Global Value Based Healthcare Market

Market Size in USD Billion

CAGR :

%

USD

12.17 Billion

USD

51.30 Billion

2024

2032

USD

12.17 Billion

USD

51.30 Billion

2024

2032

| 2025 –2032 | |

| USD 12.17 Billion | |

| USD 51.30 Billion | |

| % | |

|

Value-Based Healthcare Market Size

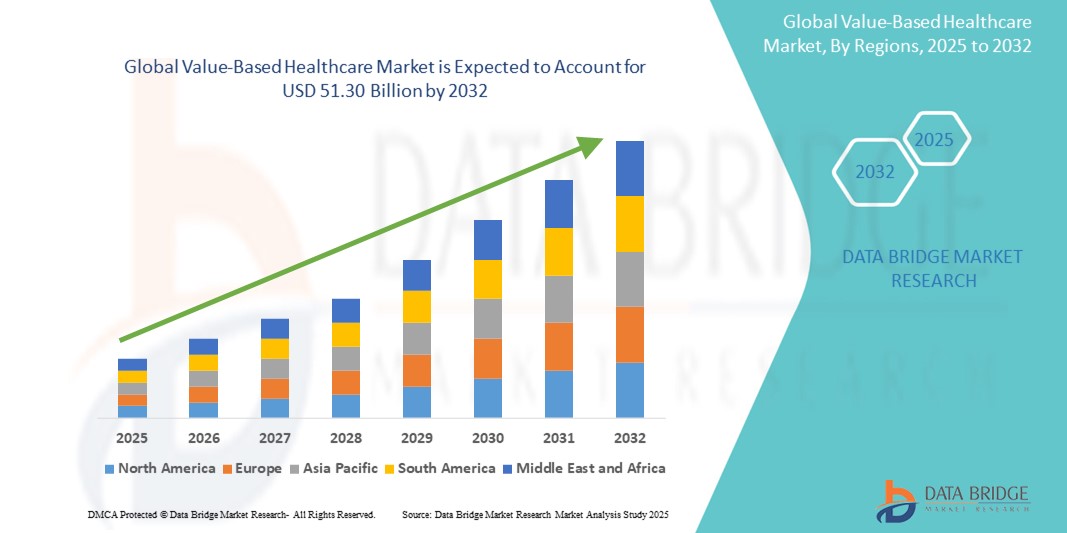

- The global value-based healthcare market size was valued at USD 12.17 billion in 2024 and is expected to reach USD 51.30 billion by 2032, at a CAGR of 19.70% during the forecast period

- The market growth is largely driven by the increasing shift from volume-based to value-based care models, which emphasize improved patient outcomes, cost-efficiency, and accountability across healthcare systems

- Furthermore, growing healthcare expenditures, rising chronic disease prevalence, and supportive government initiatives are encouraging healthcare providers to adopt data-driven, patient-centric care models. These driving forces are fueling widespread adoption of value-based healthcare strategies, thereby accelerating market expansion across regions

Value-Based Healthcare Market Analysis

- Value-based healthcare, focusing on improving patient outcomes relative to cost, is emerging as a central pillar in healthcare reform worldwide, driven by its ability to enhance care quality while optimizing financial efficiency across both public and private healthcare sectors

- The increasing adoption of value-based models is largely fueled by rising global healthcare expenditures, growing prevalence of chronic diseases, and regulatory support promoting outcome-based reimbursement over volume-driven care

- North America dominated the value-based healthcare market with the largest revenue share of 41.8% in 2024, owing to strong policy support, advanced healthcare IT infrastructure, and widespread implementation of value-based programs such as ACOs and bundled payments, particularly in the U.S.

- Asia-Pacific is expected to be the fastest-growing region in the value-based healthcare market during the forecast period, driven by expanding healthcare access, government investments in healthcare digitization, and increasing focus on cost-effective chronic disease management

- Accountable Care Organization (ACO) segment dominated the value-based healthcare market with a market share of 37% in 2024, driven by its ability to enhance care coordination, reduce unnecessary spending, and improve patient outcomes through shared accountability models

Report Scope and Value-Based Healthcare Market Segmentation

|

Attributes |

Value-Based Healthcare Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Value-Based Healthcare Market Trends

“Technology-Driven Care Coordination and Outcome Optimization”

