Global Surgical Visualization Products Market

Market Size in USD Billion

USD

3.03 Billion

USD

8.38 Billion

2024

2032

USD

3.03 Billion

USD

8.38 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.03 Billion | |

| USD 8.38 Billion | |

| % | |

|

Surgical Visualization Products Market Size

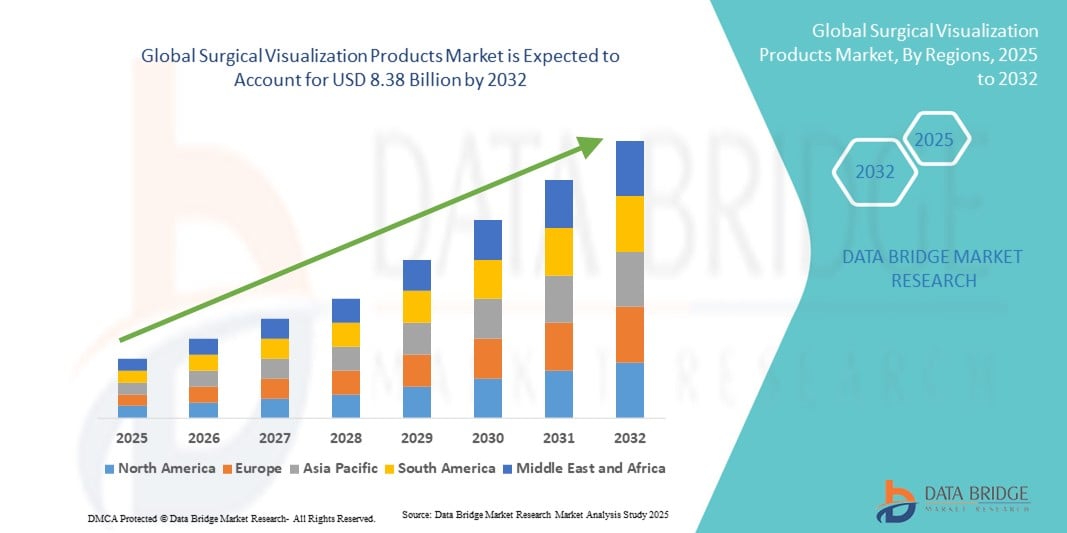

- The global surgical visualization products market size was valued at USD 3.03 billion in 2024 and is expected to reach USD 8.38 billion by 2032, at a CAGR of 13.55% during the forecast period

- The market growth is largely fueled by the increasing adoption of minimally invasive surgeries and the rising demand for advanced visualization systems that provide high-definition imaging, precision, and accuracy during surgeries. These devices enhance the surgeon’s ability to view anatomical structures clearly, which improves patient safety and surgical outcomes

- Furthermore, ongoing technological advancements, such as the integration of 3D visualization, augmented reality, and fluorescence imaging, are establishing surgical visualization products as indispensable tools in modern operating rooms. These innovations, combined with rising investments in healthcare infrastructure and growing demand for complex procedures such as neurosurgery, orthopedic, and cardiovascular surgeries, are accelerating the uptake of surgical visualization solutions, thereby significantly boosting the industry’s growth

Surgical Visualization Products Market Analysis

- Surgical visualization products, which include advanced imaging systems, endoscopic cameras, and display solutions, are becoming increasingly vital in modern operating rooms due to their ability to enhance precision, improve surgical outcomes, and support minimally invasive procedures

- The escalating demand for surgical visualization products is primarily fueled by the rising prevalence of chronic diseases, increasing adoption of minimally invasive surgeries, and continuous advancements in imaging technologies that provide surgeons with greater accuracy and control

- North America dominated the surgical visualization products market with the largest revenue share of 38.5% in 2024, characterized by advanced healthcare infrastructure, high adoption of innovative medical technologies, and strong presence of key industry players, with hospitals and ambulatory surgical centers driving substantial growth in adoption

- Asia-Pacific is expected to be the fastest-growing region in the surgical visualization products market during the forecast period, driven by rapidly expanding healthcare infrastructure, growing medical tourism, rising disposable incomes, and increasing demand for advanced surgical procedures

