Global Vasoconstrictor Drugs Market

Market Size in USD Billion

USD

7.27 Billion

USD

11.07 Billion

2025

2033

USD

7.27 Billion

USD

11.07 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.27 Billion | |

| USD 11.07 Billion | |

| % | |

|

Vasoconstrictor Drugs Market Overview

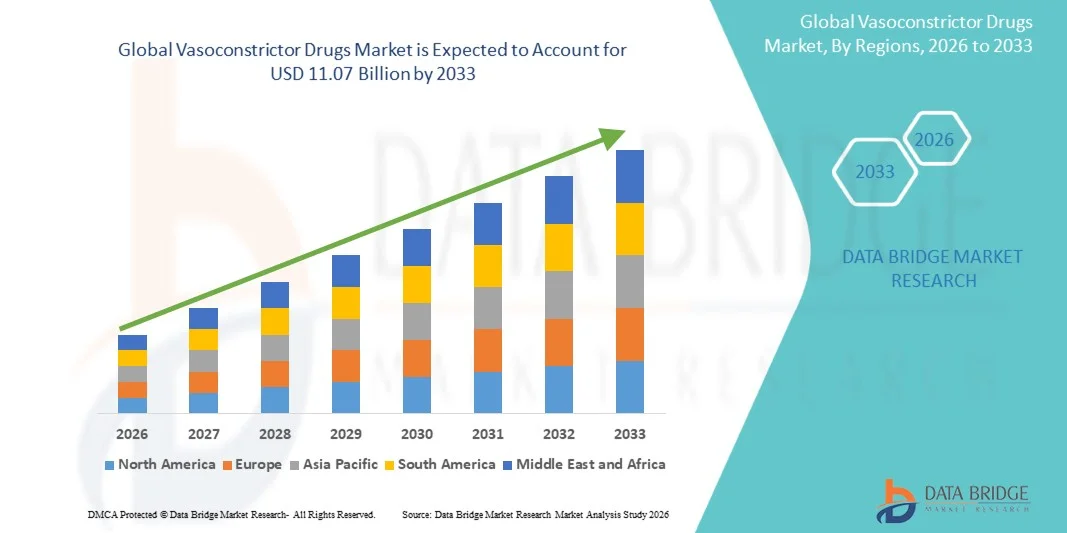

The Vasoconstrictor Drugs Market was valued at USD 7.27 billion in 2025 and is projected to reach USD 11.07 billion by 2033, growing at a CAGR of 5.40% from 2026 to 2033. The market is witnessing steady growth driven by the increasing prevalence of cardiovascular disorders, septic shock, and acute hypotension conditions that require rapid blood pressure stabilization and vascular tone regulation.

The rising burden of chronic diseases, expanding critical care admissions, and growing geriatric population are significantly boosting demand for vasoconstrictor therapies across hospital and emergency care settings. Additionally, advancements in drug formulations, improved intravenous delivery systems, and wider adoption of vasopressors in intensive care units are supporting market expansion. Increasing utilization of vasoconstrictor agents in anesthesia procedures, trauma care, and emergency medicine, along with strong clinical reliance on drugs such as norepinephrine, epinephrine, and vasopressin analogs, is further strengthening market growth

Key Market Trends & Insights

- North America dominated the Vasoconstrictor Drugs Market with the largest revenue share of 34.92% in 2025, supported by a high prevalence of cardiovascular diseases, advanced critical care infrastructure, and strong presence of major pharmaceutical manufacturers.

- The Alpha-Adrenoceptor Agonists segment led the market with a 64.28% share in 2025, driven by their strong clinical efficacy in rapidly increasing vascular tone and restoring blood pressure in acute hypotensive conditions such as septic shock and anesthesia-induced hypotension

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 6.1% from 2026 to 2033, fueled by rising healthcare expenditure, increasing ICU admissions, and expanding access to emergency and critical care medicines in countries such as India, China, and Southeast Asia.

