعّال. بالإضافة إلى ذلك، زادت استثمارات البحث والتطوير في تطوير وقود الطيران المستدام في المنطقة. ومن المتوقع أن يكون الطلب في هذه المنطقة مدفوعًا بالحكومات التي تستثمر بشكل متزايد في المشاريع الجديدة وتتخذ مبادرات نحو إزالة الكربون من انبعاثات الطيران.

كما يوفر قسم الدولة في التقرير عوامل التأثير الفردية على السوق والتغيرات في تنظيم السوق التي تؤثر على الاتجاهات الحالية والمستقبلية للسوق. نقاط البيانات مثل تحليل سلسلة القيمة المصب والمصب، والاتجاهات الفنية وتحليل قوى بورتر الخمس، ودراسات الحالة هي بعض المؤشرات المستخدمة للتنبؤ بسيناريو السوق للدول الفردية. كما يتم النظر في وجود وتوافر العلامات التجارية في الشرق الأوسط وأفريقيا والتحديات التي تواجهها بسبب المنافسة الكبيرة أو النادرة من العلامات التجارية المحلية والمحلية، وتأثير التعريفات الجمركية المحلية وطرق التجارة أثناء تقديم تحليل توقعات لبيانات الدولة.

تحليل المشهد التنافسي وحصة سوق وقود الطيران المستدام

يقدم المشهد التنافسي لسوق وقود الطيران المستدام تفاصيل حسب المنافس. وتشمل التفاصيل نظرة عامة على الشركة، والبيانات المالية للشركة، والإيرادات المولدة، وإمكانات السوق، والاستثمار في البحث والتطوير، ومبادرات السوق الجديدة، والتواجد في الشرق الأوسط وأفريقيا، ومواقع الإنتاج والمرافق، والقدرات الإنتاجية، ونقاط القوة والضعف للشركة، وإطلاق المنتج، وعرض المنتج ونطاقه، وهيمنة التطبيق. تتعلق نقاط البيانات المذكورة أعلاه فقط بتركيز الشركات فيما يتعلق بسوق وقود الطيران المستدام.

بعض اللاعبين الرئيسيين العاملين في سوق وقود الطيران المستدام هم Neste و Gevo و VELOCYS و Fulcrum BioEnergy و SkyNRG و Prometheus Fuels و World Energy و Avfuel Corporation و LanzaTech و Preem AB و Eni و Sasol Ltd و BP plc وغيرها.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELING

2.9 FUEL TYPE TIMELINE CURVE

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ANALYSIS OF FUTURE APPLICATIONS

4.2 ADVANCING SUSTAINABILITY WITHIN AVIATION

4.3 ORGANIZATIONS INVOLVED IN SUSTAINABLE AVIATION FUEL PROGRAMS

4.4 RESEARCH & INNOVATION ROADMAP FOR AVIATION HYDROGEN TECHNOLOGY

4.5 RECENT SUPPLY CONTRACTS BY SHELL

4.6 STANDARDS

4.6.1 OVERVIEW

4.6.2 INTERNATIONAL CIVIL AVIATION ORGANIZATION (ICAO)

4.6.3 INTERNATIONAL AIR TRANSPORT ASSOCIATION (IATA)

4.6.4 BUREAU OF CIVIL AVIATION SECURITY

4.6.5 FEDERAL AVIATION ADMINISTRATION

4.6.6 EUROPEAN UNION AVIATION SAFETY AGENCY (EASA)

4.6.7 CIVIL AVIATION ADMINISTRATION OF CHINA (CAAC)

4.6.8 UAE GENERAL CIVIL AVIATION AUTHORITY (GCAA)

4.7 VALUE CHAIN ANALYSIS

4.7.1 OVERVIEW OF VALUE CHAIN ANALYSIS OF SUSTAINABLE AVIATION FUEL MARKET

4.8 TECHNOLOGY TRENDS

4.8.1 OVERVIEW

4.8.2 HYDROTHERMAL LIQUEFACTION (HTL)

4.8.3 PYROLYSIS PATHWAYS OR PYROLYSIS-TO-JET (PTJ)

4.8.4 TECHNOLOGICAL MATURITY - FUEL READINESS LEVEL AND FEEDSTOCK READINESS LEVEL

4.9 IMPACT OF MEGATREND

4.1 INNOVATION AND PATENT ANALYSIS

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 INCREASING NEED FOR REDUCTION IN GHG EMISSIONS IN THE AVIATION INDUSTRY

