Europe 3d Printing Materials Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

901.50 Million

USD

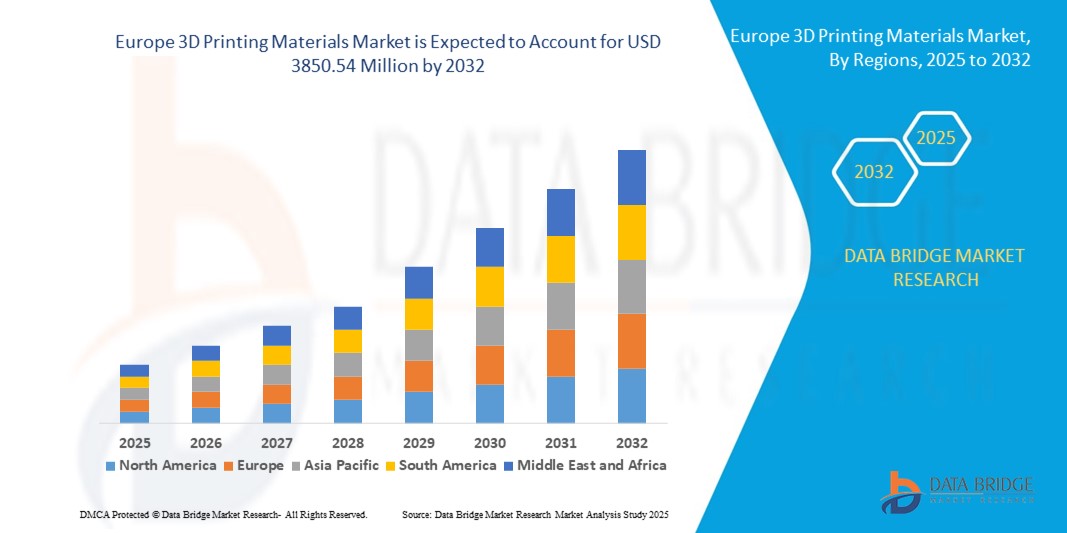

3,850.54 Million

2024

2032

USD

901.50 Million

USD

3,850.54 Million

2024

2032

| 2025 –2032 | |

| USD 901.50 Million | |

| USD 3,850.54 Million | |

| % | |

|

تجزئة سوق مواد الطباعة ثلاثية الأبعاد في أوروبا، حسب النوع (البلاستيك/البوليمرات، المعادن، السيراميك ، وغيرها)، الشكل (مسحوق، خيوط، وسائل)، التكنولوجيا (نمذجة الترسيب المنصهر (FDM)، التلبيد الانتقائي بالليزر (SLS)، الطباعة الضوئية المجسمة (SLA)، التلبيد المباشر بالليزر للمعادن (DMLS)، التصنيع الإضافي لمناطق واسعة (BAAM)، التصنيع الإضافي لقوس الأسلاك (WAAM)، تقنية ColorJet، وغيرها)، الاستخدام النهائي (التصنيع الصناعي، السيارات، الفضاء والدفاع، الرعاية الصحية، السلع الاستهلاكية، الإلكترونيات، التعليم، البناء، وغيرها) - اتجاهات الصناعة وتوقعاتها حتى عام 2032

ما هو حجم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا ومعدل النمو؟

- تم تقييم حجم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا بـ 901.50 مليون دولار أمريكي في عام 2024 ومن المتوقع أن يصل إلى 3850.54 مليون دولار أمريكي بحلول عام 2032 ، بمعدل نمو سنوي مركب قدره 19.90٪ خلال الفترة المتوقعة

- من المتوقع أن يؤدي زيادة اعتماد الطباعة ثلاثية الأبعاد في مختلف الصناعات، وارتفاع معدلات النماذج الأولية والأدوات السريعة، وإمكانية الوصول المتزايدة وبأسعار معقولة لتقنيات الطباعة ثلاثية الأبعاد عالميًا إلى دفع نمو السوق.

ما هي أهم النتائج المترتبة على سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

- هناك زيادة مماثلة في الطلب على المواد التي تلبي المتطلبات المتنوعة لهذه العملية التصنيعية المبتكرة، حيث تتبنى الصناعات القدرات الثورية للطباعة ثلاثية الأبعاد. وتمتد تنوعات الطباعة ثلاثية الأبعاد، المعروفة أيضًا بالتصنيع الإضافي، إلى قطاعات مثل الفضاء والرعاية الصحية والسيارات والسلع الاستهلاكية، حيث تُستخدم هذه التقنية في النماذج الأولية السريعة والإنتاج المخصص وتصنيع التصاميم المعقدة.