- Vasopressin Analogs are the fastest-growing drug class type, projected to register a CAGR of 5.9%, reflecting the surge in their increasing use as adjunct therapy in refractory septic shock and vasodilatory condition

- The Injection segment dominated the dosage form category with a 88.73% revenue share in 2025, led by vasoconstrictor drugs are primarily administered in emergency and critical care settings where rapid onset of action is essential.

- Intravenous accounted for 92.15% of the market, preferred by vasoconstrictor drugs require immediate systemic action to stabilize blood pressure in life-threatening conditions

- The Tablets segment is the fastest-growing dosage form category, with a CAGR of 5.7%, driven by increasing use in less acute conditions, step-down therapy, and outpatient management of vascular tone-related disorders.

Market Size & Forecast

- Global Market Value (2025): USD 7.27 Billion

- Expected Market Value (2033): USD 11.07 Billion

- Forecast CAGR (2026–2033): 5.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Vasoconstrictor Drugs Market Segmentation

|

Attributes |

Vasoconstrictor Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Baxter (U.S.) · Fresenius Kabi AG (Germany) · Pfizer Inc. (U.S.) · Novartis AG (Switzerland) · Teva Pharmaceutical Industries Ltd. (Israel) · Hikma Pharmaceuticals PLC (U.K.) · B. Braun SE (Germany) · Amneal Pharmaceuticals LLC (U.S.) · Sandoz Group AG (Switzerland) · Dr. Reddy’s Laboratories Ltd. (India) · Sun Pharmaceutical Industries Ltd. (India) · Lupin Limited (India) · Aurobindo Pharma Limited (India) · Cipla Limited (India) · AbbVie Inc. (U.S.) · Merck & Co., Inc. (U.S.) · Sanofi (France) · Eli Lilly and Company (U.S.) · Viatris Inc. (U.S.) · ICU Medical, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of ICU infrastructure and critical care capacity · Growing clinical adoption of combination vasopressor therapy protocols · Increasing research into long-acting and receptor-selective vasoconstrictor agents |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Vasoconstrictor Drugs Market Trends

Trend: Expanding Use in Critical Care and Emergency Medicine

Vasoconstrictor drugs are becoming a core component of modern critical care protocols, particularly in the management of life-threatening conditions such as septic shock, acute hypotension, anaphylaxis, and perioperative cardiovascular instability. Their ability to rapidly restore vascular tone and maintain mean arterial pressure has made them essential in intensive care units and emergency departments. Hospitals are increasingly shifting toward standardized vasopressor protocols that prioritize early initiation and continuous titration to improve patient outcomes and reduce mortality rates. The growing availability of infusion-based delivery systems and better ICU monitoring technologies is further supporting their widespread adoption in high-acuity settings. For instance, adoption of norepinephrine-first shock resuscitation protocols in ICUs across multi-specialty hospitals has become increasingly common in both developed and emerging healthcare systems.

Vasoconstrictor Drugs Market Dynamics

Key Market Driver: Rising Burden of Cardiovascular and Shock Conditions

The global rise in cardiovascular disorders, sepsis cases, trauma incidents, and post-surgical complications is significantly increasing the demand for vasoconstrictor drugs across hospitals and emergency care units. Aging populations are particularly vulnerable to hemodynamic instability, driving higher ICU admissions and greater dependence on vasopressor therapies. Additionally, improvements in diagnostic capabilities and early recognition of shock conditions are leading to earlier intervention with vasoconstrictors, improving survival rates. The expansion of critical care infrastructure in developing regions is also widening patient access to these life-saving therapies. For instance, updated sepsis treatment guidelines in several countries now recommend early vasopressor initiation when fluid resuscitation alone fails to restore blood pressure stability.

Key Restraint/Challenge: Adverse Effects and Clinical Risk Concerns

Despite their clinical importance, vasoconstrictor drugs are associated with significant safety challenges, including peripheral ischemia, cardiac arrhythmias, excessive vasoconstriction, and potential reduction in organ perfusion if not carefully managed. These risks necessitate continuous hemodynamic monitoring, making their use largely restricted to ICU and highly controlled hospital environments. Variability in patient response and narrow therapeutic windows further complicate dosing strategies, especially in critically ill patients with multiple comorbidities. Limited availability of advanced monitoring systems in low-resource healthcare settings also restricts optimal use. For instance, high-dose vasopressor therapy in septic shock patients has been linked with increased risk of tissue hypoperfusion, requiring strict clinical supervision and dose adjustments.

