Global Textile Dyestuff Market

Market Size in USD Million

CAGR :

%

USD

899.99 Million

USD

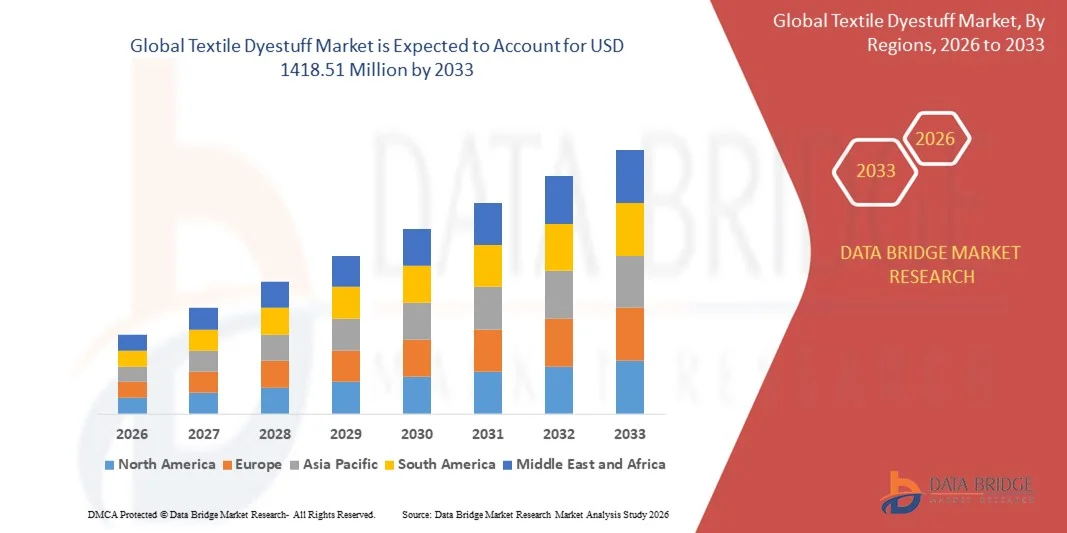

1,418.51 Million

2025

2033

USD

899.99 Million

USD

1,418.51 Million

2025

2033

| 2026 - 2033 | |

| USD 899.99 Million | |

| USD 1,418.51 Million | |

| % | |

|

What is the Global Textile Dyestuff Market Size and Growth Rate?

- The global textile dyestuff market size was valued at USD 899.99 million in 2025 and is expected to reach USD 1418.51 million by 2033, at a CAGR of 6.00% during the forecast period

- Rising strong research and development investments in plant-based dyes is the vital factor escalating the market growth, also rising innovation in the textile dyes industry, rising demand for textile dyes and low-cost of manufacturing in APAC countries, low-cost of manufacturing in APAC countries, increasing demand for textile dyes in APAC and increase in preference for non-woven fabrics are the major factors among others driving the textile dyestuff market

What are the Major Takeaways of Textile Dyestuff Market?

- Rising development of low-Vac and eco-friendly products and minimizing the water wastage and organic dyes will further create new opportunities for the textile dyestuff market

- However, rising stringent rules and regulations and increasing toxic waste production are the major factors among others acting as restraints, while rising overcapacity of dyestuffs will further challenge the growth of textile dyestuff market

- Asia-Pacific dominated the textile dyestuff market with a 43.5% revenue share in 2025, supported by the strong presence of textile manufacturing hubs across China, India, Bangladesh, Vietnam, and Indonesia

- North America is projected to register the fastest CAGR of 10.98% from 2026 to 2033, driven by advancements in sustainable dyeing technologies, rising demand for environmentally friendly dyestuffs, and increasing adoption in technical textiles, sportswear, home furnishings, and industrial fabrics

- The Reactive dye segment dominated the market with a revenue share of 36.8% in 2025, driven by its strong bonding properties, excellent wash fastness, and wide application in cotton and cellulosic fibers

Report Scope and Textile Dyestuff Market Segmentation

|

Attributes |

Textile Dyestuff Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Textile Dyestuff Market?

