Global Urinary Catheters Market

Market Size in USD Billion

USD

7.40 Billion

USD

12.24 Billion

2025

2033

USD

7.40 Billion

USD

12.24 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.40 Billion | |

| USD 12.24 Billion | |

| % | |

|

Urinary Catheters Market Size

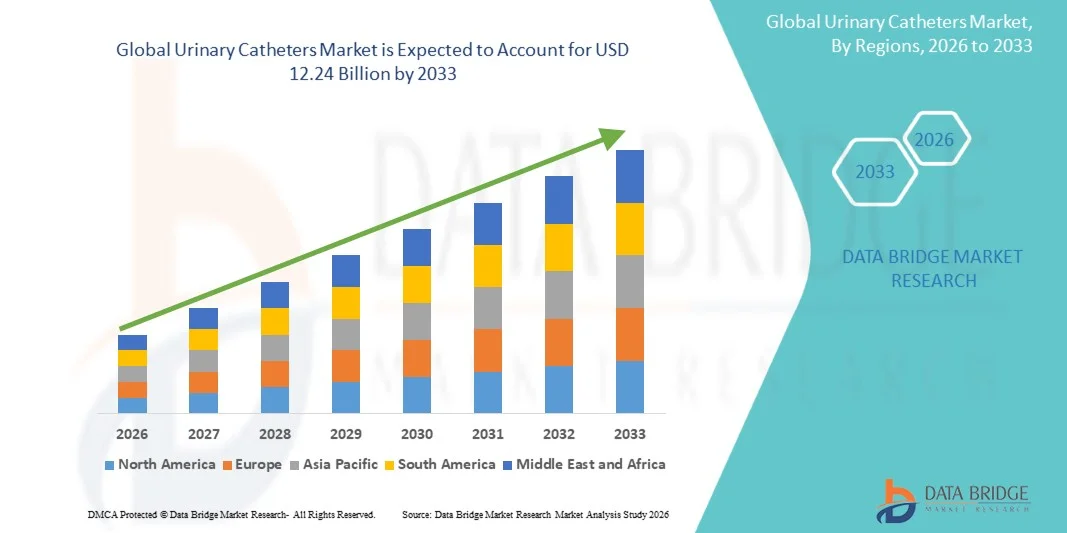

- The global Urinary Catheters market size was valued at USD 7.40 billion in 2025 and is expected to reach USD 12.24 billion by 2033, at a CAGR of 6.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of urinary disorders such as urinary retention, benign prostatic hyperplasia (BPH), spinal cord injuries, and incontinence, which has created a sustained demand for urinary catheters across hospitals, clinics, and home-care settings. Technological advancements such as antimicrobial coatings, hydrophilic catheters, and improved biocompatible materials are enhancing patient comfort and reducing infection risks, thereby supporting wider adoption. In addition, the growing elderly population worldwide, coupled with rising awareness of minimally invasive treatments, is further driving market expansion

- Furthermore, rising consumer and institutional demand for safe, hygienic, and easy-to-use catheter solutions is establishing urinary catheters as a critical component of modern urological care. Increasing investments in product innovation, availability across multiple distribution channels, and the adoption of disposable and single-use catheters to reduce hospital-acquired infections are boosting market penetration. These converging factors are accelerating the uptake of urinary catheter solutions, thereby significantly boosting the industry's growth

Urinary Catheters Market Analysis

- Urinary catheters, designed to help drain urine from the bladder in patients with urinary retention, incontinence, or those undergoing surgery, are an essential component of urological care in both hospital and homecare settings, owing to their critical role in patient management and treatment outcomes

- The escalating demand for urinary catheters is primarily driven by the rising prevalence of urological disorders, growing aging population, increasing surgical procedures, and heightened awareness regarding advanced catheterization solutions for improved patient comfort and infection prevention

