Global Wholesale And Distribution Automotive After Market

Market Size in USD Billion

CAGR :

%

USD

221.32 Billion

USD

339.66 Billion

2025

2033

USD

221.32 Billion

USD

339.66 Billion

2025

2033

| 2026 –2033 | |

| USD 221.32 Billion | |

| USD 339.66 Billion | |

| % | |

|

Wholesale and Distribution Automotive Market Size

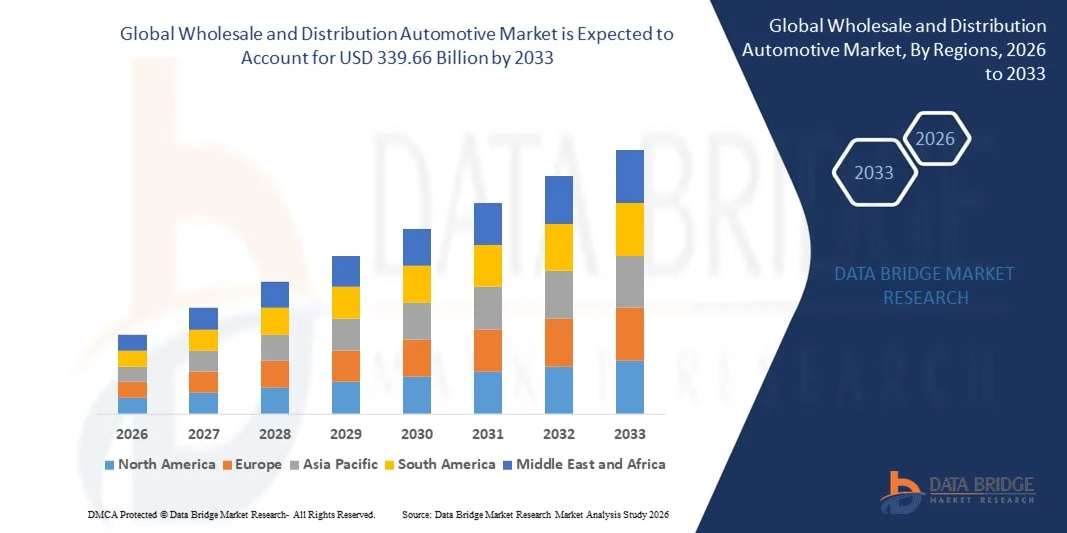

- The global wholesale and distribution automotive market size was valued at USD 221.32 billion in 2025 and is expected to reach USD 339.66 billion by 2033, at a CAGR of 5.50% during the forecast period

- The market growth is largely fuelled by the increasing demand for aftermarket automotive parts, expansion of e-commerce platforms for automotive distribution, and growing vehicle parc across emerging economies

- In addition, rising adoption of electric vehicles and the need for specialized components and parts are further driving market growth

Wholesale and Distribution Automotive Market Analysis

- The market is witnessing transformation due to the integration of digital distribution channels, supply chain optimization, and advanced inventory management solutions

- Increasing collaborations between manufacturers, distributors, and retailers are enhancing the availability and efficiency of automotive parts delivery, strengthening the overall market landscape

- North America dominated the wholesale and distribution automotive market with the largest revenue share of 25.3% in 2025, driven by a well-established automotive industry, strong aftermarket demand, and high adoption of digital distribution channels

- Asia-Pacific region is expected to witness the highest growth rate in the global wholesale and distribution automotive market, driven by increasing vehicle parc, rising disposable incomes, growing adoption of aftermarket services, and expansion of efficient logistics and distribution networks across emerging economies

- The tire segment held the largest market revenue share in 2025, driven by high replacement frequency, widespread vehicle usage, and increasing demand for durable and performance-oriented tires. Tires are essential for vehicle safety and efficiency, making them a key focus for distributors and retailers.