- العامل المساهم في زيادة الطلب على مواد الطباعة ثلاثية الأبعاد هو قدرة هذه التقنية على إنتاج مكونات معقدة وقابلة للتخصيص بشكل كبير. فطرق التصنيع التقليدية لا تتسم بالكفاءة والسرعة الكافية، إذ تسعى الصناعات إلى الحصول على قطع أكثر تعقيدًا ودقة في التصميم. وتسد الطباعة ثلاثية الأبعاد هذه الفجوة من خلال السماح بإنشاء هياكل هندسية معقدة بكفاءة أعلى.

- يتزايد الطلب على المواد المتخصصة مع تطور احتياجات القطاعات الصناعية، مثل الطيران والرعاية الصحية والسيارات والسلع الاستهلاكية، التي تطبق هذه التقنية التحويلية، حيث تواصل الطباعة ثلاثية الأبعاد إحداث ثورة في عمليات التصنيع. ولذلك، فإن تزايد اعتماد الطباعة ثلاثية الأبعاد في مختلف الصناعات يدفع نمو السوق.

- استحوذ سوق مواد الطباعة ثلاثية الأبعاد في ألمانيا على أكبر حصة بنسبة 28.11% من الإيرادات الإقليمية في أوروبا بحلول عام 2024. ويعزى هذا النمو إلى الطلب على أنظمة الأمان عالية التقنية، والمنازل الذكية الموفرة للطاقة، وتحديثات البنية التحتية الرقمية.

- من المتوقع أن ينمو سوق مواد الطباعة ثلاثية الأبعاد في المملكة المتحدة بمعدل نمو سنوي مركب قوي بنسبة 12.23٪ خلال الفترة المتوقعة، مدفوعًا بالمخاوف المتزايدة بشأن الأمن السكني والتجاري، وشعبية إعدادات المنزل الذكي DIY، والانتشار القوي لتجارة التجزئة والإنترنت.

- هيمن قطاع البلاستيك/البوليمرات على السوق بأكبر حصة إيرادات بلغت 45.8% في عام 2024، وذلك بفضل تنوعه وقدرته على تحمل التكاليف وانتشاره على نطاق واسع عبر النماذج الأولية والتطبيقات الصناعية.

نطاق التقرير وتقسيم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا

|

صفات |

رؤى رئيسية حول سوق مواد الطباعة ثلاثية الأبعاد في أوروبا |

|

القطاعات المغطاة |

|

|

الدول المغطاة |

أوروبا

|

|

اللاعبون الرئيسيون في السوق |

|

|

فرص السوق |

|

|

مجموعات معلومات البيانات ذات القيمة المضافة |

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، فإن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research تشمل أيضًا تحليلًا متعمقًا من الخبراء وتحليل التسعير وتحليل حصة العلامة التجارية واستطلاع رأي المستهلكين وتحليل التركيبة السكانية وتحليل سلسلة التوريد وتحليل سلسلة القيمة ونظرة عامة على المواد الخام / المواد الاستهلاكية ومعايير اختيار البائعين وتحليل PESTLE وتحليل Porter والإطار التنظيمي. |

ما هو الاتجاه الرئيسي في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

التحول نحو مواد عالية الأداء ووظيفية

- إن الاتجاه المحدد في سوق مواد الطباعة ثلاثية الأبعاد هو التطوير المتزايد واعتماد المواد عالية الأداء والوظيفية، بما في ذلك المركبات وسبائك المعادن والبوليمرات الحيوية، والتي تعمل على توسيع نطاق التطبيقات الصناعية والطبية والاستهلاكية.

- على سبيل المثال، تقوم شركات مثل Markforged وEOS بتقديم خيوط معززة بألياف الكربون ومساحيق البوليمر عالية الحرارة التي تسمح بإنتاج أجزاء خفيفة الوزن ومتينة لآلات الطيران والسيارات والآلات الصناعية.