- North America dominated the urinary catheters market with the largest revenue share of 39.68% in 2025, supported by well-established healthcare infrastructure, high healthcare expenditure, and widespread adoption of advanced catheter products, with the U.S. leading due to a growing geriatric population and continued innovations in catheter materials and antimicrobial coatings aimed at reducing catheter-associated urinary tract infections (CAUTIs)

- Asia-Pacific is expected to be the fastest growing region in the urinary catheters market during the forecast period, fueled by increasing awareness of urological health, rising incidences of urinary incontinence and prostate-related conditions, improving healthcare infrastructure, expanding access to healthcare services, and rising disposable incomes across countries such as China and India

- The drug dispensing and packaging segment held the largest market revenue share of 57.8% in 2025, driven by increasing prescription volumes and rising need to minimize medication errors

Report Scope and Urinary Catheters Market Segmentation

|

Attributes |

Urinary Catheters Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Urinary Catheters Market Trends

“Enhanced Convenience and Patient-Friendly Features”

- A notable and accelerating trend in the global urinary catheters market is the development of patient-centric designs and enhanced usability features, improving comfort and adherence in both hospital and homecare settings

- For instance, companies such as Hollister Incorporated and Coloplast have launched new catheter variants with softer materials, ergonomic designs, and features that reduce infection risks, making them more suitable for long-term use

- Recent innovations include hydrophilic-coated catheters and pre-lubricated options, which simplify catheterization, reduce friction, and minimize the risk of urethral injury, especially for elderly or mobility-impaired patients

- Manufacturers are also focusing on single-use and compact portable designs to enhance convenience for patients performing self-catheterization at home or during travel. These developments facilitate greater independence and improve quality of life for users managing chronic urinary condition

- The trend toward easier-to-use, hygienic, and safer catheter products is reshaping patient expectations and driving adoption across both hospital and homecare environments. Companies such as Teleflex Medical and Becton Dickinson are actively expanding their product portfolios to include these innovative catheters, emphasizing patient comfort, infection control, and usability

- The demand for such user-friendly and clinically advanced urinary catheters continues to grow across all regions, driven by aging populations, rising prevalence of urinary disorders, and increasing homecare adoption

Urinary Catheters Market Dynamics

Driver

“Growing Need Due to Rising Prevalence of Urinary Disorders and Homecare Adoption”

- The increasing prevalence of urinary incontinence, chronic urinary conditions, and an aging population, combined with the expanding adoption of homecare solutions, is driving significant growth in the global urinary catheters market. Patients and caregivers are seeking safer, more hygienic, and easier-to-use catheter options to manage urinary health effectively

- For instance, in April 2024, Teleflex Medical announced the launch of an advanced catheter management program aimed at improving patient comfort, reducing complications, and enhancing overall compliance. Such initiatives by leading companies are expected to fuel growth in the urinary catheters industry during the forecast period

- As awareness of potential health risks such as urinary tract infections increases, there is a growing preference for catheters designed with advanced features like hydrophilic coatings, pre-lubrication, ergonomic design, and user-friendly insertion techniques. These innovations provide patients with safer and more convenient alternatives to traditional catheter products

- Furthermore, the rising trend of homecare and self-catheterization is expanding the market, as patients and caregivers prioritize products that allow for independent and discreet management of urinary conditions. Portable, single-use, and ready-to-use catheter kits are particularly appealing in residential and outpatient settings, improving patient quality of life

- The ease of use, sterility, portability, and convenience of modern urinary catheters, along with increasing healthcare provider recommendations, are key factors driving adoption across hospitals, clinics, and homecare environments

Restraint/Challenge

“Concerns Regarding High Costs and Patient Compliance”

- The relatively high cost of advanced urinary catheters compared to standard alternatives continues to pose a challenge, particularly in developing regions or among cost-conscious patients and healthcare providers

- Ensuring patient compliance and correct usage is critical, as improper catheterization can lead to infections, urethral trauma, or other complications, emphasizing the need for training and educational support

- Storage and disposal of disposable catheter products can be inconvenient, especially in homecare settings where proper disposal infrastructure may be limited, potentially restricting adoption