- A significant and accelerating trend in the global value-based healthcare market is the growing integration of advanced analytics, artificial intelligence (AI), and digital health platforms to enhance care coordination, improve patient outcomes, and reduce overall healthcare costs

- For instance, Epic and Cerner now offer AI-enabled modules that support predictive risk stratification and real-time care planning, while Philips' connected care platforms enable remote monitoring and early intervention for chronic conditions

- AI-powered solutions are increasingly being used to identify care gaps, personalize treatment plans, and optimize clinical workflows by analyzing vast datasets across populations. For instance, IBM Watson Health applies machine learning to help clinicians tailor treatment based on individual patient profiles

- The widespread use of telehealth, wearable devices, and patient engagement portals allows for real-time health tracking, continuous communication, and proactive intervention, particularly in chronic care management

- The integration of these tools with EHR systems and payer-provider platforms ensures centralized, data-driven decision-making across healthcare settings, improving accountability and transparency in care delivery

- This trend toward intelligent, interoperable, and outcome-focused healthcare infrastructure is transforming patient expectations and provider operations globally, fostering a more personalized and sustainable care environment

- Consequently, major players such as Allscripts and Oracle Health are expanding their value-based care portfolios by integrating analytics, automation, and remote patient management solutions tailored to evolving care models

Value-Based Healthcare Market Dynamics

Driver

“Rising Healthcare Costs and Shift to Outcome-Based Reimbursement”

- The increasing burden of healthcare expenditures worldwide, coupled with the demand for better clinical outcomes and efficient care delivery, is a major driver for the adoption of value-based healthcare models

- For instance, the U.S. Centers for Medicare & Medicaid Services (CMS) continues to push programs such as the Medicare Shared Savings Program (MSSP) and Bundled Payments for Care Improvement (BPCI), which incentivize providers to improve care quality while lowering costs

- Value-based care models reward providers for delivering effective care by linking reimbursements to quality metrics and patient outcomes, reducing unnecessary procedures and avoidable hospital readmissions

- As chronic diseases continue to dominate global healthcare costs, the emphasis on preventive, coordinated, and long-term care under value-based frameworks is proving crucial for sustainability

- Private payers, governments, and employers are increasingly aligned with this shift, encouraging provider participation and driving systemic transformation toward quality- and value-centric care delivery

Restraint/Challenge

“Data Silos, Interoperability Gaps, and Implementation Costs”

- Despite growing momentum, the fragmented nature of health IT systems and the lack of interoperability standards remain significant barriers to the effective implementation of value-based healthcare models

- Many providers struggle with disconnected EHRs, analytics platforms, and billing systems, making it difficult to measure outcomes, share data, and manage patients holistically across the care continuum

- For instance, small and mid-sized clinics often face high upfront costs for adopting integrated platforms and training staff, delaying their transition to value-based frameworks

- Concerns over data privacy, inconsistent regulatory requirements across regions, and complex outcome tracking further hinder widespread adoption, particularly in low- and middle-income countries

- Overcoming these challenges will require coordinated efforts across public and private sectors, with emphasis on building secure, interoperable systems, offering financial incentives, and supporting healthcare providers with technical guidance and scalable solutions

Value-Based Healthcare Market Scope

The market is segmented on the basis of model, deployment, platform, and application.

- By Model

On the basis of model, the value-based healthcare market is segmented into accountable care organization (ACO), patient-centered medical home (PCMH), pay for performance (P4P), and bundled payments. The accountable care organization (ACO) segment dominated the market with the largest revenue share of 37.0% in 2024, driven by its effectiveness in fostering coordinated care, improving patient outcomes, and reducing unnecessary medical expenditures through shared accountability. ACOs are particularly prevalent in the U.S. healthcare system, where CMS and private payers incentivize providers to meet quality benchmarks while controlling costs.

The bundled payments segment is anticipated to witness the fastest growth rate of 20.5% from 2025 to 2032, as it aligns financial incentives with outcomes by offering fixed reimbursement for specific treatments or care episodes. This model is gaining traction globally due to its potential to reduce costs and improve transparency, particularly in surgical and chronic care procedures.

- By Deployment

On the basis of deployment, the value-based healthcare market is segmented into cloud-based and on-premise solutions. The cloud-based segment held the largest market share of 58.2% in 2024, supported by its scalability, cost efficiency, and ease of integration with modern health IT systems. Cloud platforms offer real-time analytics, remote access, and improved interoperability, making them well-suited to meet the data needs of value-based care frameworks.

