North America Cardiopulmonary Bypass Accessory Equipment Market

Market Size in USD Billion

CAGR :

%

USD

8.97 Billion

USD

14.08 Billion

2025

2033

USD

8.97 Billion

USD

14.08 Billion

2025

2033

| 2026 –2033 | |

| USD 8.97 Billion | |

| USD 14.08 Billion | |

| % | |

|

North America Cardiopulmonary Bypass Accessory Equipment Market Size

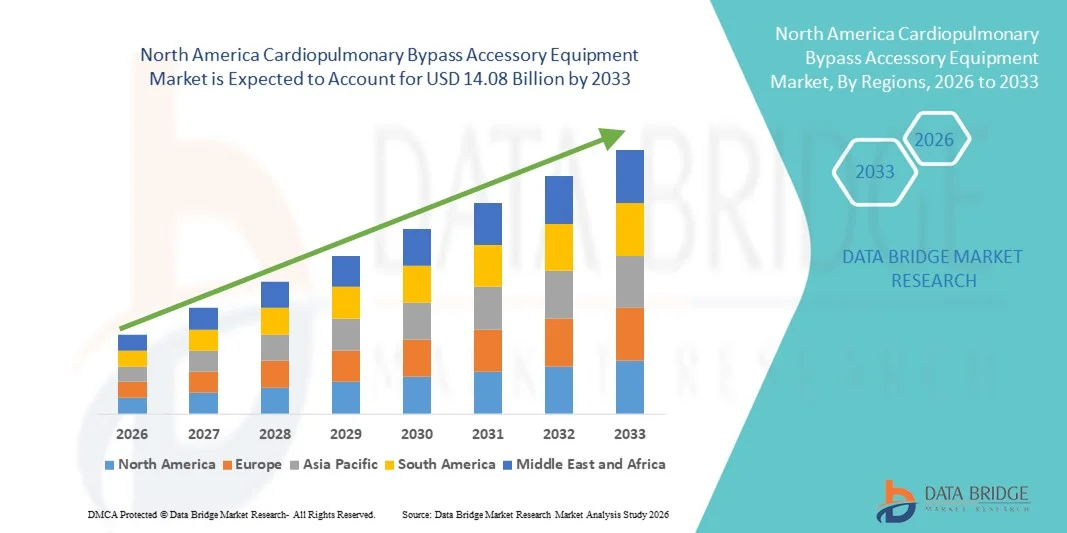

- The North America cardiopulmonary bypass accessory equipment market size was valued at USD 8.97 billion in 2025 and is expected to reach USD 14.08 billion by 2033, at a CAGR of 5.8% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular diseases, increasing number of cardiac surgeries and ongoing technological advancements in extracorporeal circulation and perfusion systems that enhance procedural efficiency and patient safety

- Furthermore, strong healthcare infrastructure, high healthcare expenditure, favorable reimbursement policies, and the adoption of advanced accessory devices such as oxygenators, cannulae, filters and heat exchangers are driving demand across hospitals, cardiac centers and ambulatory surgical settings, making cardiopulmonary bypass accessory equipment the preferred choice for modern cardiac care

North America Cardiopulmonary Bypass Accessory Equipment Market Analysis

- Cardiopulmonary bypass accessory equipment, including oxygenators, cannulae, filters, and heat exchangers, are critical components of cardiac surgeries and extracorporeal circulation procedures in hospitals and ambulatory surgical centers due to their ability to enhance patient safety, procedural efficiency, and clinical outcomes

- The growing demand for these devices is primarily driven by the increasing prevalence of cardiovascular diseases, rising number of cardiac surgeries, and continuous technological advancements in perfusion systems that improve reliability, precision, and integration with modern surgical equipment

- The U.S. dominated the cardiopulmonary bypass accessory equipment market with the largest revenue share of 79.5% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, favorable reimbursement policies, and a strong presence of leading industry players, with substantial adoption across cardiac centers and hospitals driven by innovations in minimally invasive perfusion and modular accessory systems

- Canada is expected to be the fastest-growing country in the cardiopulmonary bypass accessory equipment market during the forecast period due to increasing investments in healthcare infrastructure, expanding cardiac care facilities, and growing awareness of advanced surgical technologies

- Oxygenator segment dominated the cardiopulmonary bypass accessory equipment market with a market share of 38.7% in 2025, attributed to its crucial role in maintaining effective gas exchange and established preference among perfusionists and cardiac surgeons

Report Scope and North America Cardiopulmonary Bypass Accessory Equipment Market Segmentation

|

Attributes |

North America Cardiopulmonary Bypass Accessory Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Cardiopulmonary Bypass Accessory Equipment Market Trends