Report Scope and Wholesale and Distribution Automotive Market Segmentation

|

Attributes |

Wholesale and Distribution Automotive Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Wholesale and Distribution Automotive Market Trends

Rising Demand for E-Commerce and Efficient Distribution Channels

- The growing focus on digital sales platforms and streamlined supply chains is significantly shaping the wholesale and distribution automotive market, as businesses increasingly prefer channels that offer faster delivery, wider product selection, and reliable inventory management. Online and omnichannel distribution solutions are gaining traction due to their ability to reduce operational costs, improve service efficiency, and enhance customer satisfaction, encouraging distributors to adopt innovative logistics and digital tools

- Increasing awareness around vehicle maintenance, aftermarket parts availability, and convenient ordering options has accelerated the adoption of wholesale and distribution automotive services in passenger vehicles, commercial vehicles, and specialty segments. Consumers and fleet operators are actively seeking faster, more accessible channels for spare parts and accessories, prompting companies to strengthen partnerships with distributors and e-commerce platforms

- Technological advancements, such as AI-based inventory management, predictive analytics, and automated warehousing, are influencing purchasing decisions, with distributors emphasizing faster turnaround times, transparent supply chains, and real-time tracking. These factors help automotive companies differentiate themselves in a competitive market while improving operational efficiency and customer satisfaction

- For instance, in 2024, AutoZone in the U.S. and LKQ Corporation expanded their digital distribution networks and integrated e-commerce platforms for spare parts and accessories. These initiatives were introduced in response to rising demand for faster, more convenient parts delivery and wider product availability, with distribution across retail stores, online marketplaces, and fleet servicing channels

- While demand for efficient wholesale and distribution channels is growing, sustained market expansion depends on continuous investment in logistics infrastructure, digital platforms, and supply chain reliability. Companies are also focusing on optimizing inventory management, delivery networks, and order fulfillment to balance cost, speed, and service quality for broader adoption

Wholesale and Distribution Automotive Market Dynamics

Driver

Growing Adoption of E-Commerce And Omnichannel Distribution

- Rising demand for faster, more convenient ordering and delivery solutions is a major driver for the wholesale and distribution automotive market. Distributors are increasingly integrating online platforms with traditional retail networks to meet consumer expectations, improve product availability, and expand market reach

- Expanding automotive aftermarket, fleet management, and replacement parts segments are influencing market growth. Efficient distribution channels help ensure timely delivery, reduce downtime, and maintain vehicle performance, meeting the increasing demand for high-quality parts and services

- Automotive manufacturers and distributors are actively promoting digital sales and streamlined supply chains through partnerships, technology adoption, and improved logistics. These efforts are supported by growing vehicle ownership, urbanization, and the shift toward connected and electric vehicles, which require specialized distribution solutions

- For instance, in 2023, Advance Auto Parts in the U.S. and Brembo in Italy reported enhanced distribution efficiency by integrating digital order tracking and warehouse automation. This expansion followed higher demand for timely delivery of automotive parts and accessories, strengthening customer satisfaction and loyalty

- Although rising e-commerce and omnichannel adoption support growth, wider market penetration depends on logistics optimization, cost management, and technological investments. Investment in warehouse automation, AI-enabled inventory tracking, and robust delivery networks will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Operational Costs And Complex Supply Chain Management

- The relatively high operational cost of maintaining extensive distribution networks, warehousing, and last-mile delivery remains a key challenge, limiting profitability for some distributors. Rising fuel costs, labor expenses, and technology investments contribute to elevated operating costs

- Market awareness and digital adoption remain uneven, particularly in emerging economies where online and omnichannel distribution is still developing. Limited understanding of e-commerce and logistics efficiency restricts market growth in certain regions

- Supply chain complexities also impact market expansion, as automotive parts distribution requires coordination among manufacturers, wholesalers, retailers, and service providers. Delays, inventory mismanagement, and logistical inefficiencies can affect service quality and customer satisfaction

- For instance, in 2024, distributors in India and Southeast Asia supplying aftermarket parts to automotive service providers reported slower growth due to high operational costs and limited digital adoption. Infrastructure limitations and fragmented supply networks were additional barriers, affecting timely delivery and market reach

- Overcoming these challenges will require investment in cost-efficient logistics, digital supply chain platforms, and education for distributors and retailers. Collaboration with manufacturers, e-commerce platforms, and fleet operators can help unlock the long-term growth potential of the global wholesale and distribution automotive market. Furthermore, optimizing delivery networks and inventory management will be essential for widespread adoption

Wholesale and Distribution Automotive Market Scope

The market is segmented on the basis of replacement part, certification, distribution channel, and service channel.