Key Market Opportunity: Development of Targeted and Combination Vasopressor Therapies

The major opportunity in the vasoconstrictor drugs market lies in the development of more selective, receptor-targeted agents and optimized combination therapies that enhance hemodynamic stability while minimizing adverse effects. Pharmaceutical companies are increasingly focusing on precision medicine approaches that tailor vasopressor selection and dosing to individual patient profiles and shock subtypes. Combination regimens involving agents such as norepinephrine, vasopressin, and epinephrine are gaining clinical traction for their synergistic effects in refractory shock cases. Advances in drug delivery systems and formulation science are also enabling more stable and controllable intravenous infusions. For instance, clinical trials evaluating early combination vasopressor therapy in septic shock patients have shown improved blood pressure control and reduced overall vasopressor requirements in intensive care settings.

Vasoconstrictor Drugs Market Scope

The vasoconstrictor drugs market is segmented on the basis of drug class, dosage form, route of administration, end-users, and distribution channel.

- By Drug Class

On the basis of drug class, the Vasoconstrictor Drugs Market is segmented into alpha-adrenoceptor agonists and vasopressin analogs. The Alpha-Adrenoceptor Agonists segment dominated the market with a 64.28% share in 2025, owing to their strong clinical efficacy in rapidly increasing vascular tone and restoring blood pressure in acute hypotensive conditions such as septic shock and anesthesia-induced hypotension. Drugs in this class, including norepinephrine and epinephrine, are widely recommended as first-line vasopressors in intensive care protocols. Their rapid onset of action and predictable hemodynamic response make them essential in emergency medicine. Hospitals prefer these agents due to their broad availability and established treatment guidelines. Increasing ICU admissions and standardized shock management protocols further reinforce segment dominance. The segment also benefits from continuous clinical validation and strong physician familiarity across global healthcare systems.

The Vasopressin Analogs segment is expected to register the fastest growth at a CAGR of 5.9% from 2026 to 2033, driven by their increasing use as adjunct therapy in refractory septic shock and vasodilatory conditions. These drugs act through a different receptor pathway, making them valuable in combination vasopressor regimens when alpha-adrenergic agents alone are insufficient. Their ability to reduce catecholamine requirements and improve vascular responsiveness is increasing clinical interest. Expanding research into multi-mechanism shock management is further boosting adoption. Growing awareness of vasopressor-sparing strategies in critical care is supporting demand. For instance, vasopressin-based combination protocols are increasingly being integrated into advanced ICU treatment guidelines for severe septic shock cases.

- By Dosage Form

On the basis of dosage form, the market is segmented into tablets, injections, and others. The Injection segment dominated the market with an 88.73% share in 2025, as vasoconstrictor drugs are primarily administered in emergency and critical care settings where rapid onset of action is essential. Injectable formulations allow precise dose titration through intravenous infusion, making them ideal for ICU and surgical environments. The high bioavailability and immediate therapeutic effect of injections make them the standard route for managing acute hypotension. Hospitals rely heavily on injectable vasopressors due to strict clinical monitoring requirements. The segment also benefits from continuous infusion pump technologies that ensure controlled administration. Increasing hospital admissions for shock-related conditions further reinforces injectable dominance globally.

The Tablets segment is expected to register the fastest growth at a CAGR of 5.7% from 2026 to 2033, driven by increasing use in less acute conditions, step-down therapy, and outpatient management of vascular tone-related disorders. Oral formulations are gaining traction in controlled clinical settings where long-term or maintenance therapy is required after stabilization in hospitals. Growing preference for non-invasive administration routes in specific patient populations is also supporting adoption. Pharmaceutical companies are developing improved oral bioavailability formulations to enhance efficacy. Expanding access to healthcare in emerging markets is further accelerating demand for oral therapies. For instance, oral vasoconstrictor agents are increasingly being evaluated for post-acute care and specialized cardiovascular management in outpatient follow-up settings.

