North America Intraoperative Radiation Therapy Market

Market Size in USD Million

CAGR :

%

USD

116.39 Million

USD

192.62 Million

2025

2033

USD

116.39 Million

USD

192.62 Million

2025

2033

| 2026 –2033 | |

| USD 116.39 Million | |

| USD 192.62 Million | |

| % | |

|

North America Intraoperative Radiation Therapy Market Size

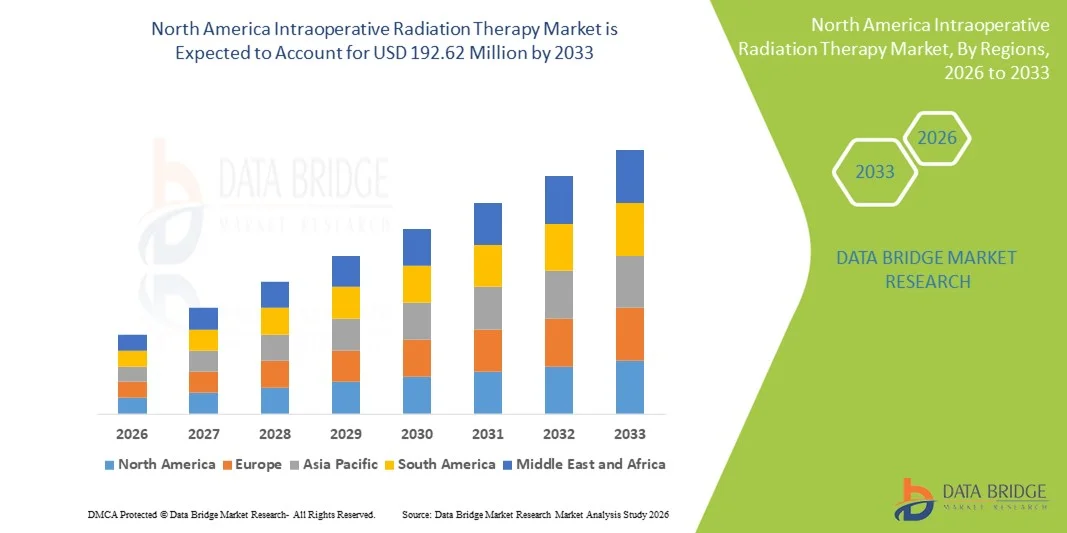

- The North America intraoperative radiation therapy market size was valued at USD 116.39 million in 2025 and is expected to reach USD 192.62 million by 2033, at a CAGR of 6.5% during the forecast period

- The market growth is largely driven by the rising prevalence of cancer, increasing adoption of advanced radiation oncology technologies, and the growing preference for targeted, single-dose radiation delivered during surgical procedures across major healthcare facilities

- Furthermore, strong healthcare infrastructure, high clinical awareness, favorable reimbursement frameworks, and the presence of leading medical device manufacturers are positioning intraoperative radiation therapy as an effective, time-efficient cancer treatment approach, thereby significantly supporting the region’s market growth

North America Intraoperative Radiation Therapy Market Analysis

- Intraoperative radiation therapy (IORT), delivering a concentrated dose of radiation directly to the tumor bed during surgery, is increasingly recognized as an effective cancer treatment modality across major hospitals and cancer centers in North America due to its precision, reduced damage to surrounding healthy tissues, and shortened overall treatment timelines

- The rising demand for IORT is primarily driven by the increasing prevalence of cancer, growing preference for minimally invasive and targeted therapies, and continuous technological advancements in radiation delivery systems and imaging integration

- The U.S. dominated the North America intraoperative radiation therapy market with the largest revenue share of 78.6% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative oncology technologies, and strong clinical evidence favoring IORT in breast, colorectal, and brain cancer treatments

- Canada is expected to witness steady growth during the forecast period due to expanding oncology care facilities, increasing healthcare investments, and rising awareness regarding the clinical and economic benefits of intraoperative radiation therapy

- Electron beam IORT dominated the North America intraoperative radiation therapy market with a market share of 62.3% in 2025, driven by their established clinical use, high precision in dose delivery, and widespread availability across leading cancer treatment centers

Report Scope and North America Intraoperative Radiation Therapy Market Segmentation

|

Attributes |

North America Intraoperative Radiation Therapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Intraoperative Radiation Therapy Market Trends

Rising Adoption of Precision-Focused, Single-Session Radiation Therapies

- A significant and accelerating trend in the North America intraoperative radiation therapy (IORT) market is the growing adoption of highly precise, single-dose radiation delivery during surgery, enabling improved local tumor control while minimizing exposure to surrounding healthy tissues

- For instance, leading cancer centers across the U.S. are increasingly deploying mobile electron and low-energy X-ray IORT systems that allow radiation to be administered immediately after tumor resection within the operating room setting