- تتيح مواد الطباعة ثلاثية الأبعاد الوظيفية بشكل متزايد إمكانية الطباعة متعددة المواد، أو تضمين الإلكترونيات، أو دمج المسارات الموصلة، وبالتالي تحويل سير عمل التصنيع التقليدي إلى عمليات إضافية متكاملة

- ويشمل هذا الاتجاه أيضًا الأحبار الحيوية والبوليمرات المتوافقة حيويًا للطباعة الطبية ثلاثية الأبعاد، بما في ذلك هياكل الأنسجة والغرسات والأطراف الصناعية المخصصة، مما يوفر دقة محسنة وتصميمات خاصة بالمريض ودورات إنتاج أسرع.

- مع تحرك الصناعات نحو التصنيع الرقمي والإنتاج حسب الطلب، تعمل شركات مثل Formlabs و3D Systems على تطوير راتنجات ومساحيق متخصصة للنماذج الأولية المتقدمة والأدوات وتطبيقات الاستخدام النهائي، مما يدفع الابتكار عبر القطاعات

- يؤدي التبني المتزايد لمواد الطباعة ثلاثية الأبعاد الوظيفية والمتينة والجاهزة للصناعة إلى إعادة تشكيل توقعات المستخدمين وتوسيع التطبيقات في جميع أنحاء السيارات والرعاية الصحية والفضاء والإلكترونيات الاستهلاكية

ما هي العوامل الرئيسية المؤثرة في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

- إن الطلب المتزايد على الأجزاء خفيفة الوزن وعالية القوة والمخصصة في الصناعات مثل الفضاء والسيارات والرعاية الصحية هو المحرك الرئيسي لسوق مواد الطباعة ثلاثية الأبعاد

- على سبيل المثال، في مارس 2024، أطلقت شركة ستراتاسيس مواد بلاستيكية حرارية عالية الحرارة ومقاومة للهب مصممة للاستخدام في الأدوات الصناعية والفضائية، مما يعزز المتانة والامتثال التنظيمي.

- إن التبني المتزايد للتصنيع الإضافي في النماذج الأولية والإنتاج على دفعات صغيرة والأشكال الهندسية المعقدة يغذي ابتكار المواد، مما يتيح التخصيص الدقيق مع تقليل النفايات وأوقات التسليم

- علاوة على ذلك، تعمل مبادرات الاستدامة على دفع استخدام الخيوط القائمة على المواد الحيوية والبوليمرات القابلة لإعادة التدوير، بما يتماشى مع أهداف الحوكمة البيئية والاجتماعية والمؤسسية والحد من التأثير البيئي

- يؤدي دمج مواد الطباعة ثلاثية الأبعاد مع الطابعات ثلاثية الأبعاد الآلية والصناعية، بما في ذلك أنظمة الألياف المتعددة المواد والمستمرة، إلى تعزيز الكفاءة والفعالية من حيث التكلفة والاعتماد الأوسع عبر العديد من الصناعات ذات الاستخدام النهائي.

ما هو العامل الذي يعيق نمو سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

- إن التكلفة العالية والتوافر المحدود لمواد الطباعة ثلاثية الأبعاد المتقدمة، وخاصة المركبات الوظيفية ومساحيق المعادن والراتنجات المتوافقة بيولوجيًا، تشكل عوائق كبيرة أمام التبني الواسع النطاق

- على سبيل المثال، غالبًا ما تأتي مساحيق المعادن الممتازة للتطبيقات الجوية والطبية بتكاليف شراء عالية وتتطلب تخزينًا ومعالجة متخصصة، مما يحد من الاستخدام في التطبيقات عالية القيمة.

- تظل اتساق أداء المواد ومراقبة الجودة والتوحيد القياسي من التحديات، خاصة بالنسبة للأجزاء الصناعية التي تتطلب الامتثال التنظيمي الصارم والسلامة الميكانيكية

- بالإضافة إلى ذلك، فإن الافتقار إلى المتخصصين المدربين والخبرة الفنية في التعامل مع مواد الطباعة ثلاثية الأبعاد المتخصصة يحد من التبني في الأسواق الناشئة والشركات الصغيرة

- إن التغلب على هذه التحديات من خلال خفض التكاليف، والابتكار في المواد، وبرامج التدريب سيكون أمرًا بالغ الأهمية لتمكين التبني الأوسع والنمو المستدام للسوق على مستوى العالم.

كيف يتم تقسيم سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

يتم تقسيم السوق على أساس النوع والشكل والتكنولوجيا والاستخدام النهائي.