- Although prices for advanced catheter systems are gradually decreasing, the perceived premium of such products may still hinder widespread uptake among certain patient segments

- Availability of specialized catheter products may be limited in rural or underdeveloped areas, leading to inconsistent access and reduced adoption in certain regions

- Potential side effects, such as irritation, infection risk, or allergic reactions to catheter materials, may discourage patients from regular use, affecting market growth

- Regulatory hurdles and lengthy approval processes for new catheter technologies in certain countries can delay product launches and restrict market expansion

- Addressing these challenges through the development of cost-effective solutions, enhanced usability, patient education, and training programs will be vital for sustained growth in the urinary catheters market

Urinary Catheters Market Scope

The market is segmented on the basis of product, pharmacy type, pharmacy size, application, and end user.

• By Product

On the basis of product, the Pharmacy Automation market is segmented into systems, software, and services. The systems segment dominated the largest market revenue share of 48.7% in 2025, driven by growing deployment of robotic dispensing units, automated medication packaging machines, smart storage cabinets, and integrated workflow systems across hospitals and retail pharmacies. Healthcare providers are increasingly investing in automation hardware to reduce medication errors, improve turnaround time, and enhance prescription accuracy. Systems help optimize labor utilization and support 24/7 pharmacy operations with minimal human intervention. Rising prescription volumes and shortage of trained pharmacy staff are further encouraging adoption. Advanced barcode scanning, unit-dose dispensing, and real-time monitoring capabilities are strengthening segment demand. Large pharmacy chains continue to modernize legacy infrastructure with next-generation systems. Strong capital expenditure by hospitals and centralized pharmacies also supports growth. Demand for scalable, high-throughput automation equipment remains robust globally. The segment continues to benefit from increasing focus on patient safety and operational efficiency.

The software segment is expected to witness the fastest CAGR of 11.9% from 2026 to 2033, driven by rising digital transformation across pharmacy operations worldwide. Software platforms help manage prescriptions, workflow scheduling, billing, refill reminders, analytics, and compliance reporting through a unified interface. Growing demand for cloud-based pharmacy management solutions is accelerating adoption among independent and medium-sized pharmacies. Integration with hospital information systems and electronic health records is another major growth factor. AI-based inventory forecasting and automated decision support tools are improving efficiency. Subscription pricing models are making advanced software more affordable. Increasing telepharmacy services are also boosting software demand. Cybersecurity upgrades and remote monitoring functions further support adoption. Expansion of SaaS models and mobile accessibility will continue driving rapid segment growth.

• By Pharmacy Type

On the basis of pharmacy type, the Pharmacy Automation market is segmented into independent, chain, and federal. The chain pharmacy segment accounted for the largest market revenue share of 46.3% in 2025, driven by high prescription traffic, multi-location operations, and strong financial capability to invest in automation technologies. Chain pharmacies require standardized dispensing systems, centralized monitoring, and consistent workflow management across branches. Automation helps reduce wait times, improve customer satisfaction, and lower dispensing errors. These operators are also adopting robotics to manage repetitive tasks efficiently. Expansion of pharmacy-led healthcare services such as vaccination and wellness consultations further increases need for automation. Strong procurement power enables faster adoption of advanced systems and software. Continuous store modernization programs support long-term segment dominance. Large retail brands are increasingly integrating digital prescription management with in-store automation. Demand for scalable solutions across nationwide networks remains high. The segment benefits from strong brand presence and growing healthcare retail expansion.

The independent pharmacy segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by growing need to improve efficiency and compete with larger chains. Affordable modular automation systems are making adoption feasible for smaller operators. Independent pharmacies are using software tools for refill management, customer engagement, and inventory optimization. Rising labor shortages are encouraging investment in automation. Personalized care models supported by faster workflows are improving competitiveness. Government support for healthcare digitization is another growth factor. Leasing and subscription options reduce upfront costs. Growing rural healthcare demand is supporting smaller pharmacy modernization. Increased focus on profitability and productivity will continue driving segment expansion.