- Technological advancements in imaging guidance, applicator design, and dose modulation are enhancing the accuracy and safety of IORT procedures. For instance, modern systems enable real-time visualization and customized radiation delivery based on tumor location and surgical margins

- The integration of IORT into multidisciplinary cancer care pathways is facilitating shorter treatment durations compared to conventional external beam radiation therapy, thereby improving patient convenience and reducing hospital visits

- This trend toward more targeted, time-efficient, and patient-centric radiation solutions is reshaping clinical decision-making in oncology. Consequently, companies such as ZEISS and Eckert & Ziegler are focusing on compact, mobile IORT platforms optimized for surgical environments

- The demand for advanced IORT solutions is rising steadily across major North American hospitals, as healthcare providers prioritize precision oncology approaches that improve outcomes while optimizing operational efficiency

- Additionally, the increasing emphasis on value-based care models is prompting hospitals to adopt IORT solutions that reduce total treatment costs and resource utilization while maintaining high-quality outcomes

North America Intraoperative Radiation Therapy Market Dynamics

Driver

Increasing Cancer Burden and Demand for Targeted Treatment Approaches

- The increasing incidence of cancer across North America, combined with a growing emphasis on targeted and localized treatment modalities, is a major driver supporting the expansion of the intraoperative radiation therapy market

- For instance, in 2025, several U.S. academic medical centers expanded their breast and colorectal cancer programs to include IORT as part of standard surgical oncology protocols, highlighting rising clinical acceptance

- As healthcare providers seek to improve treatment outcomes while reducing radiation-related side effects, IORT offers the advantage of delivering a concentrated dose directly to the tumor bed, lowering recurrence risks

- Furthermore, strong healthcare infrastructure, high adoption of advanced medical technologies, and favorable reimbursement environments in the U.S. are encouraging hospitals to invest in IORT systems

- The ability of IORT to shorten overall treatment timelines, reduce the need for post-operative radiation sessions, and enhance patient quality of life is further propelling its adoption across North America

- Rising patient awareness regarding advanced cancer treatment options is also contributing to higher acceptance rates for IORT-based procedures

- Moreover, ongoing clinical trials and expanding indications for IORT across multiple tumor types are reinforcing long-term market growth prospect

Restraint/Challenge

High Capital Investment and Operational Complexity

- The high initial cost associated with acquiring and installing intraoperative radiation therapy systems presents a significant challenge to wider adoption, particularly for small and mid-sized hospitals

- For instance, the need for specialized shielding, operating room modifications, and trained multidisciplinary teams can substantially increase implementation expenses

- The complexity of integrating radiation delivery into surgical workflows requires extensive coordination between surgeons, radiation oncologists, and medical physicists, which may limit adoption in resource-constrained facilities

- Additionally, strict regulatory requirements related to radiation safety, equipment certification, and clinical protocols can lengthen approval timelines and increase compliance burdens

- Overcoming these challenges through technological innovations that reduce system costs, streamlined regulatory pathways, and expanded clinician training programs will be essential for sustained growth of the North America IORT market

- Limited availability of skilled professionals with expertise in IORT planning and delivery may further constrain adoption in certain regions

- Variability in reimbursement policies across states and healthcare systems can also create financial uncertainty, slowing investment decisions by hospitals and surgical centers

North America Intraoperative Radiation Therapy Market Scope

The market is segmented on the basis of method, product, type, application, end user, and distribution channel.

- By Method

On the basis of method, the North America intraoperative radiation therapy market is segmented into electron IORT, intraoperative brachytherapy, high dose-rate (HDR) IORT, X-ray IORT, and others. The electron IORT segment dominated the market with the largest revenue share of 62.3% in 2025, driven by its long-standing clinical adoption and widespread availability across leading cancer centers. Electron IORT enables precise dose delivery with controllable penetration depth, reducing radiation exposure to surrounding healthy tissues. Its effectiveness in breast cancer, colorectal cancer, and soft tissue sarcoma treatments has strengthened physician confidence. The availability of mobile electron accelerators further enhances operational flexibility within surgical environments. Strong clinical guidelines and extensive published evidence also support its routine use. Additionally, high familiarity among radiation oncologists continues to reinforce its dominant market position.

The X-ray IORT segment is expected to witness the fastest growth during the forecast period, fueled by increasing adoption of compact, low-energy X-ray systems. These systems require minimal shielding, making them easier to integrate into standard operating rooms. X-ray IORT is gaining strong traction in early-stage breast cancer treatments due to shorter procedure times. Improved portability allows hospitals to optimize space utilization. Technological advancements have enhanced dose uniformity and safety profiles. For instance, hospitals increasingly prefer X-ray IORT for same-day surgical and radiation workflows.