- The endoscopic camera segment dominated the surgical visualization products market with the largest revenue share of 35.6% in 2024, as these cameras represent the central component in every surgical visualization system

Report Scope and Surgical Visualization Products Market Segmentation

|

Attributes |

Surgical Visualization Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Surgical Visualization Products Market Trends

Technological Advancements Driving Precision in Surgeries

- A significant and accelerating trend in the global surgical visualization products market is the integration of advanced imaging modalities such as 4K, 3D, and fluorescence imaging, which are significantly enhancing surgical precision, visualization of critical structures, and clinical outcomes

- For instance, leading companies have launched 4K ultra-high-definition endoscopic cameras that allow surgeons to observe minute anatomical details with greater clarity, thereby improving decision-making during complex procedures. Similarly, 3D visualization systems are being increasingly adopted in neurosurgery and minimally invasive surgeries to provide depth perception and spatial orientation

- Continuous innovation in surgical microscopes and endoscopic visualization technologies is enabling features such as digital zoom, augmented overlays, and real-time anatomical mapping. For instance, fluorescence-guided imaging systems are being utilized to identify blood flow and tumor margins, supporting more accurate and safe surgical interventions

- The seamless integration of visualization products with surgical navigation platforms and robotic-assisted systems allows surgeons to operate with enhanced accuracy and reduced invasiveness, creating a more connected and technology-driven operating room environment.

- This trend towards more intelligent, high-definition, and integrated visualization platforms is fundamentally reshaping surgical practices. Consequently, companies are focusing on the development of compact, portable, and hybrid visualization systems that can adapt to diverse surgical needs and settings

- The demand for advanced surgical visualization products is growing rapidly across hospitals and ambulatory surgical centers, as healthcare providers increasingly prioritize technologies that improve surgical efficiency, reduce complications, and enhance patient outcomes

Surgical Visualization Products Market Dynamics

Driver

Growing Need Due to Rising Surgical Demand and Technological Advancements

- The increasing prevalence of complex surgical procedures across specialties such as neurosurgery, orthopedics, cardiology, and minimally invasive interventions, coupled with the accelerating adoption of advanced operating room technologies, is a significant driver for the heightened demand for surgical visualization products

- For instance, in April 2024, Olympus Corporation introduced an advanced 4K and fluorescence-guided endoscopic system designed to enhance intraoperative imaging precision. Such product launches and innovations by key players are expected to drive the surgical visualization products industry growth during the forecast period

- As hospitals and surgical centers aim to improve patient safety, clinical outcomes, and procedural efficiency, surgical visualization systems offer advanced features such as ultra-high-definition imaging, 3D visualization, and real-time fluorescence guidance, providing a compelling upgrade over traditional imaging tools

- Furthermore, the growing popularity of minimally invasive surgeries and robotic-assisted procedures is making surgical visualization systems an integral component of modern operating rooms, offering seamless integration with navigation platforms and surgical robots.

- The ability to provide detailed anatomical clarity, enhance surgeon ergonomics, and support faster recovery times for patients are key factors propelling the adoption of surgical visualization products across both developed and emerging markets. The trend toward digital operating rooms and the increasing availability of portable and user-friendly visualization systems further contribute to global market growth

Restraint/Challenge

High Costs and Data Integration Concerns

- Despite strong growth potential, the high upfront cost of advanced surgical visualization systems, including 3D and 4K imaging platforms, remains a significant challenge to broader adoption, particularly in cost-sensitive healthcare settings. Smaller hospitals and clinics often struggle with budget constraints, limiting their ability to invest in premium visualization technologies

- For instance, while leading healthcare centers in developed regions have rapidly adopted advanced imaging platforms, facilities in developing countries face financial hurdles in upgrading to next-generation visualization systems

- Addressing these cost concerns through flexible financing, modular product offerings, and government or institutional funding support is crucial for expanding accessibility. In addition, the integration of surgical visualization systems with other operating room technologies, such as electronic health records and navigation platforms, raises concerns about data compatibility, workflow disruptions, and cybersecurity vulnerabilities