The on-premise segment, is expected to witness fastest growth during forecast period, in healthcare settings requiring strict data control and regulatory compliance. It is especially used in legacy institutions with in-house IT infrastructure, though its market share is expected to gradually decline due to the operational flexibility of cloud solutions.

- By Platform

On the basis of platform, the value-based healthcare market is segmented into standalone and integrated solutions. The integrated platform segment led the market with a 62.7% share in 2024, driven by the increasing demand for comprehensive systems that consolidate EHRs, analytics tools, claims management, and patient engagement features. Integrated platforms support seamless data flow across care settings, improving outcome tracking and enhancing provider collaboration under value-based models.

The standalone segment, is expected to witness fastest growth during forecast period, where specific functionalities such as outcome analytics or billing solutions are needed without full-system integration. However, its growth is expected to be moderate due to the rising preference for fully integrated ecosystems.

- By Application

On the basis of application, the value-based healthcare market is segmented into hospitals, clinics, insurance companies, and government entities. The Hospitals segment dominated the market with the largest revenue share of 49.8% in 2024, due to their central role in delivering coordinated care across specialties, managing chronic conditions, and integrating population health strategies. Hospitals are often the first adopters of advanced value-based care platforms, supported by dedicated IT teams and funding mechanisms.

The insurance companies segment is expected to experience the fastest CAGR of 18.9% from 2025 to 2032, as payers increasingly adopt value-based reimbursement models and analytics platforms to evaluate provider performance and incentivize outcome-based care. This shift is accelerating investment in data-driven technologies and strategic partnerships with providers to align financial and clinical goals.

Value-Based Healthcare Market Regional Analysis

- North America dominated the value-based healthcare market with the largest revenue share of 41.8% in 2024, owing to strong policy support, advanced healthcare IT infrastructure, and widespread implementation of value-based programs such as ACOs and bundled payments, particularly in the U.S.

- Healthcare providers and payers in the region increasingly prioritize outcome-driven care models, supported by widespread adoption of electronic health records, advanced analytics platforms, and population health management tools

- The region’s high healthcare expenditure, robust regulatory frameworks, and the strategic alignment of private and public sectors around patient-centric care have made North America a global leader in value-based healthcare adoption, particularly in the U.S. where integrated delivery networks (IDNs) and accountable care organizations (ACOs) are rapidly expanding

U.S. Value-Based Healthcare Market Insight

The U.S. value-based healthcare market captured the largest revenue share of 82.5% in 2024 within North America, fueled by strong federal initiatives such as the Medicare Shared Savings Program (MSSP), Accountable Care Organizations (ACOs), and Bundled Payments for Care Improvement (BPCI). The nation's advanced health IT infrastructure, widespread use of electronic health records (EHRs), and emphasis on performance-based reimbursement have made it a global leader in value-based care. Growing focus on population health management, chronic disease control, and digital innovation further strengthens the U.S. market's position.

Europe Value-Based Healthcare Market Insight

The Europe value-based healthcare market is projected to expand at a substantial CAGR throughout the forecast period, driven by escalating pressure on healthcare systems to improve quality while containing costs. EU nations are actively piloting outcome-based reimbursement models and leveraging digital health tools to improve care efficiency. National policies in countries such as Germany, the U.K., and the Netherlands are increasingly aligning with value-based principles. This regional growth is further supported by cross-border health data collaboration and strong regulatory frameworks promoting interoperability and patient-centered care.

U.K. Value-Based Healthcare Market Insight

The U.K. value-based healthcare market is anticipated to grow at a noteworthy CAGR during the forecast period, bolstered by NHS initiatives focused on integrated care systems (ICS), outcome-based payments, and long-term disease management. The country's push towards digitizing healthcare services, alongside public-private partnerships, is accelerating the shift toward value-oriented care delivery. With increasing demand for transparency, cost control, and improved patient satisfaction, the U.K. healthcare system is steadily embedding value-based approaches at both regional and national levels.

Germany Value-Based Healthcare Market Insight

The Germany value-based healthcare market is expected to expand at a considerable CAGR during the forecast period, driven by healthcare reforms promoting quality-based reimbursement and strong digital transformation efforts. The country’s universal healthcare system is adopting value-based pilot projects focused on chronic illness management, care coordination, and data analytics integration. Germany’s emphasis on sustainability, outcome transparency, and evidence-based practices supports the adoption of models that reward providers based on patient results rather than service volume.