- By Replacement Part

On the basis of replacement part, the wholesale and distribution automotive market is segmented into tire, battery, brake parts, filters, body parts, lighting and electronic components, wheels, exhaust components, and others. The tire segment held the largest market revenue share in 2025, driven by high replacement frequency, widespread vehicle usage, and increasing demand for durable and performance-oriented tires. Tires are essential for vehicle safety and efficiency, making them a key focus for distributors and retailers.

The battery segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising adoption of electric vehicles and hybrid vehicles, which require frequent replacement and advanced battery technologies. Battery replacement demand is further fueled by consumer preference for longer-lasting, high-capacity batteries and the increasing use of battery management systems in modern vehicles.

- By Certification

On the basis of certification, the market is segmented into genuine parts, certified parts, and uncertified parts. The genuine parts segment held the largest market revenue share in 2025, fueled by consumer preference for original equipment manufacturer (OEM) quality, reliability, and warranty assurance. Genuine parts are widely sought after by vehicle owners and service centers to maintain vehicle performance and safety standards.

The certified parts segment is expected to witness the fastest growth rate from 2026 to 2033, driven by regulatory compliance requirements, rising awareness of safety standards, and the increasing availability of certified aftermarket components. Certified parts offer verified quality and performance while often being more cost-effective than OEM parts.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into retailers, wholesalers, and distributors. The retailers segment held the largest revenue share in 2025, driven by the accessibility of automotive parts to end consumers, the expansion of retail networks, and growing online sales channels. Retailers often combine physical stores and e-commerce platforms to provide convenient purchasing options.

The distributors segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the increasing demand for bulk supply, fleet management services, and partnerships with automotive manufacturers. Distributors provide efficient supply chain solutions and enable wider market penetration for replacement parts.

- By Service Channel

On the basis of service channel, the market is segmented into DIY, DIFM (Do It For Me), and OEM. The DIFM segment held the largest market revenue share in 2025, driven by vehicle owners’ preference for professional installation, convenience, and assurance of proper fitment and performance. DIFM services are commonly offered by service centers, workshops, and dealerships.

The DIY segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing trend of vehicle owners performing minor repairs and replacements themselves, supported by online tutorials, instructional content, and availability of easy-to-install parts.

Wholesale and Distribution Automotive Market Regional Analysis

- North America dominated the wholesale and distribution automotive market with the largest revenue share of 25.3% in 2025, driven by a well-established automotive industry, strong aftermarket demand, and high adoption of digital distribution channels

- Businesses in the region highly value efficient supply chain management, reliable inventory availability, and fast delivery services offered by wholesalers and distributors, ensuring timely access to replacement parts and automotive components

- This widespread adoption is further supported by robust infrastructure, advanced logistics networks, and a strong focus on fleet management and service quality, establishing wholesale and distribution channels as a preferred solution for automotive parts in both commercial and retail segments

U.S. Wholesale and Distribution Automotive Market Insight

The U.S. wholesale and distribution automotive market captured the largest revenue share in 2025 within North America, fueled by increasing vehicle parc, rising demand for aftermarket parts, and the growing trend of online automotive sales. Businesses are prioritizing faster, reliable access to replacement components through integrated distribution networks. The expansion of e-commerce platforms, coupled with advanced inventory management systems and fleet servicing solutions, further propels the market. Moreover, partnerships between distributors, retailers, and manufacturers enhance availability and operational efficiency, significantly contributing to market growth.

Europe Wholesale and Distribution Automotive Market Insight

The Europe wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by regulatory requirements for quality and safety, increasing vehicle ownership, and demand for timely delivery of replacement parts. Urbanization, coupled with the growth of connected vehicle technologies, is fostering the adoption of advanced distribution solutions. European businesses are also investing in digital supply chain platforms to ensure seamless procurement and distribution across retail and commercial segments.

U.K. Wholesale and Distribution Automotive Market Insight

The U.K. wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for aftermarket parts, fleet management services, and e-commerce-based distribution. Concerns over vehicle downtime and the need for prompt maintenance are encouraging businesses and individual consumers to rely on professional distributors and wholesalers. The country’s well-developed logistics and retail infrastructure, alongside increasing online sales penetration, is expected to continue supporting market growth.

Germany Wholesale and Distribution Automotive Market Insight

The Germany wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s large automotive manufacturing base, high-quality standards, and advanced logistics networks. Businesses in Germany are increasingly adopting integrated inventory management, automated warehousing, and digital ordering solutions to enhance distribution efficiency. The emphasis on timely delivery, sustainability in logistics, and operational optimization supports market adoption across commercial and retail segments.

