Global Third Party Risk Management Market

Market Size in USD Billion

CAGR :

%

USD

7.92 Billion

USD

30.82 Billion

2023

2031

USD

7.92 Billion

USD

30.82 Billion

2023

2031

| 2024 –2031 | |

| USD 7.92 Billion | |

| USD 30.82 Billion | |

| % | |

|

Third-Party Risk Management Market Size

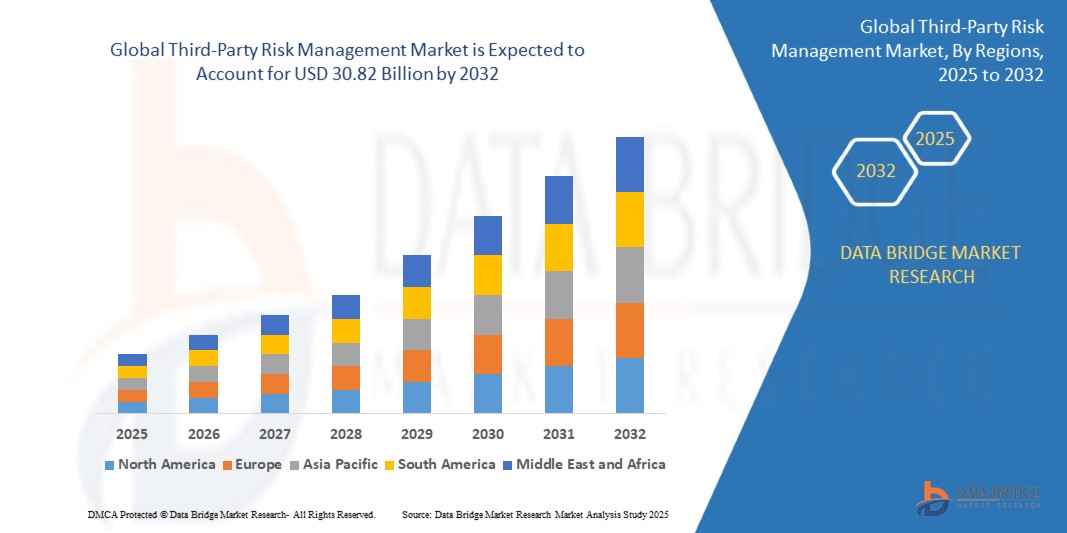

- The global third-party risk management market size was valued at USD 7.92 billion in 2024 and is expected to reach USD 30.82 billion by 2032, at a CAGR of 18.50% during the forecast period

- The market growth is largely fuelled by the increasing reliance on external vendors, growing regulatory scrutiny, and the rising need for risk mitigation across supply chains

- The rapid expansion of digital ecosystems and remote operations has heightened the exposure to third-party risks, accelerating the demand for integrated risk management solutions

Third-Party Risk Management Market Analysis

- The market is witnessing significant demand across industries such as banking, healthcare, retail, and information technology due to increasing complexities in vendor ecosystems

- The rise in data privacy regulations such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) is prompting organizations to adopt robust third-party risk management (TPRM) platforms

- North America dominated the third-party risk management market with the largest revenue share of 41.2% in 2024, driven by increasing cybersecurity concerns, regulatory compliance requirements, and the widespread adoption of digital transformation across industries

- Asia-Pacific region is expected to witness the highest growth rate in the global third-party risk management market, driven by rising awareness around third-party risks, growing cross-border trade, and the adoption of cloud-based risk management solutions among emerging economies such as India, China, and Southeast Asian nations

- The solutions segment accounted for the largest revenue share of 62.5% in 2024, driven by the increasing demand for centralized platforms that streamline vendor risk assessments, automate compliance monitoring, and ensure due diligence. Enterprises are leveraging comprehensive risk management software to consolidate third-party data and generate actionable insights, particularly in highly regulated industries such as banking and healthcare

Report Scope and Third-Party Risk Management Market Segmentation

|

Attributes |

Third-Party Risk Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Third-Party Risk Management Market Trends