Technological Advancements and Integration with Perfusion Systems

- A significant and accelerating trend in the North America cardiopulmonary bypass accessory equipment market is the integration of advanced perfusion technologies and modular surgical systems, enhancing operational efficiency and patient safety during cardiac procedures

- For instance, oxygenators and heat exchangers are being increasingly designed to integrate seamlessly with automated perfusion devices, reducing human error and streamlining surgical workflows

- Advancements in sensor-enabled cannulae and filters enable real-time monitoring of blood flow, pressure, and oxygenation, allowing perfusionists to make rapid, informed adjustments. For instance, some modern centrifugal pumps include AI-assisted algorithms to optimize flow based on patient-specific hemodynamics

- This trend towards more intelligent, interconnected, and automated accessory equipment is fundamentally reshaping clinical expectations for cardiac surgery. For instance, companies such as Medtronic and Terumo are developing oxygenators and filters compatible with automated monitoring and adaptive flow control systems

- The adoption of such advanced and integrated cardiopulmonary bypass devices is growing rapidly across U.S. hospitals and cardiac centers, as clinical staff increasingly prioritize precision, safety, and seamless integration with existing surgical equipment

- Enhanced connectivity features are also enabling remote support and troubleshooting for perfusion equipment, allowing hospitals to access expert guidance during complex surgeries and reducing the likelihood of procedural delays

North America Cardiopulmonary Bypass Accessory Equipment Market Dynamics

Driver

Increasing Cardiac Surgery Volumes and Disease Prevalence

- The rising prevalence of cardiovascular diseases, coupled with the growing number of cardiac surgeries, is a significant driver for heightened demand for cardiopulmonary bypass accessory equipment

- For instance, in March 2025, Terumo Cardiovascular announced the launch of an advanced oxygenator designed for improved gas exchange efficiency during prolonged bypass procedures, demonstrating industry focus on innovation

- As hospitals and cardiac centers seek to enhance patient safety and surgical outcomes, accessories such as filters, cannulae, and oxygenators provide critical support in maintaining stable perfusion and hemodynamics

- Furthermore, the increasing adoption of minimally invasive and complex cardiac surgeries is expanding the need for precise, modular, and compatible bypass accessory systems

- The demand for equipment that offers real-time monitoring, reliable integration with perfusion devices, and compatibility across multiple surgical setups is driving adoption in the U.S., as clinical staff increasingly prioritize efficiency, safety, and procedural standardization

- For instance, growing awareness among surgeons about perfusion-related complications is driving investments in advanced monitoring accessories to improve patient outcomes

- Technological collaborations between equipment manufacturers and hospitals are also fueling innovation in bypass accessories, leading to faster adoption of next-generation devices

Restraint/Challenge

High Costs and Regulatory Compliance Requirements

- The relatively high cost of advanced cardiopulmonary bypass accessory devices, combined with stringent regulatory requirements, poses a challenge to broader market penetration

- For instance, smaller hospitals or clinics may delay upgrades to the latest oxygenators or filters due to budget constraints, limiting adoption in cost-sensitive settings

- Compliance with FDA and ISO standards, along with the need for extensive validation and clinical testing, adds complexity and increases the time to market for new devices. For instance, new cannula designs must undergo rigorous performance and biocompatibility testing before approval

- While innovations improve clinical outcomes, the upfront investment required for advanced perfusion equipment can hinder procurement in certain U.S. hospitals, particularly in smaller or regional facilities

- Overcoming these challenges through cost-optimization strategies, streamlined regulatory pathways, and targeted clinical education will be vital for sustained growth and broader adoption of cardiopulmonary bypass accessory equipment

- For instance, hospitals are exploring leasing models or bundled procurement of perfusion accessories to reduce upfront costs and improve access to the latest technologies

- Increasing competition among manufacturers is also driving innovation while putting pressure on prices, helping more hospitals adopt advanced bypass accessory systems despite budget constraints

North America Cardiopulmonary Bypass Accessory Equipment Market Scope

The market is segmented on the basis of product, operation, application, age, end user, and distribution channel.