Growing Shift Toward Eco-Friendly, High-Performance, and Bio-Based Textile Dyestuffs

- The textile dyestuff market is witnessing a significant shift toward sustainable, bio-based, and low-impact dye formulations, driven by rising environmental concerns and tightening global regulations on hazardous chemicals

- Manufacturers are developing multi-functional dyestuffs with enhanced color fastness, UV resistance, anti-microbial properties, and energy-efficient application processes to support advanced textile performance needs

- Consumers and brands increasingly prefer natural, non-toxic, and biodegradable dyes, supporting ethical fashion, circular textiles, and reduced wastewater generation

- For instance, companies such as BASF, Archroma, Huntsman, DyStar, and Kiri Industries have expanded their eco-friendly dye ranges, including plant-based dyes and low-salt reactive dyes designed for sustainable textile processing

- Growing awareness of environmental protection, water conservation, and carbon reduction is accelerating global market adoption

- As demand for sustainable textiles continues to rise, eco-efficient and innovative dyestuff solutions will remain central to product development and industry transformation

What are the Key Drivers of Textile Dyestuff Market?

- Rising demand for sustainable, high-performance, and low-toxicity dyestuffs in apparel, home textiles, and technical fabrics is driving strong global adoption

- For instance, in 2024–2025, BASF, Archroma, and Huntsman expanded their low-water, low-energy dye technologies, supporting the textile industry’s shift toward resource-efficient coloration

- Growing textile production in Asia-Pacific, supported by population growth and rising disposable incomes, is boosting consumption of reactive, disperse, and vat dyes

- Advancements in digital textile printing, nano-dyeing, and supercritical CO₂ dyeing technologies are improving color precision, process efficiency, and environmental safety

- Increasing preference for organic textiles, recycled fibers, and eco-certified dyes is promoting market expansion, supported by global sustainability initiatives

- With continued investments in R&D, technological upgrades, and circular textile innovation, the textile dyestuff market is expected to maintain strong long-term growth

Which Factor is Challenging the Growth of the Textile Dyestuff Market?

- High production, testing, and certification costs associated with bio-based, organic, and premium sustainable dyestuffs limit adoption for cost-sensitive textile manufacturers

- For instance, during 2023–2025, fluctuations in raw material prices, petrochemical availability, and supply chain disruptions affected production stability for several dyestuff producers

- Stringent global regulations such as REACH, ZDHC, and EPA standards increase compliance requirements and operational complexities for dye manufacturers

- Limited adoption of eco-friendly dyestuffs in developing markets due to low awareness, cost constraints, and limited access to sustainable technologies restricts widespread market penetration

- Strong competition from low-cost synthetic dyes and unorganized dye producers creates pricing pressure and challenges product differentiation

- To overcome these barriers, companies are focusing on scalable production, cost-efficient sustainable formulations, regulatory alignment, and industry-wide awareness programs to strengthen global adoption of eco-friendly Textile Dyestuffs

How is the Textile Dyestuff Market Segmented?

The market is segmented on the basis of dye type, fiber type, type, and end-users.

- By Dye Type:

On the basis of dye type, the textile dyestuff market is segmented into Direct, Reactive, VAT, Basic, Acid, Disperse, and Others. The Reactive dye segment dominated the market with a revenue share of 36.8% in 2025, driven by its strong bonding properties, excellent wash fastness, and wide application in cotton and cellulosic fibers. Reactive dyes are preferred in apparel, home textiles, and printed fabrics due to bright shades, improved durability, and cost-effective processing. VAT dyes hold significant importance in premium workwear and denim applications because of their superior lightfastness and chemical resistance.

The Disperse dye segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by rising polyester production, increasing demand for sportswear, and the rapid shift toward synthetic fibers globally. Advancements in low-energy and high-dispersion formulations further accelerate adoption across Asia-Pacific. Overall, growing textile consumption and fiber diversification continue to boost demand across all dye categories.