- By Product

On the basis of product, the market is segmented into intraoperative radiation therapy devices, intraoperative radiation therapy accessories, and software & services. The intraoperative radiation therapy devices segment dominated the market in 2025 due to high capital investments and increasing system installations. These devices are essential for delivering radiation during surgical procedures. Rising cancer prevalence across North America has increased demand for advanced radiation equipment. Hospitals prioritize device upgrades to improve accuracy and treatment outcomes. Strong replacement demand for next-generation systems also supports revenue dominance. Additionally, long procurement cycles and high unit prices significantly contribute to this segment’s leading share.

The software & services segment is anticipated to grow at the fastest rate during the forecast period, driven by rising demand for treatment planning and system optimization tools. Advanced software enables real-time dose calculation and workflow integration. Service contracts ensure regulatory compliance and equipment uptime. Increasing digitalization in radiation oncology is accelerating adoption. Hospitals are investing in analytics-driven platforms to improve efficiency. For instance, software upgrades are increasingly bundled with long-term service agreements.

- By Type

On the basis of type, the market is segmented into portable and benchtop systems. The portable segment dominated the North America IORT market in 2025, owing to its mobility and flexible deployment across operating rooms. Portable systems reduce the need for dedicated radiation suites. Hospitals benefit from improved equipment utilization and lower infrastructure costs. These systems support multidisciplinary surgical workflows. Growing adoption in breast and colorectal surgeries strengthens demand. Additionally, portability enables faster procedural turnaround times.

The benchtop segment is expected to grow at the fastest rate during the forecast period, driven by advances in compact system engineering. Benchtop systems offer enhanced precision for specialized procedures. Academic hospitals increasingly adopt these systems for controlled environments. Improved ergonomics and simplified operation support adoption. Technological improvements have reduced space requirements. For instance, specialty oncology centers favor benchtop systems for targeted applications.

- By Application

On the basis of application, the market is segmented into breast cancer, brain tumor, head & neck cancer, soft tissue sarcoma, pediatric tumors, gynecological cancer, genitourinary cancers, upper gastrointestinal tumors, and other cancers. The breast cancer segment dominated the market in 2025 due to strong clinical evidence supporting IORT use. High breast cancer incidence in North America drives consistent demand. IORT enables breast-conserving surgeries with reduced radiation sessions. Patients benefit from shorter treatment durations. Favorable reimbursement further accelerates adoption. Additionally, growing awareness among patients and clinicians reinforces segment leadership.

The upper gastrointestinal tumors segment is projected to be the fastest growing during the forecast period. Rising incidence of complex GI cancers is increasing treatment demand. IORT enables high-dose radiation at surgical margins. Advanced surgical techniques support its integration. Growing clinical research validates improved local control rates. For instance, specialized oncology centers increasingly adopt IORT in GI oncology programs. The segment benefits from the growing number of hospitals with hybrid ORs that can accommodate gynecological procedures.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centers, specialty centers, and others. The hospital segment dominated the market in 2025 due to advanced infrastructure availability. Hospitals support multidisciplinary oncology teams required for IORT. High patient volumes justify capital investments. Participation in clinical trials enhances adoption. Favorable reimbursement supports hospital-based treatments. Additionally, integrated cancer care models strengthen hospital dominance.

The specialty center segment is expected to grow at the fastest rate during the forecast period. The expansion of dedicated cancer centers is driving demand. These centers focus on advanced treatment differentiation. Patients increasingly prefer the specialized oncology facilities. Streamlined workflows improve procedural the efficiency. For instance, specialty centers adopt IORT to enhance the clinical outcomes. Collaboration with device manufacturers ensures the consistent technical support.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The direct tender segment dominated the market in 2025, driven by large-scale hospital procurement. Tender processes enable cost negotiation and customization. Public healthcare systems prefer structured purchasing models. Long-term service agreements enhance vendor relationships. Regulatory compliance is easier through tenders. Additionally, high-value equipment purchases favor this channel.

The retail sales segment is expected to witness the fastest growth during the forecast period. Private hospitals seek faster procurement cycles. Compact IORT systems support retail distribution. Distributor networks are expanding across North America. Growing private healthcare investments accelerate adoption. For instance, specialty centers increasingly purchase systems through retail channels. Retail channels allow smaller hospitals to gradually invest in advanced IORT technology without heavy upfront costs.