“Increasing Integration of Artificial Intelligence and Machine Learning in Risk Assessment”

- Organizations are increasingly adopting artificial intelligence and machine learning technologies to streamline vendor due diligence workflows, reducing manual effort while enabling faster and more accurate profiling of third-party risks

- Real-time monitoring through AI-driven systems allows companies to detect anomalies in vendor behavior such as sudden performance drops or compliance gaps, enabling early intervention and reducing exposure to operational risks

- Machine learning algorithms improve over time by learning from historical data and user feedback, which enhances their ability to forecast emerging threats and fine-tune risk classification for dynamic third-party ecosystems

- AI-powered platforms support compliance functions by automatically generating audit trails, documentation, and alerts, significantly reducing the burden of regulatory reporting and improving accuracy across departments

- For instance, Prevalent’s AI-enabled platform equips large enterprises with predictive analytics tools to continuously monitor vendor health and provide actionable insights into potential risk areas before issues escalate

Third-Party Risk Management Market Dynamics

Driver

“Rising Regulatory Pressure and Compliance Mandates”

- The growing enforcement of regulations such as the General Data Protection Regulation (GDPR), California Consumer Privacy Act (CCPA), and Foreign Corrupt Practices Act (FCPA) is compelling firms to formalize structured third-party risk management frameworks

- Companies are increasingly integrating automated risk management solutions to centralize data, reduce manual compliance errors, and maintain consistent documentation across global vendor networks

- High-profile regulatory penalties such as the EUR 746 million fine levied against Amazon under GDPR underscore the financial consequences of inadequate vendor oversight and the need for robust risk protocols

- Organizations are now required to demonstrate due diligence and continuous monitoring during audits, driving the adoption of scalable systems that provide real-time transparency and auditable compliance records

- For instance, ProcessUnity’s third-party risk management platform allows financial institutions to automate risk scoring, track assessment progress, and maintain audit-ready documentation for regulatory inspections

Restraint/Challenge

“Lack of Standardization in Risk Metrics and Assessment Models”

- The absence of industry-wide standards results in fragmented third-party risk evaluation approaches across sectors and geographies, making it difficult to compare or benchmark vendor risks accurately

- Vendors often face assessment fatigue when they receive multiple risk questionnaires from different clients, each with varying formats, requirements, and scoring methodologies, leading to inefficiencies and delays

- Small and medium-sized enterprises often lack the tools, expertise, or dedicated personnel required to keep up with the diverse compliance expectations of larger clients, putting them at a competitive disadvantage

- Without standardized metrics, businesses struggle to prioritize which vendor poses the greatest risk, resulting in over or under-allocation of monitoring resources and gaps in risk mitigation strategies

- For instance, a cloud service provider supporting both financial and healthcare clients must meet disparate compliance requirements such as SOC 2 for finance and HIPAA for healthcare, which complicates documentation and operational procedures across the board

Third-Party Risk Management Market Scope

The market is segmented on the basis of component, deployment model, organization size, and end user.

• By Component

On the basis of component, the third-party risk management market is segmented into solutions and services. The solutions segment accounted for the largest revenue share of 62.5% in 2024, driven by the increasing demand for centralized platforms that streamline vendor risk assessments, automate compliance monitoring, and ensure due diligence. Enterprises are leveraging comprehensive risk management software to consolidate third-party data and generate actionable insights, particularly in highly regulated industries such as banking and healthcare.

The services segment is expected to witness the fastest growth rate from 2025 to 2032, propelled by the growing need for consulting, integration, and managed services. Organizations are increasingly turning to external experts to navigate complex regulatory landscapes, assess critical supply chain risks, and implement scalable risk mitigation frameworks tailored to evolving business environments.

• By Deployment Model

On the basis of deployment model, the market is segmented into on-premise and cloud. The cloud segment held the largest market share in 2024, supported by its scalability, lower upfront investment, and ease of access for remote teams. Cloud-based third-party risk management solutions enable real-time updates, centralized vendor databases, and seamless integration with other enterprise systems, making them ideal for dynamic, compliance-driven environments.