- Companies such as Stryker and Karl Storz are increasingly focusing on offering streamlined integration solutions, enhanced cybersecurity protocols, and software-driven upgrades to reassure healthcare providers and ensure smooth system adoption. However, the perceived premium for these advanced technologies can still hinder widespread deployment, especially in regions with limited healthcare budgets

- Overcoming these challenges through cost optimization, training programs, and collaborative initiatives to expand access in emerging economies will be vital for sustained growth of the surgical visualization products market

Surgical Visualization Products Market Scope

The market is segmented on the basis of product type, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the surgical visualization products market is segmented into endoscopic camera, accessories, light sources, display and monitors, video recorders & processor, camera heads, and video converters. The endoscopic camera segment dominated the market with the largest revenue share of 35.6% in 2024, as these cameras represent the central component in every surgical visualization system. They are widely used in laparoscopy, arthroscopy, urology, and gynecology to provide high-definition, real-time visualization of surgical sites, which is critical for precision in minimally invasive procedures. Growing demand for advanced imaging capabilities such as 4K/8K resolution, improved depth perception, and integration with robotic surgical platforms is significantly driving this segment. In addition, surgeons and hospitals are increasingly preferring high-quality endoscopic cameras due to their ability to reduce error rates and improve patient outcomes, strengthening their market dominance.

The display and monitors segment is anticipated to witness the fastest CAGR of 18.9% from 2025 to 2032, driven by rising demand for enhanced visualization solutions in operating rooms. The adoption of ultra-high-definition (UHD) displays, 3D monitors, and touch-enabled surgical screens allows surgeons to achieve superior precision and accuracy during delicate procedures. Hospitals and ASCs are increasingly investing in integrated digital OR solutions where advanced monitors serve as the central interface for displaying multiple imaging sources simultaneously. The demand is further supported by continuous upgrades in surgical visualization hardware and rising adoption of ergonomic and larger screen sizes for improved surgeon comfort during lengthy procedures.

- By Application

On the basis of application, the surgical visualization products market is segmented into arthroscopy, laparoscopy, ENT endoscopy, obstetrics/gynaecology endoscopy, urology endoscopy, gastroscopy, and others. The laparoscopy segment accounted for the largest revenue share of 32.4% in 2024, owing to its extensive use across various surgical specialties, including bariatrics, colorectal, and gynecology. Laparoscopic visualization products play a vital role in enabling minimally invasive surgeries, which are preferred due to shorter recovery times, reduced hospital stays, and improved patient safety compared to traditional open surgeries. The increasing incidence of obesity and gastrointestinal disorders globally has spurred demand for laparoscopic procedures, boosting the need for advanced visualization systems. Moreover, technological developments such as fluorescence imaging and 3D laparoscopy have further cemented the dominance of this segment.

The ENT endoscopy segment is projected to witness the fastest CAGR of 19.7% from 2025 to 2032, driven by the growing prevalence of ENT disorders such as sinusitis, vocal cord abnormalities, and hearing loss. Compact, portable, and flexible visualization devices designed specifically for ENT applications are gaining traction in both hospital and outpatient clinic settings. Rising pediatric ENT cases, advancements in minimally invasive ENT procedures, and the availability of cost-effective visualization tools are accelerating this segment’s adoption. In addition, rising awareness and increasing accessibility of ENT diagnostic and surgical services in developing regions will contribute to its rapid growth.

- By End User

On the basis of end user, the surgical visualization products market is segmented into hospitals, specialty clinics, diagnostic imaging centres, ambulatory surgical centres, and others. The hospital segment dominated the market with the largest revenue share of 48.9% in 2024, as hospitals serve as the primary hubs for complex and high-volume surgeries requiring advanced visualization equipment. They benefit from higher budgets, centralized procurement processes, and advanced infrastructure that support the adoption of state-of-the-art visualization systems. Hospitals are also more likely to integrate advanced OR technologies such as robotic-assisted systems, AI-powered visualization, and digital image management platforms, further boosting demand. In addition, government initiatives to strengthen healthcare infrastructure and the rising number of multi-specialty hospitals in both developed and emerging markets contribute to their continued dominance.

