Global Urgent Care Center Market

Market Size in USD Billion

CAGR :

%

USD

27.30 Billion

USD

41.27 Billion

2024

2032

USD

27.30 Billion

USD

41.27 Billion

2024

2032

| 2025 –2032 | |

| USD 27.30 Billion | |

| USD 41.27 Billion | |

| % | |

|

Urgent Care Center Market Size

Urgent Care Center Market Size

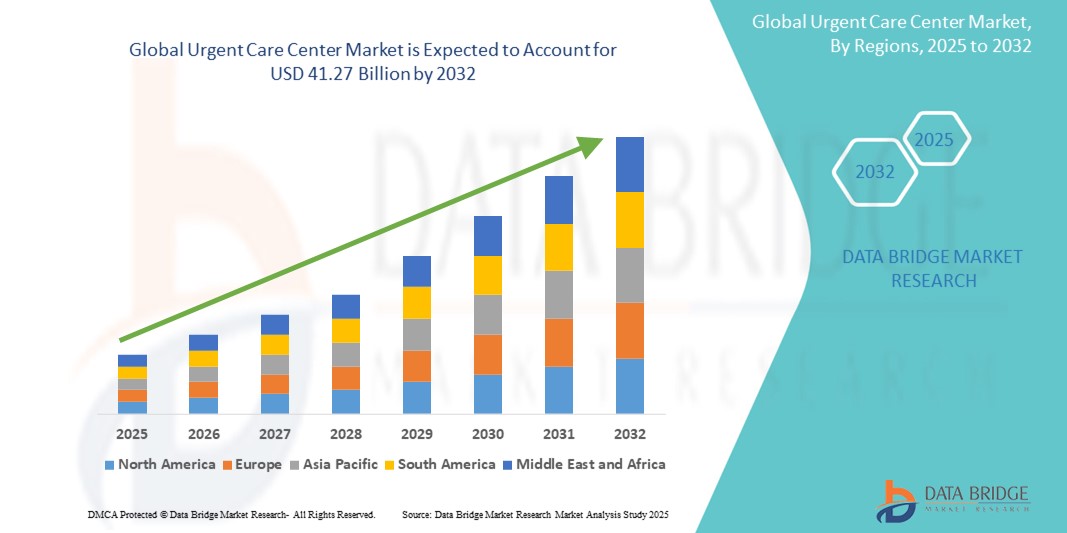

- The global urgent care center market was valued at USD 27.30 billion in 2024 and is expected to reach USD 41.27 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 5.3%, primarily driven by the rising healthcare cost

- This growth is driven by factors such as the growing patient population and growing demand for accessible and affordable healthcare services

Urgent Care Center Market Analysis

- Urgent care centers are essential components of the modern healthcare ecosystem, offering immediate, walk-in care for non-life-threatening conditions such as minor injuries, infections, sprains, and common illnesses. These centers fill the gap between primary care physicians and emergency departments by providing timely and affordable medical attention

- The demand for urgent care services is primarily driven by rising healthcare costs, long wait times in emergency rooms, and the shortage of primary care providers. As healthcare systems globally face increasing strain, urgent care centers offer a convenient solution with extended hours and faster service

- North America stands out as the dominant market for urgent care centers, particularly in the United States, where consumer preference for fast, accessible care is growing rapidly. The presence of well-established healthcare infrastructure, strong insurance penetration, and a shift toward value-based care have accelerated the growth of urgent care facilities

- For instance, in the U.S., urgent care visits have seen significant growth over the past decade, with healthcare providers and investors expanding clinic networks across both urban and suburban areas. Retail giants and health systems alike are investing in this model to improve patient reach and reduce emergency room burden

- Globally, urgent care centres are gaining importance as a cost-effective and efficient alternative to emergency departments, especially in managing acute but non-emergent medical conditions. Their ability to offer services such as diagnostics, lab testing, vaccinations, and minor procedures makes them a vital part of outpatient care delivery systems

Report Scope and Urgent Care Center Market Segmentation

|

Attributes |

Urgent Care Center Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Urgent Care Center Market Trends

“Growing Integration of Telehealth and Digital Solutions”

- One prominent trend in the global urgent care center market is the increasing integration of telehealth platforms and digital health technologies to enhance care delivery and expand access to medical services

- These digital tools allow urgent care centers to provide virtual consultations, remote triage, and electronic health record (EHR) integration, improving operational efficiency and patient convenience

- For instance, tele-urgent care services enable patients to consult with healthcare providers from home for conditions such as flu symptoms, minor infections, and medication refills—reducing in-clinic congestion and expanding access to care in remote or underserved areas

- The use of digital platforms also streamlines administrative processes such as appointment scheduling, patient intake, billing, and follow-up care, which boosts overall clinic productivity and enhances patient satisfaction

- This trend is transforming urgent care delivery by offering hybrid care models (in-person + virtual), reducing wait times, and allowing for quicker diagnosis and treatment, ultimately improving patient outcomes while supporting the scalability of urgent care networks

Urgent Care Center Market Dynamics

Driver

“Growing Demand for Accessible and Affordable Healthcare Services”

- The increasing demand for urgent care services is driven by the rising need for quick, accessible, and affordable healthcare in response to the growing prevalence of non-emergency conditions such as minor injuries, infections, and illnesses

- Urgent care centers offer a convenient alternative to emergency rooms for patients seeking immediate care without the long wait times or high costs associated with hospital visits

- The aging population and the increasing incidence of chronic conditions further fuel the demand for urgent care services as more individuals require timely treatment for acute and non-acute health issues

- The convenience of extended hours, lower cost of treatment, and quick access to care make urgent care centers an attractive option, driving the market’s growth

