North America Smart Home Market

Market Size in USD Billion

USD

79.65 Billion

USD

305.53 Billion

2025

2033

USD

79.65 Billion

USD

305.53 Billion

2025

2033

| 2026 - 2033 | |

| USD 79.65 Billion | |

| USD 305.53 Billion | |

| % | |

|

What is the North America Smart Home Market Size and Growth Rate?

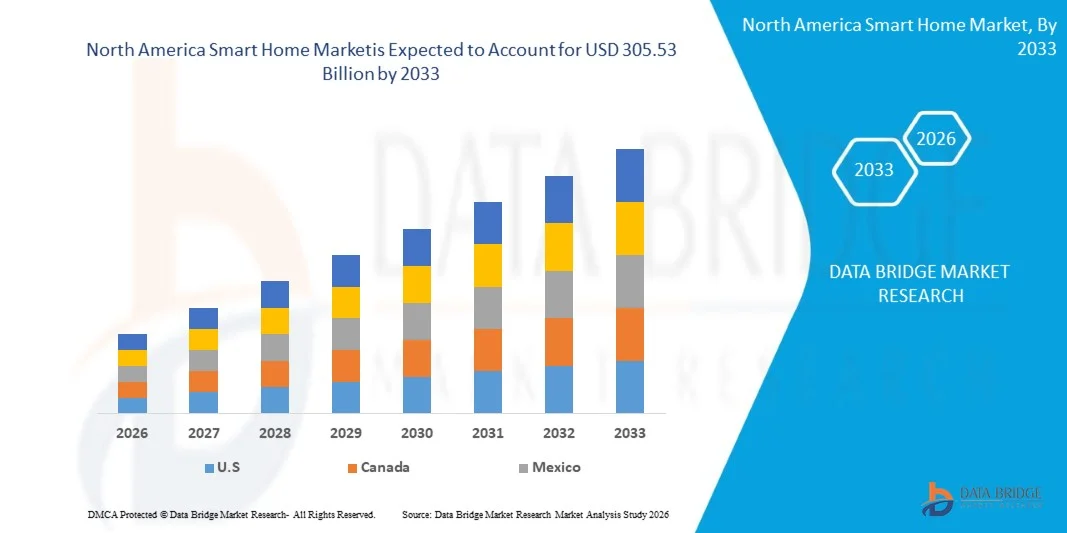

- As per Data Bridge Market Research Analysis the North America smart home market size was valued at USD 79.65 billion in 2025 and is expected to reach USD 305.53 billion by 2033, at a CAGR of 18.30% during the forecast period

- The market growth is largely fuelled by the increasing adoption of connected devices and rising demand for home automation solutions across residential sectors

- Growing consumer preference for enhanced security, energy efficiency, and convenience is further accelerating the adoption of smart home technologies

Market Size & Forecast

- North America Market Value (2025): USD 79.65 billion in 2025

- Expected Market Value (2033): USD 305.53 billion by 2033

- Forecast CAGR (2026–2033): 18.30%

North America Smart Home Market Analysis

- The market is experiencing rapid expansion driven by advancements in IoT, artificial intelligence, and wireless communication technologies enabling seamless integration of smart devices

- Increasing investments by technology companies and rising consumer awareness regarding smart living solutions are supporting continuous innovation and market growth

- U.S. smart home market dominated the North America region in 2025, driven by the high adoption of connected devices and the growing trend of home automation. Consumers are increasingly prioritizing convenience, security, and energy efficiency through the use of smart home solutions such as smart speakers, security systems, and intelligent lighting

- Canada is expected to witness the highest compound annual growth rate (CAGR) in the North America smart home market due to increasing consumer awareness, rising adoption of energy-efficient smart technologies, and supportive government initiatives promoting smart living solutions

- The security and access control segment held the largest market revenue share in 2025 driven by the increasing demand for home security solutions and rising adoption of smart locks, surveillance systems, and alarm systems. These solutions offer enhanced safety, remote monitoring, and real-time alerts, making them highly preferred among residential users. Increasing concerns regarding home safety and burglary prevention, along with integration with mobile applications and voice assistants, are further strengthening demand. In addition, continuous innovation in biometric authentication and AI-based monitoring systems is enhancing reliability and expanding adoption across both residential and small commercial applications

Report Scope and North America Smart Home Market Segmentation

|

Attributes |

North America Smart Home Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

What is the Key Trend in the North America Smart Home Market?