5.1.2 INCREASE IN AIR TRANSPORTATION CONSUMPTION OF SYNTHETIC LUBRICANTS

5.1.3 INCREASE IN DEMAND FOR SUSTAINABLE AVIATION FUEL BY AIRLINES

5.1.4 INCREASE IN INVESTMENTS FOR THE GROWTH OF COMMERCIAL AIRCRAFTS

5.2 RESTRAINTS

5.2.1 INADEQUATE AVAILABILITY OF FEEDSTOCK AND REFINERIES TO MEET SUSTAINABLE AVIATION FUEL PRODUCTION DEMAND

5.2.2 FLUCTUATIONS IN CRUDE OIL PRICES AND CONTAMINATION OF LUBRICANTS

5.3 OPPORTUNITIES

5.3.1 REDUCTION IN CARBON FOOTPRINT DUE TO LOW CAPABILITY OF SUSTAINABLE AVIATION FUEL

5.3.2 DEVELOPMENT OF ECO-FRIENDLY AND SAFE AVIATION LUBRICANTS

5.3.3 RISE IN DEMAND FOR LOW-DENSITY LUBRICANTS FOR REDUCED WEIGHT

5.3.4 RISE IN SAFETY REGULATIONS FOR AIRCRAFTS

5.4 CHALLENGE

5.4.1 THE HIGH COST OF SUSTAINABLE AVIATION FUEL INCREASES THE OPERATING COST OF AIRLINES

6 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE

6.1 OVERVIEW

6.2 BIOFUEL

6.3 HYDROGEN FUEL

6.4 POWER TO LIQUID FUEL

7 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY

7.1 OVERVIEW

7.2 HYDROPROCESSED FATTY ACID EASTERS AND FATTY ACIDS - SYNTHETIC PARAFFINIC KEROSENE (HEFA-SPK)

7.3 FISCHER TROPSCH SYNTHETIC PARAFFINIC KEROSENE (FT-SPK)

7.4 SYNTHETIC ISO-PARAFFIN FROM FERMENTED HYDROPROCESSED SUGAR (HFS-SIP)

7.5 FISCHER TROPSCH (FT) SYNTHETIC PARAFFINIC KEROSENE WITH AROMATICS (FT-SPK/A)

7.6 ALCOHOL TO JET SPK (ATJ-SPK)

7.7 CATALYTIC HYDROTHERMOLYSIS JET (CHJ)

8 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY

8.1 OVERVIEW

8.2 BELOW 30%

8.3 30% TO 50%

8.4 ABOVE 50%

9 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM

9.1 OVERVIEW

9.2 COMMERCIAL AVIATION

9.2.1 BY TYPE

9.2.1.1 NARROW BODY AIRCRAFT

9.2.1.2 WIDE-BODY AIRCRAFT (WBA)

9.2.1.3 VERY LARGE AIRCRAFT (VLA)

9.2.1.4 REGIONAL TRANSPORT AIRCRAFT (RTA)

9.2.2 BY FUEL TYPE

9.2.2.1 BIOFUEL

9.2.2.2 HYDROGEN

9.2.2.3 POWER TO LIQUID FUEL

9.3 BUSINESS & GENERAL AVIATION

9.3.1 BIOFUEL

9.3.2 HYDROGEN

9.3.3 POWER TO LIQUID FUEL

9.4 MILITARY AVIATION

9.4.1 BIOFUEL

9.4.2 HYDROGEN

9.4.3 POWER TO LIQUID FUEL

9.5 UNMANNED AERIAL VEHICLE

9.5.1 BIOFUEL

9.5.2 HYDROGEN

9.5.3 POWER TO LIQUID FUEL

10 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY REGION

10.1 MIDDLE EAST AND AFRICA

10.1.1 SOUTH AFRICA

10.1.2 SAUDI ARABIA

10.1.3 ISRAEL

10.1.4 EGYPT

10.1.5 REST OF MIDDLE EAST AND AFRICA

11 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: COMPANY LANDSCAPE

11.1 COMPANY SHARE ANALYSIS: MIDDLE EAST & AFRICA

12 SWOT ANALYSIS

13 COMPANY PROFILES

13.1 NESTE

13.1.1 COMPANY SNAPSHOT

13.1.2 REVENUE ANALYSIS

13.1.3 COMPANY SHARE ANALYSIS