For instance,

- In 2023, the American Urgent Care Association reported a steady increase in urgent care visits, with over 160 million visits annually, highlighting the need for accessible care solutions, especially for non-emergency healthcare situations

- The growing demand for urgent care services is driven by the need for quick, accessible, and affordable healthcare, fueled by the increasing prevalence of non-emergency conditions and the aging population

Opportunity

“Expansion of Telehealth Services in Urgent Care Centers”

- The growing integration of telemedicine and digital health platforms in urgent care centers offers a significant opportunity for market growth

- Telehealth services allow patients to consult healthcare providers remotely, extending urgent care accessibility, especially for rural or underserved populations. This helps to reduce patient wait times, enhances care delivery efficiency, and allows for easier management of minor illnesses and injuries from home

- The COVID-19 pandemic accelerated the adoption of telemedicine, and many urgent care centers continue to offer virtual consultations, helping to expand their reach while reducing the strain on physical clinics

For instance,

- In 2024, CVS Health expanded its MinuteClinic Virtual Care platform, allowing patients to access urgent care services remotely via their smartphones or computers, improving accessibility and convenience for those unable to visit clinics in person

- The integration of telemedicine in urgent care centers enhances accessibility, reduces wait times, and expands reach, especially for rural and underserved populations, with platforms such as CVS Health's MinuteClinic Virtual Care improving convenience

Restraint/Challenge

“Regulatory Challenges and Reimbursement Issues”

- The regulatory environment for urgent care centers presents a significant challenge, particularly concerning licensing requirements, reimbursement policies, and operational standards

- In some regions, the lack of clear reimbursement models for urgent care services under health insurance plans hinders growth and can result in financial uncertainty for operators

- In addition, the regulatory complexities surrounding telemedicine and the need for compliance with local laws and healthcare regulations can complicate the implementation of remote services within urgent care centers

For instance,

- In 2023, a report from the National Urgent Care Center Association highlighted that 35% of urgent care centers in the U.S. faced difficulties in securing reimbursement for telehealth visits, impacting their ability to scale and expand these services effectively

- The regulatory challenges, including unclear reimbursement models and telemedicine compliance, create financial uncertainty and hinder the growth and expansion of urgent care centers

Urgent Care Center Market Scope

The market is segmented on the basis of service and ownership.

|

Segmentation |

Sub-Segmentation |

|

By Service |

|

|

By Ownership |

|

Urgent Care Center Market Regional Analysis

“North America is the Dominant Region in the Critical Care Market”

- North America leads the Critical Care market, driven by a robust healthcare infrastructure, high adoption of advanced medical technologies, and a significant presence of leading healthcare providers

- U.S. holds a large share due to the increasing demand for advanced critical care treatments, rising cases of chronic diseases, and continuous advancements in medical devices and ICU technologies

- The availability of comprehensive insurance coverage, government support, and high investment in healthcare R&D further strengthens the market

- In addition, the rising number of emergency medical interventions and intensive care procedures, particularly for critical conditions such as cardiovascular diseases and respiratory failures, is boosting market expansion across the region

“Asia-Pacific is Projected to Register the Highest Growth Rate”

- Asia-Pacific is expected to experience the highest growth rate in the critical care market, driven by rapid healthcare infrastructure development, growing awareness about emergency medical services, and rising incidences of chronic and critical illnesses

- Countries such as China, India, and Japan are emerging as key markets due to their large populations, aging demographics, and increasing demand for advanced critical care facilities

- Japan, with its cutting-edge healthcare technologies and well-established critical care systems, continues to be a significant market player. The country leads in adopting innovative medical equipment to improve patient outcomes in intensive care units

- China and India, with their expanding healthcare sectors and increasing cases of life-threatening conditions, are witnessing increased investments in critical care facilities, as well as the adoption of advanced medical devices, further contributing to market growth

Urgent Care Center Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Concentra, Inc. (U.S.)

- MedExpress (U.S.)

- American Family Care (U.S.)

- NextCare (U.S.)

- GoHealth Urgent Care (U.S.)

- HCA Management Services, L.P. (U.S.)

- International SOS (Singapore)

- FastMed Urgent Care (U.S.)

- Urgent Care Group (U.S.)

- Optum, Inc. (U.S.)

- Summit Health Management, LLC. (U.S.)

- C-HCA, Inc. (U.S.)

- WellNow Urgent Care (U.S.)

- Sutter Health (U.S.)

- Ascension (U.S.)

- Aurora Health Care (U.S.)

- St. Joseph's Health Care London (Canada)

Latest Developments in Global Urgent Care Center Market

- In January 2025, CVS Health expanded its MinuteClinic Virtual Care platform, allowing patients to access urgent care services remotely through their smartphones or computers. This expansion of telehealth services improves accessibility and convenience, especially for patients in underserved areas, and aligns with the growing demand for virtual care solutions

- In December 2024, American Family Care (AFC) announced the opening of its 300th clinic in the U.S., signaling the continued expansion of urgent care centers across the country. AFC's clinics provide a wide range of services, including treatment for minor injuries, illnesses, and preventive care, contributing to the overall growth of the urgent care sector

- In November 2024, Urgent Care Association (UCA) published a report showing a 12% increase in the number of urgent care visits in the U.S., with over 170 million visits annually. This surge highlights the rising demand for convenient, accessible, and affordable healthcare services for non-emergency conditions

- In October 2024, NextCare Urgent Care launched a new integrated patient management system across its network of clinics, enabling seamless coordination between in-person and telehealth services. The new system aims to enhance patient experience, reduce wait times, and optimize resource allocation in urgent care centers

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.