- By Product

On the basis of product, the market is segmented into oxygenator, ECMO machine, pumps, cannula, temperature monitors, heat exchanger, filters, tubing clamps, hemoconcentrators, system panel, sensor and accessories, cardioplegia control, reservoir, bubble detector, electronic gas blender, electrical venous occluder, venous line clamp and accessories. The Oxygenator segment dominated the market with the largest revenue share of 38.7% in 2025, driven by its critical role in maintaining effective gas exchange during cardiopulmonary bypass procedures. Oxygenators are widely adopted across cardiac surgeries, acute respiratory failure treatments, and transplant operations due to their reliability, ease of use, and compatibility with modular perfusion systems. Hospitals and cardiac centers prefer oxygenators for their proven safety profile and consistent performance during high-risk procedures. Technological advancements such as integrated sensors and AI-assisted flow optimization further strengthen the dominance of this segment. Moreover, oxygenators are essential in minimizing complications and ensuring patient survival during complex surgeries, making them a cornerstone of bypass accessory equipment.

The ECMO Machine segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing cases of acute respiratory failure and critical care applications. ECMO machines offer life-saving support for patients with severe cardiopulmonary conditions and are increasingly used in pediatric and geriatric intensive care units. Technological improvements, including portable and modular ECMO systems, are expanding adoption in both tertiary hospitals and specialized cardiac centers. Rising awareness of ECMO therapy among clinicians, coupled with better training and infrastructure, is driving growth. The COVID-19 pandemic and other respiratory emergencies have also highlighted the importance of ECMO systems, accelerating demand. The segment benefits from ongoing innovation in automated monitoring, oxygenation efficiency, and perfusion control.

- By Operation

On the basis of operation, the market is segmented into manually operated, electrically operated, and battery operated. The Electrically Operated segment dominated the market in 2025 due to its precision, automation capabilities, and ability to integrate with modern surgical perfusion systems. Hospitals increasingly prefer electrically operated pumps, cannulae, and oxygenators for consistent blood flow and reduced manual intervention during complex procedures. This segment allows real-time monitoring, adaptive flow control, and alerts for perfusionists, improving patient safety and surgical efficiency. The integration of electrical operation with digital dashboards and perfusion consoles enhances compatibility with hospital information systems. Surgeons and perfusionists value the reliability, reproducibility, and reduced workload offered by electrically operated devices. Continuous technological upgrades, such as AI-assisted flow adjustments, further reinforce dominance.

The Battery Operated segment is anticipated to witness the fastest growth from 2026 to 2033, driven by portability requirements in ambulatory surgical centers and emergency cardiac care. Battery-operated pumps, oxygenators, and ECMO systems provide flexibility during transport, offsite procedures, and power-sensitive environments. Improved battery life, lightweight designs, and modular configurations are boosting adoption in critical care settings. Rising demand in pediatric and geriatric applications, where equipment mobility is crucial, further fuels growth. Manufacturers are focusing on reliability and safety features, including backup power and automated flow regulation. The segment is gaining popularity in remote and smaller healthcare facilities seeking high-quality bypass solutions without permanent electrical infrastructure.

- By Application

On the basis of application, the market is segmented into cardiac surgery, cardiac surgery oxygenators, acute respiratory failure treatment, lung cancer, transplant operation, and others. The Cardiac Surgery segment dominated the market with the largest revenue share in 2025, driven by the consistently high volume of open-heart and minimally invasive cardiac procedures in U.S. hospitals. Cardiopulmonary bypass accessories such as oxygenators, cannulae, filters, and heat exchangers are essential for maintaining patient stability during surgery. Surgeons rely on high-precision, validated devices for perfusion, reducing the risk of complications. The availability of advanced monitoring systems integrated with surgical dashboards further strengthens this segment. Hospitals prioritize standardized, reliable equipment that ensures procedural efficiency and patient safety. Technological innovations, including AI-assisted flow optimization and automated safety alerts, enhance surgical outcomes.

The Acute Respiratory Failure Treatment segment is expected to witness the fastest growth from 2026 to 2033 due to increasing prevalence of respiratory diseases and ICU admissions. ECMO machines, oxygenators, and associated perfusion accessories are increasingly adopted for critical care management. Rising awareness among clinicians, improved training in ECMO therapy, and enhanced device portability are driving adoption. Advanced monitoring, integration with ventilators, and improved oxygenation efficiency are key factors fueling growth. Pediatric and geriatric patients benefit from these applications, contributing to the segment’s expansion. Hospitals and cardiac centers are investing in specialized equipment to handle acute respiratory emergencies efficiently.

- By Age

On the basis of age, the market is segmented into adult, geriatric, and pediatric. The Adult segment dominated the market in 2025 due to the high prevalence of cardiovascular diseases and the majority of cardiac surgeries being performed on adult patients. Cardiopulmonary bypass accessory equipment such as oxygenators, pumps, and cannulae are extensively used in adult cardiac surgeries, transplant operations, and critical care procedures. Hospitals prioritize devices that provide reliable performance, minimize complications, and integrate with perfusion monitoring systems. Technological improvements, such as AI-assisted monitoring and automated alerts, enhance the safety and efficiency of adult bypass procedures. The large adult patient pool in the U.S., combined with advanced hospital infrastructure, supports the segment’s dominance. Standardized adult perfusion systems also ensure repeatable outcomes, contributing to sustained market leadership.