• By Pharmacy Size

On the basis of pharmacy size, the Pharmacy Automation market is segmented into large size pharmacy, medium size pharmacy, and small size pharmacy. The large size pharmacy segment dominated the largest market revenue share of 51.4% in 2025, driven by high medicine volumes, extensive inventories, and complex dispensing requirements. Large pharmacies often operate multiple counters and require advanced systems to maintain efficiency. Automation enables rapid prescription fulfillment, reduced human error, and better patient flow management. These facilities have higher budgets for robotics, conveyor systems, and enterprise software integration. Hospitals and metropolitan pharmacies significantly contribute to segment leadership. Strong compliance requirements also encourage technology upgrades. Large pharmacies increasingly adopt centralized automation hubs for bulk operations. Demand for smart inventory control and real-time reporting remains strong. Continuous modernization of high-volume pharmacies supports growth. The segment benefits from economies of scale and greater ROI from automation investments.

The medium size pharmacy segment is expected to witness the fastest CAGR of 10.6% from 2026 to 2033, driven by increasing modernization among regional operators. Medium-sized pharmacies are adopting scalable automation solutions that balance cost and performance. Rising prescription loads and customer expectations are encouraging faster service models. Inventory control software and semi-automated dispensing units are gaining traction. Financing programs and vendor leasing options support adoption. Competitive pressure from large chains is accelerating digital transformation. These pharmacies seek productivity gains without heavy capital burden. Growing urban healthcare demand further supports expansion. Continued accessibility of modular solutions will sustain strong growth.

• By Application

On the basis of application, the Pharmacy Automation market is segmented into drug dispensing and packaging, and drug storage and inventory management. The drug dispensing and packaging segment held the largest market revenue share of 57.8% in 2025, driven by increasing prescription volumes and rising need to minimize medication errors. Automated dispensing systems improve dosage accuracy, labeling precision, and prescription turnaround times. Hospitals and retail pharmacies are increasingly investing in unit-dose packaging solutions for patient safety. Robotic filling systems reduce repetitive manual tasks and improve labor productivity. Demand for same-day prescription delivery is also supporting segment growth. Regulatory emphasis on traceability and proper labeling strengthens adoption. Aging populations and chronic disease prevalence continue increasing medicine demand globally. Centralized fill pharmacies are further boosting packaging automation needs. Continuous innovation in dispensing robotics supports long-term market dominance. The segment remains essential to efficient pharmacy workflow operations.

The drug storage and inventory management segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, driven by increasing focus on reducing wastage and stockouts. Pharmacies are adopting RFID cabinets, automated shelving, and predictive analytics tools. Real-time stock visibility improves procurement decisions and medicine availability. Rising specialty and temperature-sensitive drugs require advanced storage systems. Expiry management tools reduce losses and improve compliance. Smart inventory systems also optimize working capital usage. Hospitals increasingly prioritize secure controlled-drug storage solutions. Integration with dispensing platforms enhances workflow efficiency. Growing demand for intelligent supply chain systems will support strong future growth.

• By End User

On the basis of end user, the Pharmacy Automation market is segmented into inpatient pharmacies, outpatient pharmacies, retail pharmacies, online pharmacies, central fill/mail order pharmacies, pharmacy benefit management organizations, and others. The retail pharmacies segment dominated the largest market revenue share of 39.6% in 2025, driven by high daily prescription traffic and growing consumer demand for faster service. Retail operators use automation to reduce queues, improve dispensing accuracy, and manage recurring prescriptions efficiently. Strong expansion of pharmacy chains and neighborhood stores supports segment leadership. Automated kiosks and digital counters are becoming increasingly common. Rising OTC medicine sales also contribute to workflow complexity and automation demand. Retail pharmacies benefit significantly from labor cost optimization. Integration of loyalty apps and e-prescription systems further supports adoption. Growing vaccination and wellness services are increasing operational workloads. Continuous modernization programs strengthen segment growth worldwide. Consumer convenience remains a major driver for this segment.