The ambulatory surgical centres (ASCs) segment is projected to grow at the fastest CAGR of 17.8% from 2025 to 2032, as patients increasingly prefer outpatient settings for minimally invasive procedures. ASCs provide lower treatment costs, faster turnaround, and convenience, making them an attractive alternative to hospitals. Their growing adoption of compact, portable, and cost-efficient surgical visualization products is driving rapid growth in this segment. Furthermore, insurance coverage expansion and increasing investments in same-day surgery facilities are supporting ASC adoption across both developed and developing economies.

- By Distribution Channel

On the basis of distribution channel, the surgical visualization products market is segmented into direct tender and third-party distributors. The direct tender segment held the largest revenue share of 58.3% in 2024, as large hospitals, government healthcare institutions, and multi-specialty centers prefer direct procurement from manufacturers. This model ensures bulk purchasing benefits, transparent pricing, and long-term service and maintenance contracts, making it the most reliable channel for major healthcare providers. Direct tendering also provides access to the latest visualization technologies, which is a key requirement for top-tier hospitals competing on the basis of advanced surgical capabilities.

The third-party distributors segment is expected to record the fastest CAGR of 16.2% from 2025 to 2032, supported by the increasing role of distributors in serving small- and mid-sized healthcare facilities. These distributors provide wider regional access, flexible payment options, and customized solutions to clinics, ASCs, and specialty centers that lack direct ties with large manufacturers. The segment is also benefiting from the growing presence of distributors in emerging economies where healthcare systems are fragmented and localized supply chains play a crucial role in ensuring product availability. In addition, their ability to offer after-sales support and training services further enhances their importance in strengthening market penetration

Surgical Visualization Products Market Regional Analysis

- North America dominated the surgical visualization products market with the largest revenue share of 38.5% in 2024, characterized by advanced healthcare infrastructure, strong adoption of cutting-edge medical technologies, and the presence of leading industry players

- Hospitals, specialty clinics, and ambulatory surgical centers are key contributors to this growth, supported by favorable reimbursement frameworks and continuous investments in modernizing operating rooms

- The region’s demand is further driven by the rising number of minimally invasive procedures, an aging population with higher surgical needs, and the rapid integration of digital and robotic-assisted systems. North America remains at the forefront of adopting 4K/8K visualization, 3D imaging, and fluorescence-guided surgical platforms, reinforcing its leadership position in the market

U.S. Surgical Visualization Products Market Insight

The U.S. surgical visualization products market captured the largest revenue share in 2024 within North America, fueled by extensive investments in healthcare infrastructure, early adoption of innovative visualization technologies, and a high volume of complex surgical procedures. The increasing focus on improving clinical outcomes, reducing surgical errors, and enhancing efficiency in operating rooms is significantly driving demand. In addition, strong research activities, the growing preference for minimally invasive surgeries, and supportive regulatory pathways for advanced medical devices continue to propel the U.S. market forward.

Europe Surgical Visualization Products Market Insight

The Europe surgical visualization products market is projected to witness steady growth throughout the forecast period, driven by government initiatives to strengthen healthcare systems, an aging population requiring advanced surgical care, and stringent standards for patient safety. Increasing adoption of minimally invasive and robotic-assisted surgeries, coupled with ongoing investments in digital operating rooms, is fueling demand. European healthcare providers are also emphasizing sustainability and eco-conscious surgical technologies, further shaping the market dynamics.

U.K. Surgical Visualization Products Market Insight

The U.K. surgical visualization products market is expected to grow at a noteworthy CAGR, supported by the National Health Service (NHS) initiatives to modernize surgical facilities and rising adoption of minimally invasive techniques. Growing concerns regarding patient safety and the need for better visualization in complex surgeries are key factors stimulating demand. The U.K.’s strong focus on digital healthcare integration, including AI and data-driven surgical assistance, is also driving adoption of advanced visualization platforms.

Germany Surgical Visualization Products Market Insight

The Germany surgical visualization products market is anticipated to expand considerably during the forecast period, underpinned by the country’s advanced healthcare system, continuous investments in surgical innovations, and a strong culture of technological adoption. German hospitals are actively integrating next-generation surgical visualization platforms, particularly 3D and fluorescence-guided systems, to enhance surgical precision. Sustainability-focused procurement policies and a strong domestic manufacturing base further support growth in this market.