“Rising Adoption Of Connected And Intelligent Home Ecosystems”

- The growing demand for interconnected and automated living environments is significantly shaping the North America smart home market, as consumers increasingly prefer devices that offer convenience, security, and energy efficiency. Smart home solutions are gaining traction due to their ability to integrate multiple functions such as lighting, security, climate control, and entertainment into a unified system. This trend is strengthening adoption across residential applications and encouraging companies to develop more advanced and user-friendly solutions

- Increasing awareness regarding energy conservation and sustainable living has accelerated the demand for smart home technologies such as smart thermostats, lighting systems, and energy monitoring devices. Consumers are actively seeking solutions that optimize energy usage and reduce utility costs, prompting manufacturers to focus on eco-friendly innovations and intelligent automation features. This has also led to collaborations between technology providers and utility companies to enhance system efficiency

- Convenience and enhanced security are influencing purchasing decisions, with consumers prioritizing features such as remote access, voice control, and real-time monitoring. These capabilities are helping brands differentiate their offerings while improving user experience and trust. Companies are also focusing on integrating artificial intelligence and machine learning to enable predictive automation and personalized home environments

- For instance, in 2024, companies such as Amazon and Google expanded their smart home product portfolios by introducing advanced smart speakers, security systems, and home automation hubs. These products were designed to offer seamless integration and improved functionality, with availability across online and retail platforms. The solutions were also marketed as enhancing convenience, security, and energy efficiency, strengthening consumer adoption and brand loyalty

- While demand for smart home solutions is growing, sustained market expansion depends on addressing interoperability challenges, ensuring data privacy, and reducing product costs. Companies are focusing on developing standardized platforms, enhancing cybersecurity measures, and improving affordability to support wider adoption

North America Smart Home Market Dynamics

Driver

“Growing Demand For Convenience, Security, And Energy Efficiency”

- Rising consumer demand for convenience, safety, and efficient energy management is a major driver for the North America smart home market. Manufacturers are increasingly offering integrated solutions that enable remote control and automation of household systems, improving overall living standards and user experience. This trend is also driving innovation in AI-powered devices and IoT-enabled ecosystems

- Expanding applications across residential spaces are influencing market growth. Smart home devices such as security cameras, smart locks, lighting systems, and thermostats enhance safety, comfort, and operational efficiency, enabling consumers to manage their homes more effectively. The increasing adoption of connected lifestyles further reinforces this trend

- Technology providers are actively promoting smart home solutions through product innovation, partnerships, and ecosystem development. These efforts are supported by growing consumer awareness and the rising penetration of smartphones and high-speed internet, encouraging seamless integration and adoption of smart home devices

- For instance, in 2023, companies such as Apple and Samsung reported increased adoption of smart home ecosystems integrated with voice assistants and mobile applications. This expansion followed rising consumer demand for connected living solutions, driving repeat purchases and product differentiation. Both companies also emphasized privacy, security, and user-friendly interfaces to strengthen consumer trust and engagement

- Although increasing demand supports market growth, wider adoption depends on affordability, interoperability, and reliable connectivity. Investments in infrastructure, product standardization, and enhanced user education will be critical for sustaining long-term growth

Restraint/Challenge

“Data Privacy Concerns And High Initial Costs”

- Concerns related to data privacy and cybersecurity remain a key challenge, as smart home devices collect and process large volumes of personal data. Potential risks associated with unauthorized access and data breaches can limit consumer confidence and adoption. Manufacturers must invest in advanced security protocols and transparent data policies to address these concerns

- High initial costs associated with smart home systems also restrict adoption, particularly among price-sensitive consumers. Expenses related to device installation, integration, and maintenance contribute to overall cost, making it difficult for some households to adopt these technologies. Cost reduction and flexible pricing models are essential to improve accessibility

- Interoperability issues between devices from different manufacturers create additional challenges, as lack of standardization can limit seamless integration and user experience. Consumers often face difficulties in managing multiple platforms, which can hinder adoption and satisfaction

- For instance, in 2024, several consumers in the U.S. and Canada reported challenges related to compatibility between smart home devices from different brands, as well as concerns regarding data security and privacy. These issues impacted user experience and slowed adoption in certain segments, particularly among first-time users

- Overcoming these challenges will require improved cybersecurity measures, standardized communication protocols, and cost-effective product offerings. Collaboration between technology providers, regulators, and service providers will be essential to enhance trust, simplify integration, and support long-term market growth

North America Smart Home Market Scope

The market is segmented on the basis of product type, technology, software and service, and sales channel.

• By Product Type

On the basis of product type, the North America smart home market is segmented into Entertainment Controls, Security and Access Control, HVAC Control, Home Appliances, Smart Kitchen, Lighting Control, Smart Furniture, Home Healthcare, and Others. The security and access control segment held the largest market revenue share in 2025 driven by the increasing demand for home security solutions and rising adoption of smart locks, surveillance systems, and alarm systems. These solutions offer enhanced safety, remote monitoring, and real-time alerts, making them highly preferred among residential users. Increasing concerns regarding home safety and burglary prevention, along with integration with mobile applications and voice assistants, are further strengthening demand. In addition, continuous innovation in biometric authentication and AI-based monitoring systems is enhancing reliability and expanding adoption across both residential and small commercial applications.