- By Fiber Type:

On the basis of fiber type, the textile dyestuff market is segmented into Wool, Nylon, Cotton, Viscose, Polyester, Acrylic, and Others. The Polyester segment dominated the market with a revenue share of 39.5% in 2025, supported by rising polyester textile production, affordability, and its widespread use in apparel, activewear, and home furnishings. Polyester’s compatibility with disperse dyes, along with enhanced color fastness and low-cost processing, strengthens its global prominence. Cotton follows as another major consumer of dyes due to high usage in casualwear, printed garments, and household fabrics.

The Viscose segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for sustainable, breathable fabrics and expanding adoption in women’s wear, blended textiles, and eco-friendly garments. Growth in textile recycling, regenerated fibers, and circular textile initiatives further supports market expansion across all fiber categories.

- By Type:

On the basis of type, the textile dyestuff market is segmented into Cellulose, Protein, and Synthetic. The Synthetic segment dominated the market with a revenue share of 52.7% in 2025, driven by the high-volume use of polyester, nylon, and acrylic fibers across apparel, automotive textiles, performance wear, and home furnishings. Synthetic dyes provide superior color strength, fastness, and cost-effectiveness, making them the preferred choice for mass textile production. Cellulose dyes, commonly used for cotton and viscose fabrics, continue to be essential for fashion and home décor segments due to their diverse color range and application flexibility.

The Protein segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by rising demand for wool, silk, and premium blended fabrics. Increasing innovation in natural fiber processing and the shift toward sustainable luxury textiles further contribute to segment growth.

- By End-User:

On the basis of end-user, the textile dyestuff market is segmented into Apparels, Home and Institutional, Technical Textiles, and Others. The Apparels segment dominated the market with a revenue share of 46.3% in 2025, driven by rising fashion consumption, expansion of fast-fashion brands, and continuous demand for colored clothing across all demographics. Apparels utilize a wide range of dyestuffs including reactive, disperse, and VAT dyes to achieve vibrant shades, enhanced fastness, and performance characteristics.

The Technical Textiles segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing adoption in automotive, medical, protective clothing, geotextiles, and industrial applications. Growth in functional textiles, high-performance materials, and innovation in smart textiles is further accelerating demand. Overall, rising global textile production and evolving fashion trends support sustained expansion across all end-user categories.

Which Region Holds the Largest Share of the Textile Dyestuff Market?

- Asia-Pacific dominated the textile dyestuff market with a 43.5% revenue share in 2025, supported by the strong presence of textile manufacturing hubs across China, India, Bangladesh, Vietnam, and Indonesia. The region’s leadership is driven by large-scale apparel production, rapid industrialization, rising exports, and expanding demand for reactive, disperse, and VAT dyes across woven and non-woven textile applications

- Increasing investments in dye manufacturing facilities, technological upgrades in dyeing processes, and government support for textile exports further strengthen regional dominance. Growing consumption of colored apparel, home textiles, and technical textiles accelerates market expansion

- Rising urbanization, robust supply chain networks, and availability of low-cost labor and raw materials continue to position Asia-Pacific as the global leader in textile dyestuff production and consumption

China Textile Dyestuff Market Insight

China is the largest contributor to Asia-Pacific, supported by an extensive textile manufacturing ecosystem and a well-established dyestuff production infrastructure. Reactive, disperse, and VAT dyes witness strong demand across apparel, home furnishings, and industrial fabrics. Government initiatives promoting green chemistry, wastewater treatment, and sustainable dyeing enhance market capability and export competitiveness.

Japan Textile Dyestuff Market Insight

Japan shows stable growth fueled by strong demand for premium-quality dyes used in technical textiles, functional clothing, and high-performance fabrics. Innovations in low-energy dyeing, specialty dyestuffs, and high-fastness colorants attract increasing consumer and industrial interest. Strict environmental regulations and advanced automation further support market expansion.

India Textile Dyestuff Market Insight

India is emerging as a high-potential market, driven by large-scale cotton and polyester textile production, growing apparel exports, and rapid expansion of SMEs in textile processing. Rising adoption of reactive, direct, and disperse dyes across apparel, home textiles, and industrial fabrics boosts demand. Government support through textile parks, PLI schemes, and modernization programs accelerates industry growth.