Asia-Pacific Value-Based Healthcare Market Insight

The Asia-Pacific value-based healthcare market is poised to grow at the fastest CAGR of 24.7% during the forecast period of 2025 to 2032, fueled by rising healthcare expenditures, growing prevalence of chronic diseases, and digital health adoption across countries such as China, Japan, and India. Government-led initiatives to improve access, reduce care fragmentation, and modernize reimbursement systems are accelerating regional interest in value-based care. Increasing penetration of cloud-based platforms and mobile health solutions is enabling scalable implementation across urban and rural health settings.

Japan Value-Based Healthcare Market Insight

The Japan value-based healthcare market is gaining momentum due to its aging population, high healthcare costs, and a growing focus on coordinated care delivery. The government is promoting digital health transformation through initiatives such as data sharing frameworks and remote care programs. Value-based models are increasingly adopted to manage chronic illnesses and reduce hospital readmissions. Japan's tech-driven healthcare culture, alongside integration of AI and IoT into patient monitoring, is shaping a data-informed ecosystem ideal for outcome-based care.

India Value-Based Healthcare Market Insight

The India value-based healthcare market accounted for the largest revenue share in Asia-Pacific in 2024, driven by the country’s rapid urbanization, expanding middle class, and government-backed health schemes such as Ayushman Bharat. As healthcare providers shift focus from volume to value, investment in telehealth, health analytics, and digital health records is enabling the rollout of value-based care models. India's strong domestic tech sector and growing demand for quality, affordable healthcare across private and public sectors are positioning it as a major growth hub for value-based care in the region.

Value-Based Healthcare Market Share

The value-based healthcare industry is primarily led by well-established companies, including:

- Optum, Inc. (U.S.)

- Oracle Health (U.S.)

- Epic Systems Corporation (U.S.)

- McKesson Corporation (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- IBM Watson Health (U.S.)

- Humana Inc. (U.S.)

- Cigna Corporation (U.S.)

- Elevance Health (U.S.)

- Health Catalyst Inc. (U.S.)

- Medecision, Inc. (U.S.)

- eClinicalWorks, LLC (U.S.)

- NextGen Healthcare, Inc. (U.S.)

- athenahealth, Inc. (U.S.)

- Inovalon Holdings, Inc. (U.S.)

- NantHealth, Inc. (U.S.)

What are the Recent Developments in Global Value-Based Healthcare Market?

- In April 2023, Philips announced the expansion of its Enterprise Performance Analytics platform, integrating AI-driven tools to support value-based healthcare delivery. The platform helps healthcare providers measure outcomes, identify care gaps, and optimize resource allocation, aligning with global shifts toward patient-centered care. This move reinforces Philips’ strategic focus on enabling data-informed decision-making and improving value across the care continuum

- In March 2023, UnitedHealth Group, through its Optum division, launched a new initiative aimed at accelerating value-based care adoption across independent physician practices in the U.S. The program includes shared savings models, digital tools, and care coordination resources, enabling providers to transition from fee-for-service to outcome-based reimbursement. This effort reflects the company’s continued leadership in advancing integrated, cost-effective care solutions

- In March 2023, Cerner Corporation (now a part of Oracle Health) unveiled enhancements to its population health management solutions, focusing on value-based care contracts. The upgraded platform features predictive analytics, social determinants of health integration, and care planning modules, aimed at supporting providers and payers in achieving measurable health outcomes. This development underscores the role of interoperable, data-driven platforms in scaling value-based care

- In February 2023, Humana Inc. partnered with ChenMed to expand value-based primary care services for Medicare Advantage members across several U.S. states. This partnership aims to improve health outcomes through personalized, team-based care models, especially for underserved populations. The collaboration demonstrates the growing trend of payer-provider partnerships driving innovation in value-based care delivery

- In January 2023, Allscripts Healthcare Solutions announced new features for its Veradigm platform, designed to streamline performance tracking under value-based care agreements. The enhancements include real-time quality reporting, risk adjustment tools, and payer collaboration features. Allscripts' continued investment in analytics and digital infrastructure reflects its commitment to helping providers succeed in performance-based reimbursement environments

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.