Asia-Pacific Wholesale and Distribution Automotive Market Insight

The Asia-Pacific wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, rising vehicle sales, and expansion of automotive aftermarket infrastructure in countries such as China, Japan, and India. Growing urbanization, increasing disposable incomes, and technological advancements in logistics and e-commerce platforms are driving the adoption of efficient distribution solutions. Furthermore, APAC’s emergence as a manufacturing hub for automotive components enhances affordability and accessibility of replacement parts across the region.

Japan Wholesale and Distribution Automotive Market Insight

The Japan wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s high vehicle ownership, demand for efficient fleet management, and adoption of digital supply chain solutions. Japanese businesses increasingly rely on distributors and wholesalers for timely access to replacement parts, ensuring minimal downtime and operational efficiency. Integration of automated inventory management, predictive ordering, and e-commerce channels is fueling growth, while aging population trends also boost demand for easy-to-access automotive services.

China Wholesale and Distribution Automotive Market Insight

The China wholesale and distribution automotive market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding automotive industry, rapidly growing vehicle parc, and rising demand for aftermarket services. China is one of the largest markets for replacement parts and automotive components, with wholesalers and distributors playing a critical role in ensuring availability across retail, commercial, and fleet segments. Government initiatives promoting digitalization, expansion of e-commerce channels, and local manufacturing capabilities are key factors propelling market growth.

Wholesale and Distribution Automotive Market Share

The Wholesale and Distribution Automotive industry is primarily led by well-established companies, including:

- 3M (U.S.)

- Continental AG (Germany)

- BorgWarner Inc. (U.S.)

- DENSO CORPORATION (Japan)

- Tenneco Inc. (U.S.)

- Marelli Holdings Co., Ltd. (Japan)

- Robert Bosch GmbH (Germany)

- The Goodyear Tire and Rubber Company (U.S.)

- ZF Friedrichshafen AG (Germany)

- Cooper Tire and Rubber Company (U.S.)

- LEMANS CORPORATION (U.S.)

- Motorsport Aftermarket Group (U.S.)

- Textron Inc. (U.S.)

- Western Power Sports, Inc. (U.S.)

- Polaris Inc. (U.S.)

- AISIN SEIKI Co., Ltd. (Japan)

- Deere and Company (U.S.)

- BRP (Canada)

Latest Developments in Global Wholesale and Distribution Automotive Market

- In July 2023, General Motors Co. completed the acquisition of Israel-based battery software startup ALGOLiON Ltd. This strategic move, managed by GM's Technologies Acceleration and Commercialization (TAC) team, aims to enhance GM's battery development capabilities through advanced software solutions. The acquisition strengthens GM’s position in electric vehicle technology and supports faster innovation in battery performance, efficiency, and energy management, positively impacting the EV market

- In June 2023, Continental AG introduced the UltraContact NXT, its most environmentally friendly tire to date. Made from up to 65% recycled, renewable, and mass balance certified materials, the tire delivers top-tier safety and performance while reducing environmental impact. This launch reinforces Continental’s sustainability strategy and caters to eco-conscious consumers, boosting its market competitiveness in green mobility solutions

- In May 2023, Stellantis NV partnered with Petromin in Saudi Arabia to launch the Eurorepar line of automotive parts and maintenance supplies. This collaboration enhances vehicle maintenance accessibility and supports road safety initiatives. By offering a reliable range of parts, Stellantis strengthens its aftermarket presence and expands market reach in the Middle East region

- In February 2023, Continental AG launched the CrossContact H/T summer tire, designed for versatility across paved and unpaved roads. Suitable for both conventional and electric vehicles, the tire combines rugged durability with comfort and safety, including an M+S rating for mild off-road use. The launch broadens Continental’s product portfolio and addresses consumer demand for multi-purpose, high-performance tires

- In March 2023, BorgWarner Inc. introduced bi-metallic brake discs that are lighter, quieter, and more fuel-efficient than traditional cast-iron discs. The two-part alloy design reduces weight by 15%, improving fuel economy and lowering emissions, while minimizing vibration and noise for a smoother ride. This innovation enhances vehicle performance and sustainability, strengthening BorgWarner’s competitive position in the brake component market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.