The Pediatric segment is expected to witness the fastest growth from 2026 to 2033 due to rising awareness of congenital heart defects and the need for specialized bypass equipment for children. Pediatric oxygenators, ECMO machines, and pumps are designed for smaller blood volumes and sensitive hemodynamics. Increasing pediatric cardiac surgeries and neonatal ICU care are boosting demand. Manufacturers are introducing modular, lightweight, and sensor-integrated devices for pediatric applications. Growth is further driven by hospitals investing in specialized pediatric cardiac care facilities. Technological enhancements and training programs for clinicians handling pediatric cases contribute to rapid adoption.

- By End User

On the basis of end user, the market is segmented into hospitals, cardiac centers, research and academic institutions, ambulatory surgical centers, and others. The Hospitals segment dominated the market in 2025, driven by the high volume of cardiac surgeries, transplant operations, and ICU treatments requiring cardiopulmonary bypass accessories. Hospitals prefer advanced oxygenators, pumps, and monitoring systems for reliable and efficient perfusion management. Integration with hospital dashboards and patient monitoring systems enhances workflow efficiency and patient safety. Availability of specialized surgical teams and perfusionists supports adoption. Technological advancements, including automated monitoring and AI-assisted alerts, are widely deployed in hospitals. The large infrastructure and investment capabilities of hospitals further reinforce dominance.

The Ambulatory Surgical Centers segment is expected to witness the fastest growth from 2026 to 2033 due to rising outpatient cardiac procedures and minimally invasive surgeries. Portable ECMO systems, battery-operated pumps, and compact oxygenators are increasingly adopted in these settings. Ambulatory centers benefit from lightweight, modular, and easy-to-use devices. Cost-efficiency and flexible workflow management are key drivers for adoption. Growing patient preference for outpatient procedures is boosting demand. Manufacturers are developing devices tailored for rapid deployment and mobile cardiac care, supporting segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third party distributor, and retail sales. The Direct Tender segment dominated the market in 2025, driven by hospitals and cardiac centers preferring direct procurement from manufacturers to ensure product authenticity, compliance, and timely delivery of critical cardiopulmonary bypass equipment. Direct tenders allow customization, bulk procurement, and access to technical support for complex devices. Hospitals benefit from manufacturer training programs, after-sales service, and installation support. Long-term contracts through direct tender agreements ensure consistent supply of oxygenators, pumps, and cannulae. Compliance with regulatory standards is easier through direct dealings. The reliability, trust, and manufacturer support reinforce dominance of this channel.

The Third Party Distributor segment is expected to witness the fastest growth from 2026 to 2033 due to increasing demand in smaller hospitals, ambulatory centers, and remote healthcare facilities. Distributors offer access to a wide range of products, competitive pricing, and flexible delivery options. Hospitals with limited procurement budgets benefit from distributor networks. Third-party distribution also supports rapid adoption of new technology by bridging manufacturers and end users. Training and support services provided by distributors further enhance market penetration. Rising demand for efficient, cost-effective supply chains drives segment growth.

North America Cardiopulmonary Bypass Accessory Equipment Market Regional Analysis

- The U.S. dominated the cardiopulmonary bypass accessory equipment market with the largest revenue share of 79.5% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, favorable reimbursement policies, and a strong presence of leading industry players

- Hospitals and cardiac centers in the U.S. highly prioritize patient safety, procedural efficiency, and reliable perfusion, leading to widespread adoption of oxygenators, pumps, cannulae, and other critical bypass accessories

- This strong market presence is further supported by high healthcare expenditure, favorable reimbursement policies, technological innovation in perfusion systems, and the presence of leading medical device manufacturers, establishing the U.S. as the key market for cardiopulmonary bypass accessory equipment in North America

The U.S. Cardiopulmonary Bypass Accessory Equipment Market Insight

The U.S. cardiopulmonary bypass accessory equipment market captured the largest revenue share of 79.5% in 2025 within North America, fueled by the widespread use of cardiopulmonary bypass systems in tertiary care hospitals and the increasing prevalence of heart disease. Hospitals and cardiac centers are prioritizing advanced perfusion equipment such as oxygenators, pumps, and monitoring systems to improve surgical safety and outcomes. The adoption of minimally invasive procedures, automated perfusion technologies, and AI‑enabled monitoring solutions is further propelling market growth. Robust healthcare infrastructure, favorable reimbursement policies, and presence of key medical device manufacturers reinforce the U.S. market’s leadership. Moreover, high procedure volumes for cardiac surgeries and critical care treatments sustain strong demand for bypass accessory devices.