North America Textile Dyestuff Market Insight

North America is projected to register the fastest CAGR of 10.98% from 2026 to 2033, driven by advancements in sustainable dyeing technologies, rising demand for environmentally friendly dyestuffs, and increasing adoption in technical textiles, sportswear, home furnishings, and industrial fabrics. Strong regulatory emphasis on low-VOC, non-toxic, and eco-certified dyes supports rapid market growth across the U.S. and Canada.

U.S. Textile Dyestuff Market Insight

The U.S. is the largest contributor to North America, driven by strong demand for high-performance dyes in sportswear, medical textiles, automotive fabrics, and industrial applications. Manufacturers are investing in digital textile printing dyes, bio-based dyestuffs, and energy-efficient dyeing solutions. A mature retail sector, innovation in fashion trends, and rising preference for sustainable colored fabrics continue to support market growth.

Canada Textile Dyestuff Market Insight

Canada contributes significantly, supported by rising adoption of eco-friendly reactive and acid dyes across apparel, home textiles, and institutional textile segments. Growing awareness of sustainable fashion, circular textile production, and green dyeing processes is encouraging local manufacturers to expand product offerings. Increased imports of specialty dyes and growth of domestic textile brands enhance regional demand.

Which are the Top Companies in Textile Dyestuff Market?

The textile dyestuff industry is primarily led by well-established companies, including:

- Dow (U.S.)

- BASF SE (Germany)

- Huntsman International LLC (U.S.)

- Evonik Industries AG (Germany)

- SABIC (Saudi Arabia)

- Ineos Group AG (U.K.)

- LANXESS (Germany)

- Exxon Mobil Corporation (U.S.)

- Kronos Incorporated (U.S.)

- Kiri Industries Ltd (India)

- Archroma (Switzerland)

- ALLIED INDUSTRIAL CORP., LTD (Taiwan)

- Organic Dyes and Pigments (U.S.)

- Sumitomo Chemical Co., Ltd. (Japan)

- DayGlo Color Corporation (U.S.)

- Anand International (India)

- SAMCO (India)

- VASU CHEMICALS LLP (India)

What are the Recent Developments in Global Textile Dyestuff Market?

- In April 2024, Archroma and Cotton Inc. renewed their partnership to advance sustainable dye development for the textile sector, reflecting rising demand for eco-friendly colorants driven by consumer sustainability preferences and tightening environmental regulations. This collaboration is expected to reinforce the industry’s shift toward greener dyeing practices

- In April 2024, a Scottish seaweed innovator, AlgiKnit, supported textile manufacturers in transitioning from synthetic dyes to natural seaweed-based alternatives, showcasing growing adoption of bio-derived dyes within the industry. This initiative is poised to accelerate global demand for environmentally responsible dyeing solutions

- In April 2024, Archroma invested USD 750,000 to expand its South Carolina facility, creating six new jobs and strengthening local dyeing capacity to meet rising industry requirements. This expansion is such asly to enhance the company’s regional operational efficiency and long-term competitiveness

- In June 2023, Archroma and COLOURizd entered a partnership to enable eco-friendlier production of sustainable textiles, aiming to deliver high-performance fabrics with minimal environmental footprint. This collaboration is set to advance innovation in sustainable textile manufacturing

- In February 2023, Archroma completed the acquisition of Huntsman Corporation’s Textile Effects business, integrating a global team of over 5,000 employees across 42 countries into a unified sustainability-driven platform. This acquisition is expected to significantly strengthen Archroma’s global presence and technical capabilities

- In February 2023, Archroma integrated Huntsman Corporation’s Textile Effects business into a new combined division named Archroma Textile Effects, consolidating its Brand & Performance Textile Specialties operations under one strategic entity. This organizational integration will further streamline operations and enhance value delivery across global markets

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Textile Dyestuff Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Textile Dyestuff Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Textile Dyestuff Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.