The online pharmacies segment is anticipated to witness the fastest CAGR of 13.4% from 2026 to 2033, driven by rapid e-commerce expansion and rising preference for home delivery medicines. Automated fulfillment centers are improving order speed and accuracy. Digital prescription uploads and subscription refill models are boosting convenience. Telehealth integration is increasing online medicine purchases. Centralized robotic warehouses support scalable operations. Competitive pricing and doorstep delivery continue attracting users. Demand from elderly and chronic care patients is rising strongly. AI-driven order routing and inventory systems improve margins. Ongoing investment in digital healthcare logistics will sustain rapid segment growth.

Urinary Catheters Market Regional Analysis

- North America dominated the urinary catheters market with the largest revenue share of 39.68% in 2025, supported by well-established healthcare infrastructure, high healthcare expenditure, and widespread adoption of advanced catheter products

- The region benefits from a growing geriatric population, higher incidences of urinary incontinence and prostate-related disorders, and frequent innovations in catheter materials and coatings aimed at reducing catheter-associated urinary tract infections (CAUTIs)

- Hospitals, long-term care facilities, and home healthcare services are increasingly adopting technologically advanced catheters, including coated and gender-specific designs. Awareness campaigns, robust insurance coverage, and strong distribution networks further strengthen market penetration

U.S. Urinary Catheters Market Insight

The U.S. urinary catheters market captured the largest revenue share within North America in 2025, driven by rising demand for advanced catheter technologies and preventive care measures against CAUTIs. Healthcare providers are focusing on improved patient comfort and safety through coated and disposable catheters. Government guidelines, healthcare reimbursement policies, and increasing awareness of urological health accelerate adoption. Moreover, innovations in antimicrobial and low-friction catheter designs are enhancing patient compliance and hospital efficiency. The growth is further supported by the expansion of outpatient care, home healthcare, and telehealth integration, enabling easier access to urinary catheter products for patients managing chronic conditions at home.

Europe Urinary Catheters Market Insight

The Europe urinary catheters market is projected to grow steadily during the forecast period, driven by strong regulatory frameworks, established healthcare systems, and growing awareness of urological health. Increasing incidences of urinary tract infections and age-related urinary complications are boosting demand for advanced catheter solutions. Hospitals and long-term care facilities are upgrading to coated, single-use, and specialized catheters to reduce infection risk and improve patient comfort. Urbanization, rising healthcare expenditure, and technological adoption in countries like Germany, France, and Italy are creating favorable conditions for market expansion. In addition, government initiatives promoting preventive healthcare and clinical guidelines for catheter usage are contributing to widespread adoption.

U.K. Urinary Catheters Market Insight

The U.K. urinary catheters market is anticipated to grow at a notable CAGR, driven by the increasing focus on geriatric care, urological health awareness, and adoption of innovative catheter products. Hospitals, care homes, and home-care services prefer disposable and coated catheters to ensure hygiene and patient safety. Rising healthcare expenditure, government support for elderly care, and awareness campaigns are fostering adoption. E-commerce and robust retail distribution further enhance market penetration, allowing patients and caregivers to access specialized urinary catheter products conveniently.

Germany Urinary Catheters Market Insight

The Germany Urinary Catheters ma urinary catheters market is expected to expand at a considerable CAGR, supported by advanced healthcare infrastructure, strong clinical practices, and technological innovation. Hospitals and long-term care facilities are increasingly adopting coated, single-use, and specialized catheters for patients with urinary incontinence, spinal injuries, or prostate-related conditions. Awareness of CAUTI prevention, coupled with stringent hygiene regulations, drives demand. Germany’s aging population, high disposable incomes, and preference for patient-friendly catheter designs further support market growth. In addition, integration of catheters with home-care services and outpatient facilities enhances accessibility and convenience.