The on-premise segment is expected to witness the fastest growth rate from 2025 to 2032, among organizations with stringent data control requirements, especially in sectors such as defense and finance. These deployments offer enhanced security and customization, making them suitable for businesses that require local infrastructure and greater autonomy over sensitive third-party data.

• By Organization Size

Based on organization size, the market is categorized into large enterprises and small and medium-sized enterprises (SMEs). The large enterprises segment dominated the market with the highest revenue share in 2024, driven by complex vendor ecosystems and heightened compliance responsibilities. These organizations typically operate in multiple jurisdictions and require advanced risk analytics and automation to ensure effective oversight of numerous third-party relationships.

The SME segment is expected to witness the fastest growth rate from 2025 to 2032, supported by the increasing affordability of cloud-based platforms and growing awareness of reputational risks. SMEs are gradually embracing third-party risk management tools to improve supplier transparency, streamline onboarding, and minimize operational disruptions caused by vendor non-compliance.

• By End User

By end user, the third-party risk management market is segmented into government, aerospace and defense, banking, financial services and insurance (BFSI), manufacturing, IT and telecom, energy and utilities, retail and consumer goods, healthcare and life sciences, and others. The BFSI segment captured the largest revenue share in 2024, attributed to strict regulatory mandates and the need for enhanced oversight of outsourced service providers and financial intermediaries. Financial institutions are investing in integrated risk platforms that automate due diligence, monitor third-party conduct, and support regulatory reporting.

The healthcare and life sciences segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the rising need to assess supply chain vulnerabilities, ensure data privacy compliance, and protect patient information. With increasing collaboration between healthcare providers, pharmaceutical companies, and digital solution vendors, robust third-party risk management frameworks are becoming critical for operational integrity and regulatory adherence.

Third-Party Risk Management Market Regional Analysis

- North America dominated the third-party risk management market with the largest revenue share of 41.2% in 2024, driven by increasing cybersecurity concerns, regulatory compliance requirements, and the widespread adoption of digital transformation across industries

- Organizations in the region are actively deploying third-party risk management platforms to monitor vendor activities, manage contractual obligations, and minimize data breaches

- The high concentration of financial institutions, government contractors, and healthcare providers is fostering demand for automated, scalable risk management solutions

U.S. Third-Party Risk Management Market Insight

The U.S. third-party risk management market accounted for the largest revenue share in 2024 within North America, fueled by the growing volume of outsourced operations and the rising number of third-party cyberattacks. Organizations are strengthening due diligence protocols and integrating vendor risk platforms to ensure compliance with regulations such as the Health Insurance Portability and Accountability Act (HIPAA) and Federal Risk and Authorization Management Program (FedRAMP). The adoption of AI-driven monitoring tools is further supporting real-time risk scoring and automated alerts, helping enterprises secure their supply chains and vendor ecosystems

Europe Third-Party Risk Management Market Insight

The Europe third-party risk management market is expected to witness the fastest growth rate from 2025 to 2032, driven by the introduction of robust data privacy frameworks such as the General Data Protection Regulation (GDPR). European enterprises are increasingly adopting risk management software to assess compliance risks, monitor data sharing, and prevent violations by third-party vendors. In addition, rising supply chain disruptions and geopolitical uncertainties have prompted companies across the United Kingdom, Germany, and France to invest in resilient third-party governance strategies for enhanced transparency and accountability

U.K. Third-Party Risk Management Market Insight

The U.K. third-party risk management market is expected to witness the fastest growth rate from 2025 to 2032, backed by stringent corporate governance standards and mounting pressure on enterprises to safeguard sensitive customer data. Organizations are increasingly deploying vendor assessment tools and audit trails to identify financial, legal, and operational risks. The country's expanding financial services and fintech sectors, which depend heavily on third-party service providers, are also accelerating the adoption of integrated risk platforms to ensure business continuity and regulatory compliance