- حسب النوع

يُقسّم سوق مواد الطباعة ثلاثية الأبعاد، حسب نوعها، إلى بلاستيك/بوليمرات، ومعادن، وسيراميك، وغيرها. وقد هيمن قطاع البلاستيك/البوليمرات على السوق محققًا أكبر حصة إيرادات بلغت 45.8% في عام 2024، بفضل تنوعه، وسعره المناسب، وانتشار استخدامه في تطبيقات النماذج الأولية والتطبيقات الصناعية. ويُفضّل استخدام البلاستيك/البوليمرات في تصنيع الأجزاء خفيفة الوزن، والنماذج الأولية الوظيفية، والمنتجات الاستهلاكية، نظرًا لسهولة معالجتها، وخصائصها الميكانيكية الجيدة، وتوافقها مع تقنيات الطباعة ثلاثية الأبعاد المتعددة.

من المتوقع أن ينمو قطاع المعادن بأسرع معدل نمو سنوي مركب بين عامي 2025 و2032، مدفوعًا بالطلب في صناعات الطيران والسيارات والقطاع الطبي على مكونات عالية القوة ومقاومة للحرارة ومتينة. تتيح مساحيق وسبائك المعادن إنتاج هياكل معقدة وقادرة على تحمل الأحمال، وهو ما يصعب تحقيقه بالتصنيع التقليدي. في الوقت نفسه، تكتسب المواد الخزفية زخمًا متزايدًا في التطبيقات عالية الحرارة والمتوافقة حيويًا في مجالي الرعاية الصحية والإلكترونيات، على الرغم من أن استخدامها لا يزال محدودًا بسبب ارتفاع التكاليف ومتطلبات المعدات المتخصصة.

- حسب النموذج

بناءً على الشكل، يُقسّم سوق مواد الطباعة ثلاثية الأبعاد إلى مسحوق، وخيوط، وسائل. وقد استحوذ قطاع الخيوط على أكبر حصة من إيرادات السوق بنسبة 52.3% في عام 2024، مدعومًا باستخدامه الواسع في طابعات نمذجة الترسيب المنصهر (FDM)، وسهولة التعامل معه، وسعره المناسب للتطبيقات الصناعية والاستهلاكية. تتوفر الخيوط في اللدائن الحرارية، والمركبات، والبوليمرات الحيوية، مما يوفر تنوعًا في استخدامات النماذج الأولية، والأدوات، وقطع الاستخدام النهائي الوظيفية.

من المتوقع أن يشهد شكل المسحوق أسرع معدل نمو سنوي مركب بين عامي 2025 و2032، ويعود ذلك بشكل رئيسي إلى دوره المحوري في التلبيد الانتقائي بالليزر (SLS)، والتلبيد المباشر بالليزر للمعادن (DMLS)، وغيرها من عمليات التصنيع المضافة عالية الدقة للمعادن والبوليمرات. وتُفضل مواد الطباعة ثلاثية الأبعاد السائلة، المستخدمة بشكل رئيسي في الطباعة المجسمة (SLA) والطابعات القائمة على الراتنج، في تصنيع الأجزاء عالية الدقة والأشكال الهندسية المعقدة، إلا أن تكلفتها ومتطلبات ما بعد المعالجة محدودة.

- حسب التكنولوجيا

بناءً على التكنولوجيا، يُقسّم سوق مواد الطباعة ثلاثية الأبعاد إلى نمذجة الترسيب المنصهر (FDM)، والتلبيد الانتقائي بالليزر (SLS)، والطباعة المجسمة (SLA)، والتلبيد المعدني المباشر بالليزر (DMLS)، والتصنيع الإضافي للمناطق الكبيرة (BAAM)، والتصنيع الإضافي للقوس السلكي (WAAM)، وتقنية ColorJet، وغيرها. هيمن قطاع FDM على السوق محققًا أكبر حصة إيرادات بلغت 40.9% في عام 2024، بفضل سهولة الوصول إليه وسعره المناسب وقدرته على معالجة مجموعة واسعة من اللدائن الحرارية والمركبات. يُستخدم FDM على نطاق واسع في النماذج الأولية والاختبارات الوظيفية والأغراض التعليمية، مما يجعله شائعًا في العديد من الصناعات.

من المتوقع أن تشهد تقنية SLS وDMLS أسرع نمو بين عامي 2025 و2032، نظرًا لقدرتهما على إنتاج قطع غيار عالية القوة ومعقدة لتطبيقات الطيران والسيارات والطب. تلبي تقنية SLA وBAAM وWAAM وColorJet تطبيقات متخصصة تتطلب دقة عالية وسرعة عالية أو إنتاجًا واسع النطاق، مما يوسع نطاق السوق التكنولوجي بشكل أكبر.