Asia-Pacific Urinary Catheters Market Insight

The Asia-Pacific urinary catheters market is poised to grow at the fastest CAGR of 24% during the forecast period, driven by increasing awareness of urological health, rising incidences of urinary incontinence, and improving healthcare infrastructure. Countries such as China and India are witnessing high demand due to growing geriatric populations, rising disposable incomes, and enhanced accessibility to modern healthcare services. Expansion of hospitals, long-term care facilities, and home healthcare services is promoting adoption. Furthermore, technological innovations in coated, low-friction, and disposable catheters improve patient comfort and safety. Government initiatives, health awareness campaigns, and an increasing focus on chronic disease management further accelerate market growth.

Japan Urinary Catheters Market Insight

The Japan urinary catheters market is gaining momentum due to the country’s aging population, high healthcare standards, and strong focus on patient comfort. Hospitals and home-care providers are increasingly adopting advanced catheter designs, including coated and single-use types, to reduce infection risks and enhance usability. Integration with home healthcare services and increased awareness of urological health are boosting adoption. In addition, the demand for patient-friendly, minimally invasive devices is high, supporting growth in both institutional and home-care segments.

China Urinary Catheters Market Insight

The China urinary catheters market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, rapid urbanization, and rising incidences of urinary incontinence and prostate-related disorders. Increasing awareness of urological health, coupled with improvements in healthcare infrastructure and accessibility, is driving adoption. Hospitals, long-term care facilities, and home-care services are embracing advanced, coated, and disposable catheter solutions. Technological innovations, cost-effective solutions, and government healthcare initiatives further contribute to market growth. China’s position as a manufacturing hub for urinary catheter products also facilitates availability and affordability, supporting widespread adoption.

Urinary Catheters Market Share

The Urinary Catheters industry is primarily led by well-established companies, including:

- Coloplast (Denmark)

- B. Braun SE (Germany)

- BD (U.S.)

- Hollister Incorporated (U.S.)

- Medtronic (Ireland)

- Teleflex Incorporated (U.S.)

- Cook Medical (U.S.)

- ConvaTec Group PLC (U.K.)

- Rocamed (France)

- Boston Scientific Corporation (U.S.)

- Bactiguard AB (Sweden)

- Amsino International, Inc. (U.S.)

- Well Lead Medical Co., Ltd. (China)

- Zhanjiang Star Enterprise Co., Ltd. (China)

- Jinan Chensheng Medical Silicone Rubber Product Co., Ltd. (China)

- Guangdong Haiou Medical Apparatus Co., Ltd. (China)

- Henan Shuguang Jianshi Medical Equipment Group Co., Ltd. (China)

- Urocare Products, Inc. (U.S.)

- Degania Silicone Ltd. (Israel)

- CURE MEDICAL, LLC (U.S.)

- Medical Technologies of Georgia (U.S.)

Latest Developments in Global Urinary Catheters Market

- In February 2021, Bactiguard announced that Health Canada had approved its urinary catheter equipped with a temperature sensor under a COVID-19 Interim Order. This approval was driven by the need to reduce secondary infections in critically ill patients, particularly in ICU settings, during the pandemic. The catheter's integrated temperature monitoring aims to enhance patient safety and infection control

- In November 2022, Ur24Technology launched its innovative TrueClr external catheter line at Medica 2022 in Düsseldorf, Germany. The latex-free catheter system is designed for men, women, and children, helping actively empty the bladder while minimizing the risk of urinary tract infections. Developed in collaboration with DemeTECH, this product line combines innovation with established global distribution capabilities, aiming to improve patient comfort and clinical outcomes

- In March 2025, Ur24Technology introduced a reusable version of its TrueClr external catheter system. This development offers a sustainable alternative to traditional catheters, catering to the growing demand for eco-friendly medical solutions. The reusable design maintains the product's commitment to comfort and infection prevention, aligning with environmental sustainability goals

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.