- By Route of Administration

On the basis of route of administration, the market is segmented into intravenous, oral, and others. The Intravenous segment dominated the market with a 92.15% share in 2025, as vasoconstrictor drugs require immediate systemic action to stabilize blood pressure in life-threatening conditions. IV administration enables precise titration and continuous monitoring, which is critical in ICU and emergency settings. Rapid onset of action makes it indispensable for septic shock, trauma, and anesthesia-related hypotension. Hospitals prefer IV delivery due to its reliability and controllability under critical conditions. The segment is strongly supported by advanced infusion pump technologies and ICU infrastructure expansion. Increasing global burden of acute cardiovascular emergencies continues to reinforce IV dominance.

The Others segment is expected to register the fastest growth at a CAGR of 5.2% from 2026 to 2033, driven by research into localized and alternative delivery approaches for specific clinical applications. Although still limited in clinical use, novel administration methods are being explored for perioperative and targeted vascular control. Pharmaceutical innovation is focusing on improving drug stability and reducing systemic side effects through controlled delivery mechanisms. Expanding clinical trials in specialized surgical procedures is supporting growth potential. Increasing demand for precision medicine approaches is also contributing to innovation in this segment. For instance, investigational localized vasoconstrictor delivery techniques are being evaluated in advanced surgical and interventional procedures to reduce systemic exposure.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, and others. The Hospital segment dominated the market with a 78.64% share in 2025, as vasoconstrictor drugs are primarily administered in intensive care units, emergency departments, and surgical theaters where continuous monitoring is required. Hospitals handle the majority of critical care admissions, including septic shock, trauma, and post-operative complications requiring vasopressor support. Availability of advanced monitoring systems and trained healthcare professionals further strengthens hospital dominance. Centralized procurement systems and formulary-based drug management also support high-volume usage. Expanding ICU capacity and emergency care infrastructure globally continues to reinforce this segment’s leadership.

The Clinics segment is expected to register the fastest growth at a CAGR of 5.1% from 2026 to 2033, driven by increasing availability of advanced outpatient procedures and urgent care services. Although limited compared to hospitals, clinics are gradually adopting emergency stabilization protocols for acute hypotensive events. Growing investment in ambulatory care infrastructure is supporting broader use of injectable emergency drugs. Expansion of specialty clinics and day-care surgical centers is also contributing to demand. Increasing focus on decentralized healthcare delivery is further accelerating adoption. For instance, advanced cardiac and anesthesia clinics are increasingly maintaining vasopressor emergency kits for immediate stabilization during procedural complications.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market with a 71.46% share in 2025, as vasoconstrictor drugs are primarily used in controlled hospital environments where immediate access and proper storage are critical. Hospital pharmacies ensure rapid availability of life-saving vasopressors in ICUs and emergency departments. Strict regulatory compliance and cold-chain storage requirements further strengthen centralized hospital procurement. Integration with hospital electronic medical systems improves drug tracking and administration efficiency. High inpatient volumes in critical care units continue to drive bulk purchasing through hospital pharmacies. The segment benefits from established formulary management systems across healthcare institutions.

The Online Pharmacy segment is expected to register the fastest growth at a CAGR of 5.6% from 2026 to 2033, driven by the increasing digitization of healthcare procurement systems and rising demand for efficient supply chain solutions. While direct patient access remains limited for critical drugs, online platforms are increasingly used for institutional procurement and emergency stock replenishment. Growth in telemedicine and digital healthcare ecosystems is also supporting indirect adoption. Improved logistics and cold-chain delivery systems are enhancing reliability. Increasing healthcare digitization in emerging markets is further accelerating expansion. For instance, hospital procurement systems are increasingly integrating with digital pharmacy platforms to streamline ordering and inventory management of critical care medications.