- حسب الاستخدام النهائي

بناءً على الاستخدام النهائي، يُقسّم سوق مواد الطباعة ثلاثية الأبعاد إلى قطاعات التصنيع الصناعي، والسيارات، والفضاء والدفاع، والرعاية الصحية، والسلع الاستهلاكية، والإلكترونيات، والتعليم، والبناء، وغيرها. وقد استحوذ قطاع التصنيع الصناعي على أكبر حصة من إيرادات السوق بنسبة 38.6% في عام 2024، مدفوعًا بالاعتماد السريع على التصنيع الإضافي في النماذج الأولية، والأدوات، والتجهيزات، وقطع الإنتاج. وتستفيد الصناعات من مواد الطباعة ثلاثية الأبعاد لتقليل فترات التنفيذ، وتحسين التصاميم، ورفع الكفاءة.

من المتوقع أن ينمو قطاعا الرعاية الصحية والفضاء والدفاع بأسرع معدل نمو سنوي مركب بين عامي 2025 و2032، مدفوعين بتزايد الطلب على الغرسات والأطراف الصناعية والمكونات الهيكلية خفيفة الوزن والأجزاء الحيوية المصممة حسب الطلب. ويدعم قطاعا التعليم والتطبيقات الاستهلاكية الوعي بالطباعة ثلاثية الأبعاد واعتمادها، بينما يدمج قطاعا الإلكترونيات والبناء الطباعة ثلاثية الأبعاد تدريجيًا في المكونات المتخصصة والهياكل واسعة النطاق والمنتجات المخصصة.

أية منطقة تمتلك أكبر حصة من سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

- استحوذ سوق مواد الطباعة ثلاثية الأبعاد في ألمانيا على أكبر حصة بنسبة 28.11% من الإيرادات الإقليمية في أوروبا بحلول عام 2024. ويعزى هذا النمو إلى الطلب على أنظمة الأمان عالية التقنية، والمنازل الذكية الموفرة للطاقة، وتحديثات البنية التحتية الرقمية.

- يفضل المستهلكون المنتجات المتوافقة مع منصات المنزل الذكي الشهيرة مثل Alexa وGoogle Assistant، في حين يعمل التركيز في البلاد على الاستدامة والابتكار على تسريع تبني السوق بشكل أكبر

نظرة عامة على سوق مواد الطباعة ثلاثية الأبعاد في فرنسا

يشهد سوق مواد الطباعة ثلاثية الأبعاد في فرنسا نموًا مطردًا، مدعومًا بالتوسع العمراني، واعتماد المنازل الذكية، ووعي المستهلكين بحلول الأمن الرقمي. وتشجع الحوافز الحكومية لتحديثات المباني الموفرة للطاقة، والوجود المتزايد لمُدمجي المنازل الذكية، على تبني هذه الحلول في القطاعين السكني والتجاري.

نظرة عامة على سوق مواد الطباعة ثلاثية الأبعاد في إيطاليا

من المتوقع أن يشهد سوق مواد الطباعة ثلاثية الأبعاد في إيطاليا نموًا ملحوظًا، مدفوعًا بزيادة استخدام الأجهزة المنزلية المتصلة، واهتمام المستهلكين المتزايد بأتمتة المنازل، وتحديث المباني السكنية القديمة. ويعزز التكامل مع منصات التحكم الصوتي وتطبيقات الهواتف الذكية جاذبية السوق.

ما هي الدولة الأسرع نمواً في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

من المتوقع أن ينمو سوق مواد الطباعة ثلاثية الأبعاد في المملكة المتحدة بمعدل نمو سنوي مركب قوي قدره 12.23% خلال الفترة المتوقعة، مدفوعًا بتزايد المخاوف بشأن أمن المنازل والمنشآت التجارية، وشعبية أنظمة المنازل الذكية ذاتية الصنع، والانتشار القوي لقطاعي التجزئة والتسوق عبر الإنترنت. ويعزز اعتماد أنظمة الدخول بدون مفتاح والأنظمة المتصلة في المكاتب والشقق والوحدات السكنية متعددة العائلات الطلب بشكل أكبر.