The home healthcare segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the growing aging population and increasing demand for remote health monitoring solutions. Smart home healthcare devices enable continuous health tracking, emergency alerts, and improved patient care, supporting independent living and reducing healthcare costs. Rising prevalence of chronic diseases and increasing demand for telehealth services are accelerating adoption. Furthermore, integration with wearable devices and mobile health platforms, along with supportive government initiatives for healthcare digitization, is contributing to the expansion of this segment.

• By Technology

On the basis of technology, the market is segmented into Wireless and Wired. The wireless segment held the largest market revenue share in 2025 driven by ease of installation, flexibility, and widespread adoption of Wi-Fi, Bluetooth, and other wireless communication technologies. Wireless smart home systems allow seamless connectivity and remote access, making them a preferred choice for modern households. Rapid expansion of high-speed internet infrastructure and increasing compatibility with a wide range of devices are further supporting segment growth. In addition, rising consumer preference for DIY installation and advancements in low-power communication technologies are enhancing efficiency and adoption.

The wired segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its reliability, stable connectivity, and enhanced security features. Wired systems are often preferred in large-scale installations and new constructions where long-term performance and minimal interference are critical. Increasing deployment in premium housing projects and commercial settings is supporting growth. Moreover, improved data security, reduced latency, and consistent performance are encouraging adoption in environments requiring high reliability.

• By Software and Service

On the basis of software and service, the market is segmented into Behavioral and Proactive. The behavioral segment held the largest market revenue share in 2025 driven by its ability to automate devices based on user habits and preferences. Behavioral systems enhance convenience by learning user patterns and adjusting home settings accordingly, improving energy efficiency and comfort. Increasing adoption of AI-driven personalization and integration with smart ecosystems is strengthening this segment. In addition, rising demand for energy-saving solutions and automated control systems is further supporting growth.

The proactive segment is expected to witness the fastest growth rate from 2026 to 2033, driven by advancements in artificial intelligence and predictive analytics. Proactive systems can anticipate user needs, detect anomalies, and provide automated responses, enhancing security and operational efficiency within smart homes. Growing focus on predictive maintenance and real-time alerts is accelerating adoption. Furthermore, increasing integration with cloud computing and data analytics platforms is improving system intelligence and responsiveness.

• By Sales Channel

On the basis of sales channel, the market is segmented into Direct and Indirect. The indirect segment held the largest market revenue share in 2025 driven by the strong presence of retail stores, e-commerce platforms, and third-party distributors. Indirect channels offer wide product availability, competitive pricing, and convenience, supporting higher consumer adoption. Increasing growth of online retail platforms and digital marketing strategies is further expanding reach. In addition, partnerships with distributors and retailers are enhancing product visibility and accessibility.

The direct segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing preference for manufacturer-driven sales and customized solutions. Direct channels enable better customer engagement, after-sales support, and tailored smart home solutions, enhancing overall user experience. Growing adoption of brand-owned platforms and subscription-based services is supporting this trend. Moreover, direct interaction with customers allows companies to gather insights, improve offerings, and strengthen brand loyalty.

Which Region Holds the Largest Share of the North America Smart Home Market?

- U.S. smart home market dominated the North America region in 2025, driven by the high adoption of connected devices and the growing trend of home automation. Consumers are increasingly prioritizing convenience, security, and energy efficiency through the use of smart home solutions such as smart speakers, security systems, and intelligent lighting

- The strong presence of leading technology companies, along with advanced internet infrastructure and high disposable incomes, further supports market growth

- Moreover, increasing integration of artificial intelligence, voice assistants, and IoT-enabled ecosystems is significantly contributing to the expansion of the smart home market in the U.S.

Canada Smart Home Market Insight

The Canada smart home market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising adoption of smart technologies and increasing consumer awareness regarding energy efficiency and home security. Growing investments in digital infrastructure and supportive government initiatives promoting smart living solutions are accelerating market expansion. Consumers are increasingly adopting smart home devices such as thermostats, security systems, and connected appliances to enhance convenience and reduce energy consumption. In addition, the expansion of e-commerce platforms and increasing availability of affordable smart home products are further supporting market growth in Canada.

Which are the Top Companies in North America Smart Home Market?

The North America smart home industry is primarily led by well-established companies, including:

- Honeywell International Inc. (U.S.)

- Johnson Controls International plc (Ireland)

- Emerson Electric Co. (U.S.)

- Resideo Technologies, Inc. (U.S.)

- Lutron Electronics Co., Inc. (U.S.)

- Crestron Electronics, Inc. (U.S.)

- Savant Systems, Inc. (U.S.)

- ADT Inc. (U.S.)

- Vivint Smart Home, Inc. (U.S.)

- Alarm.com Holdings, Inc. (U.S.)

- Leviton Manufacturing Co., Inc. (U.S.)

- Acuity Brands, Inc. (U.S.)

- Universal Electronics Inc. (U.S.)

- Ecobee Inc. (Canada)

- Telus Corporation (Canada)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Smart Home Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Smart Home Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Smart Home Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.