13.1.4 PRODUCT PORTFOLIO

13.1.5 RECENT DEVELOPMENTS

13.2 BP P.L.C.

13.2.1 COMPANY SNAPSHOT

13.2.2 REVENUE ANALYSIS

13.2.3 COMPANY SHARE ANALYSIS

13.2.4 SERVICE PORTFOLIO

13.2.5 RECENT DEVELOPMENTS

13.3 PREEM AB.

13.3.1 COMPANY SNAPSHOT

13.3.2 COMPANY SHARE ANALYSIS

13.3.3 PRODUCT PORTFOLIO

13.3.4 RECENT DEVELOPMENT

13.4 CEPSA

13.4.1 COMPANY SNAPSHOT

13.4.2 COMPANY SHARE ANALYSIS

13.4.3 PRODUCT PORTFOLIO

13.4.4 RECENT DEVELOPMENT

13.5 CHEVRON CORPORATION

13.5.1 COMPANY SNAPSHOT

13.5.2 REVENUE ANALYSIS

13.5.3 COMPANY SHARE ANALYSIS

13.5.4 PRODUCT PORTFOLIO

13.5.5 RECENT DEVELOPMENTS

13.6 AVFUEL CORPORATION

13.6.1 COMPANY SNAPSHOT

13.6.2 PRODUCT PORTFOLIO

13.6.3 RECENT DEVELOPMENT

13.7 ENI

13.7.1 COMPANY SNAPSHOT

13.7.2 REVENUE ANALYSIS

13.7.3 PRODUCT PORTFOLIO

13.7.4 RECENT DEVELOPMENTS

13.8 EXXON MOBIL CORPORATION

13.8.1 COMPANY SNAPSHOT

13.8.2 REVENUE ANALYSIS

13.8.3 PRODUCT PORTFOLIO

13.8.4 RECENT DEVELOPMENTS

13.9 FULCRUM BIOENERGY

13.9.1 COMPANY SNAPSHOT

13.9.2 PRODUCT PORTFOLIO

13.9.3 RECENT DEVELOPMENT

13.1 GEVO

13.10.1 COMPANY SNAPSHOT

13.10.2 REVENUE ANALYSIS

13.10.3 PRODUCT PORTFOLIO

13.10.4 RECENT DEVELOPMENTS

13.11 HONEYWELL INTERNATIONAL INC.

13.11.1 COMPANY SNAPSHOT

13.11.2 REVENUE ANALYSIS

13.11.3 PRODUCT PORTFOLIO

13.11.4 RECENT DEVELOPMENTS

13.12 HYPOINT INC.

13.12.1 COMPANY SNAPSHOT

13.12.2 PRODUCT PORTFOLIO

13.12.3 RECENT DEVELOPMENT

13.13 JOHNSON MATTHEY

13.13.1 COMPANY SNAPSHOT

13.13.2 REVENUE ANALYSIS

13.13.3 PRODUCT PORTFOLIO

13.13.4 RECENT DEVELOPMENT

13.14 LANZATECH

13.14.1 COMPANY SNAPSHOT

13.14.2 PRODUCT PORTFOLIO

13.14.3 RECENT DEVELOPMENT

13.15 PROMETHEUS FUELS

13.15.1 COMPANY SNAPSHOT

13.15.2 PRODUCT PORTFOLIO

13.15.3 RECENT DEVELOPMENT

13.16 SKYNRG

13.16.1 COMPANY SNAPSHOT

13.16.2 PRODUCT PORTFOLIO

13.16.3 RECENT DEVELOPMENTS

13.17 SASOL

13.17.1 COMPANY SNAPSHOT

13.17.2 REVENUE ANALYSIS

13.17.3 PRODUCT PORTFOLIO

13.17.4 RECENT DEVELOPMENTS

13.18 TOTALENERGIES

13.18.1 COMPANY SNAPSHOT

13.18.2 REVENUE ANALYSIS

13.18.3 PRODUCT PORTFOLIO

13.18.4 RECENT DEVELOPMENT

13.19 VELOCYS

13.19.1 COMPANY SNAPSHOT

13.19.2 REVENUE ANALYSIS

13.19.3 PRODUCT PORTFOLIO

13.19.4 RECENT DEVELOPMENTS

13.2 VIRENT, INC.

13.20.1 COMPANY SNAPSHOT

13.20.2 PRODUCT PORTFOLIO

13.20.3 RECENT DEVELOPMENT

13.21 WORLD ENERGY

13.21.1 COMPANY SNAPSHOT

13.21.2 PRODUCT PORTFOLIO

13.21.3 RECENT DEVELOPMENT

13.22 ZEROAVIA, INC.

13.22.1 COMPANY SNAPSHOT

13.22.2 PRODUCT PORTFOLIO

13.22.3 RECENT DEVELOPMENT

14 QUESTIONNAIRE