نظرة عامة على سوق مواد الطباعة ثلاثية الأبعاد في بولندا

يشهد السوق البولندي زخمًا متزايدًا بفضل التوسع العمراني، والاعتماد المتزايد على المنازل الذكية، والاهتمام المتزايد بأنظمة الوصول الآمنة والموفرة للطاقة. ويتزايد إقبال المستهلكين البولنديين على دمج مواد الطباعة ثلاثية الأبعاد مع الأجهزة المزوّدة بتقنية إنترنت الأشياء لضمان الراحة والأمان.

ما هي الشركات الرائدة في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

وتقود صناعة مواد الطباعة ثلاثية الأبعاد في أوروبا بشكل أساسي شركات راسخة، بما في ذلك:

- فورم لابس (الولايات المتحدة)

- EOS (ألمانيا)

- شركة إنفيجن تيك يو إس ذات المسؤولية المحدودة (الولايات المتحدة)

- العناصر الأمريكية (الولايات المتحدة)

- Höganäs AB (السويد)

- أولتي ميكر (هولندا)

- شركة كاربون (الولايات المتحدة)

- شركة كرايبرغ تي بي إي المحدودة وشركاه (ألمانيا)

- شركة كوفسترو (ألمانيا)

- ماركفورجيد، المحدودة (الولايات المتحدة)

- ستراتاسيس (الولايات المتحدة)

- إكس ون (الولايات المتحدة)

- أركيما (فرنسا)

- شركة 3D Systems, Inc. (الولايات المتحدة)

- شركة إيفونيك للصناعات (ألمانيا)

- ماترياليز (بلجيكا)

- شركة باسف إس إي (ألمانيا)

- شركة ساندفيك (السويد)

- سولفاي (بلجيكا)

ما هي التطورات الأخيرة في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا؟

- في أكتوبر 2023، أطلقت شركة EOS شبكة "مهندسي الرغوة الرقمية"، المصممة لتسريع تطوير وتصنيع المنتجات الاستهلاكية والطبية والصناعية التي تستخدم تطبيقات الرغوة الرقمية. "الرغوة الرقمية" ليست منتجًا، بل هي نهج لطباعة منتجات شبيهة بالرغوة ثلاثية الأبعاد. وستوفر هذه الشبكة توجهًا جديدًا للشركة في مجال مواد الطباعة ثلاثية الأبعاد.

- في أكتوبر 2023، أعلنت أركيما عن شراكات جديدة مع شركات رائدة في هذا المجال، مثل EOS وHP وStratasys، لتصميم الجيل القادم من مواد وحلول الطباعة ثلاثية الأبعاد. سيعزز هذا قدراتها الابتكارية ويعزز محفظة منتجاتها.

- في فبراير 2023، تعاونت شركة باور هوكي، الرائدة في أوروبا في مجال ابتكار معدات الهوكي، مع شركة EOS، الرائدة في مجال الطباعة ثلاثية الأبعاد الصناعية والرائدة في السوق، لدمج التصنيع الإضافي (AM، أو الطباعة ثلاثية الأبعاد) في برنامج MyBauer للمعدات المخصصة من باور. وقد منح نهج EOS الحاصل على براءة اختراع في طباعة البوليمرات باستخدام الرغوة الرقمية، شركة باور، ميزةً مميزة. وسيعزز هذا حضور EOS في سوق مواد الطباعة ثلاثية الأبعاد في أوروبا.

- في نوفمبر 2021، طرحت شركة Covestro AG أربع مواد جديدة للطباعة ثلاثية الأبعاد في معرض Formnext 2021، تغطي تقنيات متنوعة. من بينها Addigy FPC SOL1 HT، وهي مادة دعم قابلة للذوبان تُستخدم في طباعة FDM للمواد عالية الحرارة، وتتميز بسهولة إزالتها واستدامة أدائها. كما حققت مادة Arnitel AM3001 (P) المخصصة لـ SLS، وهي مادة ناعمة ذات عائد طاقة مرتفع، نجاحًا في الطباعة ثلاثية الأبعاد مع الالتزام بمعايير سلامة الألعاب. كما أطلقت Covestro إصدارات SLS وHSS من مسحوق TPU الخاص بها، Addigy PPU 86AW6، المعروف بقدرته على الارتداد، وسهولة معالجته لاحقًا، وارتفاع معدل إعادة استخدامه. تُوسّع هذه الإضافات خيارات Covestro من البوليمرات للطباعة ثلاثية الأبعاد، بعد استحواذها على أعمال التصنيع الإضافي التابعة لشركة DSM في وقت سابق من هذا العام.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.