Vasoconstrictor Drugs Market Regional Analysis

North America dominated the Vasoconstrictor Drugs Market with the largest revenue share of 34.92% in 2025, supported by a high prevalence of cardiovascular diseases, advanced critical care infrastructure, and strong presence of major pharmaceutical manufacturers. The region benefits from strong adoption of guideline-based vasopressor therapies, widespread availability of ICU facilities, and high healthcare spending. Presence of major pharmaceutical companies and rapid uptake of advanced treatment protocols further strengthen market leadership. Increasing geriatric population and rising ICU admissions continue to drive consistent demand for vasoconstrictor therapies. Strong regulatory frameworks and early adoption of innovative critical care drugs also contribute to regional dominance. Continuous advancements in emergency medicine and hospital care systems further reinforce North America’s leading position in the global market.

U.S. Vasoconstrictor Drugs Market Insight

The U.S. vasoconstrictor drugs market is witnessing strong growth due to the high prevalence of cardiovascular diseases, septic shock cases, and advanced critical care infrastructure across hospitals and emergency departments. The country’s well-established healthcare system, along with widespread adoption of evidence-based vasopressor protocols, is driving demand across ICU and surgical care settings. Increasing geriatric population and high ICU admission rates are further supporting consistent utilization of vasoconstrictor therapies. In addition, strong presence of major pharmaceutical manufacturers and rapid uptake of advanced injectable formulations are strengthening market expansion. Continuous improvements in emergency medicine practices and critical care monitoring systems are further accelerating adoption across healthcare facilities.

Europe Vasoconstrictor Drugs Market Insight

The Europe vasoconstrictor drugs market remains a major contributor to global revenue, driven by strong healthcare infrastructure, high awareness of sepsis management protocols, and well-established intensive care systems. The widespread use of guideline-based vasopressor therapy across hospitals is supporting consistent demand in emergency and perioperative care. Increasing focus on improving critical care outcomes and reducing mortality from septic shock is further boosting adoption. The region also benefits from strong regulatory frameworks and high standards of clinical practice across healthcare systems. Growing investments in hospital modernization and ICU expansion continue to enhance treatment accessibility. Additionally, rising elderly population and chronic disease burden are reinforcing steady market growth across Europe.

U.K. Vasoconstrictor Drugs Market Insight

The U.K. vasoconstrictor drugs market is experiencing steady growth, supported by increasing ICU admissions, rising prevalence of cardiovascular emergencies, and strong NHS-driven critical care protocols. Growing adoption of standardized sepsis treatment pathways and early vasopressor initiation guidelines is contributing to consistent drug utilization. Hospitals are increasingly relying on injectable vasoconstrictors for rapid stabilization in emergency and perioperative settings. Integration of advanced monitoring systems and improved critical care infrastructure is further enhancing treatment efficiency. Additionally, ongoing investments in hospital emergency services and critical care capacity are supporting market expansion. Continuous focus on patient safety and evidence-based medicine is also strengthening adoption across healthcare institutions.

Germany Vasoconstrictor Drugs Market Insight

The Germany vasoconstrictor drugs market is expanding steadily due to the country’s strong healthcare infrastructure, high ICU capacity, and advanced clinical research capabilities. Hospitals and emergency care centers are increasingly adopting vasopressor therapies for managing septic shock, trauma-related hypotension, and surgical complications. Strong emphasis on clinical guidelines and precision medicine is supporting rational and effective drug use. The presence of well-developed pharmaceutical manufacturing and research ecosystem further strengthens market availability. Increasing elderly population and rising burden of chronic diseases are contributing to higher ICU admissions. Additionally, continuous advancements in critical care protocols and hospital modernization are driving sustained market growth in Germany.

Asia-Pacific Vasoconstrictor Drugs Market Insight

The Asia-Pacific vasoconstrictor drugs market is expected to witness rapid growth, driven by increasing burden of cardiovascular diseases, rising sepsis incidence, and expanding critical care infrastructure across emerging economies. Growing healthcare investments and improving access to emergency medical services are supporting wider adoption of vasopressor therapies. Increasing ICU capacity in countries such as India, China, and Japan is further accelerating demand. Rising awareness among clinicians regarding early shock management and guideline-based therapy is also contributing to market expansion. Additionally, rapid urbanization and healthcare modernization initiatives are strengthening hospital capabilities. Expanding pharmaceutical manufacturing and improving drug availability are positioning Asia-Pacific as a high-growth region globally.