Germany Third-Party Risk Management Market Insight

The Germany third-party risk management market is expected to witness the fastest growth rate from 2025 to 2032, supported by a strong focus on industrial cybersecurity and sustainable supply chain management. German manufacturers and automotive firms are leveraging digital tools to evaluate supplier performance, ESG risks, and compliance status. With the implementation of the Supply Chain Due Diligence Act (SCDDA), businesses in Germany are increasingly investing in automated third-party monitoring systems to reduce reputational and regulatory risks while enhancing corporate responsibility

Asia-Pacific Third-Party Risk Management Market Insight

The Asia-Pacific third-party risk management market is expected to witness the fastest growth rate from 2025 to 2032, driven by the proliferation of cloud computing, outsourcing, and digital ecosystems across countries such as India, China, and Singapore. Enterprises in the region are adopting risk assessment tools to manage third-party relationships amid rising cybersecurity threats and evolving compliance mandates. Government initiatives promoting data localization, supply chain transparency, and digital infrastructure are further stimulating the adoption of third-party risk solutions

Japan Third-Party Risk Management Market Insight

The Japan third-party risk management market is expected to witness the fastest growth rate from 2025 to 2032, owing to the country's increasing focus on information security, vendor accountability, and compliance management. Japanese enterprises are investing in robust due diligence tools and continuous monitoring platforms to evaluate the operational and financial health of suppliers and partners. The market is further supported by the growing reliance on third-party IT service providers and the rising adoption of digital procurement processes, prompting companies to implement comprehensive risk governance frameworks

China Third-Party Risk Management Market Insight

The China third-party risk management market held a significant share in the Asia-Pacific region in 2024, driven by the rapid expansion of the digital economy and the growing emphasis on vendor transparency. Chinese businesses are increasingly focusing on risk mitigation strategies to ensure compliance with data protection laws such as the Personal Information Protection Law (PIPL). The emergence of domestic third-party risk solution providers, coupled with government-backed initiatives for improving supply chain resilience, is fostering growth in sectors such as manufacturing, telecommunications, and banking

Third-Party Risk Management Market Share

The Third-Party Risk Management industry is primarily led by well-established companies, including:

- RSA Security LLC (U.S.)

- MetricStream (U.S.)

- KPMG International (U.K.)

- Deloitte (U.K.)

- BitSight Technologies (U.S.)

- ProcessUnity, Inc. (U.S.)

- Genpact (U.S.)

- Venminder, Inc. (U.S.)

- Resolver, Inc. (Canada)

- NAVEX Global, Inc. (U.S.)

- SAI Global Compliance, Inc. (Australia)

- Rapid Ratings International Inc. (U.S.)

- Optiv Security Inc. (U.S.)

- PwC (U.K.)

- Aravo Solutions, Inc. (U.S.)

- OneTrust, LLC (U.S.)

- Prevalent, Inc. (U.S.)

- MITRATECH (U.S.)

- Ernst & Young Global Limited (U.K.)

- IBM Corporation (U.S.)

Latest Developments in Global Third-Party Risk Management Market

- In October 2023, Optiv Security Inc. achieved recognition as a Leader in the IDC MarketScape: Worldwide Cybersecurity Risk Management (CRM) Services 2023 Vendor Assessment. The assessment highlighted Optiv's comprehensive risk management services and proactive guidance in navigating the escalating cyber threat landscape. This acknowledgment in the respected IDC MarketScape contributed to the company's success by showcasing its expertise and effectiveness in helping clients achieve their business and risk management objectives

- In April 2021, MetricStream announced the launch of Arno software, including numerous features and innovations added to its platform and products. It also successfully added new capabilities to Internal Audit Management, Policy and Compliance Management, and Third-Party Risk Management products. With this the company was able to set a new standard for governance, risk and compliance and integrated risk management, further enabling organizations to leverage risk as a strategic advantage

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.