Asia-Pacific Surgical Visualization Products Market Insight

The Asia-Pacific Surgical Visualization Products market is poised to grow at the fastest CAGR of around 24% during 2025–2032, driven by rapidly expanding healthcare infrastructure, medical tourism, rising disposable incomes, and increasing demand for advanced surgical procedures. Countries such as China, Japan, and India are witnessing significant investments in modernizing operating rooms and adopting advanced visualization technologies. Favorable government initiatives, large patient pools, and increasing preference for minimally invasive surgeries are further accelerating market growth across the region.

Japan Surgical Visualization Products Market Insight

The Japan surgical visualization products market is gaining momentum owing to the country’s advanced technological ecosystem, high surgical procedure volumes, and emphasis on precision-driven healthcare. Demand is being fueled by rapid adoption of robotic-assisted and minimally invasive surgeries, alongside integration of AI and real-time imaging tools. Japan’s aging population is also driving the need for improved surgical outcomes, positioning the country as a leading adopter of next-generation visualization solutions.

China Surgical Visualization Products Market Insight

The China surgical visualization products market accounted for the largest revenue share in Asia-Pacific in 2024, supported by the country’s rapid healthcare infrastructure expansion, government push toward digital healthcare, and increasing availability of cost-effective advanced surgical systems. China’s emergence as a key manufacturing hub for medical devices enhances accessibility and affordability of visualization technologies. Rising surgical procedure volumes, coupled with strong domestic innovation and urbanization-driven healthcare demand, continue to propel market growth in China.

Surgical Visualization Products Market Share

The surgical visualization products industry is primarily led by well-established companies, including:

- Smith + Nephew (U.K.)

- FUJIFILM Asia Pacific Pte. Ltd (Japan)

- Medtronic (Ireland)

- Laborie (Netherlands)

- ACUTRONIC Medical Systems AG (U.S.)

- I.C. LERCHER-Solutions GmbH (Germany)

- Wuzhou Aokace Technology Co., Ltd. (China)

- MEDI-CARE SOLUTIONS S.R.L (Romania)

- Stryker (U.S.)

- Olympus Corporation (U.S.)

- Boston Scientific Corporation (U.S.)

- B. Braun SE (Germany)

- Optomic (Spain)

- SonoScape Medical Corp (U.S.)

- EC21 Inc. (South Korea)

- Xuzhou AKX Electronic Science and Technology Co., Ltd. (China)

- KARL STORZ (Germany)

- ESC Medicams (India)

- HOYA Corporation (Japan)

Latest Developments in Global Surgical Visualization Products Market

- In April 2023, Bausch + Lomb and Heidelberg Engineering introduced SeeLuma, a fully digital 3D heads-up surgical visualization platform. The system was designed to improve ergonomics for surgeons and provide advanced digital imaging capabilities, enhancing precision and comfort during ophthalmic procedures

- In September 2024, Olympus launched VISERA S, an all-in-one imaging platform that combines Narrow Band Imaging (NBI), stroboscopy, and high-definition visualization. The platform was initially introduced in Europe and parts of Asia to support a wide range of surgical specialties with improved clarity and workflow efficiency

- In September 2024, Stryker rolled out its next-generation 1788 Advanced Imaging Platform in India. This platform delivers vibrant 4K imaging and advanced fluorescence visualization, supporting surgeons with clearer anatomical detail and greater surgical accuracy

- In June 2025, GE HealthCare launched the bkActiv S series, a next-generation intraoperative ultrasound system. It was developed for urology, colorectal, and pelvic floor procedures, featuring AI-enabled prostate measurement tools and real-time image optimization to improve surgical guidance

- In May 2024, Beyeonics Vision completed the first commercial installation of the Beyeonics ONE Digital Exoscope. This innovative system is a head-mounted augmented reality device that provides ergonomic benefits and enhanced surgical visualization, offering surgeons a more comfortable and immersive experience during operations

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.