15 RELATED REPORTS

List of Table

TABLE 1 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 2 MIDDLE EAST & AFRICA BIOFUEL IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 3 MIDDLE EAST & AFRICA HYDROGEN IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 4 MIDDLE EAST & AFRICA POWER TO LIQUID FUEL IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 5 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 6 MIDDLE EAST & AFRICA HYDROPROCESSED FATTY ACID EASTERS AND FATTY ACIDS - SYNTHETIC PARAFFINIC KEROSENE (HEFA-SPK) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 7 MIDDLE EAST & AFRICA FISCHER TROPSCH SYNTHETIC PARAFFINIC KEROSENE (FT-SPK) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 8 MIDDLE EAST & AFRICA SYNTHETIC ISO-PARAFFIN FROM FERMENTED HYDROPROCESSED SUGAR (HFS-SIP) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 9 MIDDLE EAST & AFRICA FISCHER TROPSCH (FT) SYNTHETIC PARAFFINIC KEROSENE WITH AROMATICS (FT-SPK/A) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 10 MIDDLE EAST & AFRICA ALCOHOL TO JET SPK (ATJ-SPK) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 11 MIDDLE EAST & AFRICA CATALYTIC HYDROTHERMOLYSIS JET (CHJ) IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 12 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 13 MIDDLE EAST & AFRICA BELOW 30% IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 14 MIDDLE EAST & AFRICA 30% TO 50% IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 15 MIDDLE EAST & AFRICA ABOVE 50% IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 16 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 17 MIDDLE EAST & AFRICA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 18 MIDDLE EAST & AFRICA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 19 MIDDLE EAST & AFRICA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 20 MIDDLE EAST & AFRICA BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 21 MIDDLE EAST & AFRICA BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 22 MIDDLE EAST & AFRICA MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 23 MIDDLE EAST & AFRICA MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 24 MIDDLE EAST & AFRICA UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY REGION, 2020-2029 (EURO MILLION)

TABLE 25 MIDDLE EAST & AFRICA UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 26 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY COUNTRY, 2020-2029 (EURO MILLION)

TABLE 27 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY COUNTRY, 2020-2029 (METRIC TONNES)