Japan Vasoconstrictor Drugs Market Insight

The Japan vasoconstrictor drugs market is witnessing consistent growth due to rising investments in advanced healthcare technologies, strong emergency care systems, and an aging population with high cardiovascular risk. Hospitals and critical care units are increasingly adopting vasopressor therapies for managing acute hypotension and septic shock cases. The country’s focus on high-quality, technology-driven healthcare delivery is supporting efficient drug utilization. Strong regulatory standards and clinical precision in treatment protocols further enhance adoption. Increasing integration of advanced monitoring systems in ICUs is improving patient outcomes. Additionally, Japan’s growing emphasis on geriatric care and perioperative management is contributing to sustained demand for vasoconstrictor drugs.

China Vasoconstrictor Drugs Market Insight

The China vasoconstrictor drugs market is growing rapidly, driven by rising cardiovascular disease burden, increasing sepsis cases, and expanding critical care infrastructure across hospitals. Government initiatives to strengthen healthcare access and improve emergency medical services are significantly boosting market demand. Growing ICU capacity and rapid hospital modernization are further supporting increased adoption of vasopressor therapies. Increasing awareness among healthcare professionals regarding early shock intervention is also driving utilization. Strong expansion of domestic pharmaceutical manufacturing is improving drug availability and affordability. Additionally, continuous healthcare reforms and investment in tertiary care hospitals are positioning China as one of the fastest-growing markets globally for vasoconstrictor drugs.

Vasoconstrictor Drugs Market Share

The vasoconstrictor drugs industry is primarily led by well-established companies, including:

- Baxter (U.S.)

- Fresenius Kabi AG (Germany)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Hikma Pharmaceuticals PLC (U.K.)

- Braun SE (Germany)

- Amneal Pharmaceuticals LLC (U.S.)

- Sandoz Group AG (Switzerland)

- Reddy’s Laboratories Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Aurobindo Pharma Limited (India)

- Cipla Limited (India)

- AbbVie Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Sanofi (France)

- Eli Lilly and Company (U.S.)

- Viatris Inc. (U.S.)

- ICU Medical, Inc. (U.S.)

Latest Developments in Vasoconstrictor Drugs Market

- In August 2025, the U.S. FDA approved generic Norepinephrine Bitartrate injection developed by Gland Pharma, a key vasoconstrictor widely used as a first-line therapy for septic shock and acute hypotension in ICU settings, significantly strengthening the availability of injectable vasopressors in critical care medicine. This approval supports broader access to affordable life-saving adrenergic agents used for rapid blood pressure stabilization in emergency hospitals

- In August 2025, the FDA also approved Norepinephrine Bitartrate in 5% dextrose injection bags, enabling ready-to-use vasoconstrictor infusions for critically ill patients suffering from severe hypotension. This development improves hospital workflow efficiency by reducing preparation time for pressor administration in emergency and intensive care units, where rapid hemodynamic stabilization is essential for survival

- In November 2024, the U.S. FDA proposed removing oral phenylephrine from over-the-counter nasal decongestant products after determining it is not effective for relieving nasal congestion. This regulatory action significantly impacted the vasoconstrictor market by shifting consumer and clinical attention away from oral decongestants toward more effective adrenergic agents, including injectable and prescription alternatives used in clinical practice

- In September 2023, an FDA advisory committee unanimously concluded that oral phenylephrine is ineffective as a nasal decongestant, triggering a broader regulatory review that influenced later policy actions in 2024. While phenylephrine remains effective in injectable form for hypotension management in anesthesia and septic shock, its oral formulations came under scrutiny, reshaping discussions around efficacy standards for vasoconstrictor-containing OTC medications

- In March 2023, Nexus Pharmaceuticals received FDA approval for EMERPHED (ephedrine sulfate injection) prefilled syringe, a sympathomimetic vasoconstrictor used to manage intraoperative hypotension during anesthesia. The ready-to-use formulation improved safety and efficiency in operating rooms by minimizing preparation errors and enabling faster administration in surgical emergency situations, reinforcing the shift toward prefilled injectable vasopressor systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.