North America Intraoperative Radiation Therapy Market Regional Analysis

- The U.S. dominated the North America intraoperative radiation therapy market with the largest revenue share of 78.6% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative oncology technologies, and strong clinical evidence favoring IORT in breast, colorectal, and brain cancer treatments

- Healthcare providers in the U.S. strongly prioritize precision-based and time-efficient cancer treatment approaches, supporting widespread implementation of intraoperative radiation therapy across leading hospitals and comprehensive cancer centers

- This dominance is further reinforced by favorable reimbursement policies, high healthcare expenditure, strong clinical evidence, and the presence of major medical device manufacturers, establishing the U.S. as the core contributor to regional market growth

The U.S. Intraoperative Radiation Therapy Market Insight

The U.S. intraoperative radiation therapy market captured the largest revenue share within North America in 2025, driven by high cancer prevalence, advanced healthcare infrastructure, and early adoption of precision oncology technologies. Healthcare providers increasingly prioritize targeted, single-session radiation delivered during surgery to improve outcomes and reduce overall treatment timelines. Strong clinical evidence supporting IORT in breast, colorectal, and brain cancers continues to drive adoption. Favorable reimbursement policies and high healthcare spending further accelerate market growth. Moreover, the presence of leading medical device manufacturers and academic cancer centers significantly contributes to the market’s expansion.

Canada Intraoperative Radiation Therapy Market Insight

The Canada intraoperative radiation therapy market is experiencing steady growth, supported by a well-established public healthcare system and rising focus on advanced cancer treatment modalities. Increasing investments in oncology infrastructure and modernization of surgical facilities are enabling wider adoption of IORT technologies. Canadian hospitals are gradually integrating IORT into breast and gastrointestinal cancer treatment pathways. Growing awareness of the benefits of targeted, single-session radiation is supporting clinician acceptance. Additionally, government-backed healthcare funding and emphasis on patient-centered care are contributing to market development.

Mexico Intraoperative Radiation Therapy Market Insight

The Mexico intraoperative radiation therapy market is at an emerging stage but is expected to grow steadily during the forecast period. Expanding private healthcare facilities and increasing investments in advanced oncology technologies are supporting adoption. Large urban hospitals are beginning to incorporate IORT into surgical oncology practices to improve treatment precision. Rising cancer incidence and improving access to specialized cancer care are key growth drivers. Furthermore, collaborations with international medical device manufacturers are enhancing technology availability and clinical expertise in the country.

North America Intraoperative Radiation Therapy Market Share

The North America Intraoperative Radiation Therapy industry is primarily led by well-established companies, including:

- Elekta AB (Sweden)

- IntraOp Medical, Inc. (U.S.)

- Carl Zeiss Meditec AG (Germany)

- Eckert & Ziegler AG (Germany)

- iCAD, Inc. (U.S.)

- Sensus Healthcare, Inc. (U.S.)

- Ariane Medical Systems Ltd (U.K.)

- GMV Innovating Solutions S.L. (Spain)

- Ion Beam Applications SA (Belgium)

- IsoRay, Inc. (U.S.)

- Brainlab AG (Germany)

- Mevion Medical Systems, Inc. (U.S.)

- Xoft, Inc. (U.S.)

- Panacea Medical Technologies Pvt. Ltd. (India)

- REMEDI Co., Ltd. (South Korea)

- RaySearch Laboratories AB (Sweden)

- Sordina IORT Technologies (Italy)

- Zap Surgical Systems Inc. (U.S.)

- Varian Medical Systems, Inc. (U.S.)

What are the Recent Developments in North America Intraoperative Radiation Therapy Market?

- In September 2025, Varian Medical Systems (a Siemens Healthineers company) announced major advancements for its oncology treatment platforms, including precision radiotherapy systems that support intraoperative workflows and more integrated radiation delivery. These advancements aim to improve clinical outcomes and operational efficiency in surgical oncology departments, reflecting broader momentum in radiotherapy innovation

- In August 2025, mainstream cancer care organizations like the American Cancer Society updated patient-facing information on IORT, clarifying how IORT delivers high-dose radiation directly during surgery to minimize damage to surrounding tissues and potentially reduce the number of traditional post-operative radiotherapy sessions

- In May 2025, reputable clinical resources such as the Mayo Clinic published an informational overview on intraoperative radiation therapy, describing how multidisciplinary care teams use IORT during surgery to deliver targeted radiation while protecting healthy organs and outlining indications and preparation for patients

- In April 2025, Carl Zeiss Meditec received 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its INTRABEAM 700 system, a next-generation intraoperative radiation therapy platform designed to enhance precision oncology workflows in breast and neuro-oncology surgeries. The INTRABEAM 700 integrates robotic-assisted positioning, digital workflow tools, and advanced applicators to improve radiation delivery accuracy and streamline intraoperative use

- In October 2024, Varian Medical Systems entered into a strategic collaboration with Sun Nuclear to integrate SunCHECK quality assurance software into its radiation therapy ecosystem, enhancing automated verification of radiation delivery and consistency for advanced treatments used in surgical oncology settings. This partnership supports improved safety and reliability during complex intraoperative and perioperative radiotherapy procedures

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.