Canada Cardiopulmonary Bypass Accessory Equipment Market Insight

The Canada cardiopulmonary bypass accessory equipment market is expected to grow at a noteworthy CAGR during the forecast period, driven by rising healthcare investments and expanding cardiac care facilities across the country. Canadian hospitals are increasingly adopting advanced equipment such as ECMO machines, oxygenators, and sensor‑integrated perfusion accessories to enhance patient safety and procedural efficiency. Government initiatives supporting healthcare modernization and the upgrade of surgical infrastructure are contributing to the adoption of next‑generation bypass solutions. Further, growing awareness of cardiovascular diseases and demand for high‑precision monitoring in cardiac surgeries are boosting market growth. Enhanced training programs for perfusionists and clinicians also support greater adoption of sophisticated bypass accessories in Canada.

Mexico Cardiopulmonary Bypass Accessory Equipment Market Insight

The Mexico cardiopulmonary bypass accessory equipment market is poised for gradual expansion during the forecast period as healthcare reforms and infrastructure developments improve the quality of cardiac care services. Increasing investments in medical technologies, alongside rising awareness of cardiovascular disease treatment options, are driving demand for bypass accessory equipment in tertiary hospitals and specialized cardiac centers. Efforts by public and private healthcare providers to upgrade surgical facilities and adopt advanced perfusion systems are supporting market uptake. However, market growth is currently more modest compared to the U.S. and Canada due to comparatively lower procedure volumes and healthcare spending. Continued improvement in regulatory frameworks and access to advanced equipment is expected to further enhance market growth

North America Cardiopulmonary Bypass Accessory Equipment Market Share

The North America Cardiopulmonary Bypass Accessory Equipment industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- LivaNova PLC (U.K.)

- Braile Biomédica (Brazil)

- Teleflex Incorporated (U.S.)

- Getinge AB (Sweden)

- Terumo Corporation (Japan)

- Surge Cardiovascular (U.S.)

- Abbott (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- SCHNELL MEDICAL Corp. (Switzerland)

- NIPRO Corporation (Japan)

- XENIOS AG (Germany)

- Advin Health Care (India)

- Boston Scientific Corporation (U.S.)

- APC Cardiovascular Ltd (U.K.)

- MicroPort Scientific Corporation (China)

- Alung Technologies, Inc. (U.S.)

- Berlin Heart (Germany)

- Jarvik Heart, Inc. (U.S.)

- Narang Medical Limited (India)

- Technowood International Pte. Ltd. (Singapore)

What are the Recent Developments in North America Cardiopulmonary Bypass Accessory Equipment Market?

- In September 2024, Medtronic plc launched the VitalFlow™ Extracorporeal Membrane Oxygenation (ECMO) System in the United States, introducing a configurable one‑system ECMO solution designed to bridge bedside care and intra‑hospital transport with a user‑friendly interface and integrated performance data support, further expanding its cardiac surgery and perfusion device portfolio after its acquisition of MC3 Cardiopulmonary

- In August 2024, Inspira™ Technologies announced that its INSPIRA™ ART100 system received FDA 510(k) clearance for cardiopulmonary bypass procedures, marking a significant regulatory milestone for this extracorporeal circulation and oxygenation device and enabling its commercial launch in the U.S. healthcare market. The clearance confirms the ART100’s safety and effectiveness for temporary blood oxygenation and circulation support

- In May 2024, Terumo Cardiovascular announced that the U.S. Food and Drug Administration (FDA) granted 510(k) clearance to its CDI OneView™ Monitoring System, an advanced modular platform providing up to 22 essential patient parameters during cardiopulmonary bypass surgery, offering perfusion teams greater visibility and configurability to support safer clinical outcomes during complex procedures

- In May 2024, the U.S. FDA issued a safety communication advising healthcare providers to transition away from certain Getinge/Maquet cardiovascular devices, including the Cardiohelp system and associated bypass components, due to ongoing quality and safety concerns despite multiple voluntary recalls, prompting hospitals to consider alternative perfusion and bypass solutions

- In March 2023, LivaNova received FDA 510(k) clearance for its Essenz Heart‑Lung Machine (HLM) and Essenz Patient Monitor, marking the U.S. introduction of the Essenz Perfusion System designed to improve clinical workflows with individualized pump control, automated sensor checks, and enhanced disposables positioning to support tailored cardiopulmonary bypass procedures

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.