TABLE 28 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 29 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 30 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 31 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 32 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 33 MIDDLE EAST AND AFRICA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 34 MIDDLE EAST AND AFRICA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 35 MIDDLE EAST AND AFRICA BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 36 MIDDLE EAST AND AFRICA MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 37 MIDDLE EAST AND AFRICA UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 38 SOUTH AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 39 SOUTH AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 40 SOUTH AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 41 SOUTH AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 42 SOUTH AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 43 SOUTH AFRICA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 44 SOUTH AFRICA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 45 SOUTH AFRICA BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 46 SOUTH AFRICA MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 47 SOUTH AFRICA UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 48 SAUDI ARABIA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 49 SAUDI ARABIA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 50 SAUDI ARABIA SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 51 SAUDI ARABIA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 52 SAUDI ARABIA SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 53 SAUDI ARABIA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 54 SAUDI ARABIA COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 55 SAUDI ARABIA BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 56 SAUDI ARABIA MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 57 SAUDI ARABIA UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 58 ISRAEL SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 59 ISRAEL SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 60 ISRAEL SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 61 ISRAEL SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 62 ISRAEL SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 63 ISRAEL COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 64 ISRAEL COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 65 ISRAEL BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 66 ISRAEL MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 67 ISRAEL UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 68 EGYPT SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 69 EGYPT SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

TABLE 70 EGYPT SUSTAINABLE AVIATION FUEL MARKET, BY MANUFACTURING TECHNOLOGY, 2020-2029 (EURO MILLION)

TABLE 71 EGYPT SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING CAPACITY, 2020-2029 (EURO MILLION)

TABLE 72 EGYPT SUSTAINABLE AVIATION FUEL MARKET, BY BLENDING PLATFORM, 2020-2029 (EURO MILLION)

TABLE 73 EGYPT COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY TYPE, 2020-2029 (EURO MILLION)

TABLE 74 EGYPT COMMERCIAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 75 EGYPT BUSINESS & GENERAL AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 76 EGYPT MILITARY AVIATION IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 77 EGYPT UNMANNED AERIAL VEHICLE IN SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 78 REST OF MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (EURO MILLION)

TABLE 79 REST OF MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET, BY FUEL TYPE, 2020-2029 (METRIC TONNES)

List of Figure

FIGURE 1 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: SEGMENTATION

FIGURE 2 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: DATA TRIANGULATION

FIGURE 3 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: DROC ANALYSIS

FIGURE 4 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: MIDDLE EAST & AFRICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: DBMR MARKET POSITION GRID

FIGURE 8 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: VENDOR SHARE ANALYSIS

FIGURE 9 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: SEGMENTATION

FIGURE 10 THE INCREASING NEED FOR REDUCTION IN GHG EMISSIONS IN THE AVIATION INDUSTRY IS EXPECTED TO DRIVE THE MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET IN THE FORECAST PERIOD

FIGURE 11 BIO FUEL SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET IN 2022 & 2029

FIGURE 12 NORTH AMERICA IS EXPECTED TO DOMINATE AND BE THE FASTEST-GROWING REGION IN THE MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET IN THE FORECAST PERIOD

FIGURE 13 VALUE CHAIN ANALYSIS FRAMEWORK

FIGURE 14 DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGE OF MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET

FIGURE 15 MIDDLE EAST & AFRICA AIR TRANSPORT PASSENGER DEMAND

FIGURE 16 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: BY TECHNOLOGY, 2021

FIGURE 17 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: BY MANUFACTURING TECHNOLOGY, 2021

FIGURE 18 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: BY BLENDING CAPACITY, 2021

FIGURE 19 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: BY BLENDING PLATFORM, 2021

FIGURE 20 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET: SNAPSHOT (2021)

FIGURE 21 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET: BY COUNTRY (2021)

FIGURE 22 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET: BY COUNTRY (2022 & 2029)

FIGURE 23 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET: BY COUNTRY (2021 & 2029)

FIGURE 24 MIDDLE EAST AND AFRICA SUSTAINABLE AVIATION FUEL MARKET: BY FUEL TYPE (2022-2029)

FIGURE 25 MIDDLE EAST & AFRICA SUSTAINABLE AVIATION FUEL MARKET: COMPANY SHARE 2021 (%)

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.